GameStop Just Dropped a Nuclear Catalyst yesterday for the Mother of All Short Squeezes Bigger Than 2021:

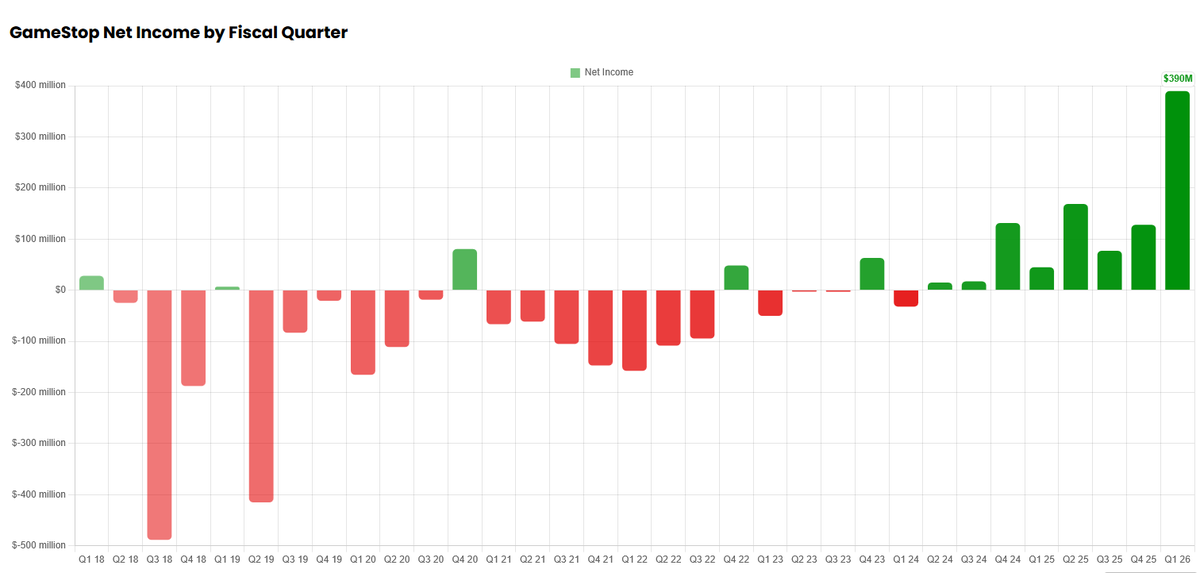

GameStop ($GME) released its Q1 2026 earnings yesterday, and the numbers are historic:

•Record quarterly net income: $389.6 million – the highest in company history.0

•Net sales: $835.3 million, up 14% YoY, led by strong collectibles growth.0

•Operating income: $143.3 million – another all-time high for Q1.

•Massive liquidity: $9.7 billion in cash, marketable securities, digital assets, and related items.

But the real fireworks? The Board unanimously approved a $2 billion discretionary share repurchase program through June 2029, replacing the old 2019 authorization.

Why This Sets Up a Squeeze Far Larger Than 2021?

1. Share Buybacks + Shrinking Float = Rocket Fuel: Buybacks directly reduce the number of shares available in the market. With GME already sitting on a fortress balance sheet and generating real profits, aggressive repurchases can remove tens of millions of shares over time. Fewer shares outstanding means any buying pressure (from shorts covering, retail, or institutions) has an outsized impact on price. In 2021, the squeeze was fueled by extreme short interest on a larger float. Today, buybacks act as a structural tailwind that shorts cannot ignore.

2. Fundamentals Have Flipped the Narrative: 2021 was largely a short-interest + retail momentum story against a turnaround company. Now? GME is profitable, cash-rich, and strategically active (see the eBay acquisition proposal). Record earnings and a buyback signal confidence from management under Ryan Cohen. Shorts betting on bankruptcy or endless dilution are staring at a fundamentally different company – one that can sustain higher valuations and punish holdouts.17

3. Short Interest Still Looms Large While exact current figures fluctuate, GME remains one of the most heavily shorted names on the market with persistent high borrow costs and synthetic share dynamics debated since 2021. Even at lower reported percentages than the 140%+ peak in 2021, the combination of reduced float (via buybacks) and any positive catalyst can create a feedback loop: rising price → margin calls → forced covering → even higher prices.

4. The 2021 Playbook, But With Better Ammo

•Stronger balance sheet = no dilution fears.

•Proven profitability = institutional FOMO potential.

•Retail community more experienced and diamond-handed.

•Options market gamma exposure can still amplify moves explosively.

A $2B buyback authorization isn’t just capital return – it’s a declaration of war on undervaluation and a direct mechanism to tighten supply. If management deploys even a portion at opportune times, it starves the short side while rewarding longs.

This isn’t hopium. It’s math: higher profits + massive cash + aggressive buybacks + unresolved short overhang = asymmetric upside with squeeze potential that dwarfs 2021’s setup.

The bear thesis is dead. GameStop is transforming, and the market is only beginning to price it in.

Load up, hold tight, and buckle up. The squeeze isn’t a meme anymore – it’s balance-sheet backed. 💎🙌

Not financial advice. DYOR. Markets are volatile.

GameStop reports highest quarterly net income in company history of $389.6 million. Highest first quarter operating income in GameStop’s history of $143.3 million. Net sales grew 14% year-over-year, driven by collectibles. Cash, marketable securities, digital assets and related receivables, and collateral pledged for derivative asset of $9.7 billion.

https://t.co/BAu3T6V9w4

Bill is a great guy - JD Vance Vice President

Bill is a good man- Ryan Cohen CEO of GameStop

Bill is the real deal fellas- PP CEO of ThePPShow

Noticing a pattern here. Imagine being on the wrong side of history.