$MMTLP Good morning, @FINRA

It was more of a burden to scour the internet to find “threats from shareholders” on social media (ignoring the 100’s of thousands of posts asking for transparency and accountability) than it is for you to provide data you are responsible for collecting and overseeing.

What was your process for validating that these people are shareholders? If you performed any validation at ALL, it was infinitely more burdensome than it is turn over the data and communications you already maintain.

Ironically, the data you refuse to turn over to would aid your shareholder validation process. 🤓

$26,000,000 GONE IN 60 SECONDS!!

BLOCKBUSTER INFO… So imagine you own approx 21000 shares of $MMTLP

You have limit stop orders out GTC.

You see $MMTLP on level 2 showing prices $1000 $2000 pre market 12/9

You tell @etrade cancel your sells. They come back and say too late. WOW they actually send a Help Desk report saying SORRY ITS TOO LATE TO CANCEL. Your orders have already been executed. The Prints as shown below say you are now $26M richer. Wow. And then Poof your trades are cancelled and your money is GONE. There were shares printed after 12/8 and someone shit their pants. Read it and weep. I got more. @CGasparino@busybrands@KarmaCollects@BasileEsq@johnbrda@RepRalphNorman@jtsmith24

THROWBACK🚨 UNDER GARY GENSLER’S LEADERSHIP, THE SEC HAS BEEN CAUGHT COLLUDING WITH WALL STREET

FOIA records reveal a broker trade group pushed the SEC to deny an S-1 due to unaccounted-for shares, known as naked shorts ⬇️ $MMTLP @annvandersteel

💥 TradeStation admits they oversold MMTLP

💥 Finra lied about 2.65 million open "short shares"

💥 SEC lied to congress about involvement.

💥Finra created a fake ombudsman.

💥FOIA docs show collusion between SEC and FIF. 👇

💥Finra Fraud

BREAKING🚨 ANN VANDERSTEEL WILL HOLD A PRESS CONFERENCE IN FRONT OF THE SEC ON JAN 12TH DEMANDING TRANSPARENCY FOR RETAIL INVESTORS

- Ann urges members of Congress to stand with her in demanding accountability for the SEC’s failure to protect retail investors $MMTLP $GME $AMC

Catclaw is the size of half a small orange and is designed to be installed in its thousands along kerbs and pavements as a parking prevention measure

https://t.co/YuJVijxKSm

I’ve had many detractors try to slow me down and this group has only lifted everybody up because they know they’re right and when you know you’re right, you don’t slow down. Even when you’re going through hell you just keep going.

Just ask.@GenFlynn he knows exactly what we are talking about. The weaponization of government against we the people.

Wow, this is not a good cliff of 2025 for the self-regulating agencies, brokers, and sleight of hand politicians who were involved. #MMTLP is an erupting volcano now. This is why you never stop when you know you're right.

12. Were the right number of Next Bridge shares distributed in connection with the corporate action?

Yes, the “right” number of NBH shares were distributed. However, FINRA fails to make the distinction (implying indistinguishability) between the distributed number of issued shares of both Meta Materials Series A Preferred Shares [MMTLP] and Next Bridge Hydrocarbons ([NBH), and the delivery of ALL shares to existing open long positions held by beneficial owners, in street name, under bulk certificates at FINRA’s broker/dealers. Discrepancies in issued shares and open long positions hide behind the veil of bulk certificates. In both FINRA FAQs, FINRA acknowledges that open short positions and open naked short positions exist in MMTLP. Every share of MMTLP sold short has a buyer with a corresponding long position, therefore it is factually incorrect to assert that ALL shareholders of MMTLP received their NBH shares, and simultaneously acknowledge open short/naked short positions. If there are existing open short/naked short positions in MMTLP, then there are more open long positions in MMTLP than issued shares of NBH. Furthermore, FINRA suggests only issuers can issue shares, which fails to recognize that market makers create short/naked short shares.

FINRA cannot claim enough shares were issued and identify a short position on a non-tradable security at the same time. Investors have experienced differences in identifiers held at each broker since the FINRA U3 halt. It is impossible to identify a short/long/counterfeit stock unless the exact allocation of “sold shares” from each broker is audited in comparison to the original allotment of shares issued by NBH.

THIS X SPACE SHOULD HAVE OVER 500 GOING REMINDERS 🚨🚨

SET A REMINDER BELOW $MMTLP $AMC $GME $GNS $QNTM $BYND $OPEN

LETS EXPOSE THE SEC & FINRA ⬇️⬇️ https://t.co/awSdVscXtE

CALLING ALL GAMESTOPPERS

The #MMTLP community has been fleeced and tens of thousands of lives ruined by investment banks, regulatory agencies, and potentially corrupt politicians.

We need to increase the army to help we the people fight back against and take down the RICO syndicate that is responsible.

THIS ENDS WHEN WE SAY IT ENDS.

$MMTLP The TD Ameritrade (TDA) message from October 14, 2021, explicitly states: "Currently, there is only one market destination accepting orders for MMTLP, which is GTS OTC." (IMAGE 1)

This confirms that on the day immediately preceding the first reported short interest, GTS was the only entity in the market accepting orders for MMTLP through TDA's platform (and TDA implies other brokers/market destinations were not connected).

The FINRA data shows that the first reported Short Interest (SI) Volume for MMTLP was on October 15, 2021, with a volume of 14,394,345 shares. (IMAGE 2)

This large initial short position appeared immediately after GTS was identified as the sole accepting market destination.

GTS was in a unique position to facilitate the short sale of these 14.4 million shares. Since short sales must be executed through a market maker/destination, the coincidence of GTS being the only acceptor and the large initial short volume on the following day strongly suggests GTS played a direct role in processing or internalizing these short sale orders.

But MMTLP shares were issued 1-for-1 only to existing TRCH investors via a reverse merger and there shouldn't have been shares locateable to facilitate shorting.

In a legal short sale, a broker must "locate" a share before the sale. The share is then borrowed and sold.

The existence of a 14.4 million share short position, particularly in a security with a severely restricted and finite float (issued 1:1 via a corporate action), suggests a massive failure in the locate and/or settlement process. GTS, as the primary/sole market destination, would have been the entity responsible for ensuring the locate requirements were met before facilitating the sale orders. The size of the short interest relative to the known float raises serious questions about whether:

GTS was able to locate this many shares.

The shares were sold without a proper locate (Counterfeit/Naked Short Selling).

GTS was the internal counterparty to many of these transactions.

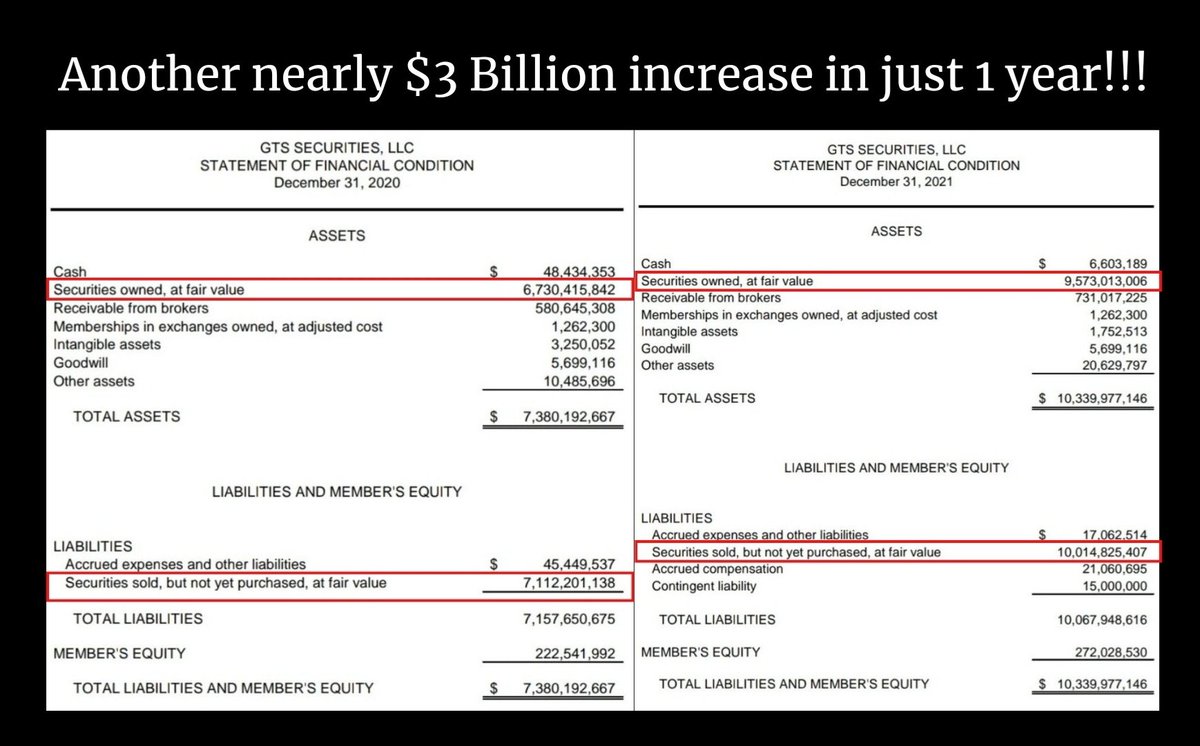

Images 3 & 4 reflect that this coincides with the financials of GTS in the relevant time period. @SECPaulSAtkins@palikaras

![bleedblue18's tweet photo. 12. Were the right number of Next Bridge shares distributed in connection with the corporate action?

Yes, the “right” number of NBH shares were distributed. However, FINRA fails to make the distinction (implying indistinguishability) between the distributed number of issued shares of both Meta Materials Series A Preferred Shares [MMTLP] and Next Bridge Hydrocarbons ([NBH), and the delivery of ALL shares to existing open long positions held by beneficial owners, in street name, under bulk certificates at FINRA’s broker/dealers. Discrepancies in issued shares and open long positions hide behind the veil of bulk certificates. In both FINRA FAQs, FINRA acknowledges that open short positions and open naked short positions exist in MMTLP. Every share of MMTLP sold short has a buyer with a corresponding long position, therefore it is factually incorrect to assert that ALL shareholders of MMTLP received their NBH shares, and simultaneously acknowledge open short/naked short positions. If there are existing open short/naked short positions in MMTLP, then there are more open long positions in MMTLP than issued shares of NBH. Furthermore, FINRA suggests only issuers can issue shares, which fails to recognize that market makers create short/naked short shares.

FINRA cannot claim enough shares were issued and identify a short position on a non-tradable security at the same time. Investors have experienced differences in identifiers held at each broker since the FINRA U3 halt. It is impossible to identify a short/long/counterfeit stock unless the exact allocation of “sold shares” from each broker is audited in comparison to the original allotment of shares issued by NBH.](https://pbs.twimg.com/media/GCkYeJAWUAAxAZt.jpg)