SMB Seller Readiness Checklist (BC/Canada)

Thinking about selling your business in BC/Canada (now or in the next 1–3 years)?

You’ve likely poured years into building something that supports your family, your team, and your customers. A strong exit isn’t just about getting a good price — it’s about selling with confidence, protecting what you’ve built, and setting up your next chapter.

The difference between a smooth, respectful process and a stressful one is rarely luck. Most deals don’t break on price — they break on surprises: unclear add-backs, owner-dependence, customer concentration, and undocumented operations.

A great exit is built 12–36 months before you go to market.

Here’s a quick Seller Readiness Checklist to help you assess where you stand in 7 key areas and focus on the highest‑impact improvements before a sale:

1) Financials and reporting

• Clean financial statements (at least the last 3 years) and up-to-date YTD results

• Normalized earnings: clear, supportable add-backs (owner perks, one-time, and non-operational items)

• Simple KPI dashboard: revenue, gross margin, EBITDA, customer concentration, backlog/pipeline (where relevant)

2) Owner dependence and management bench

• Can the business run without you day-to-day?

• Key roles documented (GM/ops, sales, finance/admin)

• Incentives / retention plan for key people (especially post-close)

3) Customer and revenue quality

• Customer concentration understood and managed

• Recurring/contracted revenue is clear (terms, renewal risk)

• Clean A/R aging, low disputes, consistent collections

4) Operations and “transferability”

• Documented processes (sales, delivery/ops, hiring, finance)

• Systems are stable (accounting, CRM, job/project tracking)

• Vendor/supplier dependencies identified (and mitigations in place)

5) Legal and risk items

• Proper contracts in place (customers, employees/contractors, leases)

• Clean corporate records + IP/brand ownership where applicable

• Known risks surfaced early (regulatory, pending disputes, warranty/claims)

6) Story and positioning

• Clear “why buy this business?” narrative

• Credible growth opportunities (not just hope)

• Buyer profile fit: strategic, financial, operator/buyer — and what each will value

7) Timing and structure

• Your ideal timeline (sell now vs. 1–3 years)

• Tax + structure considerations (asset vs share, working capital expectations, etc.)

• Plan for what you want after the sale (role, transition period, earn-out tolerance)

The above checklist is a good starting point for your planning, but it's just a beginning.

If you’re an owner thinking “maybe in the next 1–3 years”, my DMs are open. Happy to compare notes on what typically builds confidence, improves value, and helps protect your legacy — no pressure.

— Ross

#BusinessExit #ExitPlanning #SuccessionPlanning #BusinessSale #MAndA

One of the most common things owners say is: “There is so much potential in this business.”

Sometimes they are right.

Growth potential. Margin potential. New markets. Better marketing. More capacity. A buyer who could “take it to the next level.”

The issue is that buyers rarely pay full value for potential that has not been tested.

They will usually ask:

• Why has this not already been done?

• Who would execute it?

• What would it cost?

• Would margins hold?

• Is there proof customers actually want it?

Potential can attract buyers. Proof changes what they are willing to pay.

A signed contract, a qualified pipeline, a tested marketing channel, a product line with early traction, or a manager who can execute without the owner are all examples of proof that reduce uncertainty and make future performance easier to believe.

Those things change the conversation because they move the discussion from theory to evidence.

Trust traction. Prove potential.

A buyer may still share future upside through deal structure, an earnout, vendor financing, or a stronger price if the evidence is convincing enough.

But “there is lots of potential” by itself is usually not a valuation argument.

It's a starting point for a better question:

“What proof can we build before a buyer asks?”

#BusinessAcquisition #BusinessValuation #SellYourBusiness #MergersAndAcquisitions

Owners of privately held businesses can start losing value in a business sale after the LOI is signed.

There’s a memorable phrase that I really like for this: The Maui Effect.

The phrase was coined by Mike McIsaac at @bakertillycan, who wrote about it recently. The idea is simple: once an owner starts mentally shifting their attention to life after the sale, like dreaming about being on a beach in Maui, their focus can drift before the transaction is actually complete.

That drift can be expensive.

Buyers are watching the business right through due diligence. If revenue declines, margins slip, customer follow-up slows, or the team senses the owner has checked out, the buyer usually does not treat it as a harmless wobble.

They start asking harder questions.

Was the original story too optimistic? Is the business more dependent on the owner than we thought?

Do we need a holdback, earnout, price reduction, or longer diligence period?

That’s where value starts leaking out.

A private business sale can often take 9 to 18 months, Mike notes in his article. By the time an LOI is signed, many owners feel like the finish line is close. In reality, the hardest part of the process is still ahead: keeping the business performing while also responding to diligence, advisors, buyer questions, employees, landlords, lenders, and lawyers.

The owner’s job is not finished when a buyer is found.

The owner’s job is finished when the deal closes, the transition risk is under control, and the business is set up to succeed without them.

Only then is it time to start thinking about Maui.

For anyone who has gone through an exit: how did you manage the pressure of running the business while also carrying the weight of the transaction process?

Source: “The Maui Effect: Why Business Owners Lose Focus Before the Finish Line” by Mike McIsaac, Baker Tilly (May 25, 2026): https://t.co/kMgkfqfoAO

I had an article published yesterday in the Delta City News on what business owners should understand about business value.

It was written for Delta owners, but the concepts apply to small and midsized businesses almost anywhere.

Buyers and lenders look at more than revenue and profit.

They look at clean financial records, customer concentration, lease terms, owner dependence, recurring revenue, team depth, and whether the business can keep performing after a transition.

That is why two businesses with similar earnings can sell for very different prices.

For owners, value is usually built long before the decision to sell.

Article link below:

https://t.co/UL0gLh0Wg4

#BusinessValue #ExitPlanning

Most business owners do not get to choose the perfect time to sell.

Sometimes they do. Sometimes life gets in the way.

Health, family, a buyer approach, partner issue, burnout, or a market window can force the timing.

That is why it helps to think about exit planning in stages, not as a fixed calendar.

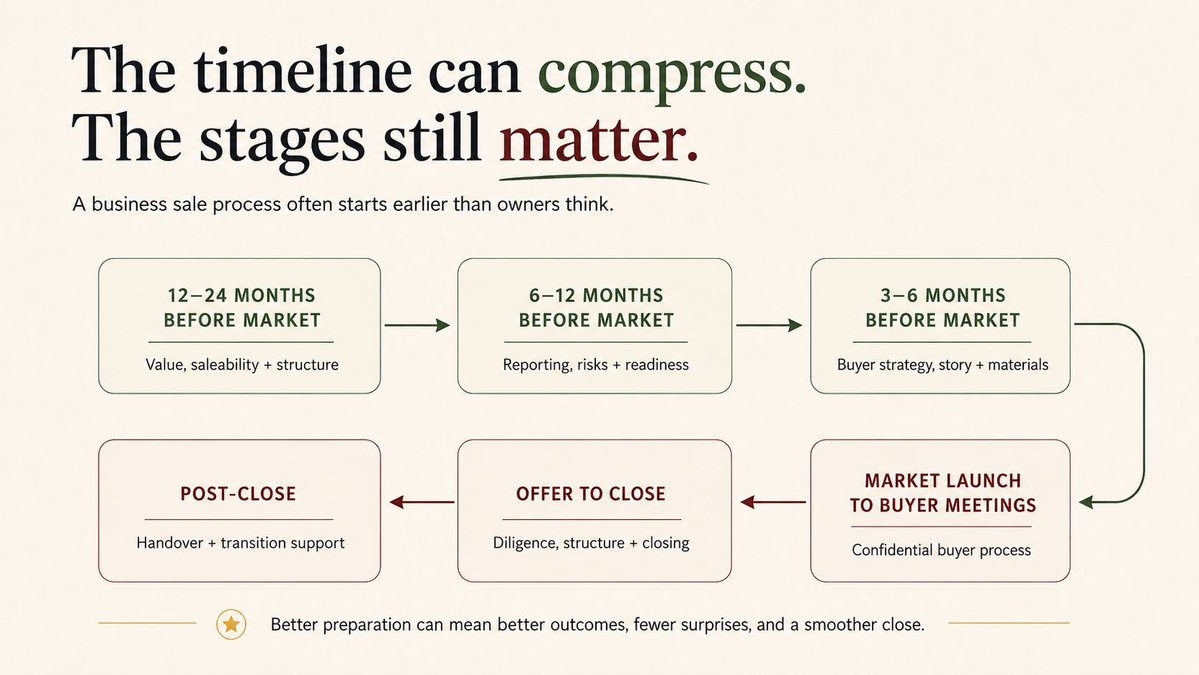

For an established business, the ideal planning window is often 12 to 24 months before market launch.

That does not mean being “for sale” for two years. It means understanding value, risks, structure, and buyer fit early enough to improve your options.

These stages are not exact for every deal, but they can help owners spot issues earlier and avoid treating the sale process as something that starts only when urgency hits.

12–24 MONTHS BEFORE MARKET

Understand value, saleability, and structure.

Get a grounded view of what the business may be worth, who the likely buyers are, and what could make them hesitate.

Involve tax, legal, accounting, and wealth advisors where needed. Share sale vs. asset sale, LCGE / QSBC status, excess cash, passive investments, shareholder loans, real estate, and family trusts can affect net proceeds and timing.

Some issues are hard to fix at the last minute.

6–12 MONTHS BEFORE MARKET

Make the business easier to explain and review.

Strengthen reporting where it will build buyer confidence. That may mean review engagements, a sell-side QoE, or better support for earnings adjustments.

Review concentration risks, key contracts, leases, owner dependence, and diligence gaps before buyers do.

3–6 MONTHS BEFORE MARKET

Build the buyer strategy, story, and supporting materials.

Who are the best-fit buyers?

What will they care about?

What should they see before and after confidentiality?

Decide what to share first, what to hold back, and how to organize what buyers will review.

MARKET LAUNCH TO BUYER MEETINGS

Run a controlled, confidential buyer process.

Outreach, buyer screening, Q&A, meetings, and feedback need to be managed carefully.

The aim is not every possible buyer. It is the right buyers, with the business protected.

OFFER TO CLOSE

Manage diligence, structure, and closing.

An accepted offer is not the finish line.

Next comes diligence, structure discussions, working capital, financing, legal agreements, transition planning, and closing mechanics.

Weak preparation often shows up here.

Buyers slow down.

They ask for price changes.

They add conditions.

Or they walk.

POST-CLOSE

Support the handover.

Depending on the deal, transition support, true-ups, training, customer introductions, or integration planning may still need attention.

The timeline can compress, but the stages still matter.

If you have time, use it to improve the business before buyers judge it.

Better preparation can mean better outcomes: more credible buyers, more confidence in the numbers, fewer diligence surprises, and a stronger chance of holding value through closing.

#ExitPlanning #MergersAndAcquisitions #BCBusiness

If you own an established lower mid-market manufacturing or industrial business , buyer appetite may be stronger than you think.

The latest @MNP_LLP Canadian middle-market update showed transactions increased 10% quarter over quarter in Q1 2026, from 251 to 276 deals.

Industrials led the quarter with 76 transactions, representing 27.5% of deal activity.

MNP’s manufacturing update adds another useful signal: North American manufacturing transaction volume increased for the seventh consecutive quarter and reached its highest level in more than eight years. Strategic buyers accounted for 85% of Q1 2026 manufacturing volume.

For owners of established manufacturing, fabrication, distribution, equipment services, and other industrial B2B businesses, that is a market signal worth paying attention to.

But I would be careful about reading this as a simple “market is hot” story.

Buyer appetite helps. Buyer selectivity still matters.

In lower mid-market industrial and manufacturing deals, buyers get practical quickly. They want to know whether earnings are supported by the operation, not only the headline profit or EBITDA.

That means questions like:

• How much deferred maintenance is hiding in the equipment base?

• Is growth coming from real capacity, or from running the team and assets harder than is sustainable?

• Are gross margins stable by product line, job type, contract, or customer group?

• How exposed is the business to tariffs, freight costs, foreign exchange, supplier concentration, or material price swings?

• Are there environmental, safety, WorkSafeBC, quality-control, or certification issues that could surface in diligence?

• Is the facility fit for a buyer’s plans: zoning, power, yard space, lease terms, and room to expand?

• Are inventory, WIP, backlog, quoting, and job-costing systems good enough for a buyer to trust the numbers?

The usual buyer concerns still matter: owner dependence, customer concentration, financial reporting quality, earnings adjustments, and management depth.

But industrial and manufacturing buyers often go a level deeper.

They are trying to figure out whether earnings are durable, assets are supported, and the business can continue to perform and grow after a transaction.

That is where preparation creates leverage.

A stronger M&A market can create more conversations and bring strategic buyers back to the table. For the right business, it can also increase the odds of a competitive process.

But market momentum does not fix operational or diligence gaps.

If a sale is possible in the next few years, the useful question is not only:

“Is buyer activity improving?”

It is:

“Would my business hold up when an experienced industrial or manufacturing buyer starts asking detailed questions?”

Source: MNP Corporate Finance, Canada’s Middle Market M&A Update – Q1 2026 - https://t.co/7BXfKDS0QO

#MergersAndAcquisitions #Manufacturing #IndustrialBusinesses #BCBusiness

Not every owner’s real choice is “sell” or “don’t sell.”

Sometimes the better question is:

Do you want a full exit, or do you want to take some chips off the table and keep building?

That distinction matters.

A recent article by Patrick Carpentier, Principal, Growth Equity at @bdc_ca, lays out growth equity as a minority-capital option for owners who want liquidity, succession support, or growth capital while staying in control of the business.

That is not the right fit for every company.

BDC notes that growth equity typically fits businesses with a proven model, experienced management, stable positive cash flow, and meaningful scale. In BDC’s case, the article references companies roughly in the $10M to $500M revenue range with at least $3M of EBITDA.

Most owner-operated businesses will not fit that profile today.

But in my experience, the underlying lesson applies much more broadly:

Businesses with management depth and operating discipline tend to have more options.

They may be able to:

• sell outright

• bring in a minority partner

• recapitalize the business

• transition to management or family over time

• keep owning while reducing personal risk

The point is not that every owner should raise growth equity.

The point is that optionality is usually created before a transaction, not during one.

By the time an owner says, “I’m ready to sell,” buyers and investors are already looking at the same things:

• Is the business dependent on the owner?

• Are the financials clean and decision-ready?

• Is there a real leadership team below the owner?

• Are systems and reporting strong enough to support growth?

• Is there a credible plan for what happens next?

Those questions matter whether the outcome is a full sale, partial liquidity, or no transaction at all.

This is why exit planning should not be treated as a last-minute event.

A business that is more sellable later is often the same business that can attract better capital options today.

For owners who are not ready to fully exit, that can be a useful reframing.

You may not need to decide between selling and doing nothing.

You may need to understand which options your business is actually ready for.

Question for owners and advisors:

If you had the choice, would you rather sell outright or take some chips off the table and keep upside?

Source: BDC, “Growth equity: A partner for what comes next” by Patrick Carpentier

https://t.co/hjEUdAt035

#BusinessOwners #ExitPlanning #GrowthEquity #CanadianBusiness

Here’s the uncomfortable truth of family business succession and exit planning: the advisors who know the family best may not be the right people to lead a third-party sale.

That is not a criticism of accountants or lawyers. Good ones are essential.

But knowing the family history is different from managing a competitive sale process.

Your accountant understands the numbers. Your lawyer understands the legal history.

A third-party buyer is looking at something else.

A family may be thinking about:

• preserving the legacy

• protecting employees

• keeping family relationships intact

• making sure the “right” buyer gets the business

A buyer is usually thinking about:

• normalized earnings

• customer concentration

• management depth

• owner dependence

• working capital

• risk after closing

• whether the deal can actually get financed

That gap matters.

A recent @IBBA_canada article cited studies showing that only about 30–35% of family businesses have a documented succession strategy. That lines up with what I see in conversations with family business owners.

In many family businesses, succession and sale planning carries years of history, expectations, and relationships.

There may be adult children with different levels of interest.

There may be family members working in the business who are not natural successors.

There may be a founder who wants to step back, but still cares deeply about what happens to the people, culture, and reputation they spent decades building.

That emotional layer can lead to good decisions. It can also lead to delayed decisions, unclear expectations, or accepting a weaker deal because the buyer says the right things early.

This is where a dedicated sell-side advisor becomes important.

A good M&A advisor or business broker does not replace the accountant or lawyer.

The better model is usually to build the right deal team, then have someone quarterback the transaction process.

The accountant can help with financial history, tax considerations, and accounting questions.

The lawyer can help with legal structure, agreements, and risk protection.

The sell-side advisor’s role is different: prepare the business for market, position it properly, manage buyer interest, create competitive tension where possible, and keep the process moving toward a real closing.

The sale of a family business is rarely only a financial event.

But the market will still treat it like one.

That’s the tension owners need to prepare for.

Question for family business owners and advisors:

When a family business is preparing for a third-party sale, who should quarterback the process: the long-time accountant or lawyer, or a dedicated sell-side advisor working alongside them?

Source: IBBA Canada, “The Evolving Realities Around Succession in Family Businesses”

https://t.co/6FlNOrhPOg

#FamilyBusiness #SuccessionPlanning #BusinessSale #CanadianBusiness

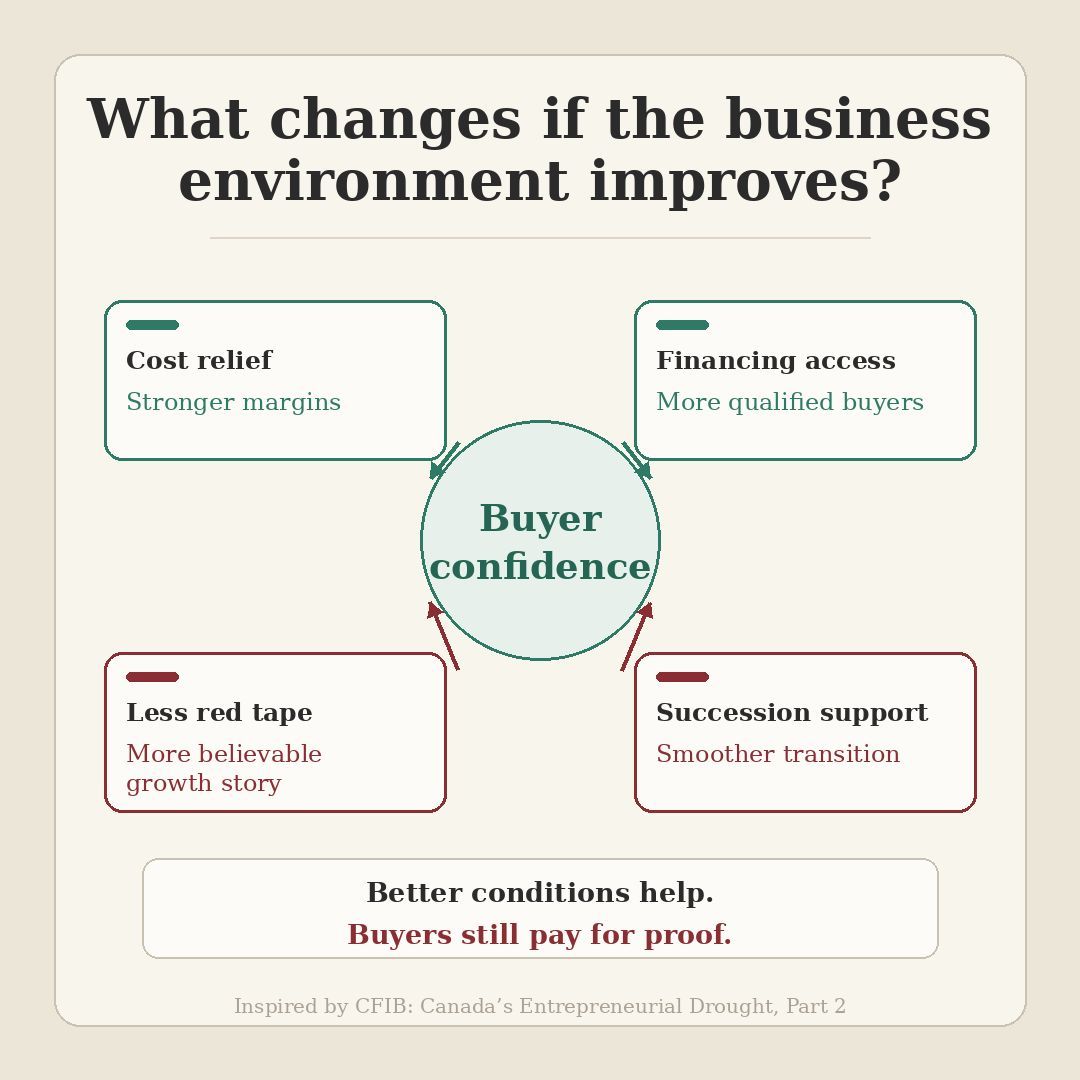

What happens to business values if Canada makes entrepreneurship easier again?

That’s the more optimistic question coming out of Part 2 of the @CFIBNews April 2026 “entrepreneurial drought” report.

Part 1 focused on the problem: Canada has had more businesses exiting than entering since early 2024. Part 2 looks at what could help reverse it.

CFIB points to some very practical priorities: reduce the cost of doing business, improve access to financing, cut unnecessary red tape, address labour shortages, and make business succession easier.

For owners thinking about selling in the next few years, implementing some or all of these measures could have a big impact.

A better small business environment does not automatically make every business more valuable, but it can change the buyer’s view of the risk:

• If costs ease, margins become easier to defend.

• If financing improves, more buyers can actually complete transactions.

• If red tape is reduced, growth plans become more credible.

• If labour availability improves, buyers have more confidence that the business can keep operating and growing after a transition.

• If succession pathways improve, fewer good businesses have to close simply because the owner ran out of time or options.

That is where the optimism comes in: good businesses become easier to believe in when the environment around them becomes more supportive.

The caution is that policy reform (if and when it happens) still will not do the seller’s job for them. Buyers still pay for proof. They want clean financials, durable earnings, transferable operations, manageable owner dependence, and a believable plan for what happens after closing.

So yes, I hope Canada becomes a better place to buy, own, and grow a business, and the sooner it happens, the better.

But for owners thinking about a transition, the practical takeaway is still the same. Make it easy for a buyer to understand why your business is worth owning.

A better environment may improve the market. A better-prepared business will be in the strongest position to benefit from it.

Which change do you think would do the most to improve buyer confidence: lower costs, better financing, less red tape, labour access, or stronger succession pathways?

Source: CFIB, “Canada’s Entrepreneurial Drought, Part 2: Fixing Canada’s Shrinking Business Landscape” - https://t.co/ue9yJSpheq

#BusinessSuccession #EntrepreneurshipCanada #SmallBusinessPolicy

“With all this uncertainty, is this really the right time to sell my business?”

I hear more business owners asking some version of that right now.

Costs are higher. Rates are still a factor. Tariffs, politics, labour, and the general economic mood all feel harder to read than they did a few years ago.

So waiting feels like it might be sensible. And sometimes it is.

If earnings are temporarily down, the business needs cleanup, or there is a clear plan to improve value over the next 12 to 36 months, delaying a sale may be the right call.

But uncertainty can also become a comfortable place to hide.

It gives an owner a logical reason to avoid a decision that already feels heavy.

Because selling a business is rarely just a financial decision. For many owners, the business is something they built, fixed, defended, carried, worried about, and eventually made part of who they are.

So when the market feels uncertain, it becomes easy to say:

“I’ll deal with it when things settle down.”

The problem is that the business may not stand still while you wait.

Competition can get tougher. Key employees can move on. Financial performance can soften. Health issues can force the timeline. Personal circumstances can shift unexpectedly.

And if the business changes while you wait, buyers will notice.

They may not see the company you remember building. They may see the version shaped by fatigue, delay, pressure, and missed preparation.

Owners cannot control the market. But they can decide whether they are reacting to uncertainty or using it to get ahead.

For strong businesses, uncertain markets are not always bad markets to sell in. Buyers may be more selective, but they still want quality. In some cases, a resilient business can stand out more when everything else feels harder to read.

So the better question may not be whether the market feels perfect.

“What would make my business compelling to a serious buyer right now?”

That question exposes the real work: value, timing, risks, and what needs to improve while the owner still has control.

You do not need perfect market conditions to sell a strong business.

You need to know whether your business is ready for the buyers who are still active in this market.

#ExitPlanning #BCBusinessOwners #SuccessionPlanning #MandA

Most business owners look at the recent rise in business closures in Canada and see scarcity. “Fewer good businesses for sale should mean mine is worth more.”

I understand the logic, but many buyers read the same signal differently.

The @CFIBNews April 2026 report on Canada’s “entrepreneurial drought” points to a shrinking business landscape. Since early 2024, more businesses have been exiting than entering. More than half of Canadian SME owners also said they would not recommend starting a business right now - ouch!

This really matters if you own a business and plan to sell in the next few years.

A buyer may look at the same market and think, “Why are so many owners heading for the exits?”

When the broader small business environment looks fragile, buyers tend to underwrite more carefully. They ask harder questions:

• How durable are the earnings?

• How dependent is the business on the owner?

• Are customers coming back because the business is genuinely sticky, or because the owner personally holds the relationships?

• Are margins holding up after wage, rent, financing, and input cost pressure?

• Will the next five years look anything like the last five?

Scarcity only helps valuation when your business looks safer, cleaner, and more transferable than the average business struggling in the market.

A shrinking business landscape may make strong companies stand out. It also makes weak companies harder to sell.

For owners thinking about a transition, the practical lesson is simple:

Do not assume a tighter market will do the work for you.

Build the buyer case before you need it. If buyers become more cautious, what part of a business do you think they scrutinize first?

Source: CFIB, “Canada’s Entrepreneurial Drought, Part 1: The Shrinking Business Landscape” - https://t.co/MNH0E8gZTS

#BusinessValuation #BusinessExit #SmallBusinessCanada

Two BC construction companies. Same EBITDA. One sold for $4.5M, the other for $2.5M.

The difference: one had no customer contributing more than 10% of revenue and a management team that could run without the owner. The other had a single customer at 60% and an owner at the centre of every decision.

Same earnings. $2M apart.

New 2026 Lower Mainland data from @arv_consultants covers BC businesses with $500K–$15M in revenue. Median EBITDA multiples run from 2.5x for brick-and-mortar retail to 4.5x for SaaS and tech.

The spread within each sector is wide. Some of the most important value drivers:

• Recurring revenue and customer diversification

• Owner independence from day-to-day operations

• Management depth below the owner

• Lease transferability and remaining term

• Financial statement quality

Most sellers find this out during diligence. By then, they are usually just absorbing it in the price.

When you start thinking about selling, ask yourself honestly: if a buyer spent 30 days looking at my business, what would they find that I haven't fixed yet?

Full 2026 BC industry multiple breakdown: https://t.co/HCdzeXki51

#BusinessValuation #ExitPlanning #BCBusiness

A lot of business owners think selling their company is mainly about agreeing on a price.

In real life, getting paid is often just as much about terms, financing, and what a buyer can actually close on.

I just read a very useful @bdc_ca article on buying and selling businesses by Grace Bartz and @deveshd, and it’s well worth a read for any owner thinking about an eventual exit.

One point in particular is worth highlighting.

Sellers rarely get 100% cash on day one.

And vendor financing is not some weird last-resort concession.

In many business sales, it’s a normal part of the structure.

That can take a few forms:

• a vendor take-back note

• part of the purchase price paid over time

• earnouts tied to future performance

• a short transition period where the seller stays involved and helps de-risk the handoff

Why does this matter?

Because buyers and lenders are not just looking at the headline price.

They’re looking at whether the business can support the purchase, whether the cash flow is clear, and whether the risk is low enough to finance.

That’s where a lot of first-time sellers get surprised.

They go in thinking: full price, full cash, fast close.

The market often says: maybe, but can the buyer get financed, can the cash flow support the payments, and will the deal still hold together through closing.

That doesn’t mean you should accept a bad deal.

It means you should understand that structure is often what turns buyer interest into a transaction that can actually close.

And the cleaner your financial reporting is, the stronger your position usually is on both price and terms.

Worth reading if you own a business and think you may want to sell in the next few years.

Would you rather take a slightly lower all-cash offer or a better-priced deal with some seller financing if the buyer and lender were strong?

Source: https://t.co/SCQKdyX5Kz

#ExitPlanning #BusinessSale #VendorFinancing #CanadianBusiness

“Time kills deals” may be a cliché, but it’s also usually true.

And in business sales, it’s even more true.

A sale process that drags on is usually a big red flag.

Momentum fades, buyers get distracted, diligence gets more drawn out, costs creep up, and confidence can start to erode on both sides. In some cases, what looked like a very workable transaction at the start slowly becomes much harder to close.

Usually, it’s not because of one dramatic issue.

More often, it’s a build-up of things like:

• poor preparation

• disorganized financials

• unclear reasons for selling

• unrealistic value expectations

• slow responses once the process is underway

That’s one reason I think owners need to be well prepared when they go to market.

And if they’re not, it may make sense to take some extra time first, get things in better order, and then run a stronger process.

Because once a sale process loses momentum, it’s hard to get it back.

I'm curious whether others see it the same way: in a business sale, what tends to do more damage - poor preparation at the start, or delays once the process is underway?

#ExitPlanning #BusinessSale #BCBusiness

A business buyer doesn't look at your company the same way you do.

Understanding business buyers | Part 5 of 5

After analyzing the data from recent business buyer outreach we've seen, one thing is pretty clear.

Most buyers are not looking for the same thing, but many do circle around some of the same core criteria.

They want steady earnings and like the predictability that comes with repeat or recurring revenue.

They pay attention to whether there’s a real team behind the business or whether everything still runs through the owner.

They tend to like practical businesses they can understand quickly, with a clear path to grow what’s already there.

That doesn’t mean every buyer wants the exact same type or size of business.

Some are comfortable with more complexity, and some care more about recurring revenue than others. Some are willing to roll up their sleeves and jump in to operate the business, and others want a strong management team in place.

But in general, business buyers aren't chasing mystery and excitement. They’re usually looking for a business that already works, has some durability to it, and can keep working through a transition.

That’s one reason owners can sometimes misread their own business. Owners often focus on what makes their business feel ordinary because they live inside it every day.

Business buyers have a different lens. They focus on whether a business is reliable, understandable, profitable, and transferable.

If you're a business owner thinking of selling in the future, the different lens a buyer uses can be a useful one to be aware of. It helps serve as a guide to planning the steps you may need to take to maximize the value of your business before you sell.

I hope this series on understanding business buyers has been helpful. If you're a business owner and thinking of selling your business in the next few years, feel free to reach out to me directly if you'd like some help with planning.

#BusinessOwners #ExitPlanning #MergersAndAcquisitions

BC is not a side market. For many business buyers, it is exactly where they want to be.

Understanding business buyers | Part 4 of 5

A lot of BC business owners assume the most serious buyers are somewhere else. Toronto, the US., maybe overseas, and some definitely are.

But that’s only part of the picture.

When I analyzed some recent buyer outreach data, what stood out to me was not just who these buyers were, but where they were actively looking. The majority specifically mentioned BC, Metro Vancouver, Vancouver Island, or Western Canada, or at least included them in a broader geographic target area.

That matters because a lot of business owners underestimate how much diverse buyer interest is focused close to where they operate.

Sometimes the right buyer is from another province or another country. But sometimes they’re much closer than people think.

Local knowledge and existing relationships matter. Travel is easier, and integration can be simpler. And for some buyers, being in or near the market they want to grow in is part of the appeal. For others, they are looking to move or expand into a new geography.

BC isn’t some side market that only gets attention when nothing else is available. Often, it is exactly where the buyers we talk to want to be.

If you found this post interesting, stay tuned for the final post in this series focused on some of the most common search criteria we're seeing from business buyers right now.

#BCBusiness #ExitPlanning #MergersAndAcquisitions

Most business owners think operational efficiency saves money. What many owners miss is that buyers often value those savings at a multiple.

I just read a very practical article from @bdc_ca featuring Josh Ramsbottom on operational efficiency. It's definitely worth a read, especially for owner-led businesses that assume efficiency is mostly about cutting a bit of cost or buying new software.

The bigger point is this.

When efficiency improvements create real, durable cost savings, they do more than improve this year’s profit.

They can increase value by a multiple of those savings because buyers pay for earnings.

A business that removes $100K of waste does not just save $100K.

In many cases, it becomes meaningfully more valuable.

And there is a second benefit that matters in a sale process.

Better efficiency usually makes the business easier to understand, easier to transfer, and less dependent on daily firefighting.

That’s why this is not just an operations issue. It’s one of the cleaner ways to build value now and make a business easier to sell later.

A few simple examples:

• smoother day-to-day workflows

• fewer mistakes and less rework

• less time wasted fixing the same problems

• more of the business documented instead of living in the owner’s head

Those changes can lift earnings now. They can also reduce buyer-perceived risk and increase value later.

That combination matters.

A lot of owners wait too long to do this work because they think they will get to it once they are ready to sell.

Usually, the owners who start earlier create more value and have more options.

What operational fix in your business would create the biggest value lift if you solved it this year?

Read the article for more insights on how to drive operational efficiency from BDC here: https://t.co/9NqBVccdZo

#OperationalEfficiency #BusinessValue #SuccessionPlanning #CanadianBusiness

You don't need to own a $5M+ EBITDA business to attract serious buyers.

Understanding business buyers | Part 3 of 5

A lot of owners assume they need to be a much bigger company before serious buyers will care. What I see is that there are buyers for good businesses of all sizes.

In the recent buyer outreach that I've analyzed, a lot of the size-specific interest was aimed below $5M of earnings, with earnings below $1M being very popular.

That doesn’t mean bigger businesses aren’t in demand. They of course are, there are just fewer of them out there.

But it does mean there are plenty of buyers who are not just looking for large platform deals. A lot of them are actively looking for good companies at a smaller size, especially when the business has steady cash flow, a clear niche, and room to grow.

This matters because owners often rule themselves out too early.

They assume they’re too small, that buyers won’t care yet, and that they need more time and more scale before it’s worth having the conversation.

Sometimes that’s true, but often it isn’t.

A good business at the right size, in the right space, and with the right buyer fit can get more attention than its owner might expect.

If you found this post interesting or helpful, stay tuned for the next posts in this series, where I'll share more details on where these business buyers are looking and what they're looking for.

#BusinessOwners #ExitPlanning #MergersAndAcquisitions

@IBBA_canada shared a good reminder recently: a lot of business sales don’t fall apart because of one big surprise at the end.

They usually start coming apart much earlier.

That’s worth paying attention to because a good business is not automatically a closeable transaction.

I see a lot of owners assume the hard part is finding a buyer.

Often the harder part is getting the business, the timing, and the process into a shape that buyers can actually get comfortable with.

That can mean things like:

• unrealistic expectations on value

• weak preparation before going out

• poor positioning

• the wrong buyer fit

• delays that slowly kill momentum

By the time those issues show up clearly in diligence, the process may already be under pressure.

That’s one reason I think owners should spend more time getting sale-ready before they ever test the market.

More time doesn’t just help with cleanup. It can improve positioning, buyer targeting, and the odds of getting to a real close.

A lot of failed sales were probably avoidable earlier.

Source: IBBA Canada, Why Business Sales Break Down

https://t.co/QSRdYGj3mk

#ExitPlanning #BusinessSale #SuccessionPlanning

If you think your business is too boring to be interesting, that may actually be a strength.

Understanding business buyers | Part 2 of 5

A lot of the buyers reaching out to us are looking for businesses that most people would call boring.

Not flashy. Not trendy. Not the kind of company that gets talked about much online.

What they keep asking about are durable B2B businesses. The kinds of companies that quietly keep things moving in the background.

That includes manufacturing, technical services, contracted B2B services, maintenance, facility services, distribution, repair, route-based businesses, printing, and other niche operators with steady customers and decent cash flow.

There’s a reason for that.

These businesses are often tied to real operational needs. The offering is usually easy to understand, the demand tends to be steadier, and buyers can often see a clearer path to improving or growing what’s already there.

They may not look exciting from the outside, but buyers tend to like repeat business, sticky customer relationships, practical offerings, and operations that don’t need to be rebuilt from scratch.

There can be a lot of value in businesses like these. So if you own one, don’t assume the market sees it as boring in a bad way. Quite often, it’s the opposite.

Keep an eye out for more posts in this series with other details on what we’re seeing from business buyers.

#BusinessOwners #B2BServices #Manufacturing

BC business confidence dropped again in March. That shouldn't surprise anyone paying attention.

Hanna Hett at @DailyHiveVan recently wrote a great article about the latest @cfibBC monthly business barometer for BC, and I think it points to a bigger issue than just "confidence."

What stood out to me from Hanna's article, the comments from CFIB's @rmttn, and some of my own recent observations is that this isn't really one problem. It's a bunch of things hitting BC business owners in quick succession.

These include:

• softer demand

• higher wage pressure

• insurance that keeps getting more expensive

• occupancy costs that keep going up

• taxes and other regulatory burdens that always, at least in recent years, seem to move in the wrong direction

Then, on top of all of these things, @Dave_Eby and his @bcndp provincial government want to expand PST to more business-related services, driving costs up even more.

At a certain point, this stops being a story about "confidence" and starts becoming a story about policy choices. Sure, it's easy to blame some of the confidence drop on the recent uptick in oil prices and uncertainty related to the conflict in Iran, but that isn't the whole story.

Business owners aren't stupid. When costs keep rising, rules keep expanding, and demand gets less predictable, they respond the way any rational person would.

They get more cautious, delay hiring, and hold back on investment. Some shelve growth plans. Others start asking themselves how much longer they really want to keep at it.

This also affects what owners do next.

Some will keep pushing, while others will scale back. And some may start thinking about just winding things down.

But for profitable businesses, it's usually worth at least exploring a sale before making that call.

Many owners assume selling will be too complicated, too disruptive, or not worth the effort. Sometimes that's true, but often it isn't.

There are buyers with longer time horizons, more capacity, and a different appetite for the grind than some owners may have at this stage.

So yes, confidence matters. But what matters more is what owners do when they're feeling the pinch.

And a reminder to the BC provincial government: if you keep making it harder and more expensive to run a business, don't act surprised when confidence drops, and investment slows.

I'm curious whether others in BC are seeing the same thing right now. Is it time to consider a sale, or double down for the long term?

Read Hanna's article at: https://t.co/XS3TSwukIa

#BCBusiness #SmallBusinessBC #BusinessOwnership #ExitPlanning