7/

168X Fortune — Chinese trading podcast / AMAs with traders

https://t.co/sW2XmvEzD9

MoneyPrinter0x — crypto trader who also watches equities

https://t.co/ylKjFc8RK4

Who else should be on this list? Especially looking for accounts covering AI infrastructure, memory, optics, power and liquidity.

1/

My X research list for semiconductors, AI infrastructure, memory and US equities.

Not investment advice — just accounts I use to filter noise, track narratives early, and learn from people closer to the supply chain.

🧵👇

6/

Useful finds

Serenity — strong at identifying rotations and emerging narratives

https://t.co/vBnOvveZVf

Alex Corrino — recently did a great HBM deep dive

https://t.co/sglNtTVTe7

AI didn’t break today.

The market just started repricing the value chain.

Memory, semis and neoclouds got hit because they were crowded and priced for perfection.

META +9% on plans to monetize excess AI compute is the real tell:

Hyperscalers are no longer just buyers of AI infrastructure.

They may become sellers of compute too.

That’s bullish for the AI buildout.

But it raises the bar for independent GPU clouds.

The question is shifting from:

“Will AI capex continue?”

to:

“Who captures the rent once the GPUs are installed?”

My answer remains: own the stack, not one narrative.

$NVDA $AVGO $TSM $MU $ANET $VRT $ETN $META

Small optionality in neoclouds, not portfolio-defining exposure.

Market feels a lot healthier today.

And the interesting part?

Nothing fundamentally changed over the last week.

$MU just confirmed memory remains one of the tightest bottlenecks in AI:

• monster beat

• 84.9% gross margins

• Q4 guide way above consensus

• supply tight through 2027+

Yet semis got sold anyway.

That wasn’t fundamentals.

That was positioning.

Now we’re seeing the reset:

• DXY down 3 straight days

• VIX back below 18

• Nasdaq bounced +2%

• KOSPI stabilizing

• Samsung + SK Hynix announced a $518B expansion plan

• Semi price hikes start July 1

That’s not what a broken cycle looks like.

That’s what a supply-constrained supercycle looks like after leverage gets flushed.

The next AI rally probably won’t be led by the obvious names.

Watch the layers under the layers:

$ALAB → memory pooling

$NBIS → compute monetization

$AVGO → custom silicon + networking

$VRT → density/cooling

$GEV → power generation

The AI stack keeps getting deeper.

And so do the bottlenecks.

I went down the humanoid robotics rabbit hole this week.

My main takeaway:

The first real bottleneck may not be AI.

It may be turning a robot from an impressive demo into a machine that can work 16 hours a day without becoming a maintenance problem.

The robot is easy to imagine.

The maintenance schedule is harder.

Markets eventually care about the second one.

I’m mapping the physical AI supply chain next:

motion, vision, power, materials, and uptime.

Micron just delivered one of the strongest memory prints of the cycle:

• Revenue crushed

• Gross margins hit 84.9%

• Q4 guide massively above consensus

• HBM demand locked through 2027+

Yet the stock gave back most of its post-earnings spike.

That tells you something:

This market is not questioning AI demand.

It’s unwinding leverage.

Look at the setup:

• KOSPI still weak

• Foreign selling continues

• Semis under pressure despite monster fundamentals

• VIX only ~18

That’s not a broken cycle.

That’s crowded positioning getting flushed.

And that’s the distinction.

Because under the surface, nothing changed:

Memory is still pre-sold.

HBM still consumes 4x wafer capacity.

Hyperscalers still race for compute.

Power, optics, and cooling are still bottlenecks.

This is not AI slowing down.

This is capital rotating, de-risking, and resetting.

The cycle looks alive.

The price action just wants cleaner hands first.

$MU $NVDA $AVGO $COHR $NBIS $GEV

The biggest risk in humanoid investing is not that robots never arrive.

It is paying 2035 prices for 2026 evidence.

The theme can be right.

The timing can be wrong.

The company can still fail.

And the stock can still be expensive.

That is why I prefer watching the proof points:

deployments, uptime, manufacturing yield, service economics, repeat orders.

Narratives create excitement.

Execution creates returns.

$TSLA may have the most interesting humanoid setup.

Not because Optimus is already proven.

Because Tesla already has:

• factories to test inside

• supply-chain leverage

• manufacturing talent

• AI/data infrastructure

• repetitive workflows worth automating

The real signal will not be another stage demo.

It will be measurable deployment inside Tesla’s own factories.

Robot-hours.

Uptime.

Tasks completed.

Cost per task.

That is when Optimus becomes an operating story, not just a narrative.

One thing I underestimated about humanoid robots:

Weight is not a cosmetic issue.

A heavier robot needs:

• more power

• larger actuators

• more cooling

• worse battery economics

• more expensive movement

That is why high-performance magnets matter.

Not because rare earths are a magic trade.

Because efficiency compounds across the entire machine.

$MP is one US-listed name I’m watching here — but it is a materials and geopolitical optionality trade, not a clean humanoid pure play.

$MU just gave the market a much bigger message than “good earnings.”

Q4 revenue guide: $49–51B vs $43.2B expected.

Gross margin: 84.9% vs 81.9% expected.

But the real bull case is underneath the headline.

Micron now has $10B+ of minimum contracted revenue under long-term supply agreements — and that is based on minimum volumes × minimum prices.

The big contracts have barely started.

HBM is also eating DRAM capacity: every wafer pushed into HBM means less commodity DRAM supply available to the market.

So this is not just a demand story anymore.

It is a supply squeeze with pre-sold revenue, cash deposits, and margins above prior-cycle peaks.

The market sold $MU into earnings because expectations were high.

Now the question is whether people still understand how tight memory can stay into 2027–28.

That is where the upside is.

Everyone is watching $MU tonight like it’s “just another earnings.”

It’s not.

Micron is the read-through for the entire AI supply chain.

Why?

Because the market is confused right now.

Nasdaq sold off (-1.3%).

$GOOG dumped 5%.

KOSPI crashed -4.2%.

People see that and think AI demand is cooling.

But under the surface?

Korean memory exports say the exact opposite:

• DRAM +576% YoY

• Flash +546% YoY

• HBM/MCP +119% YoY

That’s not slowdown.

That’s shortage.

And that’s the key.

The market is selling AI buyers (Google, hyperscalers) while memory suppliers are quietly printing.

If Micron confirms:

→ HBM still constrained

→ pricing still rising

→ CY27 supply still locked

then this isn’t just bullish for $MU.

It’s bullish for:

$NVDA

$AVGO

$LITE

$COHR

$GLW

$NBIS

$CRWV

One earnings report.

Potentially the most important AI datapoint of the month.

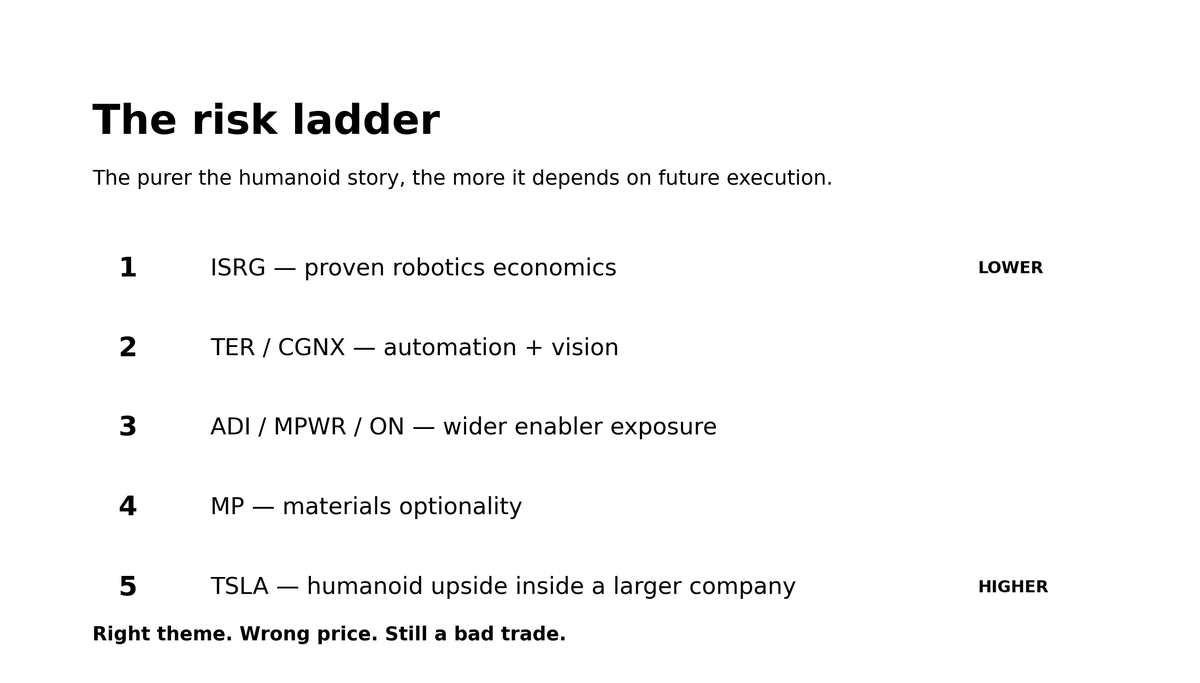

The most dangerous humanoid trade is not being early.

It is paying 2035 prices for 2026 evidence.

My risk ladder:

$ISRG — proven robotics economics

$TER / $CGNX — broad automation and machine vision

$ADI / $MPWR / $ON — enablers with much wider end markets

$MP — materials optionality

$TSLA — humanoid upside inside a much larger company

The more “pure” the narrative, the more your return depends on execution that has not happened yet.

Right theme. Wrong price. Still a bad trade.

$STRC is starting to look less like a yield product and more like a stress test for the entire $MSTR flywheel.

It was designed to trade around $100.

Now it is sitting around the high-$80s while still paying 11.5%.

That is not a normal “income trade.”

That is the market asking one question:

Can Strategy keep funding BTC purchases and preferred dividends without the STRC ATM reopening properly?

The bull case is simple:

If $BTC stabilizes and Saylor rebuilds enough cash runway, STRC can mean-revert hard toward par.

Buying an 11.5% yield at $87–89 with a path back to $100 is interesting.

The bear case is uglier:

STRC stays below par → issuance slows → Strategy raises less capital → buys less BTC → the flywheel loses momentum.

This is not a bond.

It is a leveraged confidence trade on Saylor, BTC and retail demand.

I’m watching STRC more closely than $MSTR here.

Sometimes the preferred tells you the truth before the common does.

The AI trade just got hit with a proper flush.

$MU -13% into earnings.

$TSM -5%.

$SOXL got smoked.

Korea had a near-10% panic day.

That is not “AI is dead.”

That is crowded positioning getting force-liquidated.

The opportunity is obvious:

If $MU prints strong HBM/DRAM numbers and gives a clean forward guide, the fastest money is probably made in the names that got sold for fear, not fundamentals.

My map:

$MU = event trade. Huge upside if whispers were wrong. Huge risk if guidance disappoints.

$TSM = higher-quality swing. AI demand does not disappear because one memory stock reports.

$SOXL = pure volatility. Great for a bounce, terrible to marry.

$BTC = tells you whether this is a real risk-off regime or just a leverage washout.

When everyone is staring at the red screen, I start looking for what was sold too hard.