One thing that stood out in yesterday’s #AVCT placing RNS.

@avacta could’ve said:

“We look forward to reporting initial AVA6103 data.”

“The data will help evaluate the broader potential of preCISION.”

“AVA6103 may provide further validation of the platform.”

Instead, they said:

“…We expect that these data will provide validation of our preCISION technology in patients, by demonstrating that both our First and Second Gen molecules can effectively treat human cancers.”

That’s a VERY strong statement.

AVA6103 isn’t about proving exatecan can kill cancer cells. Exatecan is already a highly potent Topo1 payload with known tumour activity.

The key question is whether preCISION can activate it in the tumour and provide sustained release while controlling systemic exposure.

Given the trial design, timing and early clinical/PK visibility, Avacta should already have a good sense of whether AVA6103 is behaving as intended.

So “we expect these data will provide validation” feels extremely deliberate.

Not proof until data is release, but this does not read like cautious language from a management team worried the platform might fail to translate.

Cohesion Bureau will be busy planning for the day they can finally tell the world why Avacta have spent 2026 comparing itself to the biggest selling ADC of all time.

Delighted to be appointed as chairman of #AVCT

My core priority is to ensure the value of preCISION is exploited to its fullest, for the benefit of all shareholders.

I am more than confident we have the team and the intellectual property to enable this.

@neil432111 Why would #AVCT hold a science day to present more preclinical results based on its sustained release mechanism if it wasn’t working in clinic. FAP-Exd working as designed. Onwards and upwards.

#AVCT plans to add indications to an already indication heavy trial, three weeks into dosing P1a, on the eve of AACR.

AVA6103’s USP is unparalleled potency and extremely wide utility.

Look across the pond at UK-listed @avacta $AVCT #AVCT.

Targeted oncology.

Its pre|CISION platform can be used to modify practically any anti-cancer small molecule or biologic, into a peptide-drug conjugate.

These PDCs can be used to target around 85% of all types of cancer cases.

Two drugs in the clinic. One to kick off a Pivotal Phase 2/3 trial this summer; the second drug having just commenced a Phase 1 trial.

The uber bull case is that pre|CISION PDCs eventually displace the large majority of the existing and anticipated ADC market. PDCs...

- are significantly more targeted than ADCs;

- are much lower cost (as don't require an expensive biologic such as a mAb);

- have broader applicability (almost tumour agnostic - see 85% fig above);

- have broader versatility (the Avacta scientists can modify practically any warhead with pre|CISION);

- have superior tumour penetration and tissue diffusion, owing to their smaller size.

In fact, it is difficult to point out a single major advantage that the existing class of ADCs enjoys over Avacta's PDCs.

If the second drug in clinic - AVA6103, a modified version of the all-powerful warhead, exatecan - replicates the published pre-clinical data (22/24 complete responses in various animals models - a CR rate of 92%), it has the real potential to blow Enhertu (and even Keytruda) out the water.

By virtue of Avacta's UK listing, this opportunity exists. The UK investment community is a shadow of what it once was - it lacks depth, breadth, and many of its participants do not possess the intellectual curiosity and/or risk tolerance for pre-revenue / lossmaking entities.

Were Avacta listed on NASDAQ right now, I would suggest it'd be valued at at least 10x its current mkt cap of $363m.

#AVCT What many do not realise is how much speedier the 6103 trial will be compared to 6000. For the following reasons

1) 6000 started by dosing patients with conditions that did not respond to dox. 6103 is dosing straight into patients expected to respond based on AI.

1/n

We are thrilled to share a major milestone for our pipeline: the first patient has been treated in the FOCUS-01 Phase 1 trial of AVA6103 (FAP-Exd), our sustained-release pre|CISION® exatecan peptide drug conjugate. https://t.co/sGGbU7vQHZ #AVCT#FOCUSontheWIN

Well, this is one of the very few raising RNSs' that I have ever been glad to see. To me it shows 1)AVA600 & AVA6103 are being kept in house to be part of the whole sale - i.e. no nasty loose ends and 2) The dilution is only 15m extra shares not 63m - brilliant! #AVCT

The Institute of Cancer Research proved it…

Add a FAP inhibitor ➡️ AVA6000 stops working.

✅ 3rd party validation of the mechanism.

Plus…

AVA6000 + ATR inhibitor = ~2x improvement in potency

✅ Combination potential confirmed.

#AVCT

2/2

New *independent* data from 🚨 The Institute of Cancer Research 🚨 shows:

AVA6000 only works when FAP is present in the TME.

No fibroblasts = no meaningful activity.

With fibroblasts = strong potency.

This is the platform doing exactly what it’s supposed to.

1/2

#AVCT

@JStonker Great to see success against the disease

This is where #AVCT stands out

Not niche HER2, CLDN12 etc expression in rare subtypes. It’s FAP

90% of solids tumours (which are ~90% of all cancers) express FAP. >80% of all cancers in scope

preCISION offers near pan-solid tumour Tx

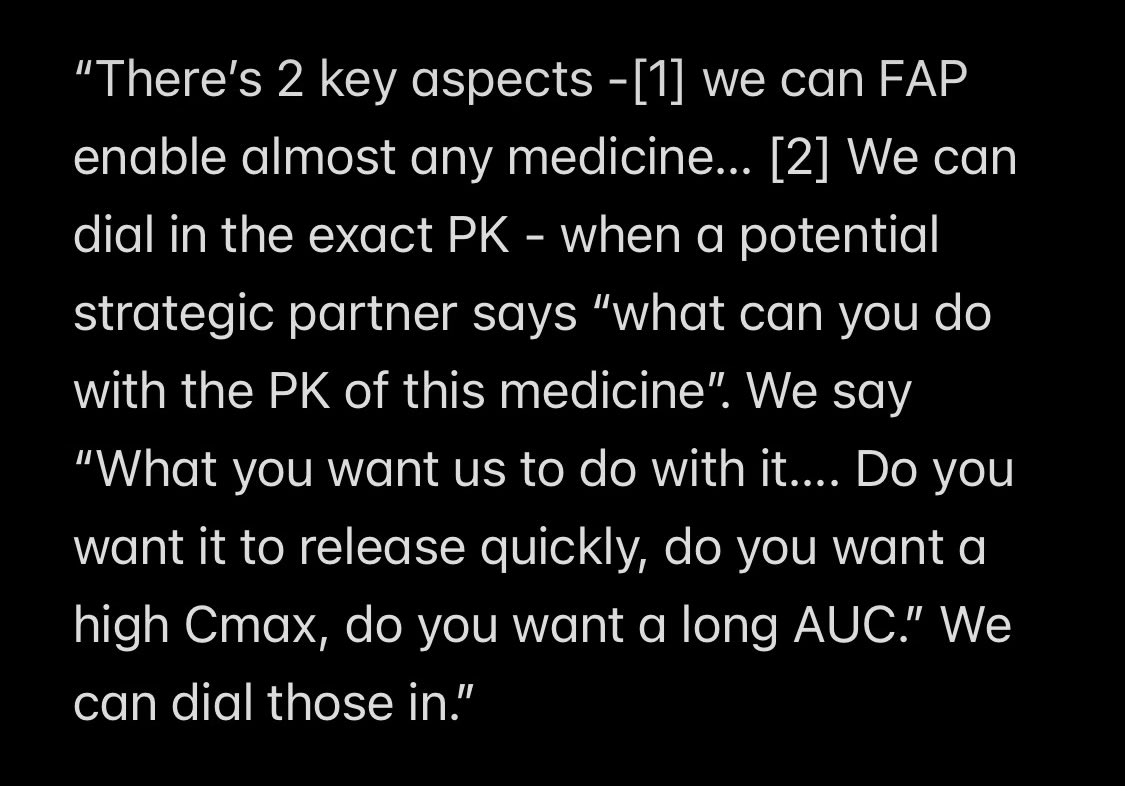

⬇️ Response to the final question at TD Cowan “What do you think is the most under appreciated aspect of Avacta?” = 🔥

Those 2 points + the confidence with which the CEO can deliver the message (due to the supporting data + science) is what will see #AVCT sold for a massive sum.

#AVCT is doing exactly what I hoped

- identify an already effective drug

- replicate vendor's own tests

- demonstrate significant improvement

- meet the bar for accelerated approval

- telegraph the fact

As long as #AVCT get multiple bidders, and why wouldn't we?, then the sale value will take care of itself - thankfully I say because far too many retail would sell cheap just to realise some gains after all these years.

Consider this: Novartis make a low-ball £2Bn offer, are DS/AZ going to sit back & watch a major BP take pre|CISION and not only destroy Enhertu sales but threaten whatever else is in their pipeline?

I seriously doubt it, so they'll go over the top and then what do Novartis do about that? They already missed out on the ADC boom, are they going to repeat that mistake again or are they going to go back over the top.

What does Lily make of all this and Merck, can't believe they'll sit on the sidelines when there is so much at stake...

I may be wrong but I think a low-ball is out the question. I believe significant money has already been agreed pending data release and thats the only reason we haven't done any deal yet. A BP wants the lot and are willing to pay a premium for it. After all, small deals are easy to do but we may end up helping the other company more than we help ourselves by doing one (im quoting AS & CC here).

AIM will never value avacta properly, it's just not going to happen.

More likely is red dot appears outlining the offer (s) and shares gap open near that amount. Avacta have kept an incredibly tight ship since Christina's tenure and I dont see that changing so there will be no warning, no heads up, no nothing and to be fair, thats what long-term investors deserve. Those of us who have done the research, held the shares through thick and thin and supported the company every way possible. This will be our year! 💪

Still buzzing about the removal of Max Dosing Limit for Faridox.

CC is 🥇

Does her master plan include for increasing patient numbers in P1b to drive up odds of achieving breakthrough therapy status for 6k pre-P2?

This being the milestone for a huge uplift in deal value…..#avct

#AVCT is the first ever company to see a Phase 1 drug achieve removal of the cardiac dosing limit.

External validation doesn’t come much clearer.

The CEO’s confidence levels are now at 11 for good reason.

pre|CISION. works.

With the lifetime limit cap of dox removed, due to an exceptional safety profile, it's a matter of time before ODD/AA, is granted for #AVCT's pathfinder drug in Salivary Gland Cancer (SGC) - a major derisking event for Big Pharma (BP).

Before this limit was removed, peak sales for 2030 (<4yrs away) were modelled at $250m pa.

But now we know Pre|CISION modified doxorubicin (dox) is so good that it can:-

✅️Treat patients at 4x the max dose

✅️Treat them MORE frequently

✅️Treat patients ineligible for straight dox due to their age/fragility

✅️Treat patients for MUCH longer (indefinitely? Treat as a chronic condition?)

What the above means is those peak sales forecasts need to be increased, significantly and risk-adjusted DCF calculations updated accordingly. I've just run some numbers through AI and I get a current risk-adjusted value for Avacta of between £500 & £1Bn today, so between double and quadruple today's valuation, based off just one indication! 🤯

That's in a fair market of course, not with the company sat on the AIM casino.

90% of SGC patients currently taking Faridoxorubicin are living at least twice as long without the disease progressing (Progression Free Survival [PFS]), than those not taking it.

Note: *PFS is increasingly being used as a proxy for overall survival by the FDA.*

In simple terms patients are living better quality of lives and almost certain to live longer (Overall Survival) taking Avactas drugs than current best alternatives.

Avacta's drugs are kinder and more efficacious but that's not all...

Peptide Drug Conjugates (PDC's) are 90% cheaper to manufacture than ADC's also.

The data hitherto (which is only improving) justifies accelerated approval for SGC in addition to ODD. Once approved, off-label use is likely to skyrocket as what clinicians would prescribe straight dox again given there is a kinder more efficacious version of the same drug? Basically Faridoxorubicin replaces doxorubicin entirely, not just in SGC.

And the really funny thing, Faridoxorubicin isn't even that good when compared to Avacta's 2nd and 3rd generation PDC's or worth ANYWHERE NEAR as much money to the company.

AVA6103, Avacta's highly anticipated pre|CISION modified version of Exetecan has just completed IND and goes into humans within weeks. It uses the exact same delivery system as the pathfinder drug and has already performed better than Faridoxorubicin did in the pre-clinical setting.

At some point the gaping chasm between current value and fair value for this company closes and violently I expect.

Avacta will recieve multiple, multi-billion pound takeover approaches this year from BP desperately seeking to address their £180Bn patent cliffs. pre|CISION fits perfectly.

Always DYOR

![SeanDentBsc's tweet photo. With the lifetime limit cap of dox removed, due to an exceptional safety profile, it's a matter of time before ODD/AA, is granted for #AVCT's pathfinder drug in Salivary Gland Cancer (SGC) - a major derisking event for Big Pharma (BP).

Before this limit was removed, peak sales for 2030 (<4yrs away) were modelled at $250m pa.

But now we know Pre|CISION modified doxorubicin (dox) is so good that it can:-

✅️Treat patients at 4x the max dose

✅️Treat them MORE frequently

✅️Treat patients ineligible for straight dox due to their age/fragility

✅️Treat patients for MUCH longer (indefinitely? Treat as a chronic condition?)

What the above means is those peak sales forecasts need to be increased, significantly and risk-adjusted DCF calculations updated accordingly. I've just run some numbers through AI and I get a current risk-adjusted value for Avacta of between £500 & £1Bn today, so between double and quadruple today's valuation, based off just one indication! 🤯

That's in a fair market of course, not with the company sat on the AIM casino.

90% of SGC patients currently taking Faridoxorubicin are living at least twice as long without the disease progressing (Progression Free Survival [PFS]), than those not taking it.

Note: *PFS is increasingly being used as a proxy for overall survival by the FDA.*

In simple terms patients are living better quality of lives and almost certain to live longer (Overall Survival) taking Avactas drugs than current best alternatives.

Avacta's drugs are kinder and more efficacious but that's not all...

Peptide Drug Conjugates (PDC's) are 90% cheaper to manufacture than ADC's also.

The data hitherto (which is only improving) justifies accelerated approval for SGC in addition to ODD. Once approved, off-label use is likely to skyrocket as what clinicians would prescribe straight dox again given there is a kinder more efficacious version of the same drug? Basically Faridoxorubicin replaces doxorubicin entirely, not just in SGC.

And the really funny thing, Faridoxorubicin isn't even that good when compared to Avacta's 2nd and 3rd generation PDC's or worth ANYWHERE NEAR as much money to the company.

AVA6103, Avacta's highly anticipated pre|CISION modified version of Exetecan has just completed IND and goes into humans within weeks. It uses the exact same delivery system as the pathfinder drug and has already performed better than Faridoxorubicin did in the pre-clinical setting.

At some point the gaping chasm between current value and fair value for this company closes and violently I expect.

Avacta will recieve multiple, multi-billion pound takeover approaches this year from BP desperately seeking to address their £180Bn patent cliffs. pre|CISION fits perfectly.

Always DYOR](https://pbs.twimg.com/media/HASIxi6WEAAv6LT.jpg)