Microcap investor from2001. F.I.R.E achiever from 01 Nov 2021. Stock market 3.0 journey from 22 Jun 2022 towards 15 Aug 2047 goal. No buy/sell recommendations

Thanks a lot @VijayKedia1 sir as following you and implementing your investing mantras in my life has made me financially independent (F.I.R.E) from 01 Nov 2021.

God bless @VijayKedia1 guruji.

"@VijayKedia1" is the only investment "book" i decoded in my investment journey.

A framework to get you to a 50-100 bagger stock.

What it takes:

1. Small/Mid starting market cap - so that there is enough scope for the market cap to expand.

2. Institution worthy but under-owned by institutions - Secular multi year growth catalyst + scope for persistent buying over months and years

3. Neglect (during hold period) - not a mainstream idea - often they don't believe in it till the last one-third phase - ability to hold against consensus is the edge

4. Long Holding period - huge gains are made only if you’re willing to hold the positions for years and decades and have an aversion to selling or booking profits.

5. Drawdown - methodology to ignore 50-90% drawdowns. I don’t say ability to stomach as one can’t really stomach it. It essentially comes down to not even looking at it or avoiding calculating your returns or drawdowns. Vision helps (covered below).

6. Allocation - Just the right starting allocation (typically small enough) that you never feel the pinch even if it goes wrong and you can continue to hold on for as long as it takes

7. Vision - to see the big picture and the larger trend and not be bothered by events in the interim.

This in no way means one should follow this approach - there are many ways to make it work in the markets - but just to understand that this is what it takes.

𝗣. 𝗘. 𝗔𝗻𝗮𝗹𝘆𝘁𝗶𝗰𝘀 𝗟𝘁𝗱 𝗜𝗻𝘃𝗲𝘀𝘁𝗼𝗿 𝗣𝗿𝗲𝘀𝗲𝗻𝘁𝗮𝘁𝗶𝗼𝗻 𝗙𝗬26 🚀:

P. E. Analytics Limited (PropEquity) has released its investor presentation for the financial year ended March 31, 2026, highlighting key financial performance and strategic initiatives. The company has demonstrated consistent growth across its business segments.

𝗞𝗲𝘆 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 (𝗙𝗬26 𝘃𝘀 𝗙𝗬25):

𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗲𝗱:

- 𝗢𝘃𝗲𝗿𝗮𝗹𝗹 𝗥𝗲𝘃𝗲𝗻𝘂𝗲𝘀: Increased by 6% to ₹53.84 Cr from ₹50.69 Cr.

▸ Subscription Business: Grew by 22% to ₹29.01 Cr.

▸ Research & Consulting: Saw a significant jump of 106% to ₹1.41 Cr.

▸ Valuation/ CRM Business: Grew by 18% to ₹16.41 Cr.

▸ Other Income: Increased by 11% to ₹7.02 Cr.

- 𝗣𝗿𝗼𝗳𝗶𝘁 𝗕𝗲𝗳𝗼𝗿𝗲 𝗧𝗮𝘅 (𝗣𝗕𝗧): Rose by 17% to ₹20.98 Cr from ₹17.92 Cr.

𝗦𝘁𝗮𝗻𝗱𝗮𝗹𝗼𝗻𝗲 (𝗣𝗿𝗼𝗽𝗘𝗾𝘂𝗶𝘁𝘆):

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗳𝗿𝗼𝗺 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝘀: Grew by 24% to ₹30.41 Cr from ₹24.49 Cr.

▸ Website Subscriptions: Increased by 22% to ₹29.01 Cr.

▸ Research & Consulting Services: Grew by 106% to ₹1.41 Cr.

- 𝗧𝗼𝘁𝗮𝗹 𝗜𝗻𝗰𝗼𝗺𝗲: Up 22% to ₹37.61 Cr.

- 𝗣𝗿𝗼𝗳𝗶𝘁 𝗕𝗲𝗳𝗼𝗿𝗲 𝗧𝗮𝘅 (𝗣𝗕𝗧): Increased by 32% to ₹21.05 Cr from ₹16.01 Cr.

𝗦𝘂𝗯𝘀𝗶𝗱𝗶𝗮𝗿𝘆 (𝗣𝗿𝗼𝗽𝗘𝗱𝗴𝗲):

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲 𝗳𝗿𝗼𝗺 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝘀: Decreased by 18% to ₹16.41 Cr from ₹19.90 Cr.

- 𝗣𝗿𝗼𝗳𝗶𝘁 𝗕𝗲𝗳𝗼𝗿𝗲 𝗧𝗮𝘅 (𝗣𝗕𝗧): Declined by 110% to ₹(18.25) Lakhs from ₹1.91 Cr.

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁𝘀 & 𝗙𝘂𝗻𝗱𝗿𝗮𝗶𝘀𝗶𝗻𝗴 💰:

- 𝗛𝗗𝗙𝗖 𝗖𝗮𝗽𝗶𝘁𝗮𝗹 𝗜𝗻𝘃𝗲𝘀𝘁𝗺𝗲𝗻𝘁: A term sheet has been signed for strategic investment by HDFC Capital.

▸ Investment in Parent Company (P.E Analytics Ltd.): ~₹8 Cr via Preferential Issue.

▸ Investment in Subsidiary (PropEquity Tech Pvt. Ltd.): ~₹7 Cr via CCPS & Equity Shares.

- 𝗣𝗿𝗼𝗽𝗘𝗾𝘂𝗶𝘁𝘆 𝗔𝗜 𝗙𝘂𝗻𝗱𝗿𝗮𝗶𝘀𝗶𝗻𝗴: Plans to raise an additional ₹50-100 Cr through equity for PropEquity AI (PropEquity Tech Pvt. Ltd.).

▸ Roadshows for fundraising are set to commence soon.

▸ The investment round is validated by HDFC Capital's term sheet, recognizing PropEquity's vision and business model. 🌟

- 𝗣𝗿𝗲-𝗠𝗼𝗻𝗲𝘆 𝗩𝗮𝗹𝘂𝗮𝘁𝗶𝗼𝗻 (𝗣𝗿𝗼𝗽𝗘𝗾𝘂𝗶𝘁𝘆 𝗧𝗲𝗰𝗵 𝗣𝘃𝘁. 𝗟𝘁𝗱.): Band of ₹300 Cr to ₹600 Cr, to be determined on a WAP basis in upcoming funding rounds.

𝗕𝘂𝘀𝗶𝗻𝗲𝘀𝘀 & 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗼𝗻𝘀 𝗨𝗽𝗱𝗮𝘁𝗲 📊 :

- 𝗖𝗹𝗶𝗲𝗻𝘁𝗲𝗹𝗲: Serves 300+ clients with an 80%+ retention rate, including Private Equity Funds, Real Estate Developers, Banks, Financial Institutions, and NBFCs.

- 𝗖𝗼𝘃𝗲𝗿𝗮𝗴𝗲: Operates in 53 cities (14 Tier 1, 39 Tier 2) and has data on over 1.82 Lakh projects & 1.30 Crore units.

- 𝗣𝗿𝗼𝗽𝗘𝗾𝘂𝗶𝘁𝘆 𝗔𝗜: The company is launching its AI platform within the year, backed by HDFC Capital's validation. 🤖

𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗖𝗼𝗺𝗺𝗲𝗻𝘁𝗮𝗿𝘆:

Mr. Samir Jasuja, MD & CEO, stated, "PropEquity has been a leader in real estate data and analytics, consistently driving innovation to empower data-backed decision-making."

📊 P. E. ANALYTICS LTD | 🏷️ Investor Presentation

🌐 Details: https://t.co/eHmSlPPgxs

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 https://t.co/PdwQDWbq5q

🧵 Sakar Healthcare: Oncology-led transformation explained (Q3 FY26)

1️⃣ Business Model — 🧬

Sakar Healthcare operates a diversified pharma model:

• CDMO / CMO services for global & Indian pharma

• Own brand exports across 60+ countries

• Licensing & technology transfer of developed dossiers

This ensures recurring revenues + higher-margin growth

Unihealth FY27E Snapshot

₹248 Cr Revenue

₹60 Cr PAT

~₹31 Cr Attributable PAT

Uganda drives profitability, while India ops continue to scale.

Key triggers to watch:

• Nashik hospital commissioning + Navi Mumbai scale-up

• Potential mainboard migration

• Africa expansion

• Margin sustainability

• Reduction in working capital days (India mix)

• Hospital peers trading at ~40–50x PE

Valuation angle:

If Unihealth delivers, even a partial rerating vs hospital peers could significantly reprice the stock.

#UnihealthHospitals #Unihealth

Note: These are my estimates based on concalls & promoter commentary. Actual numbers may vary.

Shri Ahimsa Naturals Ltd

#SHRIAHIMSA

Title: 𝐄𝐱𝐭𝐫𝐚𝐜𝐭𝐢𝐧𝐠 𝐂𝐫𝐮𝐝𝐞 𝐂𝐚𝐟𝐟𝐞𝐢𝐧𝐞 𝐟𝐫𝐨𝐦 𝐭𝐞𝐚 𝐚𝐧𝐝 𝐜𝐨𝐟𝐟𝐞𝐞 𝐰𝐚𝐬𝐭𝐞!

🔹The company’s main products are Caffeine Anhydrous Natural and Green Coffee Bean Extract (GCBE), used in food & beverage, nutraceuticals, cosmetics, and pharmaceuticals. It also offers herbal extracts like Senna Leaf, Bacopa Monnieri, and Curcumin, which are currently outsourced.

🔹The company pioneered a “waste to value” philosophy, developing technology to extract crude caffeine from tea and coffee waste. It is currently exploring ways to monetize this waste.

🔹Demand: Global caffeine anhydrous market projected to reach USD 881.5M by 2030 (CAGR 6.9%). The company’s products—Caffeine Anhydrous Natural and GCBE—are well-positioned to benefit.

🔹Capex: A greenfield facility in Sawarda, Jaipur, will expand Natural Caffeine capacity (270→700 MTPA), GCBE (200→300 MTPA), and bring herbal extracts in-house. This aims to boost sales, export competitiveness, and R&D efficiency.

🔹Advantage : The new facility in Sawarda is being built to meet rigorous global standards, including US FDA guidelines. The company maintains strict quality control measures, which have resulted in low process loss (2-3%) compared to the industry average (10%). This efficiency is a significant competitive

👉My takeaway: overall, it’s an export-oriented business. Once the US tariff issue is resolved, this could become very interesting. Added to watchlist—tracking closely. Share your views.

Note: This is an SME, newly listed company, DYODD.

Disc: No buy

#SME#PurpleUnitedSales#PurpleUnited#PurpleUted

Purple United Sales H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️No specific topline number was provided, but emphasis on scaling retail and e-commerce

💠Targeting 500-600 daily orders on D2C website, scaling to 2,000; H1-H2 split approximately 40:60

💠Targeting a retail revenue contribution of around 50% for FY26 / ~60% FY27 (store maturation, higher ASPs in H2 due to winter and festival seasons)

💠Plans to touch 100 stores by end-FY26 through internal accruals

💠Ongoing fundraise; if succeeds, will support further growth, with 60-70% allocated to capex (new stores), 30% to working capital, and the rest to marketing/technology/general corporate purposes.

▫️Margins are expected to remain broadly in the same range as H1FY26

💠Short-term pressures from hiring, marketing spends, and ESOP costs (potentially 25-50 bps impact), but long-term benefits from scale, vendor pricing, and retail mix shift

💠No major dip expected despite new store openings (7-8 per month)

💠Footwear margins similar to apparel; overall focus on improving per-script sales without margin dilution

👉Projects and pipeline:

▫️32 Letters of Intent already signed for new stores, with 15-20 additional in the project/development stage

💠Signing new Letters of Intent every week or 10 days. Business development) retail ops, and planning teams in place to support execution

💠Expansion in Punjab (due to high disposable income, NRI influence, lower rentals, and high-street malls)

▫️Recent openings include Mumbai (Orbit: ~7 lakhs/month GMV; Vasai: ~3.5 lakhs in 15 days), Bhopal, Mohali, Indore (focus on standalone properties in new-age colonies)

💠Total stores at 86 as of call

▫️Pipeline:

💠 Aim for 100+ more stores starting FY27 (7-8/month pace)

💠Focus on Pune, Bangalore, Hyderabad, and omnichannel (using stores as e-commerce distribution points)

💠Exploring FOCO model (already tested 6-7 stores) for faster scaling

💠Long-term vision: 500-600 stores by FY30 possible with growth capital visibility. International inquiries (e.g., Gulf/Saudi from Riyadh participation), but no short-term plans; potential maturation in FY27+

👉 Others :

▫️E-commerce Strategy: Revamped website launched 15-20 days ago (contemporary look, developed over 4-5 months)

💠Shift from liquidation channel to never-out-of-stock styles with algorithm focus

💠Targeting 400-500 daily orders initially (conservative; potential for 2,000)

💠15-member team; new hires for planning/scheduling

💠Marketplace focus on fashion portals like Myntra (premium positioning); Amazon/Flipkart as secondary/liquidation

💠Promoting via SEO, Google/Facebook ads, cross-selling with retail (e.g., CRM integration, gift vouchers)

💠Investor Feedback: Increase variety (apparels low on marketplaces; aim for 15-20 options/category), add child models/AI-generated images for appeal

▫️Regional/Operational Insights: Punjab growth due to NRI economies, high-street malls, decent sales/rentals

💠Competition in 5-14 age group (gap filled by extensions like Allen Solly Kids, US Polo Kids; no one-stop shop)

💠Mature stores: 10 lakhs/month GMV (1.2cr annualized); Same Store Growth discrepancies due to regional variations (e.g., 12-24 month cohort drop from 9 lakhs to 6.98 lakhs)

💠Receivables improved to 120-180 days (from 210); targeting 90-120 with retail shift

💠Dead stock minimized via core/seasonal/fashion inventory split, reviews, incentives, factory outlets (1 per 5 stores), and planning software exploration

▫️Product/Financial Notes:

💠Footwear (10% contribution) focuses on premium (e.g., ballerinas/sports shoes; ASP INR 500-3,500); helps per-script sales, less competition post-BIS policies

💠Apparel ASP ~INR 900-1,000 overall. Repeat customers at 26% (industry norm for premium kids; higher transaction of 4-6 pieces/visit)

💠Working capital focus: Reduce reliance on high-WC channels (distributors); positive cash flows in H1

💠Fundraise timeline: 3-5 months (approvals needed)

💠Tech investments: Exploring merchandise planning/predictive software; current ERP with BI tools; potential SAP migration later

💠Sales per sq ft: ~900 for mature stores (potential 1,400-1,600)

💠Celebrity Addition: Might be pursued (maybe yes, maybe not) due to mixed reviews for benefits, potentially allocating budget for it after the next fundraise, acknowledging that it comes with a cost

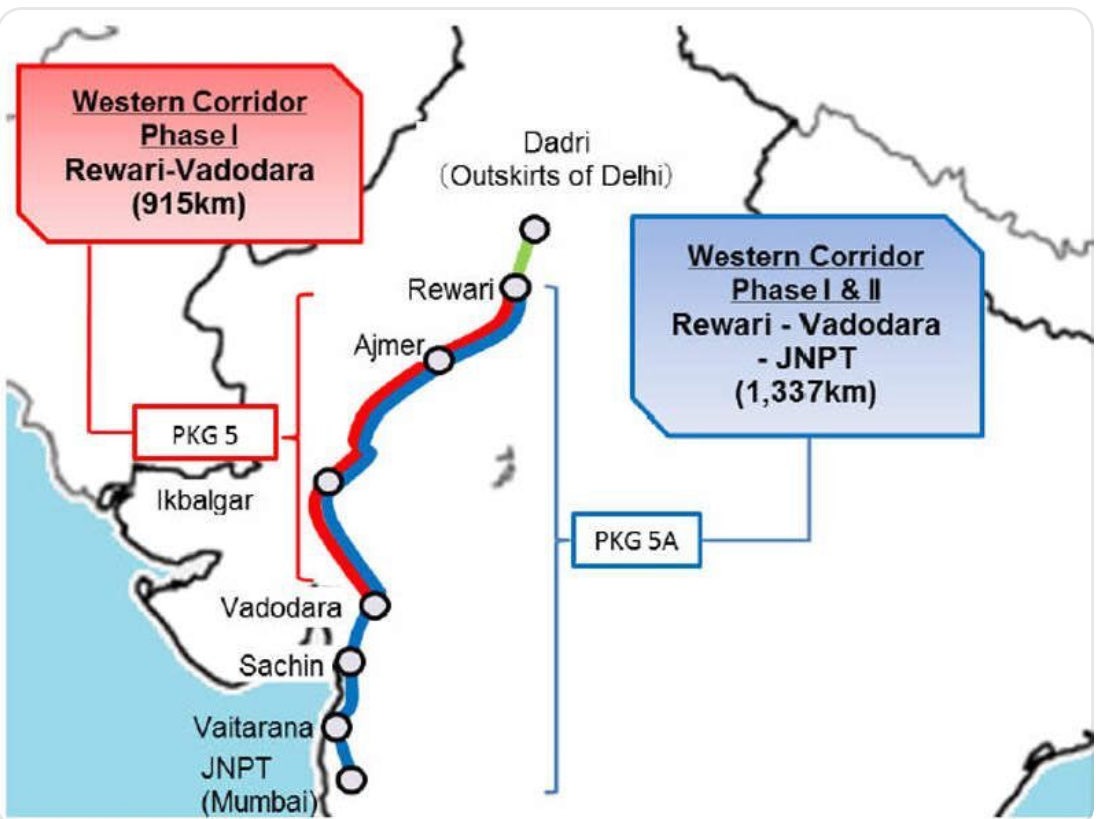

🚨 The Final Stretch is Complete – Western Dedicated Freight Corridor (DFC) 🇮🇳

With the Rewari–JNPT corridor now fully operational, India’s logistics backbone just transformed.

At Kalyani Cast Tech, we are strategically positioned at BOTH ends:

📍 Existing presence near North corridor

📍 Upcoming facility at Kandla Port, Gujarat

This puts us right at the heart of India’s fastest freight highway.

🚛 Game Changer: Double Stack Containers

Built for double-stack container trains running at ~100 km/hr, enabling:

✔️ Higher load efficiency

✔️ Faster turnaround

✔️ Lower logistics cost per unit

⏱️ Transit time revolution:

From 48+ hours → just 15–20 hours

🔩 Our Opportunity:

Kalyani Cast Tech is uniquely positioned to:

• Drive end-to-end freight movement using our containers & wagon solutions

• Enable seamless port-to-hinterland connectivity

• Capture value across the entire logistics chain

This is not just infrastructure.

This is India’s logistics leap — and we are at the center of it.

#KalyaniCastTech #DFC #LogisticsRevolution #DoubleStack #FreightCorridor #MakeInIndia #InfraGrowth #SupplyChain #IndiaGrowthStory #MultimodalLogistics #PortToPort #RailLogistics #InvestI