The biggest red flag I see people raising with $SYM is that one customer, Walmart, represents roughly 85% of revenue.

That is clearly a real concentration risk. But I think the market often misses the other side of it, that customer is one of the largest companies in the world by revenue. When your anchor customer is that big, the number of new customers required to materially dilute that 85% is enormous. That kind of diversification is a multi-year process, not something that happens overnight.

People also seem to overlook that $WMT owns close to 12-14% of Symbotic. So while there is always a fear that Walmart could move elsewhere, their incentives are also aligned with Symbotic continuing to scale and succeed.

Long SYM

$ADBE headline ARR growth needs context. Total Adobe ARR exited Q2 at $27.1B, up 12.5% YoY, but that includes roughly $480M from Semrush. Strip that out and underlying ARR is closer to $26.62B, or roughly 10.5% growth versus $24.08B last year.

More importantly, FY26 ARR growth guidance is only 10.2%, and that now includes Semrush. If you simply back out the $480M Semrush contribution, implied organic ARR growth would be closer to 8.3%.

Management also admitted the freemium push and deferred Creative Cloud line optimisations will hit short-term ARR. So revenue and EPS guidance went up, but the forward ARR signal looks weaker than the headline suggests.

Markets need to be careful reading too much into this jobs beat. A huge chunk of the strength, 70k of the 170k added, looks tied to short-term hiring, especially World Cup-related roles.

That is far from broad, healthy, long-term job creation. If the next jobs report strips out that temporary boost, the number could look very different.

One month the market panics because jobs are too strong. Next month it could panic because the underlying labour market looks much weaker than expected.

Be careful treating one headline print like the full picture.

Advanced nuclear just crossed a real line: Antares’ Mark-0 reached zero-power criticality at INL, the first privately developed US non-light-water reactor to do so in 40+ years.

Bull case: validates the pathway, boosts nuclear sentiment, supports future fuel demand and helps the wider chain: $UUUU $OKLO $SMR

Bear case: Antares got there first, which could make $OKLO and $SMR look behind, while public “picks and shovels” names like $BWXT may get the cleaner read-through.

https://t.co/vQ6Ogixmpg

Where do you think $UUUU’s market cap could get to over the next 5 and 10 years?

I’ve been running some rough reverse calculations based on current guidance and the recent feasibility studies.

From what I can see:

Base case, this could be a $8-10B company if Mesa Phase II, uranium production and parts of the rare earths strategy execute properly.

Stronger bull case, $15-17B looks possible if Vara Mada gets built, White Mesa Phase II delivers the stated EBITDA, uranium stays tight and ASM adds real downstream value.

The key numbers I’m looking at:

Vara Mada: $1.8B NPV and $500M+ annual expected EBITDA.

White Mesa Phase II: $410M capex and $311M annual standalone EBITDA.

Current market cap is still only around $3-4B.

Not saying it gets there. But I’m trying to work out whether this is just a decent uranium/REE trade, or a genuine 5-10 year multi bag play. Thoughts?

$UUUU

The DoD is officially cutting off Chinese rare earths for military tech, and it could be a massive structural tailwind for $UUUU

The new mandate strictly prohibits the DoD from using high-performance magnets (NdFeB & SmCo) processed in China or Russia. Since China controls ~90% of this market.

Energy fuels White Mesa Mill is the only US facility actively separating these exact rare earth oxides at commercial purity.

https://t.co/00XfB6FcW8

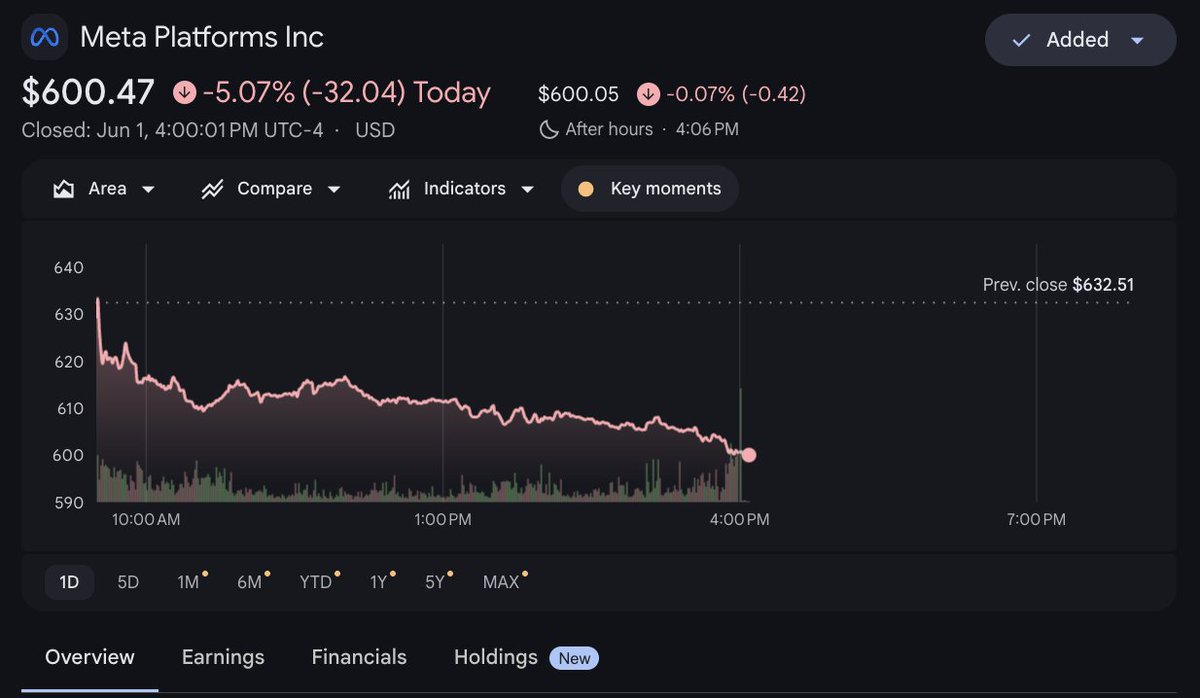

Playing around with $META fair value assumptions. I used what I’d consider pretty conservative inputs:

- 5 year operating cash flow growth: 15%

(5-year historical average OCF growth: 25.4%)

- Price to operating cash flow multiple: 14.13x

- Required return: 15.1%

- Annual share count change: 0%

(assuming no buybacks due to capex)

Even with those numbers, it spits out a fair value of $685.59, around 14% upside from today’s price of $600.47.

Future stock price comes out at $1,374.47, which implies an 18.19% CAGR.

Stupidly good valuation.

$META

$NVDA unveiled its Arm-based RTX Spark PC chip for laptops and mini-PCs, pushing deeper into full consumer computing together with Mocrosoft and Google also announcing not long ago a new AI-focused laptop, all eyes now shift to Apple...

What does $AAPL do next, and more importantly, who do they partner with?

$NVDA $ARM $MSFT $GOOGL $AAPL $QCOM $INTC $AMD

Berkshire is still hunting after buying homebuilder Taylor Morrison for $6.8B cash, a 24% premium.

One of Greg Abel’s first major acquisitions as CEO.

Adds a scaled US homebuilder with hundreds of millions in annual free cash flow (6-700m), exposure to long-term housing demand, and obvious tie-ins across Berkshire’s existing insurance and housing-linked businesses.

$TMHC $BRK.B

Obvious rotation into $IGV, with $XLE catching a bid on Iran.

While there are some obvious software plays that are not going away anytime soon, many will, and plenty of retail will be left holding the bag.

Let’s hope for a continued pullback. Happy to fish the rotation wave.