Those who listen will become MILLIONAIRES.

Once the AI hardware rotation slows down…

power will still need to grow exponentially.

Here’s the AI Power Super cycle that RETIRES you:

1. Layer 1 Fuel & Natural Gas Supply

(the energy feeding the AI boom)

• $EQT - largest U.S. natural gas producer

• $KMI - gas pipelines + infrastructure

• $WMB - natural gas transport + LNG

• $ET - massive U.S. energy network

2. Layer 2 Onsite / Fast Deploy Power

(the real near-term bottleneck solution)

• $BE - Bloom Energy fuel cells

• $GEV - gas turbines + power systems

• $CAT - backup generators

• $CMI - power generation systems

• $KGS - gas compression + mobile power

• $TE - solar + microgrid exposure

3. Layer 3 Grid & Electrical Infrastructure

(the hidden AI winners)

• $ETN - electrical systems

• $PWR - grid buildout

• $VRT - cooling + power management

• $HUBB - transformers + grid equipment

• $NVT - electrical infrastructure

• $EMR - industrial power systems

4. Layer 4 Nuclear & Long-Term Baseload

(the future AI power source)

• $OKLO - advanced nuclear

• $SMR - small modular reactors

• $NNE - portable microreactors

• $CEG - largest U.S. nuclear fleet

• $VST - nuclear + power generation

• $BWXT - reactor components + services

Here is how it breaks down.

AI models get larger. Data centers get bigger.

Energy demand keeps accelerating.

The biggest IPO in history is coming this summer. It's not AI. It's not crypto. It's space.

The space economy has 5 layers. This is the breakdown with all the tickers you need to know before the rest of Wall Street wakes up 👇

🔧 1. MANUFACTURING & SUPPLY

Nothing goes to orbit without someone building it. The defense primes and aerospace manufacturers design, build, and supply every satellite, rocket, and component. L3Harris builds military satellite payloads. Northrop Grumman builds rocket motors and entire spacecraft. Lockheed Martin runs the largest classified space programs on earth. Honeywell supplies avionics. Redwire is the pure play for in orbit manufacturing.

Most of these names have massive non space revenue so the thesis is diluted. Redwire ($RDW) is the purest exposure here with 2025 revenue of $335M and 2026 guidance of $450 to $500M. The rest give you space wrapped in a broader defense portfolio.

Tickers: $LHX $NOC $RTX

🚀 2. ORBITAL LAUNCH

The transportation layer. Launch costs dropped 95% in a decade and that single shift unlocked the entire modern space economy. SpaceX dominates with 60%+ market share and is filing for a $2 trillion IPO this summer. When it lists, every space stock gets repriced overnight.

Rocket Lab is the clear number two. Record $602M revenue in 2025. $2.2B backlog. Neutron medium lift rocket targeting first launch H2 2026. The $816M SDA defense satellite contract proved it's not just a launch company but a vertically integrated space platform.

Tickers: $RKLB $FLY $SPCE

🛰 3. SPACE INFRASTRUCTURE

Once you're in orbit, someone needs to build the platforms, landers, and systems that actually operate there. This is the fastest growing and most volatile segment.

Intuitive Machines is the standout. $943M backlog. 2026 revenue guidance of $900M to $1B, nearly 5x trailing. NASA lunar contracts including the $4.6B Lunar Terrain Vehicle program. BlackSky runs a real time Earth observation constellation with Gen 3 satellites at 35cm resolution and expects positive EBITDA in 2026. This layer has the most asymmetric opportunities because most names are small cap, underfollowed, and growing 50%+.

Tickers: $LUNR $BKSY $SATL

📡 4. SATELLITE SERVICES

Satellites deliver broadband, track ships, monitor crops, predict weather, and connect phones where zero cell coverage exists. This layer has the most direct path to recurring revenue because it runs on long term government and enterprise contracts.

AST SpaceMobile is building space based cellular broadband connecting directly to standard smartphones from orbit. If it scales, it's a paradigm shift. Planet Labs posted record revenue of $308M with a $900M backlog and 98% recurring contract value. KULR provides thermal management for batteries and electronics in space.

Tickers: $ASTS $PL $KULR

🤖 5. COMMUNICATIONS & OPERATIONS

The connective tissue. Every other layer depends on satellite communications networks, data relay, and in orbit logistics to function.

Iridium operates the only constellation covering 100% of Earth's surface with predictable subscription revenue. Globalstar was acquired by Amazon to support Project Kuiper, the Starlink competitor launching in 2026. Spire Global runs a nanosatellite constellation collecting weather, maritime, and aviation data for government and commercial clients.

Tickers: $IRDM $GSAT $SPIR

🎯 THE BIG PICTURE

$626 billion today. $1 trillion by 2034. $1.8 trillion by 2035. SpaceX IPO this summer is the single biggest catalyst the space sector has ever seen. A $2 trillion listing forces Wall Street to reprice every pure play in the ecosystem.

This is not 2021 SPAC hype. Real revenue. Real contracts. Real growth. 5 layers. Most investors only know the rockets. The full space economy is much bigger. And the best opportunities are in the layers nobody is watching.

Photonics value chain in 5 layers. The companies building AI’s optical backbone.

$AXTI – Compound semiconductor substrates. Small, cyclical AI photonics supplier.

$AAOI – Optical transceivers for AI data centers. High risk, high upside.

$LITE – Diversified photonics. Stable, slower growth than AAOI.

$ASML – Only maker of EUV lithography machines. Irreplaceable monopoly.

$ONTO – Semiconductor inspection/metrology tools. Smaller KLAC alternative.

The largest bottleneck in the AI-Infrastructure Buildout is still not priced in yet.

Not Photonics.

Not Memory.

Over 50% of planned Data-centers had to be canceled due to insufficient energy.

These are the layers and stocks that profit the most:

1. Nuclear | SMR's

$OKLO

$CEG

$SMR

$CCJ

2. Energy Storage

$EOSE

$FLNC

$STEM

$NRGV

3. Grid Tech

$BE

$AMSC

$WOLF

$POWL

4. Utilities & IPPs

$VST

$NEE

$ETR

$NRG

This sector is about to go on a generational run, and these sectors will profit the most from it.

When SpaceX goes public, institutional money floods the entire sector. $NASA etf also has SPACE X exposure

$RKLB — Only scaled launch alternative. SpaceX IPO validates the market, RKLB gets the multiple expansion.

$ASTS — Highest-beta space name. Sector ETF inflows hit this first.

$PL — Space data pure-play. IPO headlines bring retail back to Earth imaging.

$FLY — Speculative flows lift all space-adjacent mobility names in a sector re-rating.

$LUNR — Only pure-play Moon stock. Artemis ecosystem gets a spotlight when SpaceX lists.

A look back at the top high growth stocks 👀

$TSM $LITE $MU $SNDK $COHR $ALAB $AAOI $AXTI $CIEN $CRDO $DELL $NBIS $CRWV $VRT $AGX $POWL $MRVL $AVGO $ICHR $FORM

The AI supercycle will last 15 years. We're in year 3.

Most investors are still buying Phase 1 names while the real money is already rotating into Phase 3.

I mapped the entire cycle into 4 phases with the tickers that matter at each stage:

The AI supercycle is the biggest investment theme of our generation. Bigger than mobile. Bigger than cloud. A 15 year structural shift that will reshape every sector of the global economy. Hyperscalers just committed $725 billion in capex for 2026, nearly doubling last year. Microsoft, Google, Amazon, and Meta each spending over $100 billion individually.

This is not speculation. I've mapped the entire supercycle into four phases so you know exactly where we are and where the asymmetric opportunities sit.

🔴 Phase 1: Already Ran (2023 to 2025)

The foundation layer is complete. $AMD ran 78% in 2025, $NVDA 39%, and $INTC just posted a blowout Q1 that sent the Philadelphia Semiconductor Index above 10,000 for the first time. Chips still power every phase but the generational entries are gone and risk/reward has compressed.

- $NVDA, $AMD, $ARM, $INTC, $AVGO, $MU, $GLW

- Semiconductors, Memory & Storage,Photonics/Optics

- Foundation complete. Still growing but priced for it.

🟠 Phase 2: Peak Buildout (2025 to 2027)

The phase most investors just woke up to. $CEG acquired Calpine to become the largest U.S. private power producer at 55 GW. $GEV up over 200% in a year. $VRT co engineering cooling for NVIDIA's Rubin architecture. $GLW up 74% YTD on optical fiber demand. Nuclear SMRs are the breakout with $OKLO, $SMR, and $BWXT positioning to power data centers directly. Still upside but the obvious names have moved.

- $CEG, $GEV, $VRT, $VST, $TLN, $ANET, $GLW, $MOD, $EQIX $OKLO, $SMR, $BWXT, $NNE

- Power/Grid, Cooling, Networking, Nuclear/SMR Peak buildout.

- Nuclear SMRs are the sleeper.

🟡 Phase 3: The Positioning Window (2026 to 2028)

Where AI escapes the data center and enters the physical world. Most will be late. Tesla converting Fremont to Optimus production, $25B capex, mass production targeted H2 2026. Rocket Lab posted record $602M revenue with $1.85B backlog. $LUNR up 47% YTD with $943M in contracts. $KTOS Valkyrie drone selected for the Marine Corps. The window to position is open right now.

- $TSLA, $RKLB, $LUNR, $KTOS, $AVAV, $PATH, $ISRG $MP, $FCX, $ALB, $ASTS

- Robotics/Autonomy, Space/Defense/Drones, Rare Earths

- This is where the asymmetric risk/reward lives.

🟢 Phase 4: Final Frontier (2028+)

The endgame. Microsoft capex $190B. Alphabet $190B. Amazon $200B. Meta $145B. Google Cloud backlog past $460B. They're building the rails for AI software dominance and AGI. Quantum still early but $IONQ and D Wave are laying groundwork. The platforms that control the software layer win the entire supercycle.

- $MSFT, $GOOGL, $AMZN, $META, $ORCL, $IONQ

- AI Software Dominance, AGI Infrastructure Decade long thesis.

- Accumulate on weakness.

💊 Key Takeaway

- Phase 2 is confirmed ($725B hyperscaler capex)

- Phase 3 is where the smart money positions nowRobotics, space, defense, nuclear

- SMR are the 2026 to 2028 trades

- Most will rotate into these names 12 months too late

15 year supercycle. Not a trade. Phase 1 ran. Phase 2 is priced. Phase 3 is where you want to be.

The Space Economy – Przegląd Sektora Kosmicznego (Kwiecień 2026) 🛰️📈

Co macie w portfelu? Na co najbardziej liczycie?

𝗦𝗽𝗮𝗰𝗲 𝗜𝗻𝗳𝗿𝗮𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲 (Infrastruktura) 🏗️

• $RKLB (Rocket Lab) – Systemy wynoszenia i produkcji satelitów. 🚀

• $LUNR (Intuitive Machines) – Logistyka i lądowniki księżycowe. 🌑

• $RDW (Redwire) – Produkcja komponentów w mikrograwitacji. 🛠️

• $FLY (Firefly) – Rakiety nośne średniego udźwigu. 🔥

• $VOYG (Voyager Space) – Budowa komercyjnych stacji orbitalnych. 🛰️

• $YSS (York Space Systems) – Seryjna produkcja platform satelitarnych. 🏭

• $SPAI (Sidus Space) – Oferuje kompleksowe usługi projektowania, produkcji i wsparcia misji satelitarnych w modelu "Space-as-a-Service". 🛰️🛠️

• $SIDU (Sidus Space) – Model „Space-as-a-Service”, od produkcji satelitów po zbieranie danych. 🛰️🛠️

• $MNTS (Momentus) – „Kosmiczny holownik”, zajmuje się transportem satelitów na konkretne orbity. 🚜🌌

• $LLAP (Terran Orbital) – Kluczowy producent małych satelitów (głównie dla wojska i dużych graczy). 🛰️🏭

𝗦𝗮𝘁𝗲𝗹𝗹𝗶𝘁𝗲 𝗖𝗼𝗺𝗺𝘂𝗻𝗶𝗰𝗮𝘁𝗶𝗼𝗻𝘀 (Łączność) 📡

• $ASTS (AST SpaceMobile) – Satelitarna sieć 5G dla zwykłych smartfonów. 📱

• $IRDM (Iridium) – Globalna sieć głosowa i danych M2M. 🌍

• $VSAT (Viasat) – Szerokopasmowy internet dla rynków mobilnych. ✈️

• $SATS (EchoStar) – Usługi satelitarne i technologie broadcastowe. 📺

• $GSAT (Globalstar) – Komunikacja IoT i systemy ratunkowe. 🆘

• $GILT (Gilat Satellite) – Infrastruktura naziemna do obsługi satelitów. 🌐

• $TSAT (Telesat) – Operator zaawansowanych konstelacji LEO/GEO. 📡

𝗦𝗽𝗮𝗰𝗲 𝗜𝗺𝗮𝗴𝗶𝗻𝗴 (Obrazowanie) 📸

• $PL (Planet Labs) – Największa konstelacja monitorująca Ziemię 24/7. 🗺️

• $BKSY (BlackSky) – Wywiad geoprzestrzenny z niskimi opóźnieniami. 👁️

• $SATL (Satellogic) – Masowe mapowanie planety w wysokiej rozdzielczości. 🌎

• $SPIR (Spire Global) – Analityka danych pogodowych i morskich. ⛈️

• $QUBT (Quantum Computing Inc.) – Choć nazwa sugeruje komputery, zajmują się też zaawansowanym teledetekcyjnym obrazowaniem (LiDAR) z orbity. 👁️ quantum

𝗦𝗽𝗲𝗰𝗶𝗮𝗹𝗶𝘁𝘆 𝗠𝗮𝘁𝗲𝗿𝗶𝗮𝗹𝘀 (Materiały specjalistyczne) 🧪

• $ATI (ATI Inc) – Zaawansowane stopy odporne na ekstremalne temperatury. 🦾

• $CRS (Carpenter Tech) – Specjalistyczne stale i proszki do druku 3D. 🖨️

• $MTRN (Materion) – Metale o wysokiej wydajności do optyki satelitarnej. 🔭

• $HXL (Hexcel) – Struktury kompozytowe dla konstrukcji lotniczych. 🧶

• $GLW (Corning) – Ultra-precyzyjne szkło i lustra do teleskopów. 💎

𝗔𝗲𝗿𝗼𝘀𝗽𝗮𝗰𝗲 & 𝗗𝗲𝗳𝗲𝗻𝘀𝗲 (Obrona i lotnictwo) 🛡️

• $LMT (Lockheed Martin) – Potężne systemy obronne i program Orion. ⚔️

• $NOC (Northrop Grumman) – Napędy rakietowe i moduły mieszkalne. 🛰️

• $BA (Boeing) – Kapsuły załogowe i duże platformy satelitarne. 🏢

• $RTX (RTX Corp) – Zaawansowane czujniki i systemy nawigacji. 🧭

• $LHX (L3Harris) – Technologie wywiadowcze i łączność taktyczna. 📻

• $GD (General Dynamics) – Integracja systemów i misje kosmiczne. 🗄️

𝗦𝗽𝗮𝗰𝗲 𝗖𝗼𝗺𝗽𝗼𝗻𝗲𝗻𝘁𝘀 (Podzespoły) ⚙️

• $HEI (Heico) – Specjalistyczna elektronika do trudnych warunków. 🔩

• $TDG (TransDigm) – Krytyczne części mechaniczne i zawory. 🎮

• $PH (Parker Hannifin) – Systemy kontroli płynów i napędy. 💧

• $APH (Amphenol) – Złącza i kable o standardzie kosmicznym. 🔌

• $AME (AMETEK) – Przyrządy pomiarowe i precyzyjne czujniki. 📏

• $HON (Honeywell) – Systemy kontroli lotu i awionika. 🕹️

• $VLD (Velo3D) – Druk 3D dla sektora kosmicznego (ich maszyny tworzą części silników dla SpaceX). 🖨️🔥

#SpaceEconomy #Investing #Stocks #Giełda #Kosmos #SmartKapital001 🌌🛸

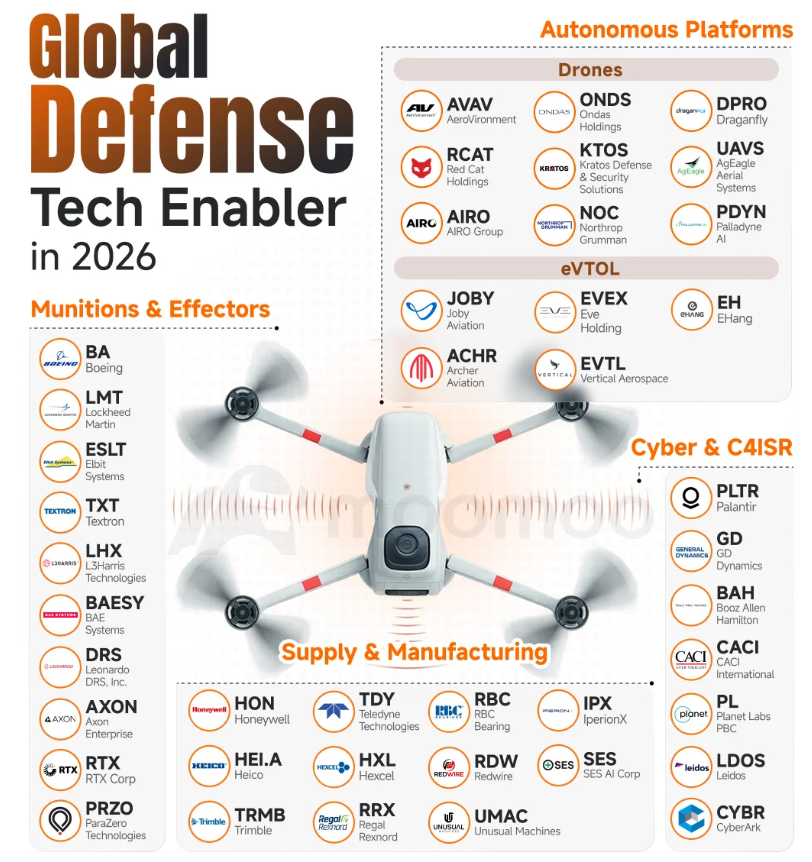

GLOBAL DEFENSE CHEAT SHEET

Defense is about drones, software, communications & the industrial base that makes them scale with these companies enabling that shift:

Drones

• $ONDS builds the secure comm layer drones use to transmit video, data & commands without being jammed or hacked

• $AVAV is the primary U.S. military drone prime operating large, long-endurance ISR & strike platforms embedded across DoD programs

• $KTOS designs attritable unmanned systems built for scale where loss tolerance & cost matter more than perfection

• $RCAT sells short-range tactical drones used by military units, police & emergency responders for real-world ISR

• $DPRO operates on the services layer providing drone operations, training & deployment rather than manufacturing hardware

• $UAVS focuses on drone manufacturing & contract production tied to defense, logistics & government customers

• $NOC integrates autonomous platforms into large-scale defense systems where reliability matters more than speed

eVTOL

• $JOBY leads eVTOL on certification progress, test hours & commercial readiness through early FAA engagement & operating partnerships

• $ACHR designing eVTOL aircraft for defense & government procurement rather than consumer air taxi services

• $EVTL is focused on building eVTOL manufacturing & certification infrastructure to scale production over time

• $EH operates autonomous aerial vehicles at scale in China where regulatory approval allows faster deployment

Decision Software

• $PLTR turns drone & satellite feeds into real-time command decisions

• $GD integrates drones into existing military command-and-control systems

• $BAH moves drone data through defense workflows without human bottlenecks

• $PL provides wide-area satellite imagery that gives context before & after drone missions

Strike Systems

• $AXON supplies non-lethal effectors & real-time capture tools used by law enforcement & domestic security forces.

• $BA builds large-scale military aircraft & strike platforms that deliver munitions across air & space

• $LMT designs advanced weapons systems where precision, stealth & survivability matter most

• $LHX provides sensors & guidance systems that keep munitions accurate in jammed or GPS-denied environments

• $TXT manufactures tactical aircraft & mission systems that carry & deploy effectors in contested environments

• $RTX is a core missile & interceptor prime supplying precision strike and air defense at scale