RZ Prime: What Comes After the DeFi Loop

The critique is fair. Most of DeFi's last cycle wasn't moving real capital — it was counting the same deposit three times. You'd put in $100, borrow $80 against it, loop it again, and four protocols would each claim a piece of TVL that never existed as separate capital.

Yield wasn't yield. It was dilution with better branding.

Now that the loop is visible, the numbers don't hold. That's the whole thesis, and it's right.

So the question isn't whether on-chain finance was a mistake. It wasn't. The question is: what does a non-loop mechanism even look like?

RZ Prime is one answer.

It's a reservation dApp on BNB Chain. The model inverts the commit order:

→ You pick a token inside the RZ Ecosystem

→ You pick a time window

→ A smart contract locks the slot at that price

→ No payment. No deposit. No transfer of custody.

At the end of the window, you decide. Pay and receive the tokens, or drop and walk. 3% monthly service fee, charged only at payoff — not at reservation.

Here's what changes when commitment is the last step instead of the first:

There's no pool of capital to loop. The contract holds a slot, not your funds. No TVL to recycle, no collateral to rehypothecate, no receipt token to restake. The surface area that makes the loop possible just isn't there.

Yield isn't part of the pitch, because the mechanism isn't a yield mechanism. RZ Prime isn't trying to pay you to deposit. It's selling you optionality on a price, and it's being transparent about what that optionality costs.

Verifiability without the predictability trap. The rules are fully on-chain. Anyone can read them. But because your capital never enters the system until you actively choose payoff, the "public rules become tradeable edge" dynamic doesn't apply.

Non-custodial. No KYC. Only supports tokens inside the RZ Ecosystem: MGC, RZ Coin, RZUSD, Industrial, Jewelry, Car, RealEstate, Trip, CZW. Operated as a dApp; legal correspondence via Coin Factory AG, Zug, Switzerland.

DeFi's last shape was designed to multiply a number. The next shape is designed to hold a decision open.

That's a different primitive. Worth paying attention to.

https://t.co/iZbeZ3TQ95

DeFi is dead and most of you still don’t understand what it actually was

It was never a financial system. It was a loop designed to manufacture synthetic valuations from minimal capital

Protocols didn’t grow capital, they multiplied how it was counted by turning one deposit into multiple positions

A token gets emitted, you’re paid to deposit it, and that deposit is recorded as TVL. That’s position one.

You borrow stables against that same collateral, deploy them somewhere else, and now that same base capital is supporting a second position on another protocol

Then you take the LP token from that, restake or loop it again, and it gets counted a third time

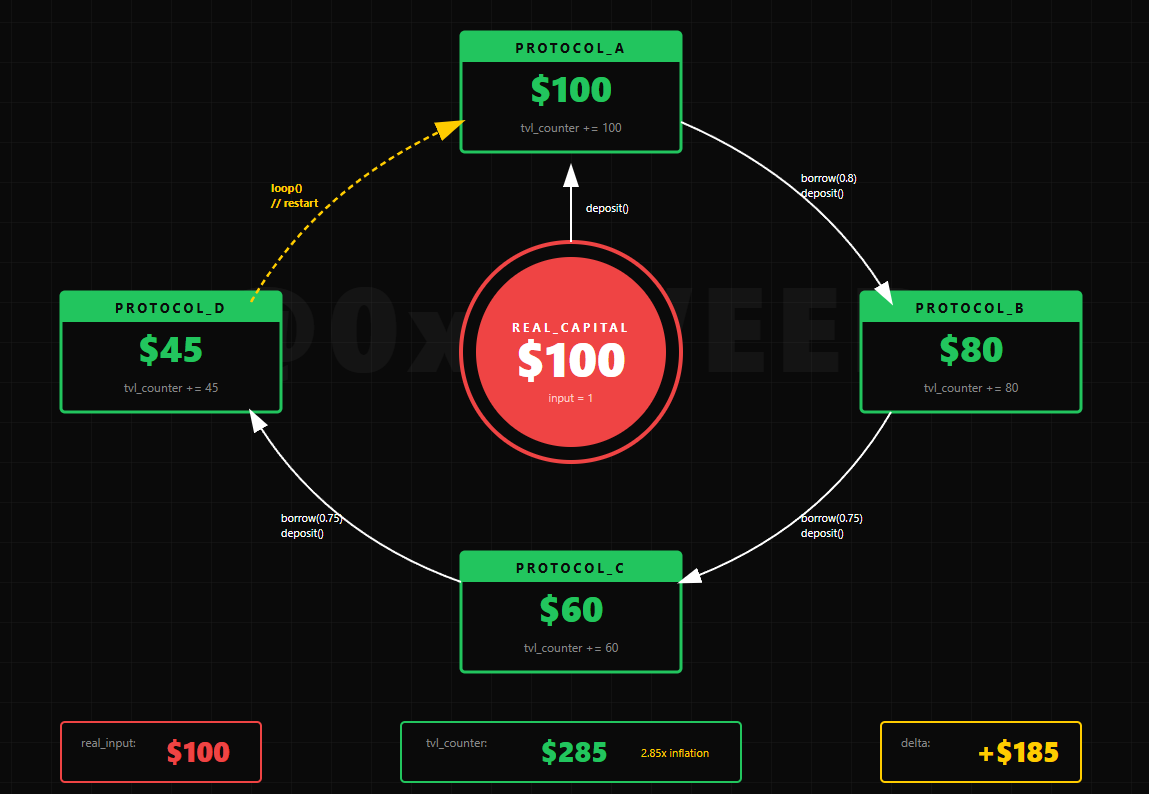

Lets simplify it with $100:

> You deposit $100 into a protocol, that’s your first position and it’s recorded as $100 TVL

> You borrow $80 against that same $100 and deposit it somewhere else, now there’s another $80 being counted

> You borrow $60 against that $80 and deploy it again, now that’s another layer

You take the receipt from that and loop it one more time

On paper you now have $280+ across protocols, but in reality its still the same $100

This is the same illusion as altcoins printing billion dollar market caps on tiny float

A $2B token with 5% circulating isn’t $2B of value, it’s $100M of liquidity marked higher by thin trading

DeFi did the same thing with TVL. Instead of multiplying price across supply, it multiplied the same capital across protocols

TVL became FDV in a different format

Protocols emitted tokens to LPs, counted those tokens as TVL, then counted the incentivized volume as usage

That volume generated fees, fees justified valuation, valuation justified emissions, and the loop continued

No external demand was needed and the system kept feeding itself

Every narrative ran the same structure. Yield farming, LSDs, restaking, points. Different names for the same mechanic

You weren’t earning yield. You were being paid in dilution

At the peak, $200B+ TVL implied capital that never existed. The real base was a fraction of that, looped, leveraged and counted multiple times

Each protocol reported it independently, dashboards aggregated it as if it was additive

That’s how the industry looked massive

This is why altcoin market caps and DeFi TVL broke at the same time

Both were built on internal pricing, thin liquidity, and recycled capital. One inflated valuation through float, the other through collateral loops

Neither represented real economic scale

The fragility came from this exact structure. The hacks weren’t random....

You don’t extract hundreds of millions from systems generating real external cash flow, you extract from systems where the value was already abstract

Strip out token denominated TVL, emission based yield, recycled collateral, and wash volume. What’s left is a small set of protocols actually moving capital

DeFi didn’t fail. It worked exactly as designed. It took limited capital, looped it, marked it higher, and distributed it

Now that the loop is visible, the numbers don’t hold

That’s why it doesn’t bounce. There’s nothing underneath it to support the scale it once claimed

RWA demand is no longer just about assets moving on-chain. It is about new market structures forming around access, timing, and execution. The next layer of adoption will be defined by how users interact with these assets, not just where they trade.

@RWAFoundation_ Tokenized stocks leading inflows shows users want earlier and broader access to real-world value. The next evolution is flexibility: not just what assets are available on-chain, but how people choose to enter them.

RWA holder growth shows that access is expanding beyond institutions. The next step is not only bringing assets on-chain, but giving users more flexible ways to participate, reserve exposure, and make decisions with better timing.

The RWA ecosystem now has more than 833,000 asset holders, adding nearly 90,000 new participants over the past 30 days.

U.S. Treasuries continue to lead the market, followed by commodities and private credit, three asset classes that have become the foundation of institutional adoption onchain.

As more familiar financial products move onchain, participation continues to expand alongside them.

Tokenisation is gradually becoming part of how financial products are issued, accessed, and managed.

The $5.5T RWA forecast is not just about assets moving on-chain. It is about access changing. As more real-world value becomes programmable, users will expect smarter ways to reserve, enter, and decide - not just buy immediately

CZ was right:

"Most AI companies will fail — same as any other new industry."

Crypto is no different.

The projects that survive? They have real utility.

RZPrime's "Reserve Now, Pay Later" model:

→ No upfront payment

→ User decides later: pay OR walk away

→ Smart contract transparency

Most crypto asks for money first.

We let users decide.

That's the difference.

#Crypto #Web3 #ReserveNowPayLater #RZPrime

AI will stay and grow exponentially.

But most AI companies will go bust. There are just too many.

Even survivors will see huge price fluctuations.

There will be new survivor entrants too.

Same as any other new industry, really.

Utility cycles are not built by narratives alone. They are built by products that give users clear actions, transparent rules, and a reason to participate even after the hype cools down

@Vivek4real_ Big price targets get attention. Clear execution gets remembered. In any cycle, users need more than conviction - they need defined rules, transparent terms, and a way to act without emotion taking over.

@CryptoHayes Dreaming big is part of crypto. The mature part is adding structure around the dream: clear rules, defined timing, and decisions users can actually understand before the chart moves.

@ChadSteingraber If the next cycle is utility-led, the focus shifts from simply “owning the asset” to understanding how users interact with it. Clear terms, on-chain logic, and real decision points matter more than ever.

If digital asset rules are delayed, platforms must become even clearer by design.

RZprime defines its role carefully:

not an exchange, not a broker, not a custodian.

Just wallet-based token reservations, smart-contract logic, and user-controlled payoff decisions.

🇺🇸 NEW: Senator Cynthia Lummis warns that if the CLARITY Act does not pass this Congress, meaningful U.S. digital asset legislation may not return until 2030.

Crypto does not just need more hype — it needs clearer rules.

RZprime is built around that same idea:

clear token reservation terms, wallet-based participation, smart-contract execution, and no custody of user funds.

The model should be understandable before the user connects a wallet.

The next window for digital asset legislation after this Congress is likely 2030. Until then, developers remain exposed with no legal protections, and law enforcement remains without the tools to hold bad actors accountable. The Clarity Act solves both.

Regulation is pushing every crypto platform to be clearer about what it is — and what it is not.

RZprime is built as a wallet-based token reservation dApp: no custody, no exchange model, no broker role.

Just smart-contract rules, on-chain actions, and user-controlled payoff decisions.

LATEST: 🇪🇸 Polymarket and Kalshi are now blocked in Spain after regulators launched disciplinary proceedings, claiming they operated without licenses under Spanish gambling law.

Tax clarity matters because it changes how capital plans ahead. The next edge is not just where people hold crypto - it’s how they structure exposure without rushing every market decision.