DevvExchange vs Traditional & Crypto Exchanges – The Winner is Clear. 🏆

@DevvExchange isn’t just another exchange—it’s a paradigm shift. 🚀

🔜 Launching in H2 2025 $DevvE @DevveEcosystem#CryptoRevolution#FutureOfFinance

$BTC $ETH $XRP $SOL $BNB $UNI $HYPE

🚨 I just learned about a concept, I can't stop thinking about.

The Four Burner Theory.

It destroyed Elon Musk's first marriage.

It explains why Bezos is jacked but divorced.

And why Zuckerberg has no real friends.

Once you understand it, your life will never be same:🧵

Today is the official unveiling of my new AI business Fias! Check it out at https://t.co/GmwPKRYNjg. I've been involved with AI for 30 years and have built a powerful blockchain technology (DevvX) over the past 10 years. Now I am combining the two, to create a powerful monetization platform for AI, addressing arguably the biggest challenge in the space. If you want to get into the AI space, you have to build something that won't simply be crushed by the big players. The Fias architecture fits that description with a new approach and significant competitive advantages over all else in the AI space.

Most people think price in crypto is the result of organic buying and selling.

It isn’t.

Price is a negotiation between liquidity and intent - and in crypto, liquidity is thin, fragmented across countless CEXs/DEXs, and remarkably easy to influence.

A market maker isn’t a shadowy villain with a big red button. In theory, their job is simple: provide bids and asks so trading can happen smoothly. In practice, where that liquidity is placed, how dense it is, and when it’s added or removed matters more than almost anything else.

In traditional markets, liquidity is deep, regulated, and spread across massive venues. In crypto, liquidity often lives in a few pools with large gaps in between. When they want price to move, it doesn’t glide - it jumps. It falls through empty space or accelerates upward once resistance disappears.

This is how price can be pushed down without massive selling. Pull liquidity below price and even moderate sell pressure can cause a cascade. The chart looks like panic, but structurally it’s just gravity doing its thing.

The same mechanics work in reverse.

Stack liquidity strategically, absorb sells, and allow buyers to hit thin air above. Once overhead liquidity is removed or exhausted, price doesn’t need explosive demand to rise - it simply travels to the next available pocket. That’s how you get slow, controlled climbs that suddenly turn into vertical moves with no obvious catalyst.

Derivatives amplify all of this. Perpetuals introduce leverage, leverage creates liquidation levels, and liquidation levels become magnets. When too many traders lean the same way, price doesn’t move because the market is “wrong.” It moves because clearing those positions is profitable and mechanically easy to the powers that be.

This is why you see clean stops run below support and euphoric breakouts above resistance that immediately accelerate. The market isn’t reacting - it’s being guided through liquidity.

To newcomers, this feels fake.

Compared to traditional equities, it kind of is.

But that doesn’t make it evil or unwinnable. It just means you stop asking why price moved and start asking who benefited from the move, and what liquidity was cleared or created as a result.

Once you understand that price follows liquidity - not narratives, not indicators, not opinions - charts stop looking as chaotic.

They start looking intentional.

And once you see that, you’re no longer trading the story.

You’re trading the structure.

🫡 From the depths —

The White Whale 🐋

Everyone is suddenly back to debating who to unfollow because this whole space has turned on itself yet again, so here is my take…

I usually stop following accounts that pump out views when everything is going up and then disappear the moment things turn down, right when the community needs them most.

Most step back because they do not want to be ridiculed. I get it. None of us do. But if you are in this game, it comes with the territory. You have to learn to take the hits...

I have been doing this a long time. I have been more right than wrong over the years, but I have had my fair share of bad takes too. That is the nature of markets. They humble everyone. If you do not like these insights, unfollow. Simple.

What counts is having the courage to stand up, be brave, and be bold when others are fearful. That is how you actually show up for the community when it matters most.

Right now, almost nobody wants to take a view. Everyone has their head buried in the sand and a bullish argument is the last thing anyone wants to hear.

When the market is falling like this it becomes almost impossible to separate signal from noise because every narrative is competing for emotional bandwidth. That is exactly why I am posting this. It is not a call and it is not an opinion. It is fact. Objective, not subjective, is what we need right now.

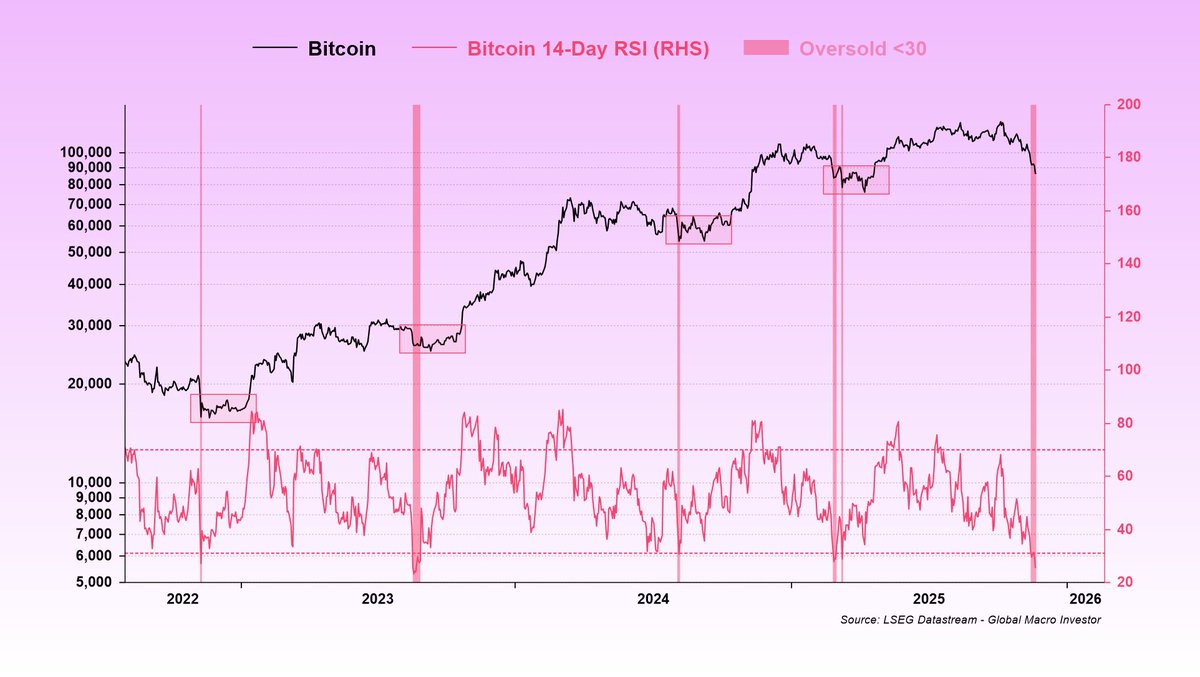

This market is oversold, but bottoms take time to form (chart 1).

When you look back at past oversold conditions, the path of least resistance has on average been higher following the last five times Bitcoin’s RSI dropped below 30 since this bull market began in Q4 2022 (chart 2).

Important note: If you believe the bull market is finished and we are entering twelve months of pain, these charts are not for you. Move along...

I wanted to give everyone something meaningful, a gift…

This comes from Global Macro Investor (GMI) and a deep, long-running body of research developed by @RaoulGMI and myself.

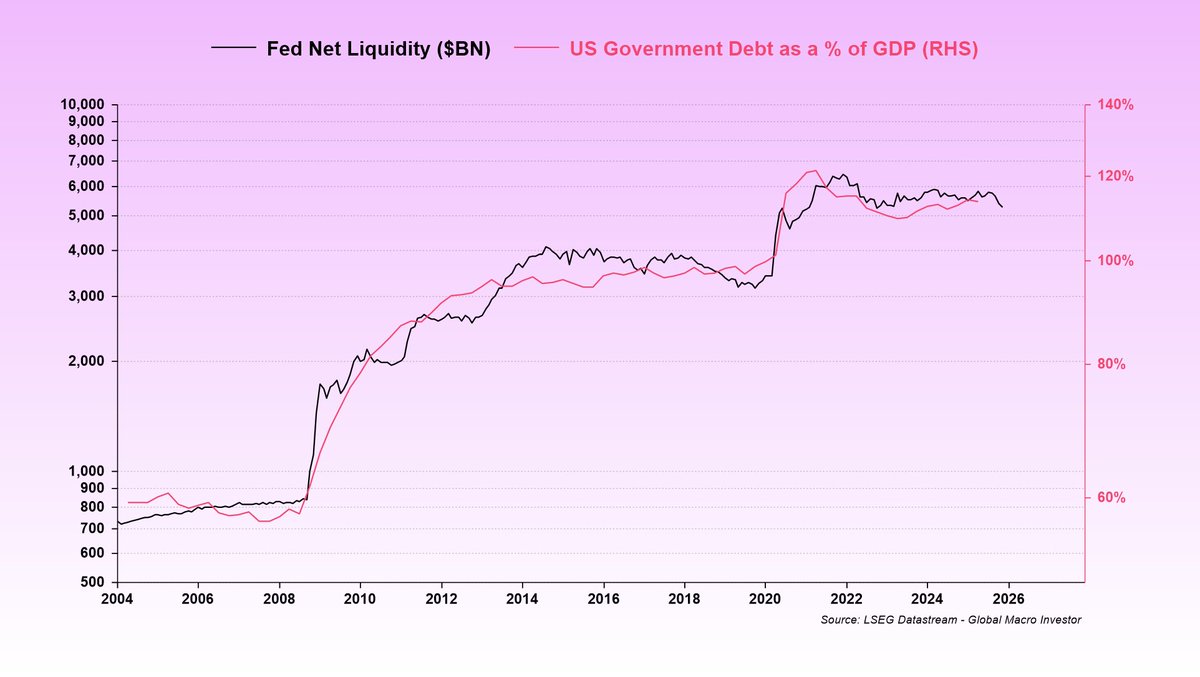

Many of you already know The Everything Code, which is our framework for understanding the macro landscape and why major central banks are debasing their currencies to manage aging demographics and overwhelming debt loads.

I call this a gift because these four charts, while only scratching the surface of The Everything Code, give you the big-picture context you actually need in moments like this.

They stop you from getting lost in every Bitcoin pullback and explain why Raoul and I never panic, even when, to borrow one of his expressions, everyone’s acting like monkeys throwing poo at each other.

Once you understand The Everything Code, you stop trading short-term noise and expand your time horizon. You cannot unsee it.

The starting point is what we call The Magic Formula:

GDP growth = population growth + productivity growth + debt growth.

Population growth and productivity growth have been falling for decades. Debt growth is the only thing filling the gap.

The private sector has been deleveraging since 2008, mainly households, but debt levels are still around 120% of GDP. The public sector sits at roughly the same level.

Here’s the problem…

If the government is running debt at 100% of GDP and the private sector is sitting on another 100%, and for simple math we call rates 2% even though they are really closer to 4%, then the entire 2% trend growth of the economy is being consumed by servicing private-sector debts. That is a completely unproductive use of GDP. And then there’s the issue of public-sector debts. There’s just not enough organic growth to service the existing debt load.

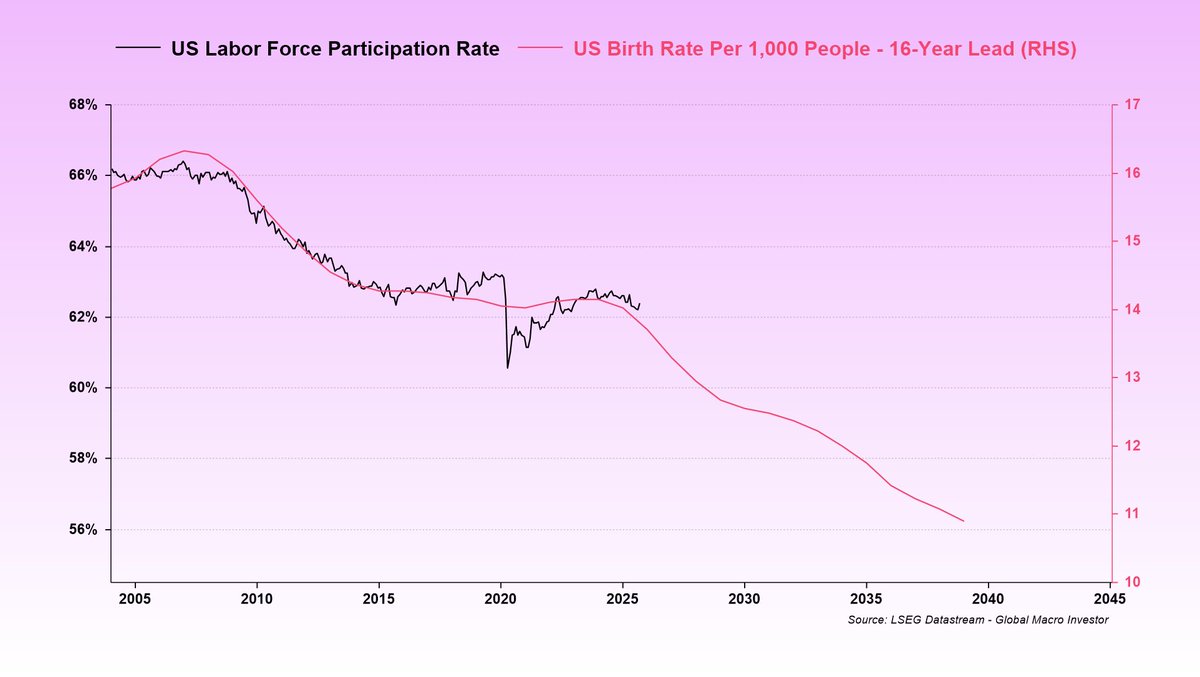

To understand why this dynamic persists, you need demographics.

Birth rates peaked in the late 1950s and have been declining ever since. This shows up about sixteen years later in the labor force participation rate as each generation enters the workforce (chart 1).

That means the labor force participation rate is not going to rise any time soon. It is set to keep drifting lower. This is a structural problem.

Aging populations, falling birth rates, and rapidly expanding automation make the backdrop even more deflationary. AI and robotics are replacing humans at scale, and we are only at the beginning. This reinforces the need for ongoing stimulus to keep the system functioning.

With weak population growth and sluggish productivity, the only way to keep GDP expanding is through debt.

Now here’s where it gets interesting…

Government debt growth is completely offsetting the demographic decline and policymakers know exactly what they are doing (chart 2).

And what happens next?

All debt growth in excess of GDP gets monetized (chart 3).

Basically, since 2008, magic money has effectively been paying the interest. Governments issue new debt to cover old interest, and once rates fall enough, central banks absorb it onto their balance sheets.

So to wrap this up, demographics drive the decline in the labor force. Governments offset that decline with more debt. That debt eventually gets monetized through quantitative easing (QE) style operations, not always directly by the Fed, but through the coordinated ecosystem of the Fed, the Treasury, and the banking system. And the bottom line is that there’s still a massive wall of interest that needs to be monetized, far more than GDP can ever cover. Liquidity is literally the only game in town.

And what thrives in a world of perpetual debasement? Bitcoin (chart 4).

I know this correction has been painful, but it’s all part of the journey. These periods feel brutal in the moment, then they fade and the trend resumes. This too shall pass…

To quote Walter White from Breaking Bad, later echoed by @LynAldenContact, nothing stops this train.

MOAR COWBELL (liquidity) = number go up over time. Zoom out and be more bullish…

1. In 1965, Rosenthal ran an experiment that many later tried to discredit because the results were inconvenient.

Participants were told that certain people in the study were "more gifted," even though they had been chosen at random.

Within eight weeks, those "gifted" participants started acting as if they genuinely were superior, they made decisions faster, doubted themselves less, and their performance increased by almost a quarter.

2. Years later, researchers in Zurich repeated the experiment on adults. One group was told they would "perform better" because they supposedly had a "hidden cognitive resource." The tests were identical to the other group's, but within 40 minutes their brains began producing answers 89% faster. The researchers said: "We didn't increase their abilities, we changed their expectations of themselves."

3. One participant admitted he felt a clarity he hadn't experienced in years: "I just thought I could, and then I could." Rosenthal insisted there was nothing mystical about it: people act not from their actual abilities, but from what they believe is possible for them. Give someone a version of the future that feels real, and the body begins to behave as if it has already happened.

4. The darkest conclusion from the experiment: the Rosenthal effect works in reverse too. If someone is made to believe they are "difficult," "faulty," or "a failure," the brain starts confirming that script, as if it were testing a hypothesis planted in childhood. Neuroscientists have shown that negative expectations from others slow neural transmission almost as much as chronic fatigue.

5. At a Harvard conference, a psychologist said a line that made the room go silent:

"We become who others think we are, unless we realize in time that this voice isn't ours." He added that when a person changes not their motivation, but their forecast of themselves, the psyche reorganizes instantly, as if it receives a new operating instruction.

Have you noticed that the biggest turning points in life happen right after you stop believing someone else's prediction of who you are?

We may never cross paths again. Follow The White Rabbit 🐇.

🧵 **THE MOST TERRIFYING TRUTH ABOUT YOUR MONEY AND THE ONE TECH THAT FIXES IT**

1. Let’s get real.

Right now, if someone gets your phone, your 2FA, or tricks you into a fake login…

Your bank can say:

“You authorised it.”

Refund denied.

Savings gone.

Life ruined.

This is finance today.

2. And crypto is even worse.

Lose your seed? Gone.

SIM swap? Gone.

Clipboard malware? Gone.

One click can erase a decade of work.

Crypto has no safety net.

None.

And that’s why many people and serious institutions stay far away.

3. Now imagine something nobody thought possible.

A hacker steals:

Your device

Your passwords

Your seed phrase

Your private key

Your PIN

He signs a full wallet drain…

And still cannot take your real wealth.

Because the chain itself blocks the transaction.

Holds it for days.

Lets you cancel it instantly.

And the thief walks away with nothing.

This has never existed in TradFi.

It has definitely never existed in crypto.

Until now.

4. The setup is stupidly simple.

Your $DEVVE wallet is born with a special NFT that defines:

How fast funds can move

How long big withdrawals wait

Recovery rules

Freeze rules

Spending limits

You put 95 percent of your net worth in the protected wallet.

You keep 5 percent liquid.

If the protected wallet gets drained?

The chain freezes it.

You cancel the action.

You move the funds.

Your attacker gets zero.

This isn’t a smart contract.

This isn’t a custodial service.

This isn’t MPC.

This is protocol level defence.

5. Real world examples that would save real people.

House burns down. Seed phrase melts.

Trigger recovery → funds move safely.

If a hacker triggered it → you reverse it.

SIM swap. Phone stolen. Keys stolen.

Funds sit locked.

You cancel.

You lose nothing.

Thief forces you to unlock your phone.

He drains your wallet.

You get home, hit cancel, move protected funds.

He goes home empty handed.

TradFi can’t do this.

Crypto can’t do this.

Only one architecture can.

6. Institutions need this even more than retail.

A bank cannot allow a customer to self custody if:

A stolen phone can drain everything

A SIM swap can wipe out a retirement

A bad signature is irreversible

A compromised laptop ruins lives

A lost key means permanent loss

That is legal liability.

Regulatory exposure.

Operational disaster.

Reputation meltdown.

Institutions need chain enforced guardrails.

Not trust.

Not hope.

Not multisig.

Not MPC.

Not “sorry contact support”.

Actual safety.

7. How a bank actually deploys this.

You open a crypto enabled account.

The bank instantly creates a native $DEVVE wallet.

The wallet has rules baked in at creation:

Automatic timelocks

Withdrawal delays

Emergency freeze

Recovery paths

Fraud rollback window

If your device is hacked?

Funds lock.

You reverse it.

Bank has zero liability.

Regulator approves it.

Everyone sleeps at night.

This lets banks finally offer real self custody without actually taking custody and without the risk of customer disasters.

This is impossible on any other chain.

8. This is stronger than TradFi.

Stronger than DeFi.

Stronger than anything.

Banks cannot reverse a fraudulent authorised transfer.

Crypto cannot undo a malicious signature.

Smart contracts cannot save you from a stolen key.

MPC cannot stop a forced transaction.

Multisig does not help if the user signs under duress.

Chain enforced safety is the only thing that works.

And one chain built it into its DNA.

9. And here’s the killer point.

Crypto will not go mainstream because of speed.

It will not go mainstream because of TPS.

It will not go mainstream because of cheap gas.

Crypto will go mainstream when people realise:

“I literally cannot lose everything.”

When institutions realise:

“We can offer digital assets without legal exposure.”

When regulators realise:

“This system protects consumers by default.”

Only one chain solves the problem that stops crypto from reaching billions.

And this is just one of its features.

One.

@DevveEcosystem@DevvExchange

I am betting my money on the fact that this is a mere deep correction in Crypto and not the end of it.

All dooms day scenario are wrong. All deep dips on Bitcoin are for buying.

🚀 $5,000 GIVEAWAY ALERT! 🚀

If $devve hits $20 before December 31st, 2025, Five lucky winners will each receive $1,000! 💸

To enter:

1️⃣ Follow me

2️⃣ Retweet this post

3️⃣ Tag $devve

Don’t miss your chance! 🔥 #CryptoGiveaway@DevveEcosystem#crypto#Giveaway

Good luck! 🍀

🚨 The Credit System Devve Is Building Makes Every DeFi Lender Look Like a Toy

Everyone’s cheerleading $Aave's institutional offering Horizon hitting $520M deposits.

$SYRUP bragging about half a billion.

RWAs “popping off.”

TVL charts everywhere.

None of this is even in the same galaxy as real institutional credit. And $Devve isn’t competing with DeFi, it’s coming to replace the rails it sits on.

Let me explain why the entire market is asleep.

✅ The Numbers That Make $Aave Look Like Monopoly Money

Here are the “big leagues” DeFi thinks it’s entering:

– DeFi lending TVL: ~$55B

– $Aave (all versions): ~$26B

– Maple: ~$500M

– Aave Horizon: $520M

Now here’s finance:

– Repo markets: $12–15 TRILLION per day

– Securities lending: $3 TRILLION

– FX swaps: $3 TRILLION per day

– Prime brokerage + margin: multi-trillion

Aave Horizon celebrating $520M is like bragging your garden hose can fill an ocean.

Meanwhile, $Devve is building a water distribution system for the entire planet.

✅ Devve’s Credit Engine Is Not DeFi

It’s the First Blockchain That Eliminates Settlement Risk Entirely

Every DeFi lending system today depends on:

– probabilistic settlement

– oracle windows

– liquidator networks

– collateral buffers

– pre-funded liquidity

– smart contract complexity

– chain congestion

– siloed state

– out-of-band reconciliation

Institutions CANNOT run trillions on that.

$Devve’s credit system does the opposite:

✅ Mathematically Instant Settlement (MIS) — instant, risk-free, irreversible

✅ Contingent Transaction Sets (CTS) — atomic multi-leg credit

✅ Deterministic finality across shards

✅ No oracles

✅ No liquidation bots

✅ No bridge risk

✅ No pre-funding

✅ Protocol-level fraud/theft/loss

✅ REST + FIX rails (institution-grade)

✅ Interest accrual at the settlement layer

✅ Atomic margining across markets

This is not Aave 2.0.

This is CME Clearing + DTCC + Prime Brokerage mashed into a single deterministic network.

✅ And Here's the Insane Part:

The Exchange Partner Is Already Signed.

Delubac Is Already Public.

More Are Coming.

This isn’t “if an institution signs.”

They already did.

Let that sink in:

A credit engine designed for trillion-dollar flows is about to go live with real institutional connections.

Crypto has never seen anything remotely like this.

✅ The TVL Potential Is Stupidly High

Realistic projections:

📌 Year 1: $75B–$100B

📌 Years 2–3: $300B–$500B

📌 Long-term: $1–2 TRILLION**

Aave Horizon at $520M isn’t competition, it’s background noise.

And that’s BEFORE:

– tokenized money markets

– broker-dealer credit lines

– securities lending

– cross-asset hedging

– market maker inventory financing

– multi-venue atomic margining

– exchange settlement networks

– prime brokerage on-chain

$Devve isn’t targeting RWA DeFi.

It’s targeting the entire institutional credit stack.

✅ Devve’s Credit + Exchange Feedback Loop Will Be UNSTOPPABLE

This is where the nuclear part happens:

The exchange feeds the credit system.

The credit system feeds liquidity.

Liquidity feeds the exchange.

Institutions have no choice but to integrate.

$Devve is on track to become the first blockchain to recreate that flywheel

and improve it with deterministic atomic settlement.

✅ Final Warning to the Market

Everyone is sleeping on the lending/credit side of $Devve.

The exchange is going to be huge, but the credit engine is the thing that institutions cannot operate without.

$Aave, $SYRUP, $SOL, $Sei, $AVAX, $POL, $KTA:

none of them can do deterministic, atomic, riskless credit across markets.

$Devve can.

And when institutions start running serious flows through it,

the TVL will make everything in DeFi today look like pocket change.

Read this again in 12 months.

Screenshots will age like diamonds.

@DevveEcosystem@DevvExchange

🚨 People Still Don’t Understand What $Devve Is About to Trigger 🧵🔥

Crypto is obsessed with $100M → $1B “RWA narratives.”

Meanwhile $Devve is sitting under $50M, while preparing to power the settlement rails of a global exchange.

And the thing nobody gets?

One exchange integration isn’t “one partner.” It’s the first domino in an unstoppable chain reaction.

Let’s talk about it. 👇

1️⃣ Exchanges Don’t Move Alone — They Drag the Whole Industry

If an exchange upgrades to real-time, deterministic settlement using $Devve:

Brokers MUST integrate.

Custodians MUST integrate.

Market makers MUST integrate.

Liquidity partners MUST integrate.

If they don’t? They lose:

✅ order flow

✅ spreads

✅ clients

✅ competitive edge

No broker wants to be the one settling in 2 days when their competitor settles instantly.

$Devve doesn’t spread because people choose it.

$Devve spreads because market incentives FORCE it.

2️⃣ This Creates a Snowball That CT Completely Underestimates

Once brokers onboard $Devve rails to access the exchange:

→ They start using $Devve settlement for more assets

→ Custodians follow because their clients demand it

→ Market makers follow because flow moves where settlement is fastest

→ Other exchanges start migrating because liquidity pools shift

→ More jurisdictions begin spinning up shards

→ It becomes the de facto standard before anyone realizes it

This is how global adoption actually happens in finance.

Not hype.

Not vibes.

Incentive pressure + competitive survival.

3️⃣ This Is Why a Single Exchange Integration Is Basically a Nuclear Catalyst

Crypto looks at $Devve and sees a “$40M microcap.”

But zoom out:

Traditional market infrastructure is a $20–$100 TRILLION problem.

Most blockchains are fighting over scraps:

$200M TVL → $500M TVL.

Meanwhile $Devve is lining up to serve the entire trading stack:

✅ atomic settlement

✅ deterministic ordering

✅ no bridges

✅ instant reconciliation

✅ global shared rails

✅ across multiple institutions

You know what happens when crypto finally realizes this?

$40M → $400M is a blink.

$400M → $4B is a narrative.

$4B → $40B is adoption.

And no, that’s not hopium — that’s what happened to chains with far less tech and zero institutional alignment.

4️⃣ And Here’s the Funniest Part…

Crypto is out here:

• worshipping $SEI

• chasing $ONDO

• hyping $LINK partnerships

• simping for $KTA

• pretending $CC is “the institutional chain”

While $Devve quietly builds the only settlement architecture that solves what TradFi actually needs.

Not “RWA token wrappers.”

Not “proof-of-concept CBDC demos.”

Not “oracle-mediated approximations.”

Real settlement.

Real atomicity.

Real institutions.

Real use cases.

And it’s STILL sitting under $50M.

That’s not undervalued —

that’s generational mispricing.

✅ Final Thought

Most people will only understand $Devve after the first exchange goes live.

What they don’t see today:

➡️ That one integration forces brokers.

➡️ Brokers force custodians.

➡️ Custodians force liquidity partners.

➡️ Liquidity partners force more exchanges.

➡️ More exchanges force cross-border adoption.

This is how rails take over. Slowly… then all at once.

When this clicks, $Devve won’t be a $50M project. It won’t even be a $500M project.

It’ll be the settlement backbone everyone wishes they bought early.

And right now?

It’s still early.

Ridiculously early.

@DevveEcosystem@DevvExchange

Every major exchange, bank, and clearing house is built on one assumption: that settlement takes time.

DevvX is making this assumption obsolete.

New technology changes the foundation of global finance.

👇