The Cheapest Market No One Wants to Touch.

A note on JCI, the rupiah, and the silence from Senayan

On a pure valuation basis, the Indonesian equity market right now is one of the most asymmetric setups I have seen in this region in over a decade. A 40% drawdown from peak. Multiples that would make a value investor weep with joy. Banks trading at fractions of book. Commodity names priced like the cycle is permanently over. If you put this data in front of any analyst at a different house with no context at all, they’d be banging the table to go long.

And yet here they are. Not buying.

Why Cheap Is Not Enough

Valuation is a mirror. It tells you what the market thinks today. What it cannot tell you is when the story changes. And right now in Indonesia, I cannot point to a single credible signal that the policy environment is improving. Not one. That is the problem.

This is a market that has been repriced by a structural question that nobody in Jakarta seems to want to answer clearly: what is the actual development model this government is running, and who does it serve?

We have watched regulatory uncertainty pile up quarter after quarter. We have watched export policy shift in ways that punish the very sectors that attract foreign capital. We have watched governance at the state enterprise level deteriorate in ways that used to be the kind of thing emerging market investors quietly accepted, until they didn't.

"Cheap markets stay cheap for a long time when the catalyst for re-rating is political. And politics in Indonesia right now is giving me nothing to work with."

The Rupiah and the Silence From Senayan

USD/IDR at 18,050. SGD/IDR at 14,080. These are not numbers you explain away with a Fed rate cycle or global risk-off sentiment alone. The rupiah has been systematically losing credibility because the fiscal and policy signals coming out of Jakarta are, at best, ambiguous. At worst, they are alarming.

What concerns me most is not the exchange rate itself. Currency weakness is manageable. What concerns me is the institutional non-response. The DPR Indonesia's parliament has been conspicuously, almost aggressively, silent. And that silence is doing real damage.

When a currency depreciates this sharply, the population has a right to expect its elected representatives to either explain what is happening, hold the executive accountable, or at minimum ask the hard questions publicly. That is what a functioning legislature does. What we are seeing instead looks like an institution that has either lost the will to check executive power, or has made a quiet political calculation that silence is the safer play.

Neither interpretation is good for country risk. Foreign institutional investors price political risk in ways that go beyond spreadsheets. When we see a legislature go quiet during a macro stress event of this magnitude, the question we ask is: who is actually governing this country, and through what accountability structure? Right now, that question does not have a clean answer.

What Would Change My View

I want to be clear: I am not structurally bearish on Indonesia. The demographic tailwind is real. The commodity endowment is real. The middle class consumption story, however delayed, is real.

What I need to ser is actual evidence that policy is correcting. A credible signal from the executive that investor protection will be respected. A legislature that wakes up and starts performing its oversight function. A Bank Indonesia that is given the operational space to defend monetary credibility without being pulled into political theater. Any one of those three things, if done with conviction, could be the catalyst that re-rates this market fast. Very fast. Because when value this deep meets a credible narrative change, the move will be violent to the upside.

“Bull or bear we all want the same thing.

Indonesia deserves better than this, and I believe it is capable of it.”

God Bless Indonesia

@rickyho_1989 What a valuable insight sir.

Even though people said the stock market is not reflecting the real economy, but i see something forward by partake in the stock market, the foreign investors see the future growth of the country.

Valuation-wise, Indonesia is arguably one of the cheapest equity markets in Asia today. Many well-known blue-chip companies are trading at what can only be described as crisis-like multiples despite maintaining healthy balance sheets, dominant market positions, and attractive dividend yields.

BBCA trades at roughly 11x forward earnings and 2.6x book value. Bank Mandiri trades at around 6x forward earnings and 1.2x book value. BRI trades at approximately 7x forward earnings and 1.3x book value. Astra sits at 6x forward earnings. Kalbe trades at 9x forward earnings. Amman trades at roughly 10x forward earnings. The list goes on.

Many of these companies also offer high single-digit dividend yields, with some names approaching double-digit yields. On paper, this should attract significant investor interest. Yet share prices continue to drift lower.

The obvious question is: where are the buyers? Where are all the investors who have spent years believing Indonesia’s long-term potential? Indonesia’s weight in MSCI Emerging Markets remains only around 0.5-0.6%, remarkably small relative to the size of its economy, population, and long-term growth aspirations.

More importantly, where is Danantara? It was presented as a potential new source of domestic capital and a stabilizing force for Indonesian financial markets. If the local market is trading at distressed valuations, this should be the type of environment where a large domestic institutional investor helps establish confidence.

The problem, however, is that cheap valuation alone is rarely enough. Markets ultimately pay for growth.

Indonesia’s core challenge today is not valuation. It is earnings growth. Aggregate earnings growth for the market has slowed materially, with many sectors struggling to generate meaningful expansion. Compare that with South Korea and Taiwan, where investors are being offered direct exposure to AI, semiconductors, advanced manufacturing, memory, and high-performance computing. Foreign investors are naturally willing to pay higher multiples for companies whose earnings are compounding rapidly.

Currency concerns add another layer of complexity. Investors are not simply underwriting Indonesian corporate earnings. They are also underwriting the rupiah. If currency depreciation continues to offset equity returns, valuation discounts can persist far longer than expected.

There is also a credibility issue that should not be ignored. For years, many foreign investors have complained that parts of the Indonesian market function primarily as distribution channels rather than genuine capital formation venues. Domestic equity sales teams routinely promote names that later become exit liquidity for local institutions seeking to reduce exposure. Over time, repeated experiences like this erode trust.

The persistent allegations of wash trading, questions around effective free float, concentrated ownership structures, and concerns over genuine liquidity have further damaged confidence. Investors do not simply buy low valuations. They buy governance, transparency, liquidity, and confidence in future earnings.

This is why cheap markets can remain cheap for years. A stock trading at 6x earnings can still fall to 5x. Valuation itself is not a catalyst.

The harsh reality is that Indonesia does not have a valuation problem. It has a growth and confidence problem.

Until investors see stronger earnings growth, more credible policy execution, better market governance, improved liquidity, and a clearer path for capital to generate attractive real returns, low multiples alone will not be enough to attract meaningful foreign capital back into the market.

Cheap without growth is a value trap. Cheap with deteriorating confidence is even worse.

Ketika mandat Bank Indonesia (BI) menjadi "mendukung pertumbuhan negara" dan DPR yang mengevaluasi, di situ lah BI kehilangan independensi. Bayangin kumpulan seorang teknokrat dievaluasi oleh kumpulan orang yg duduk di kursi legislatif yang belum tentu capable.

Artinya apa? Di saat negara ingin prioritaskan growth, BI mau tidak mau harus patuh di bawah tuntutan itu, sangat berbeda dengan peran sebelumnya untuk menjaga kestablian Rupiah dan inflasi. Seharusnya ini menjadi alarm besar buat seluruh rakyat yang sadar arah negara kita ini mau di bawa ke mana.

Tentu saya tidak bilang kalau negara ini bakal menjadi ekstrim parah seperti Turki, yang mana bank sentral dievaluasi langsung oleh Presiden. Tapi coba berpikir lagi, di negara tanpa oposisi, siapa yang berani melawan presiden? Legislatif kita sebenarnya sudah mati sejak lama.

Yang jelas, negara ini hanya butuh 20 tahun untuk lupa seramnya Orba karena propaganda belas kasihan dan tingkah gemoy. Sungguh bangsa pemaaf yang sangat pandir. Masing2 dari kita saat ini cuma bisa menyelamatkan diri sendiri, maka dari itu begitu botol (bodoh dan tolol) jika ada seorang mahasiswa yang bilang justru kita itu "Traitor" negara, karena sebenarnya mereka yang berkuasa itu yang ingin menghancurkan Indonesia.

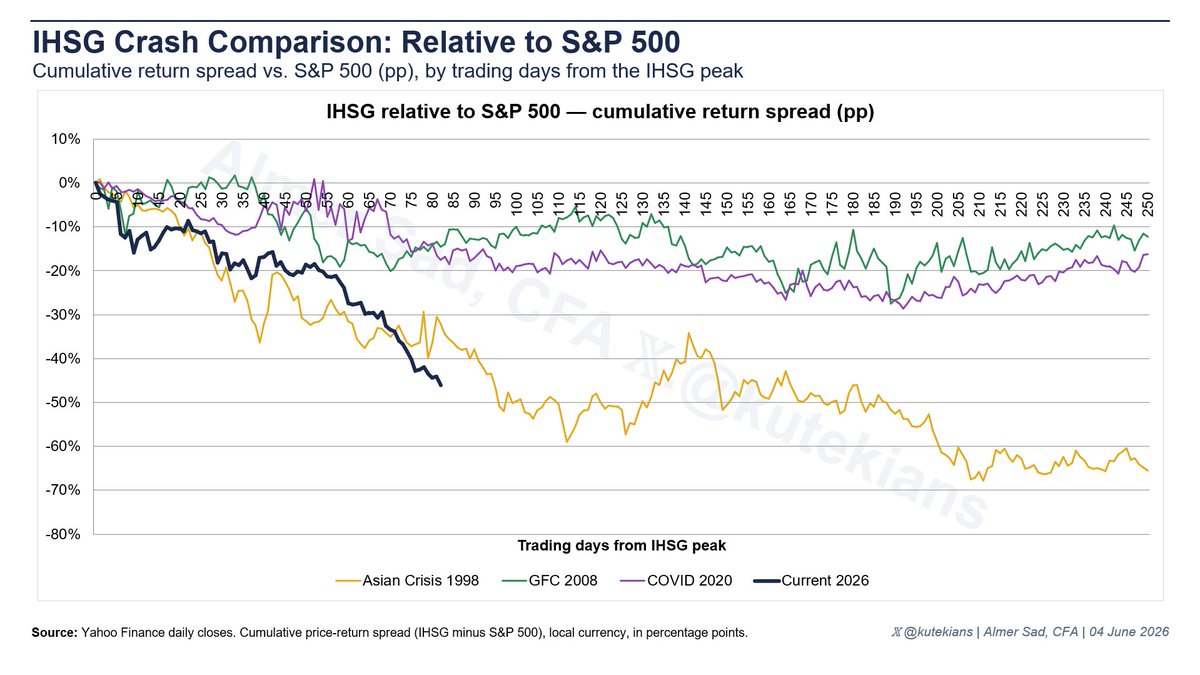

Inspired by @meridian_rsrch chart yang compare drawdown IHSG saat ini vs 1998, GFC 2008, dan COVID 2020, saya coba extend analisisnya dari angle berbeda.

Bukan absolute return dari peak, tapi relative performance IHSG vs regional dan global (proxy: MSCI EM ex-Indonesia dan S&P 500).

Waktu GFC 2008 dan COVID-19 2020, IHSG memang jatuh, tapi semuanya jatuh bersama.

Spread terhadap EM peers tetap di kisaran -15% sampai -20%.

Bahkan di GFC 2008, spread kita positive compared to EM peers.

Wajar, karena itu krisis global.

Current 2026 sudah menyentuh spread -55% relatif terhadap MSCI EM ex-Indonesia dalam 90 hari pertama.

EM lain tidak sedang crash seperti ini, apalagi global.

Kita jatuh sendiri.

Dampak dari ketidakpastian global pasti tetap ada, tapi yang lebih terlihat adalah:

Market sedang repricing sesuatu yang spesifik tentang Indonesia.

Ini bukan krisis global/regional yang kita ikut kena.

Ini krisis yang kita buat sendiri.

GUYS $VKTR MAU RIGHTS ISSUE GEDE BANGET

$VKTR (PT VKTR Teknologi Mobilitas Tbk, 3 Juni 2026) "Informasi PMHMETD I"

🚗 Saham baru yang ditawarkan: 25 miliar lembar

📊 Rasio: setiap 7 saham lama → dapat 4 HMETD

💧 Dilusi maksimal bagi yang tidak ikut: 36,36%

💰 Estimasi nilai rights issue: Rp16–25 triliun (asumsi harga pelaksanaan di kisaran harga Mei 2026: Rp655–Rp995/saham, harga final belum ditetapkan)

Ini bukan rights issue kecil-kecilan. Kalau semua pemegang saham ikut, jumlah saham beredar naik dari 43,75 miliar jadi 68,75 miliar lembar.

Kita jadikan studi kasus yuk 👇

#RangkumKeterbukaanInformasi

@handierawan Kayaknya kita harus nungguin asing masuk big bank lgi yaa ko utk dorong IHSG.

Kalo dari konglo yg tipis liquiditas gak organik mnurut saya kenaikan index ny.

The beauty of Higher Highs and Higher Lows.

After falling from the 1,500 area, KETR spent months building a base. The chart then started showing higher lows, followed by higher highs, while repeatedly holding key support levels.

The recent move to 660 matters because it continues that structure.

Strong rallies often begin with a simple change in trend:

Higher Highs.

Higher Lows.

That's what caught my attention in KETR, and that's the beauty of price action.

Seperti biasa, sebelum beli, kita perlu tau dulu bisnisnya. Kita coba overview saham $IBM. Dunia teknologi sedang bersiap menghadapi era baru bernama quantum computing. Ini adalah teknologi yang jauh lebih canggih dari komputer biasa yang kita pakai saat ini.

Obligasi Negara Indonesia: Leading Indicator Paling Jujur Buat Arah USDIDR & IHSG

Kebanyakan retail di Indonesia masih sibuk banget ngelihat candle saham, ngejar foreign flow, atau kejar-kejaran sama berita ekonomi harian di medsos.

Padahal ada satu pasar yang jauh lebih jujur dan lebih cepat kasih sinyal soal kondisi ekonomi serta arah uang besar: pasar obligasi negara (SBN).

Di Investing lo bisa liat lengkap dari ID01M sampai ID30Y. Itu bukan cuma angka yield doang. Itu denyut nadi ekspektasi investor global terhadap Indonesia.