Trying to make sense of three basic facts about our macroeconomy:

(1) Fed has tightened substantially over past 15 months.

(2) There are essentially no visible effects in the labor market.

(3) Price inflation has fallen.

Yield curve inversion as predictor of recession has failed. 10-year Treasury yield (orange) fell below the federal funds rate (white) in 2019, much as it fell below the funds rate in 2022. In neither case did recession happen. Time to send the inversion signal into retirement...

If the dollar is set to rally from here, what does that mean for inflation? A short 🧵

Conventional wisdom holds that if the dollar rallies, US inflation will fall. A good narrative, as the US is a net importer, and imports become cheaper when the dollar strengthens

BUT...

1/8

Biggest market puzzles

1. If global growth is so strong, why are oil prices flat?

2. Why no China reopening lift to commodity prices?

3. Why are yield curves inverted if there's no recession?

4. Why do so many people want to be long Euro?

5. Why has Fed pivot not lifted S&P 500?

WHATS HAPPENING WITH US EMPLOYMENT / PAYROLLS and implications

a thread:

1/x

After a +517k Jan 23 payrolls & resilient employment mth after mth despite a year of rate hikes, whats really happening & does it mean soft landing?

read on

#macro#unemployment#stocks $SPY $QQQ

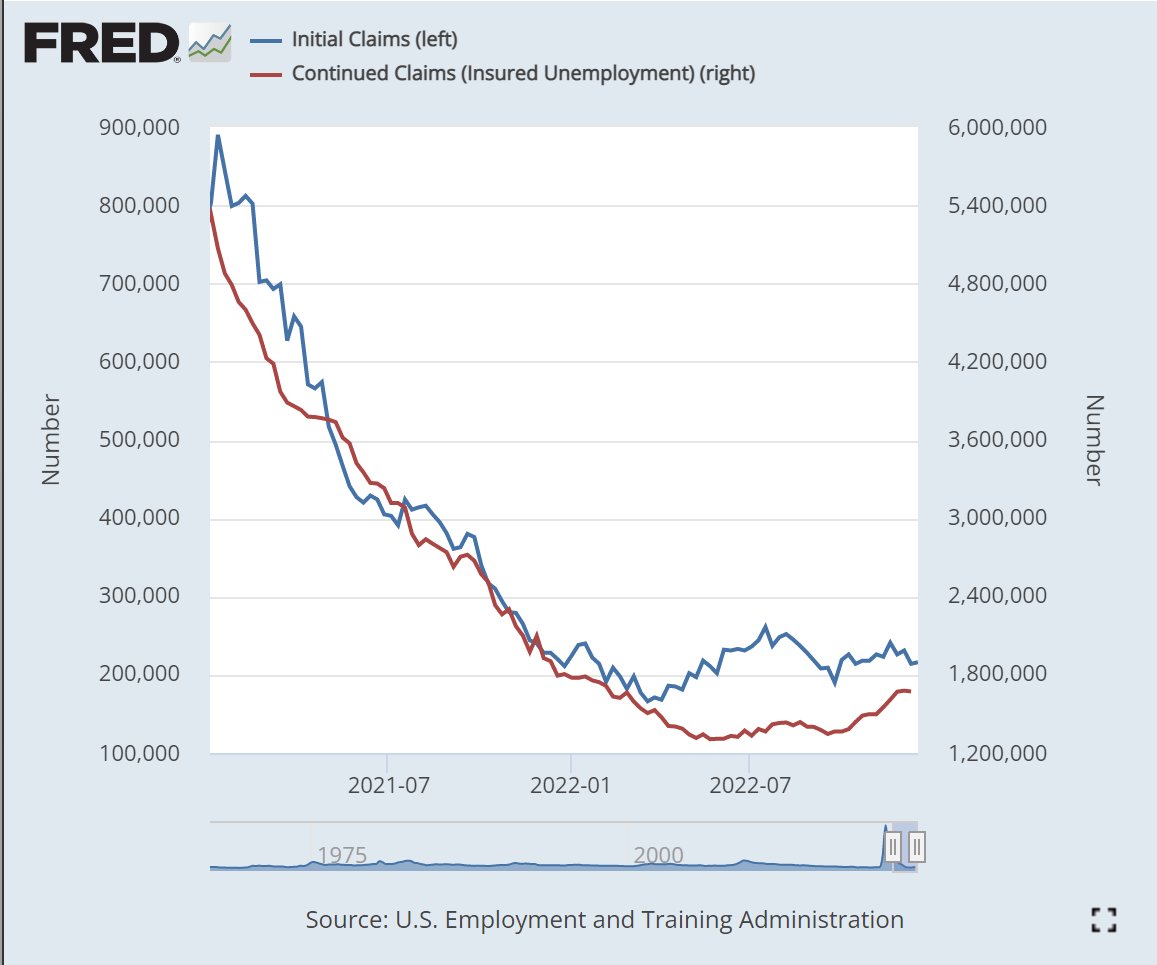

This is your weekly reminder that the US labor market remains secularly tight.

Initial claims SA basically stable at 216k. NSA ticking down. Been in a tight channel for all of '22. Continuing claims stabilizing another week at just under 1.7mln.

Very far from recession.

Anybody who has cared about making the ‚work pays‘ variety of capitalism work should have a look at @davidautor s new research. The US have actually managed to engineer substantial real gains for low wages through the market

https://t.co/KK5JMprAEh

H/t @MESandbu /1

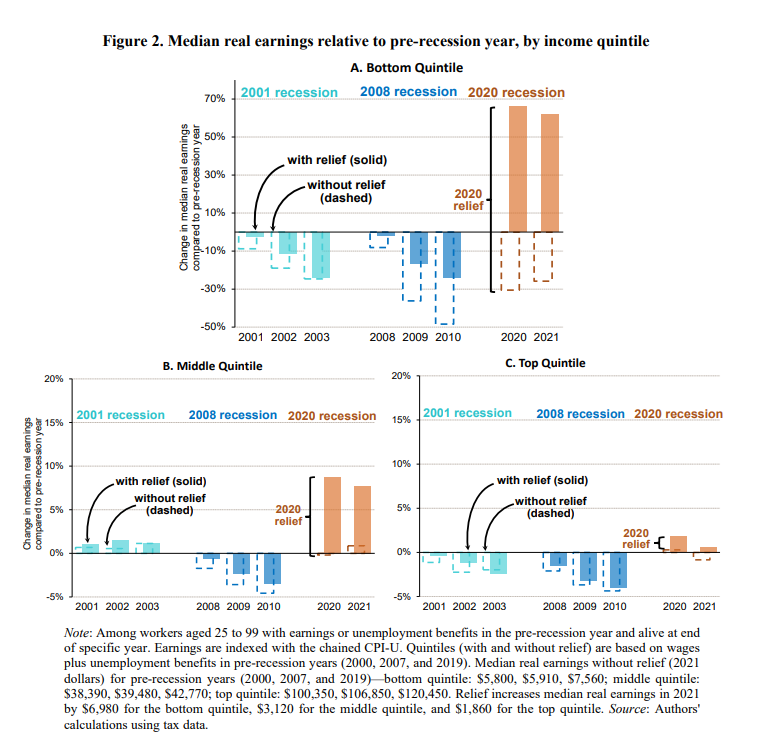

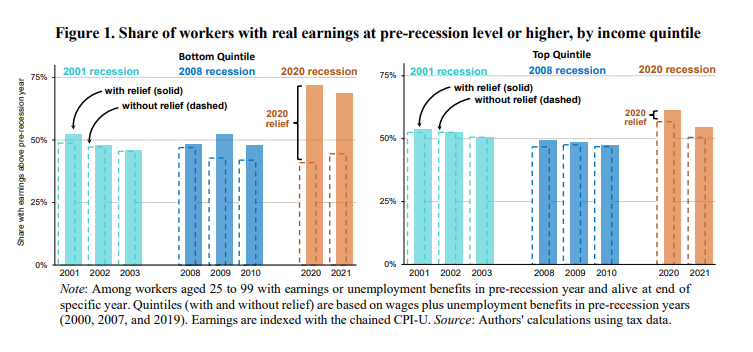

Using IRS tax records, researchers at the JCT and Federal Reserve found that the lowest-income earners saw earnings gains in 2021 while the top quintile saw declines — the opposite of what occurred after the recessions in 2001 and 2008 https://t.co/KQxSyRjlES

At this point, the Bank of Japan has pulled the goalie and is hoping for a last-second tying goal. Maybe get to overtime. Maybe somehow pull it out. Except they’re down 5-1. The game is over, and they just don’t know it yet.

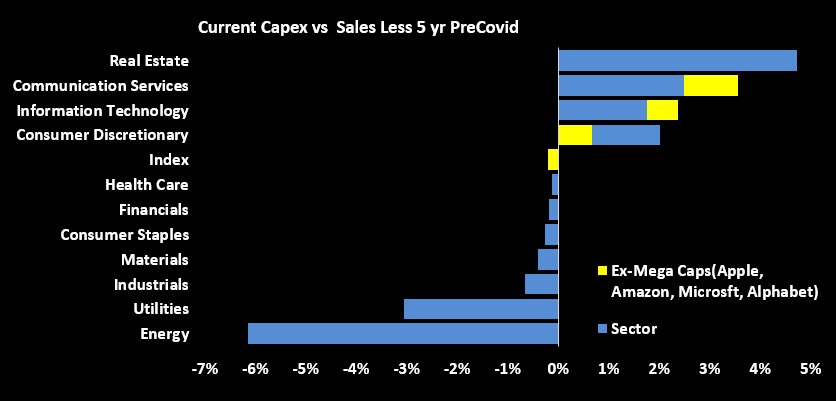

Capex-to-sales ratios well below prepandemic averages for most segments of the S&P 500 supports the idea that a recession will not be particularly deep this time around.

What’s happening now that Fed slowed hikes pace as inflation is slowing but labor market still hot? Real disposable incomes are going up and that is anything but recessionary. US curves will have a painful wake-up!