A long/short book can look well-constructed on any given day

Sector diversified. Factor neutral. Reasonable gross and net

But those attributes are measured against the book itself, not against the environment driving it

https://t.co/E0shlQJywJ can help measure these impacts

A portfolio can look right in one environment and wrong in another.

Some positions are driven more by rates, spreads, and growth expectations than by company fundamentals.

That's not a stock problem. It's a visibility problem.

Are you measuring it?

https://t.co/iemAdAVM2p

📊 Nikkei/SPX at 5yr lows—mean reversion setup

💴 CHFJPY cheapest Yen cross—efficient short entry

⚠️ US 5s30s steepener stretched vs macro fair value

Mean reversion or regime change? 🎯

📥 Full PDF at the link below:

https://t.co/PT9drL7b2Q

SPY's GDP sensitivity is at a 5-year high. Markets just flipped regimes again:

➡️Jun '21-Sep '23: Good news = good news

➡️Sep '23-Jul '24: Bad news = good news

➡️Jul '24-now: Good news = good news

📥 Full PDF at the link below.

https://t.co/pt5mX6hl9S

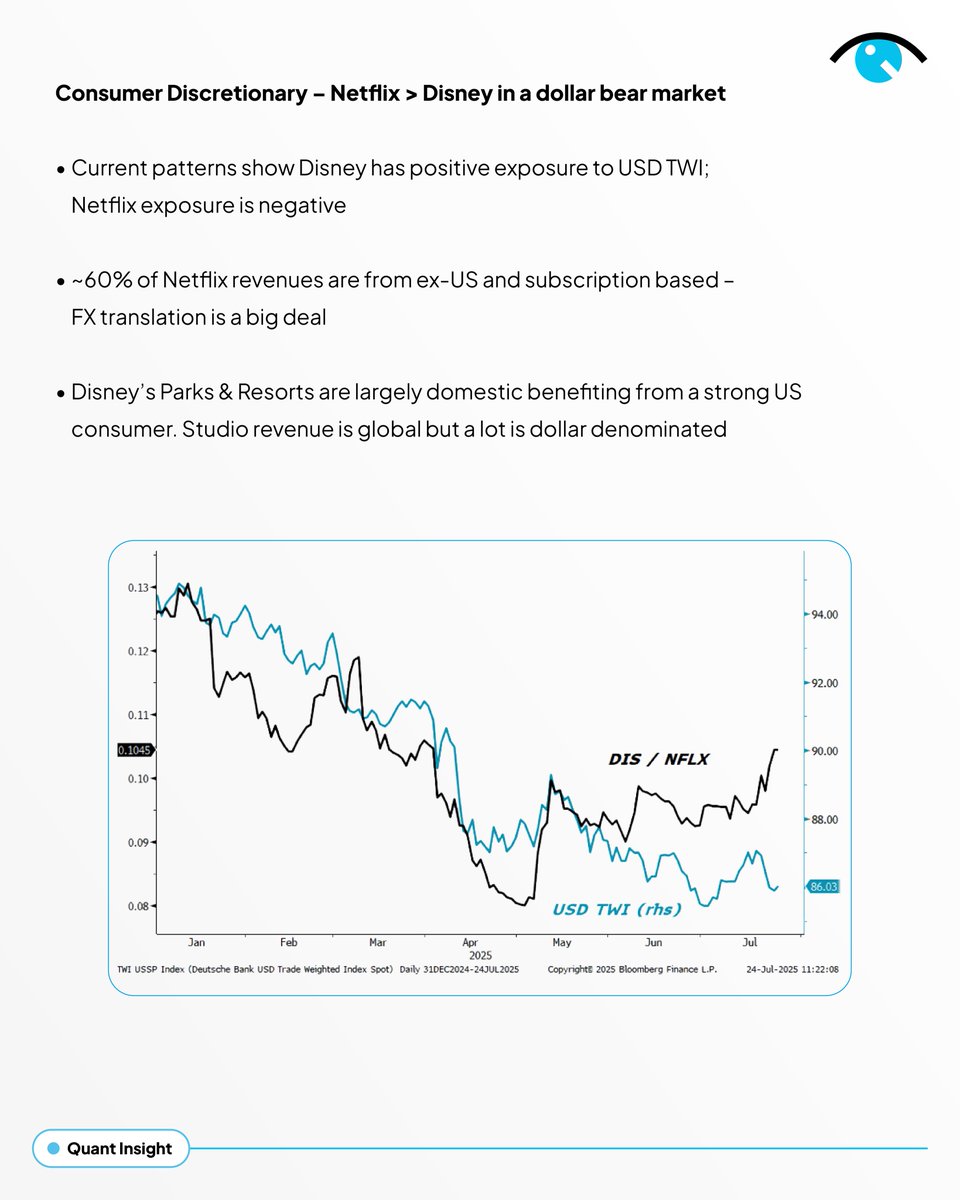

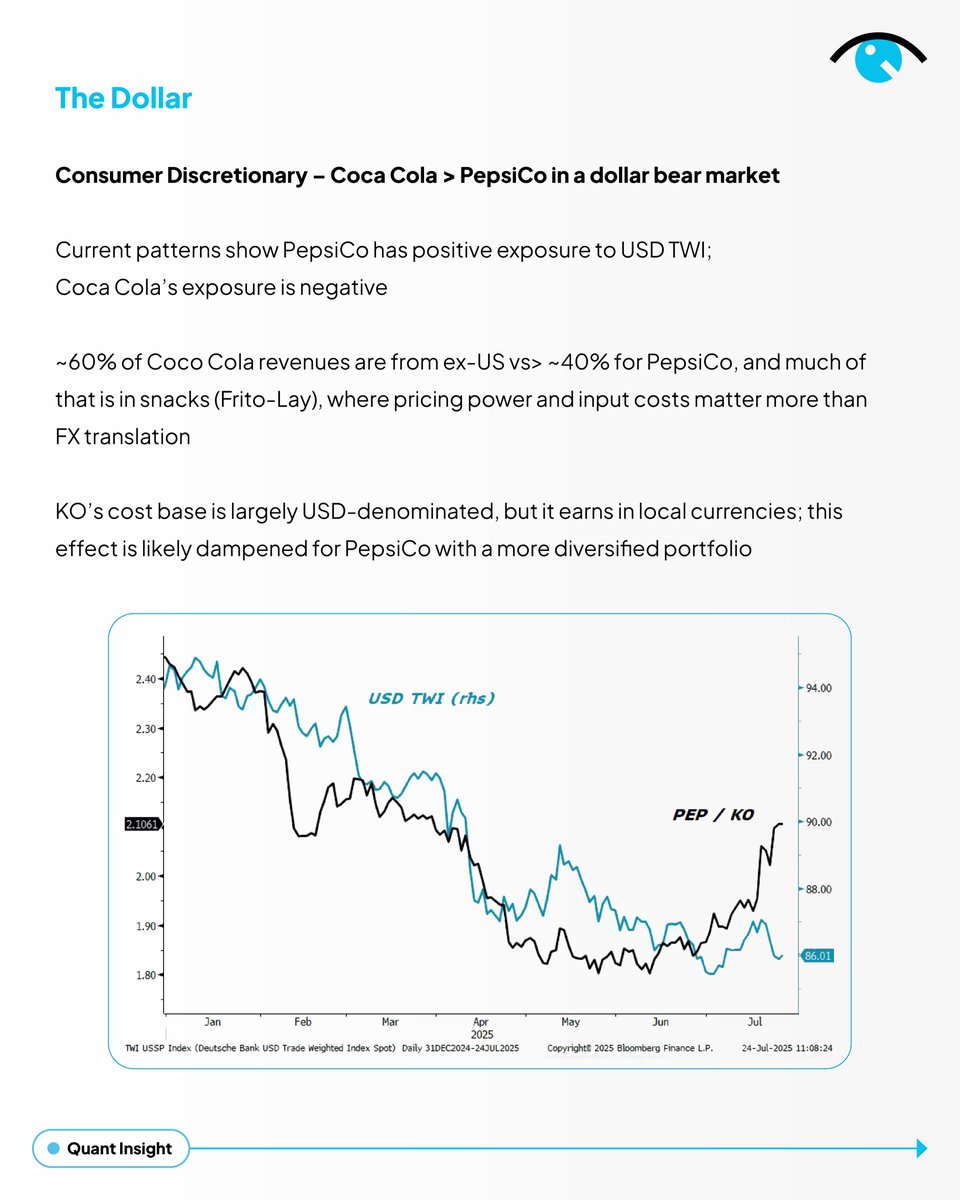

🕵️Hidden FX bet in Consumer Stocks💲

Coke vs Pepsi. Netflix vs Disney.

Looks like stock picking but you also just bet on the Dollar.

PEP & DIS = USD positive exposure

KO & NFLX = USD negative exposure

Quant Insight shows the hidden macro risks in L/S equity trades. 👇

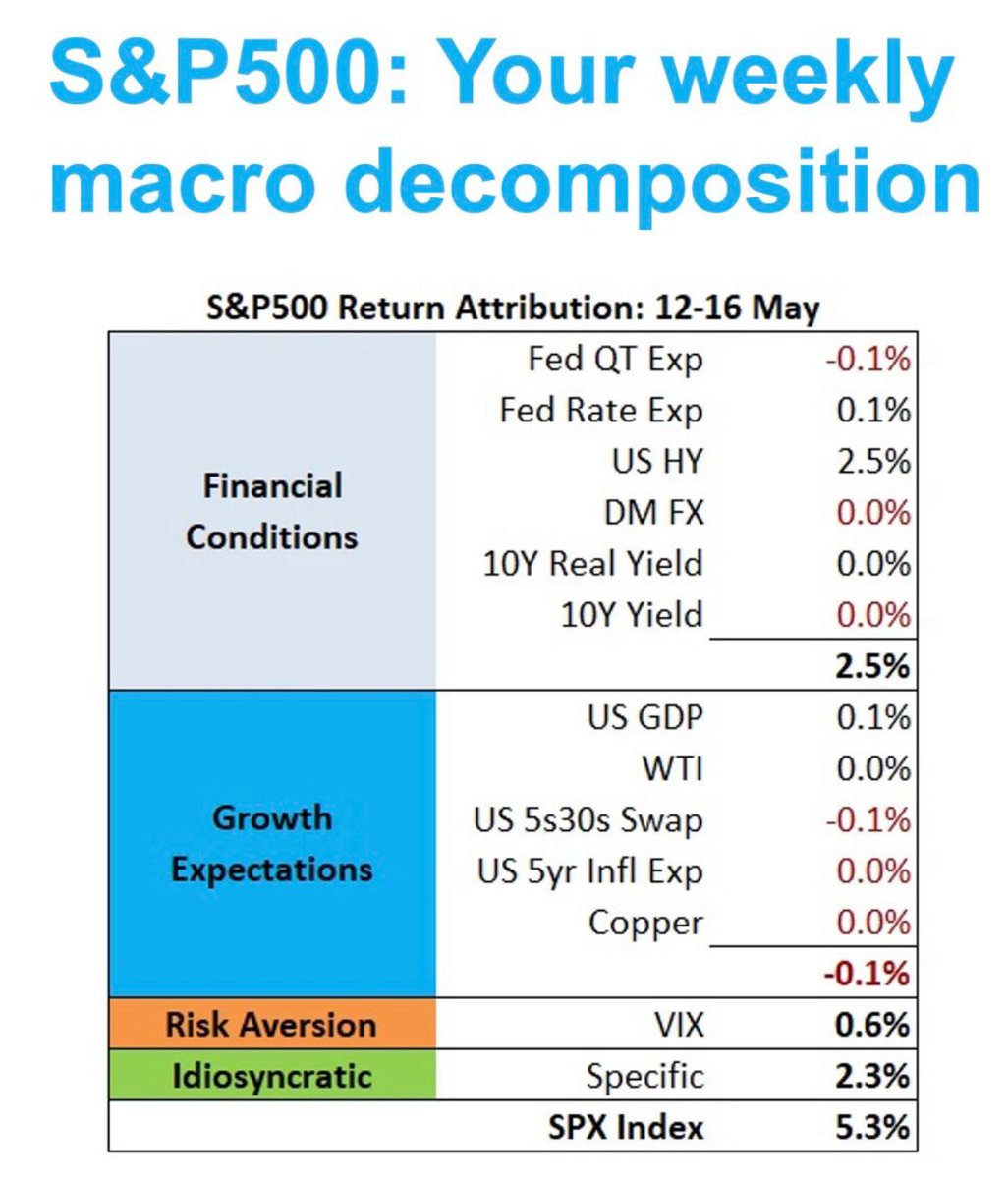

Last weeks #sp500 5.3% move higher was largely macro driven . Markets reduced recession odds. This was captured by the move lower in HY credit spreads

Full breakdown below 👇

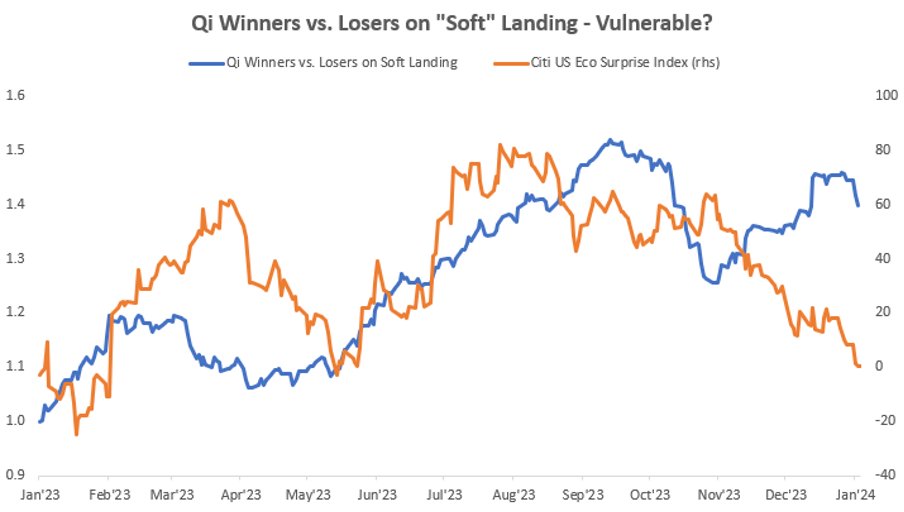

US Soft landing stocks overshooting a bit here.

We screened the SP500 stocks for 30 stocks that benefit most from a soft landing and 30 most vulnerable to a soft landing.

We plotted this against the Citi Econ Surprise Index

Soft landing beneficiaries have overshot

2/ ...going forward. When infl vol is falling as it has been, all you need to know about is the biz cycle/where is the growth. So now regime shift is where inf matters more than growth for risky assets. This probably makes for more range bound / timing of mini cycles markets

1/A broader picture point - deflobalisation and demographics should mean higher inflation volatility over the next few years is a decent base case. This probably means the equity/ bond price correlation will remain flat to positive. So bonds will act less well as a cyclical hedge