CICC: SiC to the left, GaN to the right—third-generation semiconductors emerge as the inevitable solution for high-voltage architectures in data centers

> Our estimates suggest that by 2030, a single MW of data center deployment could require approximately 10,000 SiC devices and 21,000 GaN devices, corresponding to per-MW values of $220,000 and $49,000, respectively—indicating considerable market opportunities.

> Between 2026 and 2030, rack-side (white zone) and server-room-side (gray zone) systems are expected to be progressively upgraded to 800V/±400V DC configurations, thereby driving demand for third-generation compound semiconductors. In the short term (1–2 years), transitional architectures led by 800V sidecar units may offer limited upside for SiC demand. However, as the following developments materialize: (1) blade-level voltage step-down or even high-density 800V-to-6V power conversion at the rack side, (2) centralized rectification at the server room side, and (3) implementation of solid-state transformer (SST) solutions, we believe the long-term optionality of SiC/GaN-related companies warrants proper pricing.

> We believe Chinese companies have already established deep positions in the SiC/GaN space, with continuously strengthening competitiveness. Going forward, Chinese firms across the third-generation compound semiconductor value chain stand to benefit substantially from the adoption of high-voltage data center architectures.

> Legacy data center racks average around 7 kW. In comparison, NVIDIA’s Hopper architecture consumes ~40 kW, Blackwell GB300 NVL72 reaches 134–140 kW, Rubin will exceed 200 kW, and future architectures (Kyber in 2027 and Feynman in 2028) are projected to scale to 600 kW and over 1 MW per rack.

The industry is projected to move through four transitional stages to implement 800V DC setups:

Phase 1 (2026/2027): White Space Retrofit with "Sidecar"

Setup: Gray space (facility level) remains untouched. A custom 800V DC side-mounted power cabinet ("Sidecar") is added next to the IT rack to rectify AC to 800V DC locally.

Semiconductor Impact: SiC demand is concentrated in the sidecar's front-end rectification/PFC modules.

SiC Volume: ~1,594 units per MW.

Phase 2 (2027/2028): Native 800V DC Computing (The GaN Inflection Point)

Setup: Centralized low-voltage UPS systems are phased out in favor of distributed rack-level battery backup units (BBUs) and supercapacitors. The 800V DC bus connects directly to the compute blade.

Semiconductor Impact: GaN replaces a massive portion of SiC for the main onboard power step-down stage (Intermediate Bus Converters) to meet strict space and thermal restrictions near the GPU. However, SiC finds rigid demand in high-voltage hot-swap protection and Solid-State Circuit Breakers (SSCBs).

Volume: ~1,755 SiC units per MW; ~10,303 to 10,667 GaN units per MW.

Phase 3 (2028/2029): Centralized Rectifiers in the Gray Space

Setup: Power rectification moves entirely upstream into the gray space. Massive facility-level centralized rectifiers convert grid power to an 800V DC injection backbone distributed throughout the facility.

Navitas GaN Transformation (June 2026): Driven by Navitas' GaNFast integration into NVIDIA’s MGX ecosystem, setups will begin converting 800V directly to 6V, entirely eliminating the traditional 48V intermediate step-down bus.

Volume: SiC surges to ~6,948 units per MW (driven by massive industrial DC distribution, BBUs, and energy storage systems). GaN usage explodes to 20,800–21,600 units per MW.

Phase 4 (Post-2029): The Final Solid-State Transformer (SST) Architecture

Setup: Both the low-voltage transformer and low-voltage rectification stages are completely eliminated. Megawatt-scale Solid-State Transformers (SSTs) directly convert medium-voltage grid AC to 800V DC.

Semiconductor Impact: High-frequency SST operation relies heavily on high-voltage SiC. The gray zone infrastructure captures 54% of the total SiC value chain.

SiC Volume: Skyrockets to ~9,886 units per MW.

Market Value

> As setups transition from Phase 1 to Phase 4, the hardware value of SiC per MW jumps drastically from $10,000–$25,000 to approximately $270,000. This value growth is primarily driven by voltage rating upgrades (moving from 650V to 1200V and 3.3kV devices).

> GaN addressable market value grows from $33k–$33.8k/MW in Phase 2 to $46.5k–$49.1k/MW in Phases 3/4.

Silicon Carbide (SiC) Unit Costs

The unit cost for SiC scales aggressively as devices move from standard rack components to high-voltage, high-density infrastructure:

Non-SST / In-Rack Devices: $2.5 – $3.5 per unit.

UPS / PDU / BESS Peripherals: $3.5 – $5.0 per unit.

800V Transitional / Early SST Stages: $10.0 base price per unit (utilizing mass-production 1200V-class SiC MOSFETs).

Full SST Architectures:

1200V SiC Modules: $15.0 – $20.0 base price per unit.

3.3kV SiC Modules: $50.0 base price per unit (reflecting the severe technical premium for medium-voltage direct conversion).

Gallium Nitride (GaN) Unit Costs

GaN pricing is stratified by application scenario, specifically focusing on its proximity to the high-voltage bus and the GPU itself:

Phase 2 (On-Blade Intermediate Bus Converters / IBC):

High-Voltage IBC (800V --> 50V): $3.8 per unit

(utilizing 650V integrated GaN ICs).

Low-Voltage IBC (50V --> 12V): $2.2 per unit (utilizing

100V-class GaN chiplets).

Phases 3/4 (Centralized & GPU-Proximate):

Navitas PDB Board System: $3.2 per unit.

GPU-Proximate Embedded GaN: $2.2 per unit (scaled AI server order pricing).

The SiC Step-Function Explosion

SiC exhibits massive value elasticity, meaning the financial value grows significantly faster than the physical unit count due to the transition to higher-priced, higher-voltage (1200kV -->3.3kV) devices.

Volume Growth: Scalings jump from 1,594 units/MW (Phase 1) to 9,886 units/MW (Phase 4), representing a strong ~83.73% CAGR.

Value Growth: Financial capture skyrockets from $2,000 – $15,000/MW (Phase 1) to $220,000/MW (Phase 4). This represents a staggering value CAGR of 144.78% to 379.14%.

The GaN High-Volume, Steady-Value Curve

Conversely, GaN follows a high-volume, highly localized deployment strategy. Its volume scales rapidly, but because it operates at lower, more commoditized voltage classes closer to the compute blade, its dollar-value growth is more linear.

Volume Growth: Unit counts double from 10,303 – 10,667 units/MW (Phase 2) to 20,800 – 21,600 units/MW (Phases 3/4), a CAGR of 95% – 110%.

Value Growth: Financial capture shifts from $33,000 – $33,800/MW to $46,560 – $49,120/MW, representing a more modest value CAGR of 38% – 49%.

1/10

Everyone talks about CPO as if the hard part is only the ASIC, lasers, or silicon photonics.

But there is a very physical bottleneck in the middle:

fiber-to-PIC coupling.

How do you plug many optical fibers into a photonic chip with low loss, high density, and enough reliability for AI data centers?

That is what $GLW GlassBridge is trying to address.

Nomura Securities: Global Memory

> Global Data Center (DC) capex is projected to skyrocket from $668 billion in 2024 to $6,127 billion ($6.13 trillion) by 2030.

> The "Big 8" technology firms continue to represent the largest chunk of this spending, starting at $282 billion (42%) in 2024 and expanding to $2,653 billion (43%) by 2030.

> AI DC capex is expected to grow from $206 billion in 2024 to $3,379 billion by 2030, taking a 55% mix within total DC capex by the end of the decade.

> Total global memory revenue is forecasted to experience a massive surge, climbing from $181 billion in 2024 to $2,625 billion by 2030.

> Data centers will become the dominant force in memory consumption. The share of memory revenue coming from data center capex rises from 33% in 2024 to a peak of 56% in 2029 (leveling off slightly to 53% in 2030).

> While AI memory demand grows substantially (from $20B to $517B), memory demand for general-purpose data centers is projected to spike even faster in terms of absolute revenue contribution, moving from $39 billion in 2024 to $881 billion by 2030.

Shift in Hardware Architecture Costs (Memory vs. Logic)

Blackwell: Memory/Logic ratio stands at 200%.

Blackwell Ultra: Rises to 337%.

Rubin: Jumps sharply to 677% as NAND requirements enter the equation at $49,371 million.

Rubin Ultra: Explodes to 1,190%, with total memory TAM reaching $189,977 million compared to a rapidly shrinking relative logic share (only 8%).

1/8

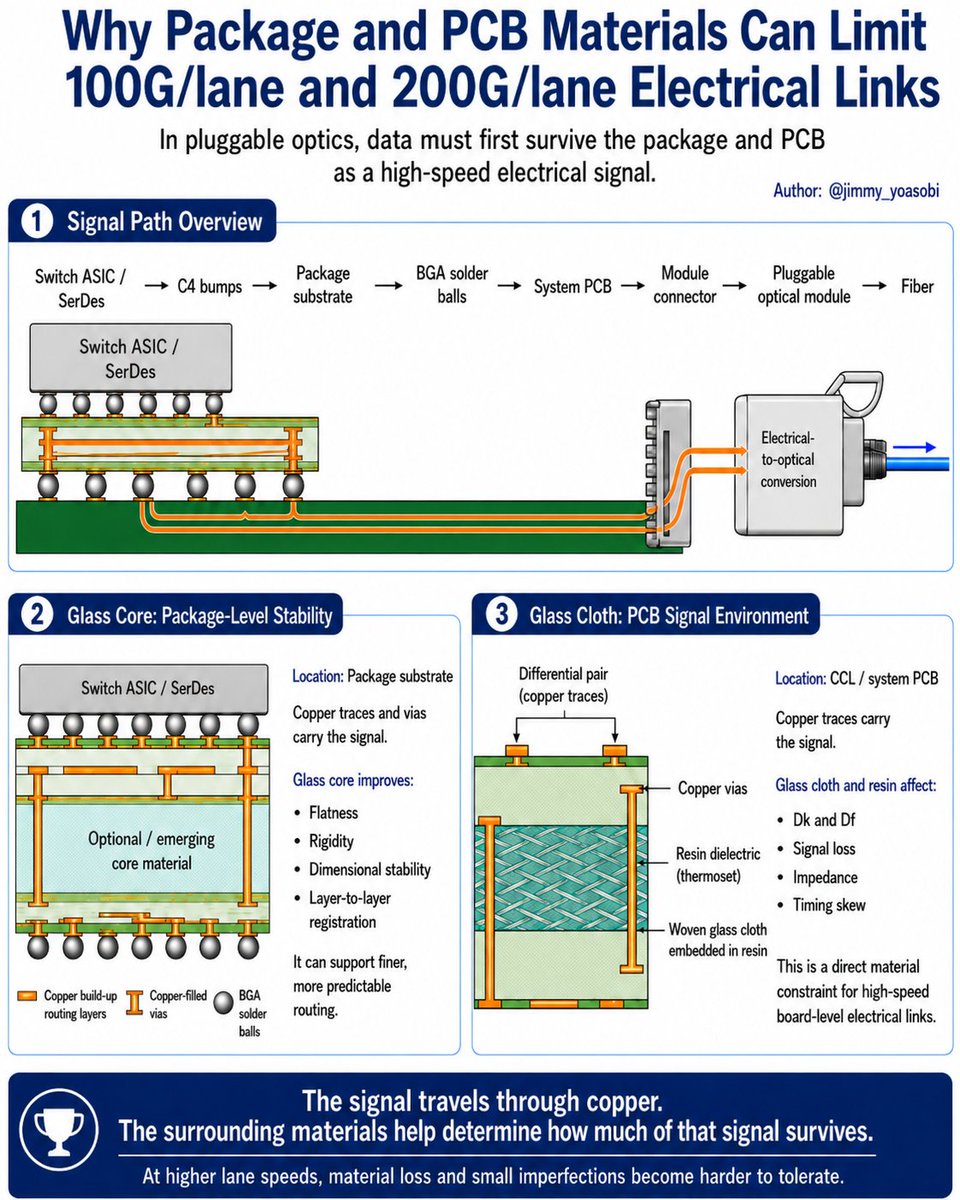

We previously separated two materials that are easy to confuse:

Glass core sits inside the package substrate.

Glass cloth is used inside CCL / PCBs.

But this leaves a more important question:

Why do AI servers care about the materials inside these substrates and boards?

Because before data becomes light,

it usually travels through a high-speed electrical path.