$SCU insider podcast

Optimal Blue SVP Corporate Strategy tells the story of how product P&L ownership changed the way his teams think and operate post acquisition.

https://t.co/JJXdNMYH18

@Spencer_Invest True, you can’t expect that immediately. Important is that de rest of board and management was not aware of it or involved. Starting an investigation is good, as it’s still speculation. When Charles did what he did, he needs to step down asap himself, to protect integrity of TVK.

@PronkDaniel@HiddenGemsInves It’s operational still the same company with great perspectives, but will have to regain the trust of the investor regarding the corporate governance back.

@PronkDaniel@HiddenGemsInves I can give you mine. That this happens is really bad. Two things stand out, 1. It’s isolated to Pellerin(as insider)which is the positive in this. 2. Management and board where not aware of the house searches, which is odd.

Pellerin needs to step down asap, until it’s settled.

$CSU $TOI.V TSS buys Operis, a specialist in digital urban planning authorization mgmt tools for local authorities in France. They enable fully paperless processing of planning permissions, & serves all stakeholders—citizens, professionals, permitting authorities, & consultants.

$CSU $TOI.V TSS buys Operis, a specialist in digital urban planning authorization mgmt tools for local authorities in France. They enable fully paperless processing of planning permissions, & serves all stakeholders—citizens, professionals, permitting authorities, & consultants.

The 18% sell-off following the 3i Group Action seminar left me in shock. I didn’t expect a drop of that magnitude at all, especially after the stock had already endured a significant beating. Just wanted to share some thoughts.

$III.L

Investors seem spooked by the French LFL (Like-for-Like) numbers. France represents roughly one-third of the revenue, and while the market was quick to label the weakness as a thing of the past after a +2.1% improvement in the first four weeks of 2026 (up from -2.7% in Q4 2025), that optimism was obviously too premature. By the end of the first 12 weeks, growth had cooled to a marginal +0.9%; still a decent recovery.

The current geopolitical climate in the Middle East will be another headwind for France (and the whole of Europe) and will likely cause a prolonged period of economic uncertainty which will pressure the growth and the margin. Action has a leeway compared to competition when it comes to being able to increase and decrease prices, but that doesn’t make it immune to macroeconomics. That being said, it’s not firm specific, every other competitor will also be having a harder time which might even bring more revenue to Action due to that mentioned leeway.

But even if organic growth remains under pressure, Action’s store expansion strategy provides a massive cushion. Historically, they have achieved a 12-14% CAGR in store openings. Eventually this might normalize due to the size of the organization but with the amount of identified white space left this shouldn’t come below 10% the for the foreseeable future, if it does that would make me reconsider the investment case. Since these stores typically become profitable within 12 months, the company can likely generate 8-11% cash flow growth through inorganic expansion alone.

The market also appeared to be harsh in response to the US entry announcement, already pricing it as a complete failure. This overlooks the past two decades of successful scaling. Management is being transparent about higher upfront costs for local buying teams and brand awareness; this is a strategic necessity in a harder market like the US, not a red flag.

In the end it will be all about brand awareness, they will probably have to sacrifice margin for a longer period of time to get their boots on the ground. A sacrifice every shareholder should be willing to make considering how big of a reward the US market can bring.

That said, the stock has been severely punished. Excluding France, the company is performing well, with consistent growth and expansion to even more countries. The guidance management provided was on the conservative side, but in this current climate, I don’t blame them.

In my opinion, all these factors don’t justify the -18% drop in the stock price, but who am I to argue…

…on March 27, 2026, CEO Simon Borrows purchased over 350,000 shares at an average price of £25.55, which amounts to nearly £9 million.

The 18% sell-off following the 3i Group Action seminar left me in shock. I didn’t expect a drop of that magnitude at all, especially after the stock had already endured a significant beating. Just wanted to share some thoughts.

$III.L

Investors seem spooked by the French LFL (Like-for-Like) numbers. France represents roughly one-third of the revenue, and while the market was quick to label the weakness as a thing of the past after a +2.1% improvement in the first four weeks of 2026 (up from -2.7% in Q4 2025), that optimism was obviously too premature. By the end of the first 12 weeks, growth had cooled to a marginal +0.9%; still a decent recovery.

The current geopolitical climate in the Middle East will be another headwind for France (and the whole of Europe) and will likely cause a prolonged period of economic uncertainty which will pressure the growth and the margin. Action has a leeway compared to competition when it comes to being able to increase and decrease prices, but that doesn’t make it immune to macroeconomics. That being said, it’s not firm specific, every other competitor will also be having a harder time which might even bring more revenue to Action due to that mentioned leeway.

But even if organic growth remains under pressure, Action’s store expansion strategy provides a massive cushion. Historically, they have achieved a 12-14% CAGR in store openings. Eventually this might normalize due to the size of the organization but with the amount of identified white space left this shouldn’t come below 10% the for the foreseeable future, if it does that would make me reconsider the investment case. Since these stores typically become profitable within 12 months, the company can likely generate 8-11% cash flow growth through inorganic expansion alone.

The market also appeared to be harsh in response to the US entry announcement, already pricing it as a complete failure. This overlooks the past two decades of successful scaling. Management is being transparent about higher upfront costs for local buying teams and brand awareness; this is a strategic necessity in a harder market like the US, not a red flag.

In the end it will be all about brand awareness, they will probably have to sacrifice margin for a longer period of time to get their boots on the ground. A sacrifice every shareholder should be willing to make considering how big of a reward the US market can bring.

That said, the stock has been severely punished. Excluding France, the company is performing well, with consistent growth and expansion to even more countries. The guidance management provided was on the conservative side, but in this current climate, I don’t blame them.

In my opinion, all these factors don’t justify the -18% drop in the stock price, but who am I to argue…

…on March 27, 2026, CEO Simon Borrows purchased over 350,000 shares at an average price of £25.55, which amounts to nearly £9 million.

@SimeonResearch_ Asseco has not much in Poland it self agreed. To play that story, Sygnity is a far better play. Both are very interesting investments at currents levels 🙂

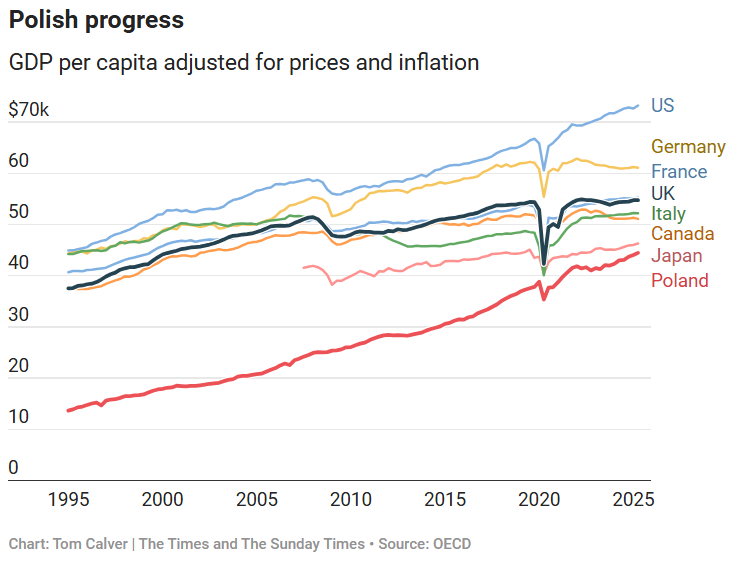

Poland is overtaking Switzerland economically and knocking on the door of the G20. It is an impressive growth story, yet technologically the country still lags ten to fifteen years behind Western Europe.

That is precisely where the opportunity lies for Asseco Poland.

Poland is overtaking Switzerland economically and knocking on the door of the G20. It is an impressive growth story, yet technologically the country still lags ten to fifteen years behind Western Europe.

That is precisely where the opportunity lies for Asseco Poland.

As the backbone of the Polish IT infrastructure, the company benefits from the necessary digital catch-up race. The recent entry of Topicus (part of the Constellation Software group) changes the playing field fundamentally. The Canadian blueprint for capital allocation, value-based pricing and cost discipline is now being rolled out in Warsaw.

We see a rare combination of structural market growth and the implementation of proven best practices.

Read our full analysis below 👇

$ACP.WA $TOI.V $CSU.TO

@joepify