As economies get richer, advertising grows faster than GDP. What looks like low ad spend today is often future runway.

Our latest report explores how AI could accelerate the next phase of AdTech growth - https://t.co/z3yMYzk1gc

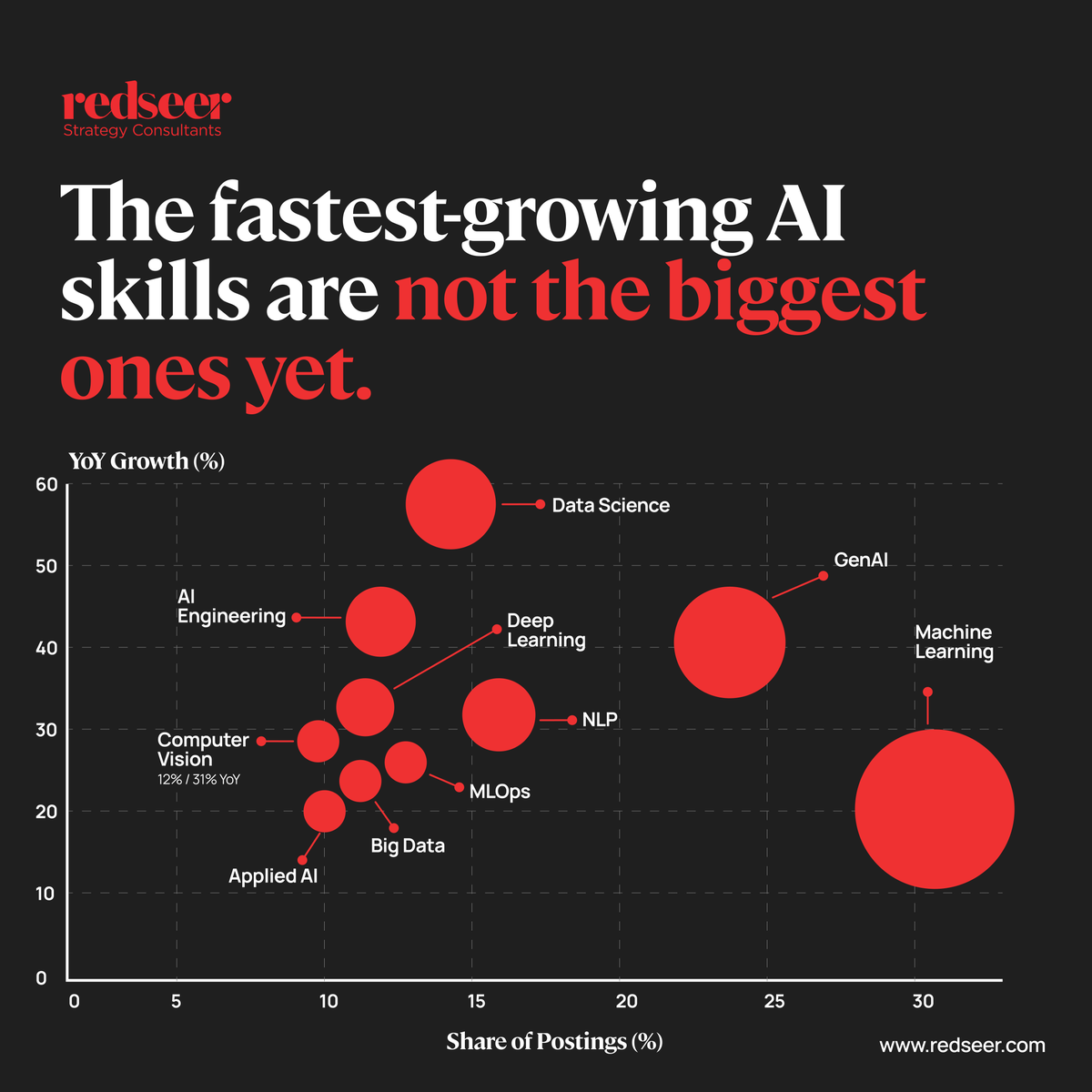

India's AI hiring has grown 6x since 2019, but the fastest-growing skills aren't the biggest ones.

Data Science, AI Engineering and Generative AI are reshaping talent demand and, with it, the future of workplace strategy.

Read more from https://t.co/6Wqd5hwzjT

AI is not just reshaping who companies hire. It is reshaping the space they hire them into.

Our Associate Partner Chhavi Singh spoke to ET HRWorld on how AI-led teams are pushing enterprises toward "core plus flex" workplace models.

Full report - https://t.co/nt2S62u0qM

Markets no longer wait for certainty. Categories get rewritten in quarters & AI compresses every cycle. Strategy can't stay theoretical, it has to move at market speed.

Redseer - Guiding through critical decisions in disruptive markets.

#RedseerConsulting

AI doesn’t level the field. It widens the gap.

More data builds better models, attracts more advertisers, and creates even more data. The leaders keep pulling ahead. Execution speed is the new moat.

Full report here: https://t.co/6akTeNtOco

First, "AI" in advertising isn't one thing. It's three.

i. ML: predicts, ranks, and scores. Cheap and mature.

ii. GenAI: writes and designs on demand. Scaling fast.

iii. Agentic AI: plans and acts on its own. Still early.

Different costs, different jobs, different winners.

India sits at the centre of building this stack.

The global AI ad infrastructure is engineered here. AdTech roles pay 2-4x local IT salaries, and home-grown players like InMobi and Affle now operate across 50+ countries from an India base.

Global advertising spends just crossed $1 Tn and AI is about to rewrite it all.

For 30 years, every adtech shift added a new layer, AI is the first to rewrite them all at once: targeting, creative, bidding, measurement & the transaction itself.

A thread 👇

#GenAIAds#Redseer

AI doesn’t level the field. It widens the gap.

More data builds better models, attracts more advertisers, and creates even more data. The leaders keep pulling ahead. Execution speed is the new moat.

Full report here: https://t.co/6akTeNtOco

India sits at the centre of building this stack.

The global AI ad infrastructure is engineered here. AdTech roles pay 2-4x local IT salaries, and home-grown players like InMobi and Affle now operate across 50+ countries from an India base.

India is now #2 globally in AI talent concentration, growing 2.2x since 2019 on a workforce base far larger than UAE. AI isn’t reducing office demand, it’s increasing collaboration. By 2030, AI could drive ~79 Mn sqft of new office demand across India.

Quick commerce signals consumer mood early. Sunscreen in March: units up 1.8x vs Jan, GMV up 1.5%, price per unit down. More buying, lighter spend. Trial packs drive easy adds. Platforms are priming demand before peak summer. Volume leads value, spend likely to follow.

Quick commerce hit $13–14Bn in FY26 (~17% of online retail). It leads online grocery (~70%), but grocery is just ~2% of total retail. In high-value categories, penetration is <5%. The real opportunity lies ahead. Can it scale beyond convenience into discovery-led segments?

Premium India is now a defined geography, not a persona. By FY31, gated communities could drive $900B consumption at 15% growth vs 9% urban. 32M households, ~$15k per capita income. Clustered, connected, and directly reachable within a single ecosystem.

https://t.co/4MykJWmC6i

Challengers grew from ~12% to ~25% of quick commerce in a year, scaling 1,800+ dark stores. Stronger execution across supply, assortment, conversion, UX, and pricing is driving faster growth than the market.

Catch-up phase or lasting shift? Benchmarks: https://t.co/dDNQT5fUNr