I help people with $1M–$10M+ portfolios coordinate investments, taxes, retirement, and risk.

That includes business owners, executives, high-income professionals, retirees, and families who have already built meaningful wealth.

At this level, the biggest financial mistakes usually come from treating decisions separately.

A portfolio decision can create tax consequences.

A tax decision can affect retirement income.

A retirement decision can change how much risk the portfolio should take.

And concentration risk can show up across a business, company stock, real estate, or even a diversified-looking index fund.

My work is about helping those pieces fit together.

Here I write about how taxes, portfolio decisions, retirement income, charitable giving, concentration risk, market risk, and overlooked opportunity sets fit together.

The goal is simple: make better decisions with the wealth you already built.

Near the end, the riskiest portfolios often produce the best returns.

The concentrated bets.

The crowded trades.

The stocks everyone is talking about.

For a while, they can make discipline look outdated.

That's the trap.

As those investments keep outperforming, investors naturally begin measuring themselves against the hottest part of the market.

Risk management starts to feel expensive.

Diversification starts to feel unnecessary.

Patience starts to feel like a mistake.

That's often when portfolios become most vulnerable.

The goal is to build wealth over time, not win the final stage of a speculative cycle.

That's why we focus on participation without dependence.

Stay invested.

Keep compounding.

But don't build a plan that requires one story, one sector, or one group of stocks to be right forever.

Reply MARKET and I'll send the framework behind that approach.

"The Nasdaq eventually recovered."

That's one of the most common responses whenever someone brings up the dot-com bubble.

It's true.

But it also assumes quite a bit.

➢That you had 25+ years to wait.

➢That you could tolerate an 80% decline.

➢That you didn't need the money during that period.

➢That you kept buying instead of selling near the bottom.

➢That valuations and portfolio management decisions didn't matter.

➢That there was no benefit to reducing exposure when valuations became extreme and adding when expected returns became much more attractive.

And even after the recovery, the long-term Nasdaq returns from the 2000 peak have not been nearly as spectacular as the last few years make it feel.

None of this means investors should try to perfectly time the market.

But it also doesn't mean valuation, diversification, and asset allocation become irrelevant simply because an investment eventually recovered.

The question isn't:

"What looks obvious after a massive recent run?"

The better question is:

"What portfolio gives me the highest probability of achieving my goals while allowing me to stay invested through the next full market cycle?"

Those are very different questions.

The Beanie Baby bubble is easy to laugh at now.

These were roughly $5 stuffed animals that, at the peak, were trading for hundreds—and in some cases thousands—of dollars in the secondary market.

But it is also one of the clearest examples of how bubbles form.

A story forms. Scarcity gets emphasized. Prices start rising. People see others making money. Media attention reinforces the excitement. Skeptics look foolish for a while.

Then the price becomes the proof.

At some point, people are no longer buying the thing because of its intrinsic value. They are buying it because they believe someone else will pay more later.

That is not unique to Beanie Babies.

The object changes, the human behavior does not.

Tulips. Railroads. Dot-com stocks. Housing. Crypto. Collectibles. AI infrastructure.

Every cycle has its own narrative.

And the narrative usually has some truth in it.

That is what makes bubbles hard.

The mistake is assuming something cannot be a bubble just because the underlying story is real.

The internet was real. Housing was real. Blockchain technology was real. Artificial intelligence is real.

But real technology does not automatically justify every valuation, every capital spending plan, or every assumption investors build around it.

When evaluating bubble risk, the question is not:

"Is the story completely fake?"

The better question is:

"Has the story become so powerful that people are ignoring price, risk, competition, capital intensity, and the possibility of disappointment?"

That is usually where bubbles form.

Not because people are dumb, but because the story becomes so convincing that questioning it starts to feel irrational.

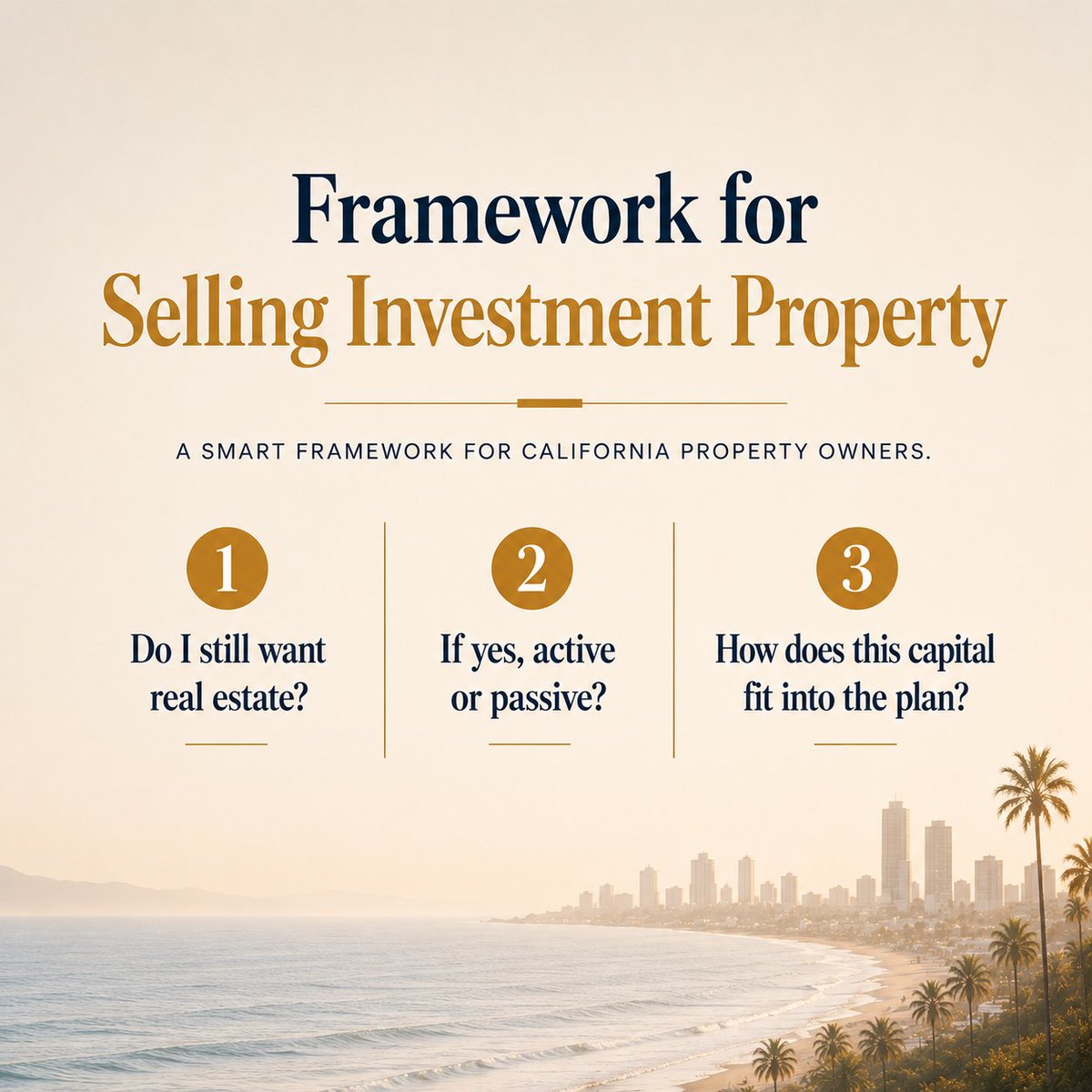

Selling an appreciated rental property without a framework is how owners end up optimizing for the wrong thing.

For high-income California property owners, the question is not just:

“Should I do a 1031 exchange?”

The better starting point is:

“What framework should I use to decide?”

Because a taxable sale, traditional 1031 exchange, and passive 1031 option all solve different problems.

Before choosing the strategy, the owner needs to answer three questions:

1. Do I still want real estate exposure?

This is the first filter.

Some owners still want real estate. Others are done. They want liquidity, diversification, fewer headaches, or more flexibility.

If the answer is “I don’t really want real estate anymore,” then forcing a 1031 exchange just to avoid tax may create a new problem. The tax may be painful, but buying another property you do not actually want can be worse.

2. If I still want real estate, do I want active or passive ownership?

Direct ownership and passive ownership are not the same decision.

Owning another rental property may mean more control, but it also means tenants, repairs, leases, financing, insurance, vacancies, and constant decisions.

A passive 1031 structure may reduce the management burden, but it usually comes with less control, limited liquidity, and reliance on the quality of the sponsor and underlying properties.

So the question is not just:

“Can I defer the tax?”

It is:

“What type of ownership still fits my life?”

3. How should this capital fit into the rest of the plan?

This is the step many owners skip.

A rental property may be one asset, but the sale proceeds can affect the entire balance sheet:

income needs, portfolio risk, cash reserves, estate planning, retirement timing, future liquidity, and concentration in real estate.

That is why the “best” answer is not always the one that defers the most tax.

A traditional 1031 may keep more capital working. A passive 1031 may reduce management responsibility. A taxable sale may create the flexibility the owner actually needs.

None of these paths is automatically right.

The practical framework is:

Do I still want real estate?

If yes, do I want active or passive exposure?

And how does this capital fit into the rest of the plan?

Once those answers are clear, the strategy usually becomes easier to decide.

#RealEstateInvesting #1031Exchange #PropertyOwners #CaliforniaRealEstate #InvestmentStrategy #PassiveIncome #RealEstatePlanning #TaxPlanning #RentalProperty #WealthManagement

The biggest risk for families with $1M–$10M+ portfolios often isn’t one bad investment.

It’s disconnected decisions.

Many families have a lot of the right pieces in place:

Investments.

Tax preparation.

Estate documents.

Insurance.

Retirement accounts.

Real estate.

For many, also a business, equity compensation, or concentrated stock position.

But the bigger question is whether those pieces are actually working together.

A portfolio can look reasonable on its own while still being out of sync with the broader plan.

Here’s what disconnected planning looks like:

The investment strategy is not coordinated with the tax plan.

The estate documents do not match account titles or beneficiary designations.

The retirement income strategy is unclear.

The risk level does not match what the plan requires — or what the family can actually live with in a difficult market.

The CPA, attorney, advisor, and insurance professional are each doing useful work, but no one is clearly responsible for connecting the moving pieces.

That is why I put together a short self-assessment:

7 Planning Mistakes Families With $1M–$10M Portfolios Often Miss

It is designed to help identify where your financial plan is well coordinated — and where important gaps deserve a closer look.

If you’d like a copy, comment or dm me “assessment” and I’ll send it over.

“Should we sell from the portfolio or borrow?”

That is usually the first question when a family is considering a major purchase.

A second home.

A major renovation.

Helping an adult child buy a house.

A large tax bill after a liquidity event.

A lifestyle purchase right before retirement.

At first, it sounds like a simple choice:

Use portfolio assets.

Or take on debt.

But that is too simplistic.

The better question is:

“What is the true cost and risk of each option?”

Selling from the portfolio can feel clean.

No new loan.

No interest payments.

No monthly obligation.

But the cost may be larger than it looks.

Selling could mean:

→ triggering capital gains taxes

→ giving up future compounding

→ selling during an unfavorable market

→ disrupting the portfolio allocation

→ reducing assets meant to support retirement

→ using liquidity today that may be needed later

Borrowing can look attractive because it preserves the portfolio.

But debt is not just “debt.”

The details matter.

→ What is the interest rate?

→ Is it fixed or variable?

→ Is the interest potentially tax deductible?

→ Is the loan amortizing, interest-only, or due as a balloon payment?

→ Can it be prepaid without penalty?

→ Can the lender change terms, call the loan, or require more collateral if markets fall?

→ Does the payment still work if income drops, a business has a slower year, or retirement begins earlier than expected?

Those details can completely change the answer.

A 4% fixed-rate mortgage with a long repayment period is a very different planning decision than an 8% variable-rate securities-backed line of credit.

A deductible interest expense is different from nondeductible consumer debt.

A loan that fits comfortably within cash flow is different from a loan that only works if markets cooperate.

For a high-income household, the comparison should usually be made on an after-tax basis.

Not just:

“What rate is the loan?”

But:

“What is the after-tax cost of borrowing compared with the after-tax cost of selling investments?”

For example, if a family needs $500,000 for a major purchase, the decision is not just where the money can be accessed.

It is what that funding source does to the rest of the plan.

Selling may reduce debt risk but create taxes and shrink the portfolio.

Borrowing may preserve investments but add interest cost, repayment pressure, and downside risk if markets or income change.

Sometimes selling is cleaner.

Sometimes borrowing preserves more flexibility.

Often, the best answer is a blend:

Sell part.

Borrow part.

Use cash reserves.

Spread gains across tax years.

Sell lower-gain assets first.

Borrow temporarily, then pay it down after a planned liquidity event.

Match the debt term to the expected source of repayment.

The mistake is treating the question as:

“Where can we get the money?”

The better question is:

“Which funding source creates the least strain on the overall plan?”

The goal is not to avoid taxes at all costs.

And it is not to avoid debt at all costs.

The goal is to compare the real tradeoff:

Tax cost.

Interest cost.

Portfolio risk.

Cash-flow flexibility.

Repayment timeline.

Retirement impact.

Downside scenario.

For major purchases, the funding decision should not be based on whichever account is easiest to access.

It should be based on the best overall choice after weighing all the factors.

#FinancialPlanning #PortfolioManagement #InvestmentStrategy #DebtVsEquity #TaxPlanning #RetirementPlanning #WealthManagement #MajorPurchases #CashFlowManagement #RiskAssessment

One thing I find interesting here is that AI adoption and AI ROI are often treated as the same thing.

They’re not.

AI can absolutely create value while companies simultaneously work aggressively to lower inference costs, improve routing, and increase caching.

That’s exactly what you’d expect if management is trying to maximize ROI.

The more interesting investment question isn’t whether AI is useful—it’s whether the value created ultimately exceeds the enormous capital required to build the infrastructure behind it.

How to keep AI spend flat while token usage grows exponentially: Not with friction and spend alerts. With better defaults, routing, and caching.

Better Defaults (not Usage Caps) – Engineers can choose any model they want, but defaults matter. We’re experimenting with defaulting to open weight models like GLM 5.2 and Kimi 2.7 through our LLM gateway, while still encouraging engineers to choose the right model for the task. 91% of our employees were never hitting their usage caps, so instead of lowering caps and driving up alerts, we're moving to cheaper defaults. Note that code reviews use a diversity of models, so they can check each other's work.

Better Routing – In our custom harnesses, we preprocess prompts and route to the best model for the job, considering cache hits and model pricing. For instance, you may want a frontier model for planning, but not for execution where they can be overkill. Ultimately, humans shouldn't be choosing models - AI can automate this task.

Better Caching – Cache misses are the easiest way to drive your cost up. All of our requests are cache aware, so we’re reusing a warm cache wherever possible. For example, our cache hit rate went from 5% → 60% in LibreChat once properly implemented.

Keep Context Lean – Start fresh sessions when switching tasks. Scope file context narrowly. Disconnect unused tools. Don't just compact. The goal isn't fewer tokens used, it's fewer tokens wasted.

Better Visibility – Our engineers can use as many tokens as they want, from whatever model they want, but we’ve made usage visible – and the more you spend on AI, the more impact we expect.

The goal isn't to suppress usage. It's to build the infrastructure that makes exponential growth sustainable.

Putting this into practice has cut our AI spend nearly in half, while our token usage continues to grow.

Brian’s post actually highlights why this is a more nuanced question. They’re reducing AI spend through better routing, caching, and cheaper defaults while maintaining or increasing usage. AI creating value and AI earning an attractive ROI aren’t the same thing. Companies optimize costs precisely because ROI depends on both value created and the total cost of delivering it.

@jackprandelli@jackprandelli great info thanks. Japan's spending their reserves down at a rapid pace too, any idea when they'll start refilling and how much demand that will add to the market?

This is critical to avoid getting carried away by one short-term statistic like Price-to-Earnings.

In a boom period 'earnings' can be highly and temporarily inflated.

I believe it is much more informative and complete to value a highly cyclical business relative to sales rather than just earnings to get a fuller picture of the multiple. After hearing again yesterday that Micron was cheap, trading at only 7x earnings, I want to highlight that Toll Brothers was trading at 6x earnings in 2006. I heard then it was cheap. After falling by 75% by late 2008, its stock was trading at 30x earnings. For a highly cyclical business, it was thus better to sell perceived ‘cheap’ and buy ‘expensive.’ This is no advice or opinion on where Micron and other memory/storage stocks go as maybe the strategic customer agreements being signed smooth out the business volatility and a higher multiple is deserved but just trying to recommend a broader way to value stocks such as this.

What if your portfolio is more concentrated than you think?

Many investors believe they're diversified because they own hundreds of stocks through an index fund.

But that's not always how risk works.

Today, a significant share of market performance is being driven by a small group of mega-cap companies tied to the same story: AI.

That means an investor can technically own hundreds of stocks...

while still being heavily dependent on 10 or 20 companies.

That's not true diversification.

It's concentrated exposure wearing diversified clothing.

The goal isn't avoiding those companies entirely.

The goal is making sure your financial future doesn't depend on them continuing to be perfect.

Because diversification isn't about how many stocks you own.

It's about how many independent drivers of return you own.

Reply DIVERSIFICATION and I'll send the framework we use to identify hidden concentration risk.

#InvestmentStrategy #PortfolioManagement #Diversification #RiskManagement #StockMarketTips #FinancialPlanning #MegaCapStocks #AIInvesting #ConcentratedRisk #InvestmentEducation

15 months ago, Micron, $MU, was worth just $60 billion producing $8.1 billion in quarterly revenue.

Today, it's worth $1.3 trillion and producing $41.5 billion in quarterly revenue.

Rarely ever does the world experience a revolution like we are seeing right now now.

The AI infrastructure boom is not happening in a vacuum.

It is pulling demand into memory chips, copper, power equipment, energy, data center land, cooling, grid capacity, and engineering talent.

That raises costs for everyone else competing for the same inputs.

And it also makes the cost of producing AI more expensive.

This is the part of bubbles people miss in real time:

They do not just destroy capital after the fact.

They distort prices while they are inflating.

Tim Cook, who told The Wall Street Journal that the jump in costs was unlike anything he had seen “in any area in over 40 years.”

Biggest price jump in anything I’ve ever seen too. https://t.co/aypJGgssnN

The Nasdaq-100 peaked in March 2000.

It didn't fully recover that high until 2015.

Think about that.

Fifteen years.

That's why chasing late in a bubble can be so damaging.

Markets can continue rising long after valuations become extreme.

Many do.

The challenge comes when investors buy after years of future success have already been reflected in the price.

When expectations break, the recovery can take far longer than most people expect.

The internet transformed the economy.

The technology story was right.

Investors who paid extreme prices still spent years recovering.

That's a lesson worth remembering today.

Great technologies create enormous value.

Successful investments still depend on the price you pay.

Reply MARKET and I'll send the chart showing what happened after the 2000 peak.

I had a client conversation today with a retiree relying on a $1.5M+ portfolio to support her income.

She is in a good financial position. Her cash-flow needs are reasonable, and based on the plan, she does not need to take excessive risk to stay on track.

So the real question was not whether she could take more risk.

It was whether she needed to.

We reviewed her risk level and talked through what portfolio declines could actually feel like in real life. Not just, “Are you conservative, moderate, or aggressive?” But something more tangible:

“If a difficult six-month period meant being down around 8% — about $120,000 on a $1.5M portfolio — would that still feel manageable?”

That matters because taking more risk is not just a chance at more upside. It also means accepting the possibility of a larger drawdown.

And if the next level of risk pushes the potential decline beyond what you are actually comfortable living with, the portfolio may look better on paper but be harder to stick with in real life.

In her case, she was comfortable with that approximate risk level. And based on her goals, cash flow, and overall financial picture, she did not need to take more risk to stay on track.

That matters right now because speculative markets have a way of making reasonable plans feel inadequate.

Cash feels lazy. Bonds feel boring. Diversification feels like a mistake. A portfolio designed around your actual life starts getting compared to whatever is working best right now.

That is backwards.

The right portfolio is not the one that looks best during a bubble. It is the one that fits your goals, your risk tolerance, your cash-flow needs, and the market environment.

Sometimes the most valuable planning conversation is not:

“How do we get more upside?”

It is:

“You are already in good shape. Let’s not let this market talk you into taking risk you do not need.”

What are the two questions to ask before selling an investment property?

Most owners focus on the first one:

Should I sell?

But the second question often matters even more:

What happens after the sale?

That is where the real trade-offs show up.

For example, say an owner sells a California investment property for $1 million.

They have $500,000 of debt, so they may think they have $500,000 of equity.

But after appreciation and depreciation, the taxable gain could be closer to $800,000 before sale costs.

That changes the entire decision.

If they sell and pay the tax, they may have closer to $220,000 left before sale costs.

If they do a traditional 1031 exchange, they may keep the full $500,000 working in real estate, but they still have to find, finance, close on, and manage another property under tight deadlines.

If they use a passive 1031 structure, such as a Delaware Statutory Trust, they may defer tax and reduce management responsibility, but they give up control and accept limited liquidity.

None of these paths is automatically best.

The right answer depends on what the owner is actually trying to solve for:

tax deferral, income, control, liquidity, management responsibility, or simplicity.

I wrote a short guide walking through a simple example and the trade-offs between selling, doing a traditional 1031 exchange, and considering a passive 1031 option.

A great technology does not automatically make a great investment.

History is full of examples.

Railroads transformed transportation.

The internet transformed commerce.

Telecom networks transformed communication.

Investors still lost enormous amounts of money when they paid prices that assumed too much future success.

AI may become one of the most important technologies of our lifetime.

Many businesses are already adopting it.

The technology is improving rapidly.

The challenge for investors is that today's prices already reflect a tremendous amount of optimism.

Investors are betting that:

• AI adoption keeps accelerating

• massive infrastructure spending pays off

• profit margins remain strong

• competition stays manageable

• today's leaders remain dominant

Those assumptions may prove correct.

But when a stock already reflects years of future success, the margin for error becomes very small.

That's why valuation matters.

The technology can succeed.

The businesses can succeed.

Investors can still earn disappointing returns if they pay too much for that success upfront.

History has taught that lesson many times.

Reply AI and I'll share the framework we use to evaluate transformational technologies as investments.

If you own the S&P 500, you're making a much bigger bet on AI than you probably realize.

A small group of mega-cap technology companies now represents an extraordinary share of the market.

Those same companies have become the primary drivers of index performance.

As a result, many investors who believe they are broadly diversified are increasingly dependent on a handful of companies and one dominant theme.

That's an important risk to understand.

Because concentration often feels safest when it's working best.

The largest companies keep outperforming.

The headlines stay optimistic.

The story becomes harder to question.

Then investors wake up and realize their portfolio was far less diversified than they thought.

This isn't a prediction that those companies will fail.

It's a reminder to understand what actually drives your returns.

Because owning hundreds of stocks doesn't automatically mean you're diversified.

Reply RISK and I'll send the framework we use to evaluate concentration risk in today's market.

The AI investment thesis has a narrow path.

Narrative:

AI will be useful, so the buildout will work.

Reality:

A technology can succeed while the investment assumptions fail.

We've seen something similar before.

In the late 1990s, telecom companies built infrastructure around forecasts that internet traffic would double roughly every quarter.

Traffic growth was extraordinary...

But it was closer to doubling annually.

Think about that for a moment.

Doubling annually is still one of the fastest adoption curves in history.

The internet changed the world.

But it wasn't enough to justify the amount of fiber, infrastructure, and capital being deployed.

The internet succeeded.

The investment assumptions failed.

The enormous AI buildout faces a similar risk.

The narrow path has two sides.

Side #1: Compute demand disappoints.

A huge part of today's AI investment boom assumes an enormous and continually growing need for compute, requiring trillions of dollars of investment in data centers, chips, networking equipment, and related infrastructure.

But enterprises are increasingly incentivized to route work to the cheapest option that gets the job done while using less compute.

Summarization.

Search.

Extraction.

Drafting.

Classification.

Document review.

Customer service.

Many of the most valuable use cases may not require the largest or most expensive models available.

If AI adoption grows rapidly but companies increasingly use cheaper models, compute demand could grow much more slowly than investors currently expect.

Side #2: Compute demand is real, but the infrastructure can't keep up.

Even if demand is enormous, data centers still need power.

They need chips.

Cooling.

Transmission.

Permits.

Construction.

If those bottlenecks delay deployment, the revenue needed to justify today's commitments arrives later than expected.

Either way, the path is narrow.

If compute demand disappoints, the infrastructure is overbuilt.

If compute demand is real but deployment lags, the cash flows arrive too late.

The market is currently underwriting a near-flawless conversion of capex into future cash flow.

That is a much bigger assumption than simply saying:

"AI will be useful."

That does not mean investors need to avoid AI entirely.

It means they should understand how much of their portfolio now depends on a very specific outcome:

Massive compute demand.

Rapid infrastructure deployment.

Fast monetization.

Attractive returns on enormous capital spending.

AI can be useful without every AI-linked investment being attractive.

Participation is one thing.

Dependence is another.