#earnedit Friday

Weekly "best of"...

- Her reaction when we revealed she's now a millionaire

- Turning his accepted offer on a house from anxiety to excitement

- Giving her newly graduated daughter what she needs to know to start down her path towards financial zen

#earnedit Friday!

At an industry event this week, a lady came up to Amanda. "Financial Zen?! I know you guys. Love what you're doing."

Amanda asked me if I knew her. I was like definitely not. She said "Me neither."

Taking the world by storm starts w a rain drop...

“I quit.”

Ten years ago today, I walked into my branch manager’s office for the last time and uttered those two beautiful words.

May 1, 2016: Financial Zen was born.

But it’s been anything but a straight line before or since.

THE UNKILLABLE YEARS

The years leading up to that day were the Unkillable Years. I spent seven years battling gut-wrenching self-doubt and sleepless nights, wondering how I’d make rent. I got knocked down 1,000 times and got up 1,001.

The absolute lowest point? New Year's Eve 2014.

While my friends celebrated inside, I stood outside by myself in the snow, staring into the fire, tears streaming down my face.

8 hours earlier, my girlfriend (now wife) and I were at Safeway picking up supplies. She impulsively put a $35 bottle of wine on the belt as a gift for our hosts. I looked at her, fighting back tears, and said: “I can’t buy that. I don't have 35 more dollars. There's literally zero money in my checking and no room on my credit card.”

All my buddies (who were clients) were making the kind of money I would have if I stayed on the tech sales path. Instead, here I was - a 38-year-old who couldn't afford a $35 bottle of wine.

(But still chasing his dream, dammit!)

I had no idea that just 16 months later, I'd launch Financial Zen.

THE UNRELENTING YEARS

The next chapter wasn't much easier. Welcome to the Unrelenting Years.

Our industry peers still think I'm crazy for how involved we get with our members. We're basically a family office for the masses. But I refused to compromise on the vision.

And we can now confidently say our model works:

- 104 households

- $150M managed

- 98% retention

- 60% margins.

Yeah, NOW it works.

But getting here meant cutting my income in half when I updated our fee structure to serve younger demographics. It meant wasting tens of thousands of dollars and endless hours on early mis-hires. It meant ignoring the late-night whispers to “just make it a lifestyle business” or “sell out to another firm.”

I won’t take the easy road. Never have. Never will.

THE UNSTOPPABLE YEARS

Now, we enter the Unstoppable Years.

It’s no longer "me." It’s "us." Our team is lights-out incredible, and absolutely nothing will stand in our way.

When Jack Bogle started Vanguard in 1975, people thought he was bonkers. Forty years later, index funds are the ubiquitous investment worldwide. In 30 years, Financial Zen will be credited with that exact same massive impact on financial planning

LET'S GOOOOO!!!!!

We’ve never been knocked down and not gotten up. We've never settled. We’ve never taken the easy road.

To my wife Nicole, who saw me at my "Safeway Floor" and didn't blink: Thank you.

To my team—Claudine, Taylor, and Amanda: Let’s go fucking get some!

To our members: Thank you for betting on the guy who refused to sell out.

The dawn is officially here. We’ve come a long way, but the best is yet to come.

Just watch us now.

Warren Buffett on the 5% market dip: "This is nothing."

In a recent CNBC interview, the anchor tried to frame the recent market drop as a disaster: "The market has come down substantially..."

Buffett immediately cut her off: "...well... not SUBSTANTIALLY."

When pressed on the worst quarterly performance in years, his response was a masterclass in Financial Zen. He reminded everyone that true market crashes are 20% drops in a single Monday or 50% wipeouts. A 5% drop isn't a crisis. It's a teeny, tiny toe-stub.

The headlines are scary. The markets are not.

The media’s business model relies on keeping you anxious and glued to the screen. But the stock market is a math machine, not an emotional one. It completely ignores the headlines.

Here is the Financial Zen playbook to handle the next "crisis":

📉 Stop zooming in: A 5% drop day-to-day looks like a cliff. Decade-to-decade, it’s a microscopic speedbump. Zoom out.

🛑 Ignore the noise: Never make a portfolio move based on a breaking news banner. The media is selling fear; you don't have to buy it.

⚙️ Rely on your system: Let your automated investments run. Keep buying into the market with every paycheck without agonizing over the timing.

You are the CEO of You, Inc. If a 5% dip is "nothing" to Warren Buffett, it absolutely should be nothing to you.

Turn off the TV, let your automated systems do the heavy lifting, and go enjoy your day. 🧘♂️📈

#WarrenBuffett #Investing #FinancialZen #WealthBuilding #StockMarket #CEOofYou #PersonalFinance

Financial Zen is closing its doors after 10 years.

It is with a heavy heart that we announce the official closure of Financial Zen.😥

When we started this firm a decade ago, our goal was to help you automate your wealth, buy back your time, and reach Financial Zen as fast as possible. But after looking at the landscape today, we’ve realized something:

- People just don't want high-touch accountability and handholding anymore.

- Investors are completely disciplined now.

- Emotions never get in the way of smart financial decisions.

- Everyone naturally pushes through the administrative "sludge" of managing their own finances.

- And human nature has officially been conquered.

After all, there’s just no room for a swing coach when your golf swing is perfect. 🏌️♂️

(Said no one on the PGA tour, ever.)

...APRIL FOOLS! 🤡

Did we get you?

We are absolutely full steam ahead, and business is booming. 📈

The truth is, being the CEO of You, Inc. is hard work. Even the best golfers in the world have swing coaches because we can't always see our own blind spots.

We need an accountability partner to keep us on the Fast Track, talk us off the ledge when the news cycle manufactures a panic, and remind us to actually enjoy the journey along the way.

Financial Zen isn't going anywhere. In fact, we're just getting started. 🚀

The Big Announcement: We Are Turning 10! 🎉

Not only are we not closing our doors, but Financial Zen is officially turning 10 years old next month!

A decade of ignoring the noise, managing the risk first, and building true, generational wealth is a massive milestone. And we are not going to let it pass by quietly.

To celebrate, we are throwing a massive blowout bash exclusively for our Financial Zen Members.

Stay tuned. The official invitation with all the details will be hitting your mailbox & inbox soon.

Here is to the last 10 years, and to the decades of fast-tracking you to financial independence yet to come! 🥂

Why we feel like we never have "enough."

Another gem from our own behavioral finance expert, Amanda Bearden!

[Make sure to follow her!]

I was convinced that hitting my savings goal would be one of the greatest feelings. Seeing the number in my account and thinking how satisfying it would be.

And then I hit it. And I actually felt nothing. Like overwhelmingly nothing. I even forgot about it within the same week.

Why is it that the pay raise or hitting “the number” doesn’t actually make us any happier?

Thousands of years ago, we were taught that being satisfied was dangerous. If you were satisfied, you stopped gathering. If you stopped gathering, you wouldn't survive the winter.

Our brains have not evolved to keep up with modern living. We are hardwired to stay unsatisfied. But our current reality is filled with abundance, and it creates two psychological money hurdles...

1. Hedonic Adaptation: We hit a goal, celebrate for an hour, and then immediately reset. The new salary or bonus becomes the new normal, and the cycle starts over.

2. Impact Bias: We are terrible at predicting our future feelings. We think the big number in the bank will provide months of bliss. In reality, it’s a dopamine spike that lasts a few days at most.

This is why having enough feels like a forever-moving target. I know I am guilty of it, too.

The happiest people I see don’t treat having enough money as a destination. Instead, they use it as a tool to align their life with their values today, acknowledging that hitting a specific number won’t provide the lasting joy they are looking for.

I spent 3 months preparing for the Oscars. And then I missed them...

Yesterday, we went all out for the actual show: champagne, charcuterie, and deliberately delaying the start by two hours so we could skip the commercials.

We finally flipped on YouTube TV, ready for the big payoff... only to land smack in the last hour of the broadcast. I looked for the little red line to rewind. It wasn't there.

It hit me upside the head: I forgot to hit record.

I was so bummed. But after the initial shock wore off, I found the silver lining: I still got to enjoy the process. I loved the movies, the weeks of anticipation, and the damn good charcuterie.

The journey itself was great, even if I totally botched the grand finale.

The "Ramen Noodle" Trap of Investing

This is exactly how we need to look at our path to wealth.

At Financial Zen, our goal is to get you to your number as absolutely fast as possible. We want you on the Fast Track.

But if your strategy to get there involves eating ramen noodles every night, never going on a vacation, and white-knuckling your way through the next 15 years... you are doing it wrong.

Finding the Balance

Building wealth should not be an exercise in daily misery. If you don't enjoy the journey, crossing the finish line isn't going to magically make you happy.

You have to find the balance:

Don't WASTE money: Cut the sludge. Cancel the subscriptions you don't use. Stop buying things just to impress people you don't like. Optimize your taxes and lower your investment fees.

But don't be afraid to SPEND money: If taking a great family vacation, buying back your time on a Sunday, or getting the nice bottle of champagne brings you genuine joy—spend the money.

The goal of Financial Zen isn't to arrive at the end of your life with the highest possible bank account balance and zero memories.

Enjoy the movies. Enjoy the anticipation. And don't forget to enjoy the charcuterie along the way.

Remember the dad from A Christmas Story constantly fighting the furnace? 🤬 That used to be me every Sunday doing meal prep.

Banging pots, cursing, and spending 2+ hours of my weekend recharge just to save a few bucks.

Four weeks ago, I’d had enough. I signed up for Factor 75.

For $80 a week, I bought back two hours of my Sunday. And the math proves I was an idiot for not doing it sooner:

The Cost: $80/week

The Time Saved: 2 hours

The "Earner" Math: Doing it myself meant I valued my weekend time at just $40/hr.

Based on our membership fees, my time is worth $550/hr.

By spending $320 a month, I buy back 8 hours.

8 hours x $550/hr = $4,400 in generated value.

That’s a 1,275% ROI. 🤯

But the real return isn't the math. It’s what I do with those two hours. I don't work—I hang out with my wife and actually decompress.

Because of that, I log in on Monday at 100% capacity, making better decisions and generating far more wealth than the $80 I "saved" boiling my own quinoa.

What are you doing right now that sucks, but you do it to save a buck? Filing your own taxes? Managing your own portfolio?

Don't step over dollars to pick up pennies.

You're the CEO of You, Inc. Invest your time in CEO-level activities, not entry-level busywork.

#grateful Friday

Just finished the Quarterly Accomplishments & Opportunities Reviews w/ our team...

...and I am just so grateful for each of them individually and us as a collective.

We love working together, we love the Members we have the opportunity to serve and most importantly we deeply believe in our mission.

I am truly blessed to work w such amazing people!

The Miami Gang, the BMW M4, and My Dad's Stolen Identity

A week after my dad passed away, a Miami detective knocked on my mom's door in Palm Beach.

He was investigating a hit-and-run involving a BMW registered to my dad. My mom explained that her husband had just passed away https://t.co/ddbanbBZAB they hadn’t owned a BMW in 15 years.

A few days later, the impound lot called demanding tow fees. My mom refused.

That’s when it unraveled: Someone had purchased a sweet 2023 BMW M4, taken out an auto loan, and set up Progressive insurance - all in my dad's name.

Over the next three months, the plot thickened.

Miami PD pulled over a car and found a massive stack of credit cards in my dad's name in the backseat.

Then, my mom got a toll ticket for a Cadillac Escalade speeding through Naples registered to... you guessed it... good ol' dad.

My Mom got a play-by-play from the detectives, and apparently, a Miami gang had an identity theft ring that my dad had obviosuly been a victim of.

The sad part is my mom then spent months fighting tow yards, police, and insurance companies to clear his name. Believe it or not, the mess is still ongoing.

The Hard Truth: It Was Kind of My Fault

Here is the confession. My dad wasn't very tech-savvy in his later years. Because of the hassle, I didn't check his credit report every year like we diligently do for our Financial Zen Members.

If we had, we would have spotted the car loan and stopped this nightmare in its tracks. (Sorry, Mom!)

The Two-Step Defense Plan

1. Check Your Credit Reports Annually

Go to www.https://t.co/7EsgpjFsQR (the only federally authorized site (which also ironically looks sketch)). Pull your reports and check them line by line for accounts you don't recognize.

2. The New FZ Rule: Freeze Your Credit

We've officially added this to our Financial Zen checklist: Freeze your (and your parents') credit with all three bureaus. You can now toggle a freeze on and off from your phone in seconds.

Protect your identity. Protect your parents. Go freeze your credit today.

How to avoid the "Permanent Vacation" trap.

All Mike and Mary could dream about was achieving Financial Zen.

They didn't hate their jobs. They weren't miserable. But they absolutely did not want to work a day longer than they had to.

So, they put their heads down. They saved aggressively, slashed their expenses, and did everything right mathematically.

Their hard work paid off: They officially retired at 51.

With nearly half of their lives left to live, they went all out. For the first few years, it was the ultimate dream come true—uncapped travel, endless golf, and zero alarm clocks. (Sounds amazing, right?)

But eventually, the permanent vacation started to feel like a waiting room.

Just like a cheat meal that turns into a two-week binge, the endless fun started to wear thin. Without a mission, they lost their sense of contribution. Believe it or not, living the exact life they had dreamed about for twenty years actually got... boring.

So, seven years after retiring, they went back to work.

Not because they needed the money. Because they needed a purpose.

Mike and Mary started as the ultimate success story. But they turned into a warning.

If you're reading this, you likely have the earning power and discipline to retire insanely early. But doing the math to cross the finish line ahead of schedule is actually the easy part.

The hard part is staying fulfilled once you get there.

Don't take my word for it. If you spend five minutes scrolling the FatFIRE subreddit, you will see countless examples of people just like Mike and Mary—millionaires who hit their number in their 40s, only to realize they have no idea who they are without their careers.

Speaking from experience, our most successful early retirees don't just build a spreadsheet for their money. They build a blueprint for their time.

They put as much work into planning their post-work life as they do getting to the finish line.

It's never too early to start trying things out to see what might stick on the other side.

#earnedit Friday

A new WeWork neighbor saw my Financial Zen mug sitting on the kitchen counter.

"Financial Zen!? I know you guys. You guys work w tech people right?"

"Uhh. Yup That's us. How'd you know?"

"My buddies were telling me about you last year."

"Oh yeah? Who's that?"

"Joe Blow and John Schmoe" (Some guys I had never heard of.)

"Thanks, man. You just made my day."

The train is coming...

Most of us are employees 9-to-5. But in our financial lives? We are the CEOs of You, Inc. 👔

The problem is, we’re still acting like "Earners" instead of "Allocators."

We spend entire weekends fighting with TurboTax to save a few hundred bucks on a CPA. 📉 We spend Saturday fixing the sink to save $150 on a plumber. We think we're winning because the bank account is slightly higher.

But a CEO knows that’s a losing trade.

A CEO’s only job is to allocate resources - money, people, and energy - to the highest-impact areas. If a CEO saw their star engineer fixing the printer for 3 hours to "save money" on IT, they’d lose their mind. 🤯

So why do we do it to ourselves?

When we spend 15 hours doing our own taxes to save $500, we are valuing our limited time on this earth at $33/hour. (And I bet you make more than $66k/year.)

Is that really what our time is worth?

Whatever we "buy back" with that time - learning a new skill, building a side hustle, or just resting so we can crush it on Monday - has a higher ROI than being our own housekeeper or accountant.

And if we don't know what we'd do with that free time? Then our new job is to spend that time figuring it out.

Because on the path to Financial Zen, we’re going to have a lot of free time eventually. We might as well start practicing now. 🧘♂️

🛑 You have until April 15th to take 5 minutes to review your 2022 tax return for overpayment.

In the last two years alone, we’ve uncovered over $100,000 in accidental "tips" to the IRS while reviewing old tax returns for new members.

We have a rule at Financial Zen: Pay the IRS as little as you legally can.

The culprit? RSUs.

If you work in tech and ESPECIALLY if your company uses Fidelity or E*Trade, it's possible you overpaid your taxes in 2022, 2023, or 2024.

Here is why: These brokerages often report your RSU cost basis as $0 on the standard 1099 form. If you filed with that number, you paid tax TWICE on the same money (Income Tax on the vest + Capital Gains Tax on the full sale price).

The 2-Minute DIY Audit:

Go pull up your old tax returns (PDFs) and find Schedule D.

Scan the "Cost Basis" column.

See a $0? 🚩 STOP. You likely overpaid.

How to Fix It (And Get Your Money Back):

You can amend your tax returns for up to 3 years.

For Fidelity: Go back to your 1099 PDF and scroll to the very end. The real numbers are hidden in the "Adjusted Cost Basis" section.

For E*Trade: Log in and download the "Supplemental Tax Notification" for that year.

⏰ URGENT DEADLINE: You only have until April 15, 2026 to amend your 2022 tax return.

That is roughly 60 days from now.

Go check your Schedule D today. There might be a nice refund check waiting for you. 💸

#FinancialZen #TaxRefund #RSU #TechSales #Fidelity #ETrade #MoneyHacks #TaxSeason2026

Everyone knows the secret to getting a six-pack: Eat fewer calories than you burn. 🔥 It's simple math. So, why doesn't everyone have one?

Because knowing what to do is easy. Actually doing it is hard.

It's the same with your money. You don't need more complex information; you need execution. At Financial Zen, 80% of what we do is provide the accountability to ensure the things you know you should do actually get done.

Think of us as the "Ultimate Health Partner" for your finances 🤝:

🏋️♂️ The Spotter: We're there to spot you on the heavy lifts, like making big investment decisions, so you don't hurt yourself.

🥗 The Nutritionist: We create a custom plan to fuel your financial future, ensuring you're investing in the right things for your goals.

👨⚕️ The Doctor: We track your financial vitals and recalibrate your plan as your life changes to keep you healthy.

We're here to reduce the friction between "knowing" and "doing." Stop trying to do it all alone. Let's get to work. 💪

#FinancialZen #MoneyMindset #Accountability #WealthBuilding #FinancialFreedom #DoTheWork

I'm not ashamed to admit I wash and reuse Ziploc bags.

Similarly, Keith "admitted" that he buys bruised fruit and washes then reuses paper towels.

His coworkers chuckled under their breath.

At the end of the episode, the camera zoomed in on his computer screen to reveal that the unassuming nurse on St. Denis Medical had $4.1M.

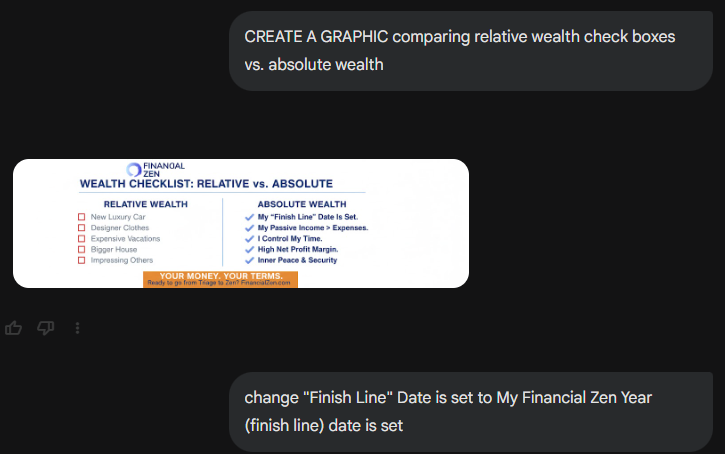

While his coworkers were busy "looking" successful, he was busy being successful. That is the difference between Relative Wealth and Absolute Wealth.

THE VANITY OF RELATIVE WEALTH

Most of us are trapped in the Relative Wealth cycle. We gauge our success by how we look compared to our peers.

The blow-out kitchen renovation... the luxury SUV in the private school pickup line... the new Rolex... the Instagram reel of 5-star resort vacations...

But here is the truth: A brand-new $90,000 car parked in a driveway isn’t a sign of wealth. It’s a sign that $90,000 (plus interest) has left someone's net worth.

Relative wealth is a game we can never win. There will always be someone with a faster boat or a bigger house. If we use other people's spending as our benchmark, we are letting their bad habits dictate our financial future.

THE SANITY OF ABSOLUTE WEALTH

Absolute Wealth doesn't care about the driveway next door. It’s invisible.

It’s the peace of mind that comes from knowing exactly when we’ll hit our Financial Zen Number. It’s the stability of a high Net Profit Margin on our paychecks. It’s the freedom to know that if we walked into work and quit today, our lifestyles wouldn't change.

True wealth is the money we haven't spent on toys. It’s the ability to own our time rather than having our lifestyles own us.

Now THAT'S a financial flex.

THE GRINDER MINDSET

The nurse with the $4.1M knew a secret: Wealth is built in the margins. It’s built by the people who don’t care what the "crowd" thinks of their habits because they are too busy focused on their destination.

People might laugh at the guy buying bruised fruit, but they aren't laughing at the $4.1M.

And for the record? I actually wash and reuse Ziploc bags.

(The 2 headed, 2 legged dog is what AI came up with when prompted to update the graphic It was too funny not to share.)

My Whoop band tells me the Weather (Did I sleep well last night?). My Withings scale tells me the Climate (Am I getting healthier over 6 months?).

In investing, most people obsess over the Weather (Daily dips, headlines, Fed rates). They ignore the Climate (Compounding, asset allocation, net worth).

If you chase the weather, you're just frantically changing clothes. Build for the climate.

Buying a stock = Buying a share of human ingenuity.

Buying Gold/Crypto = Betting someone else will pay more later.

Companies create value out of thin air: • Apple turns glass into iPhones. • Financial Zen turns anxiety into freedom.

Commodities just sit there. They don't have babies.

We invest in the "ceaseless progress of mankind." We don't bet against it.

![RickValenzi's tweet photo. Why we feel like we never have "enough."

Another gem from our own behavioral finance expert, Amanda Bearden!

[Make sure to follow her!]

I was convinced that hitting my savings goal would be one of the greatest feelings. Seeing the number in my account and thinking how satisfying it would be.

And then I hit it. And I actually felt nothing. Like overwhelmingly nothing. I even forgot about it within the same week.

Why is it that the pay raise or hitting “the number” doesn’t actually make us any happier?

Thousands of years ago, we were taught that being satisfied was dangerous. If you were satisfied, you stopped gathering. If you stopped gathering, you wouldn't survive the winter.

Our brains have not evolved to keep up with modern living. We are hardwired to stay unsatisfied. But our current reality is filled with abundance, and it creates two psychological money hurdles...

1. Hedonic Adaptation: We hit a goal, celebrate for an hour, and then immediately reset. The new salary or bonus becomes the new normal, and the cycle starts over.

2. Impact Bias: We are terrible at predicting our future feelings. We think the big number in the bank will provide months of bliss. In reality, it’s a dopamine spike that lasts a few days at most.

This is why having enough feels like a forever-moving target. I know I am guilty of it, too.

The happiest people I see don’t treat having enough money as a destination. Instead, they use it as a tool to align their life with their values today, acknowledging that hitting a specific number won’t provide the lasting joy they are looking for.](https://pbs.twimg.com/media/HDzj6WGWMAAevtt.jpg)