SHOP-focused REITs have lagged over the past few sessions—and again today—while the broader REIT sector has been strong, especially Hotels and Offices. This might be the start of sector rotation as investors trim SHOP names trading at elevated valuations after their strong run.

Fundamentals in senior housing remain strong, so I see this as a setup for better dip-buying opportunities ahead. Watching $NHP, $DHC, $WELL, and $VTR, in particular.

On a mixed market day, $EQIX is rising notably—up around +2.5% and closing in on its all-time intraday high of $1,128. I strongly prefer $EQIX and $IRM over other non-REIT data center plays, including the neoclouds.

It’s no surprise that current forecasts project explosive data center growth, but those projections typically bake in both rising AI demand and today’s hardware constraints. If we take a very optimistic view on innovations in model techniques, chips, and networking, we might ultimately need far less physical footprint overall. What ultimately matters is compute and power density.

In that world, smaller efficient colocation data centers around city centers might be far more valuable than gigantic state-of-the-art facilities in remote areas—especially once most training shifts to space and inference remains increasingly latency-sensitive.

@lebron_ex Investing in REITs over the last few years has been like waiting to be remembered while others prosper. In my experience, it’s not a straightforward “set and forget” strategy. Perhaps REIT ETFs might be easier and potentially safer, but then where’s the fun? 🙂

@ruimarques84 Profit-taking and a preference for data center names — I’m not particularly excited about MFR in general, but I may get back in on significant dips.

Walmart paid $440 per square foot—understandably expensive given the exceptional specs and premium location.

Cold storage REITs have faced headwinds recently, but at the end of the day, the fundamentals win out. If you need it, quality cold storage isn’t always easy to come by—it’s insanely expensive to build, and supply has been extremely tight, especially in areas like SoCal. I hold $LINE and $COLD—I like $LINE in particular as a long-term investment.

Hotel/lodging has been one of the hottest REIT subsectors, and all 15 REITs in the sector are trading above their 50-day SMAs. This reflects strong sector-wide momentum driven by solid earnings and optimism around the World Cup.

Hotel REITs were (and still are) among the cheapest REIT sectors, alongside offices. I hold $APLE, $PEB, and $HST—their stock prices have appreciated between 25% and 37% YTD. In particular, $APLE, which is one of my core positions, is now delivering material returns after heavy DCA over the last three years—complete with meaningful monthly dividends.

Nibbling on $GFS (Global Foundries). It’s one of nine quantum computing companies receiving part of the $2B funding from the Trump administration ($375M allocated to $GFS). More importantly IMO, the company recently launched its silicon photonics platform, which is gaining traction as a next-gen AI scale-up architecture.

The stock has already run up ~160% YTD, but after being mostly flat for the past few years, the long runway in both photonics and quantum computing makes $GFS another compelling asymmetric risk/reward setup. I’m considering trimming $NBIS a bit to buy more $GFS and $INTC. I prefer data center REITs like $EQIX and $IRM over neoclouds.

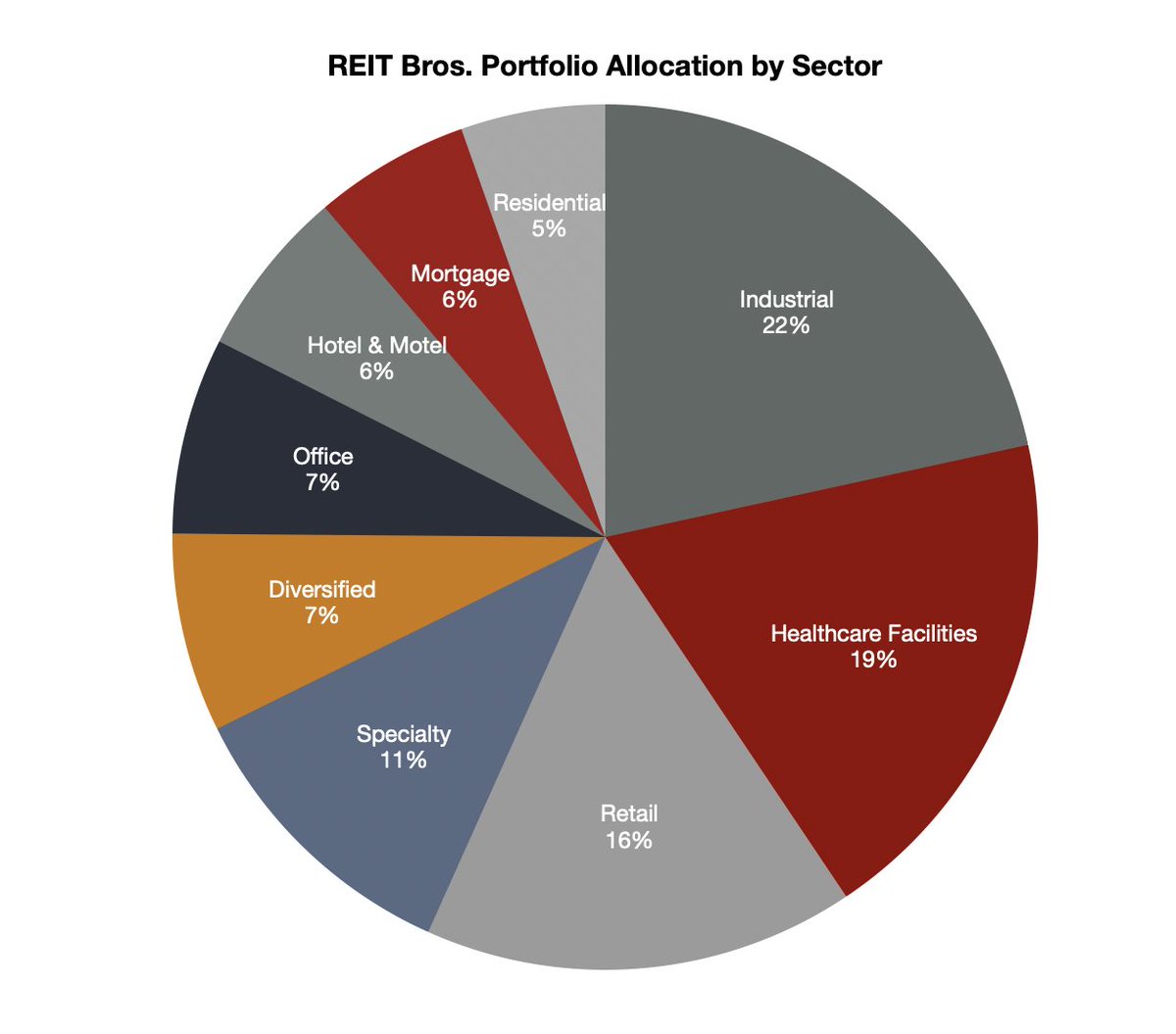

I find $GOOD (Gladstone Commercial) interesting. It’s a small-cap diversified REIT with a primary and growing focus on industrial properties. Industrial assets now comprise 69% of the portfolio (up from 35% in 2018), while office spaces account for 28%. The stock seems heavily discounted due to this lingering office exposure.

As of Q1 2026, overall occupancy stands at 98.7% (99.8% for industrial and 91.4% for office). The stock pays a monthly dividend yielding over 9%. While its 5-year total return is negative (roughly –7%), the 10-year total return is about +70% (+5.5% annualized), which is respectable given the office headwinds.

Its strategy mirrors $OLP, another diversified REIT with heavy industrial exposure (~80% of its portfolio) and a 7.7% dividend yield. Other comparable names increasingly pivoting toward industrial real estate include $GNL and $BNL. I’ve maintained a tiny position in $GOOD since 2022 (~0.2% of the portfolio), and I am considering materially increasing it.

I started a small position in $BXDC with a cost basis of $22—paying a 10% premium for a business that currently has no operating business! It is a blind-pool equity REIT that plans to acquire and operate “mission-critical” data center properties. According to the IPO prospectus, the mission-critical nature of these assets means tenants prioritize operational reliability over cost considerations. Historically, several REITs have launched successfully as blind-pool equity vehicles—most notably $TRNO, $PEB, $ROIC (acquired by Blackstone in 2025), and $CHSP (acquired by $PK in 2019).

I expect the majority of BXDC’s acquisitions will come from other Blackstone affiliates—Blackstone is already one of the world’s largest data center operators. While this setup means there are no guarantees that the transactions will be fully arm’s-length, it potentially gives BXDC a strong and reliable acquisition pipeline. Currently, $BXDC holds roughly $1.9 billion in net IPO proceeds in cash, along with an undrawn $1.0 billion credit facility. No acquisitions have been announced yet.

Blackstone and Google recently announced a major JV (literally days after BXDC’s IPO) in which Blackstone provides the infrastructure and capital, while Google contributes its TPUs and ecosystem. The JV targets its first 500 MW of capacity online in 2027, with plans to “scale significantly” beyond that. I wouldn’t be surprised if some of BXDC’s future acquisitions come from this JV via sale-leaseback structures.

If BXDC ends up with de-risked, income-producing assets backed by long-term triple-net leases to high-credit-quality hyperscalers like Google, it would be a major positive catalyst. This thesis is likely to play out over the next 1 to 5 years. That said, if the AI boom turns out to be a bubble and eventually bursts, $BXDC could end up serving as exit liquidity for Blackstone. Overall, I see this as a high-risk, high-reward setup that is worthwhile to bet on with a small position.

Watching $BXDC, which is up roughly 10% since its IPO at $20 on May 14.

It currently has no assets and no publicly announced deals. It might essentially serve as an eventual exit strategy and/or capital recycling channel for Blackstone. There are protections against dumping underperforming assets: any related-party sale must be approved by a majority of independent directors and be on terms “no less favorable” to $BXDC than what it could obtain from a third-party seller. That said, this does not guarantee true arm’s-length best-price outcomes. At least in the short to medium term, Blackstone should be incentivized to allocate top-quality performing properties into the REIT to get it off to a strong start.

The company is externally managed by a Blackstone affiliate, and none of the $BXDC executives have hands-on technical or operational expertise in AI or data center infrastructure. The recent announcement of Blackstone’s (not $BXDC) partnership with Google to launch a new AI infrastructure company could be a tailwind for $BXDC down the road.

I see it as a defensive move amid rising political scrutiny on housing. Their synergies are real—albeit not massive—but the deepened coastal concentration (roughly 90% of NOI for the combined company) is a double-edged sword. Regulatory and execution risks are also not insignificant.

While a clear institutional multifamily leader with durable competitive advantages is intriguing, I’ll watch from the sideline for now. I recently exited both names.

$AVB $EQR

🚨 AvalonBay Communities and Equity Residential Announce $69B Merger of Equals 🚨

Huge news shaking up the multihousing sector today as $AVB AvalonBay Communities and $EQR Equity Residential have officially announced a definitive agreement to combine in an all-stock merger of equals.

📊 The Combined Powerhouse by the Numbers

* $52 Billion pro forma equity market capitalization

* $69 Billion total enterprise value

* 180,000+ rental apartments across premier U.S. metro markets

* $4.4 Billion currently under construction (approx. 10,800 apartments)

* $175 Million in gross synergies ($125 million net after real estate tax reassessments)

* 51.2% / 48.8% ownership split, with AVB shareholders receiving 2.793 shares of EQR stock per AVB share

🎯 Key Strategic Takeaways

* The new entity aims to leverage combined investments in AI, automation, and centralized services to drive margin expansion and enhance the resident experience.

* Expanding regional density further unlocks hyper-local, neighborhood-based operations, reducing the cost-to-serve while increasing Net Operating Income (NOI).

* Boasting dual A3/A- credit ratings, the combined company secures a formidable cost-of-capital advantage and a combined $2 billion in annual cash flow for self-funded growth.

* With a massive $4.2 billion development rights pipeline, the entity is positioned to be a leading creator of new market-rate and affordable housing supply.

* Exceptional scale allows for highly disciplined, data-driven capital allocation across development, acquisitions, and strategic investments to capture the highest risk-adjusted returns.

💰 Dividend & Investor Impact

* The combined company expects to deliver an initial annualized dividend of $2.81 per share.

* This initial dividend is equivalent to EQR’s existing dividend per share, representing a yield increase over AvalonBay’s current payout level.

* Both REITs intend to maintain their regular, independent quarterly dividend payments through the completion of the transaction.

👥 Leadership & Governance

* Benjamin Schall (President & CEO of AvalonBay) will serve as President, CEO, and Trustee of the combined company.

* Steve Sterrett (current Lead Independent Trustee of Equity Residential and former long-time CFO of Simon Property Group) will serve as Chairman of the Board.

* Mark J. Parrell (CEO of Equity Residential) will retire at transaction close after an incredible 27-year legacy with EQR.

* The Board of Trustees will initially consist of an even split—7 existing trustees from EQR and 7 existing directors from AVB.

* The entity will maintain a meaningful presence in both Arlington, VA and Chicago, IL, operating under a entirely new name to be announced at closing (expected H2 2026).

https://t.co/n4ASppW8YR

Watching $BXDC, which is up roughly 10% since its IPO at $20 on May 14.

It currently has no assets and no publicly announced deals. It might essentially serve as an eventual exit strategy and/or capital recycling channel for Blackstone. There are protections against dumping underperforming assets: any related-party sale must be approved by a majority of independent directors and be on terms “no less favorable” to $BXDC than what it could obtain from a third-party seller. That said, this does not guarantee true arm’s-length best-price outcomes. At least in the short to medium term, Blackstone should be incentivized to allocate top-quality performing properties into the REIT to get it off to a strong start.

The company is externally managed by a Blackstone affiliate, and none of the $BXDC executives have hands-on technical or operational expertise in AI or data center infrastructure. The recent announcement of Blackstone’s (not $BXDC) partnership with Google to launch a new AI infrastructure company could be a tailwind for $BXDC down the road.

While it may leave a bad taste in the mouth for some, the case was basically thrown out on a technicality. In a sense, the ruling is a major de-risking event for the entire AI supply chain—especially chip makers, hyperscalers, and data centers. The immediate uncertainty is off the table, although an appeal remains possible.

BREAKING: Jury unanimously finds OpenAI not liable in Elon Musk lawsuit that alleged breach of charitable mission, saying statute of limitations bars the claims https://t.co/nr3evvDIpR

Once carriers start leveraging the technical feasibility and cost advantages of satellite technologies, they will expand it to urban settings. Within five years, phones will connect natively worldwide, without dead zones and roaming charges.

That said, cell towers should still remain necessary with D2C technology because of issues with penetration, latency, bandwidth, and even device battery drain. While the existence of rapidly improving alternatives will erode pricing power and stifle growth for cell tower REITs ($AMT, $CCI, $SBAC), some of them might be good investments for stable income once stock prices come down enough. I have no position for now.

Verizon, AT&T and T-Mobile said on Thursday they agreed in principle to form a new JV with an aim to address long-time coverage gaps, especially in rural areas, by using satellite-based technologies.

This comes as the industry increasingly worries about what Elon Musk’s @Starlink Mobile might do to shake up the terrestrial mobile space.

Musk has said he’s not going to put the U.S. terrestrial carriers out of business, but at the same time he’s expanding Starlink and buying up more spectrum...