@manupalop84@albertrjf De acuerdo, aún están en una fase temprana a medida de que los Hyperscalers utilicen más chips propios TPUs, Maia,etc. El costo de adquisición de estos comparados con las GPU de Nvidia se reducirá drásticamente.Ademas de un mayor rendimiento lo que reducirá el coste de inferencia

1/8

$DGV #DigitalValue#OPA

Primer día de OPA. Esto es lo que ha pasado.

OEP ha comprado 21.894 acciones en mercado y ha sumado 1.540 por adhesiones. Total: 23.434 acciones.

Eso es solo el 0,23% del capital.

OEP pasa del 69,57% al 69,80%.

Siguen muy lejos del 90%.

US inflation today and the tariff effect, according to real-time price data:

US CPI: 0.94%

US Goods inflation: 1.14%

US Services inflation: 0.84%

Our data suggest that goods prices began rising shortly after the tariff announcement in April 2025 and continued to increase gradually before easing from December 2025 onward.

The diminishing difference between goods and services inflation suggests the effect of 2025 tariffs has now been completely priced in.

We estimated that the pass-through effect on goods prices contributed to a cumulative 0.8% increase in Truflation CPI by November 2025. In the absence of tariffs, the November CPI would have been closer to 1.5%. If anything, 2025 tariffs might have temporarily deferred deflation.

The overall tariff-related inflation in our price data was relatively modest compared to the announced tariff rates, indicating limited pass-through to consumers, with the bulk of the burden absorbed by foreign producers and importers.

Is Apple making the right choice?

CapEx Growth since 2018:

Amazon +882%

Microsoft +455%

Meta +401%

Google +264%

Apple -4%

$AMZN $MSFT $META $GOOGL $AAPL

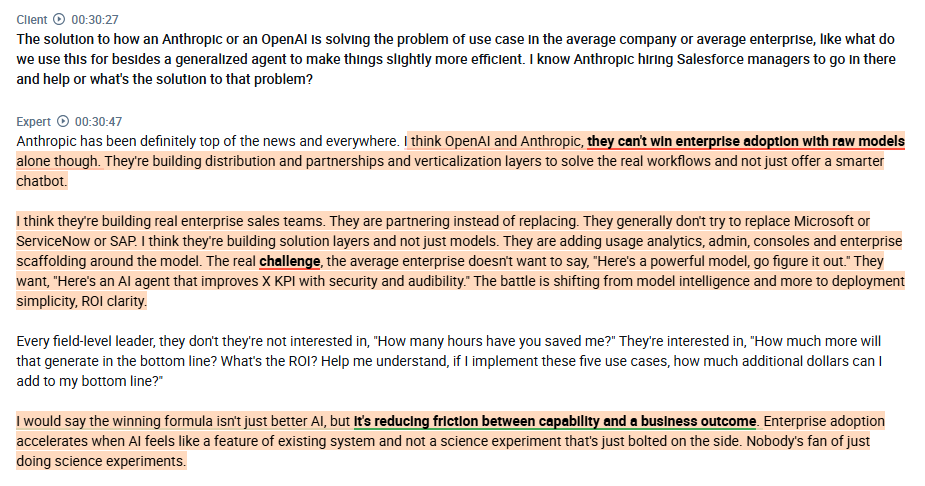

A very insightful interview with an $MSFT employee who works on Copilot on the SaaS disruption debate:

1. According to him, AI doesn't eliminate software value; it redistributes it. He thinks the recent declines in software share prices due to AI risk are partially justified, as it can compress margins, lower switching costs, and shift value from the application layer to the platform or maybe even the model layer. He thinks companies with strong proprietary data, deep workflow integration, and AI execution capability are more likely to expand value rather than lose it.

2. He gives a good example of value for a SaaS provider. The advantage isn't that we host your data, it's that we see patterns like no single customer can see, explaining the value of pattern intelligence across millions of records. He also thinks that in an AI world, owning where revenue decisions happen may be more valuable than owning where attention happens.

3. If SaaS gross margins move from 85% down to 50-60%, the math forces a redesign of the SaaS model. He thinks that if 20-30% of gross margin disappears, the most logical offset is sales and marketing efficiency. The industry will no longer look like the classic SaaS industry, but will more closely resemble an infrastructure economy. Not all players can sustain that 30% operating margin.

4. According to him, $MSFT's Satya always says we're going to have 1.3 billion agents by 2028. He thinks we are rapidly moving from AI that answers to a more agentic mode where AI does. The next 6-12 months are all about orchestration and enterprise control. He thinks the year won't be about AI getting smarter, but more about AI becoming more reliable and integrated into real business processes.

5. He thinks OpenAI and Anthropic realized they can't win enterprise adoption with a raw model alone. They're building distribution, partnerships, and verticalization layers to solve real workflows, not just offer a smart chatbot. The battle is shifting from model intelligence to deployment simplicity and ROI clarity. The winning formula is reducing friction between capabilities and a business outcome. Enterprise adoption accelerates when AI feels like a feature of the existing system and not a science experiment that's just bolted on the side.

found on @AlphaSenseInc

La inflación REAL está colapsando a pasos agigantados Las medidas reportadas por el BLS van con mucho lag, y por eso la FED siempre va muy por detrás de la curva

BREAKING: US CPI inflation today 0.68%

Our independent inflation index dropped from 0.86% yesterday to 0.68% today, Sunday, Feb 8.

Independent price data show another strong wave of cooling inflation, this time driven by a ~20% drop in natural gas prices charged to residential consumers.

Utility providers purchase gas at wholesale hubs or under contracts, with household prices adjusted later due to regulatory factors and billing cycles. This latest cooling reflects commodity price declines from previous months, which are only now trickling into retail gas prices.

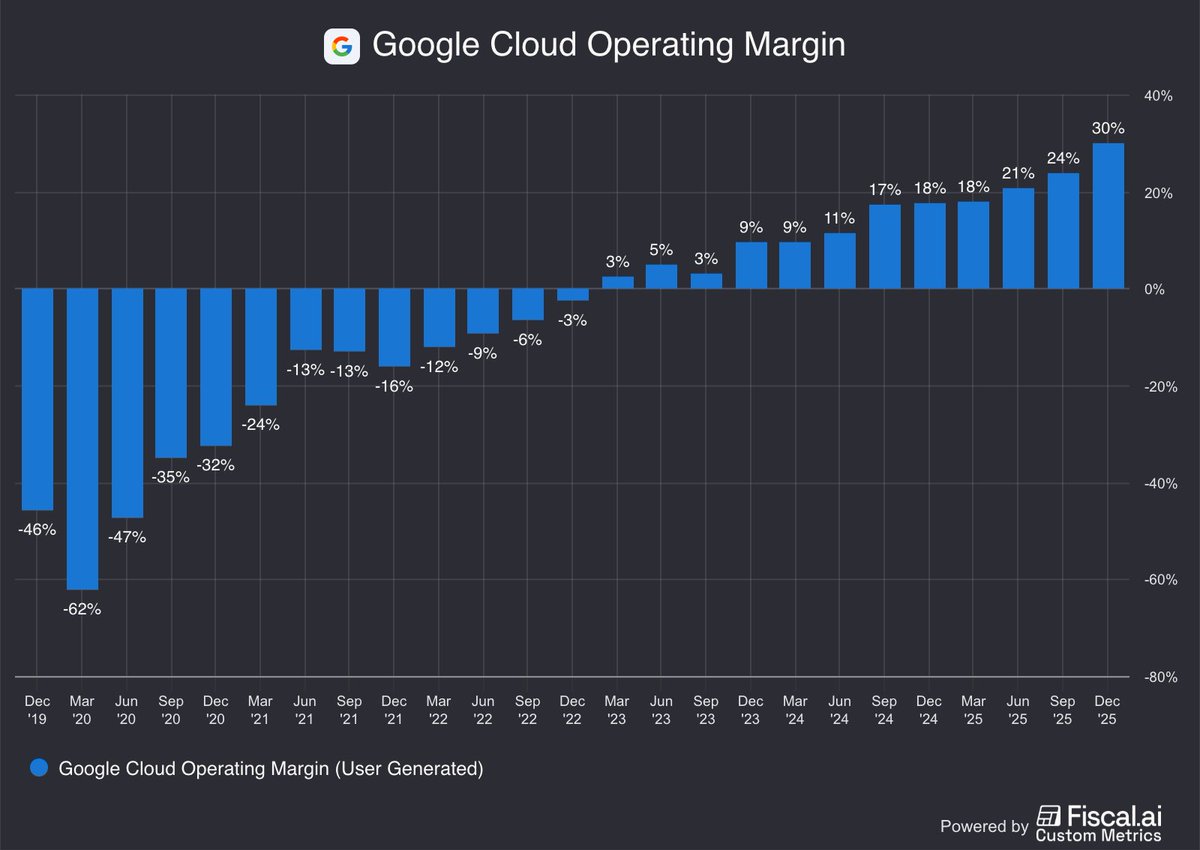

The Hyperscalers now have more than $1 trillion in total cloud commitments.

Google Cloud: $243B (+161%)

AWS: $244B (+38%)

Microsoft Azure: $631B (+108%)

$GOOGL $AMZN $MSFT

Amazon AWS backlog just got updated.

Balance is now at $244b, up +40% YoY.

Google Cloud's backlog is almost equivalent, now at $240b.

$AMZN $GOOGL $GOOG

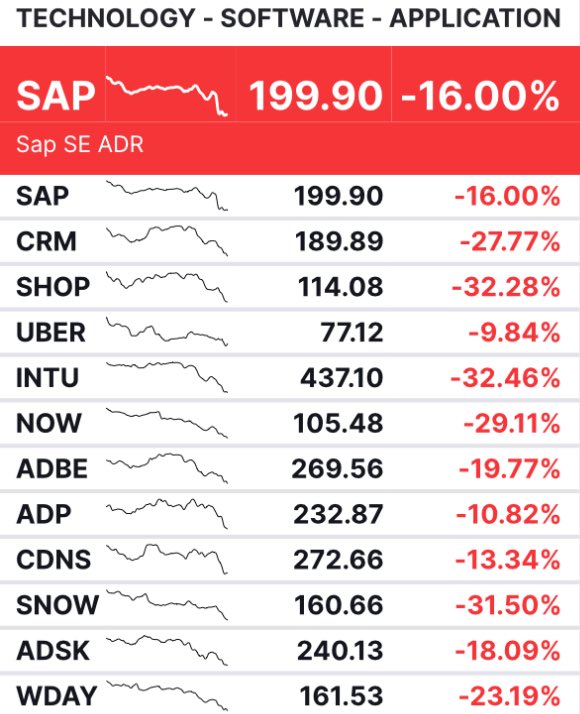

The SaaS carnage is confusing for this simple premise:

If AI is going to commoditize all of SaaS, then why isn’t the market rotating heavily into Semis and Hyperscalers?

If Anthropic were to destroy $CRM and $NOW, I’d imagine we need tons of compute. More than we can fathom if agents take over hundreds of billions of marketcap for SaaS companies.

Yet, the market is selling off SaaS AND AI names which doesn’t seem to make sense if all the demand for the SaaS carnage will lead to AI growth.

Also, how is AI a bubble if we are talking about massive enterprise software companies being decimated by AI?

The entire logic behind the selloff feels more like forced, structural rotation without a pure reason for why the rotation is happening.

From Goldman: “The forward P/E multiple for software has declined from 35x in late 2025 to 20x currently, representing the lowest absolute level since 2014 and the smallest premium to the average S&P 500 stock since 2010.”

Say what you want, but I'm right.

CNN: Tesla scraps Model S and Model X to build robots

"Tesla (TSLA) CEO Elon Musk, who turned an upstart electric vehicle maker into an industry-changing powerhouse, is pulling the plug on the two models that helped get him there, as he struggles with another quarter of declining profits and car sales.

He announced the end of production of two models – the Model S and Model X, among the company’s most expensive models, on a Wednesday earnings call. Instead, the company will use that factory space to build humanoid robots instead."

Foundations: The Tragic Algebra of Stock-Based Compensation https://t.co/LuacufI6Ps

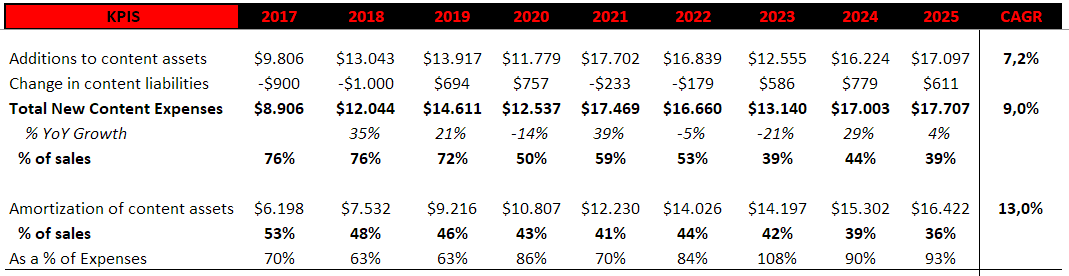

Una de las claves en la tesis de $NFLX

El apalancamiento masivo que tienen y tendrán sobre los gastos en contenido

En el mismo periodo de tiempo, las ventas han crecido al 12.6% CAGR

Mirad la diferencia del efecto compuesto

@Fontainelantop1 Como está la situación no se pierde nada, solo el coste de oportunidad pero son 2-3 meses más. Y en caso de salir victoriosos podemos llevarnos una buena ganancia.

Gracias por todo el trabajo