The instinct is to buy uranium through $URA, the popular basket.

Don't.

Our silver work showed the miner basket delivered about 1x the metal, not leverage, and URA is diluted the same way.

The leverage is in the parts, not the basket.

Full trade:

https://t.co/1t1TZC2M8a

Every war has winners, and the wire just named one of this one's quiet ones.

While Kuwait's airport burns and Bahrain takes missiles, Saudi Arabia's economy is proving resilient enough to pull in wartime Gulf business. Capital, companies and activity are migrating toward the part of the Gulf that looks safest.

This is the second-order story I am most interested in, and the one the oil tape ignores completely. A regional war does not just move the oil price. It redraws the economic map of the region. It re-rates jurisdictions. The Gulf state seen as stable in a crisis wins flows from the ones that are not, and those shifts outlast the shooting.

Airlines rerouted over Syria and handed Damascus a windfall. Now business reroutes toward Riyadh. The map is being redrawn in real time by where people feel safe putting capital.

When the ceasefire finally comes, the oil price will mean-revert toward something. The redrawn Gulf map will not. Some of these shifts are permanent.

The trade in front of you is crude. The trade behind it is which Gulf jurisdiction comes out of this bigger.

Want to see where this oil shock actually lands? Look at the airlines.

IATA said today that many airlines are being hit hard by jet fuel price swings, and not all of them can hedge.

That second part is the one that matters. Hedging is not free and it is not available to everyone. The big carriers lock in fuel months out. The smaller ones, the ones in weaker markets, the ones whose credit will not support a hedging book, are simply exposed. They eat the spot price.

So a chokepoint event thousands of miles away becomes a margin event in an airline's next quarter, and the carriers least able to absorb it are the ones flying naked into it.

This is the pattern I keep coming back to. Oil is the headline. The damage shows up two and three steps downstream, in the cost line of a business with no strategic reserve, no substitute, and now no hedge.

The strait is a story about ships. The bill arrives in industries that never touch the water.

Which other sectors are flying unhedged into this? That is where the next earnings shock is hiding.

The war just changed shape, and almost nobody is pricing the new one.

For three months this was the US and Israel against Iran. The Gulf monarchies, Kuwait, Bahrain, Saudi, were nervous bystanders hosting US bases and praying it stayed offshore.

It did not stay offshore. Iran put missiles into Kuwait's international airport, killing a civilian and injuring 63. It hit Bahrain, home of the US Fifth Fleet, for the first time since April. And Iran's foreign ministry said the "colonial use of the territories" of those countries places "direct and clear responsibility" on the rulers of Kuwait and Bahrain.

That is not a warning to Washington. That is a threat to the monarchies. Iran is telling the Gulf hosts: keep letting the US operate from your soil and you become the target.

The oil risk premium is not just about the strait anymore. It is about whether the Gulf states get dragged in as combatants. Every airport hit, every base struck, widens the war and the premium with it.

The market is pricing a ceasefire. Iran is busy turning the neighbours into front lines.

Let me give you the state of US diplomacy this week, in the President's own words.

He confirmed he called Benjamin Netanyahu, the leader of America's closest ally in the region, "crazy" on a phone call.

In the same week, he said of Iran's Supreme Leader, whose forces just bombed Kuwait's airport and killed a civilian, that they are "getting along quite well" and he "probably will" meet him "at some point."

So the ally is crazy and the enemy is a friend. The man Iran is shooting at is the man Trump is golfing toward, and the man fighting alongside the US is the one Trump is calling unhinged on a call.

This is the foreign policy the oil market is trying to price. Brent has been yanked from a six-week low to 98 dollars on this stuff.

My advice on trading the President's relationships: don't. You cannot build a position on a man who calls his friend crazy and his enemy "quite well" on the same fucking Wednesday.

Trade the barrels. The barrels are not insane.

This is the most important sentence in today's wire, and it kills the trade most people are in.

A Kuwait Petroleum executive said Kuwait could restore 70 percent of its oil output within 6 to 8 weeks of Hormuz reopening.

Read that slowly, because the market has not.

Seventy percent. In six to eight weeks. After the strait reopens.

So even in the bull case, the one where diplomacy works and the ships sail, a major Gulf producer is telling you it limps back to two-thirds of normal in two months, and the last third takes longer.

That is not a V. It is not fucking close to a V. The market is pricing crude as if the day Hormuz reopens, the barrels flood back and the price collapses. The people who actually run the production are quoting you months to reach 70 percent.

I have said this since March. There is no V-shape. The reopening is the start of the recovery, not the end of the crisis.

When the producers themselves quote six to eight weeks for 70 percent, why are you short crude on a ceasefire rumour?

Here is a detail from this morning's wire that should stop you cold.

Vessels are now stuck inside Hormuz.

Not turned away at the entrance. Trapped inside the Gulf, unable to get out. Ships that sailed in before the disruption, or got caught mid-transit, are sitting there with cargo they cannot move and war-risk premiums compounding by the day.

This is what a real chokepoint event looks like, and it is the opposite of how the market prices it. The screen treats Hormuz as a switch: open or closed, risk-on or risk-off. The reality is a building queue of stranded steel, demurrage stacking up, charter rates blowing out, cargo owners eating losses they never priced.

I wrote in There Is No V-Shape that the crude rebuild takes quarters and the market was pricing weeks. The ships trapped in the Gulf right now are the first physical evidence.

You do not clear a traffic jam of supertankers the morning a fucking ceasefire is announced. The disruption is not a headline. It is a logistics knot, and knots take time to untie.

The President of the United States got on the phone yesterday with, in his words, "highly placed Representatives" of Hizbollah.

Let that sit. The US has Hizbollah on fucking speed dial now.

He emerged to announce that Israel and Hizbollah had agreed "all shooting will stop." A ceasefire. Done. By phone.

Three problems.

One: Reuters reports the ceasefire is partial and the attacks are continuing.

Two: Netanyahu, the same evening, said the IDF "will continue to operate as planned in southern Lebanon." The other party to the ceasefire, saying he is not stopping.

Three: this is the conflict where Israeli troops seized a crusader castle two days ago and a million Lebanese have been displaced since March.

So we have a ceasefire announced by a man who is not doing the shooting, agreed by a militia through intermediaries, and contradicted within hours by the actual army on the ground.

Trump also told everyone to "sit back and relax, it will all work out in the end. It always does."

Crude is up 4 percent on the day. Relaxing yet?

Yesterday Iran vowed to completely close the Strait of Hormuz.

This morning, Reuters: oil products exited Hormuz and an LNG tanker loaded at the UAE.

So which is it? Complete closure, or tankers still loading?

The binary misses the point. The strait has never been fully shut, and it is not shut now. Iran has slowed the flow to a trickle, and it controls the dial. It has spent this entire war turning that dial, not slamming it to zero.

That is not weakness. It is strategy. A complete closure invites the maximum military response and unites the world against you. A managed trickle bleeds the global economy slowly, keeps the oil price as a weapon, and preserves deniability. The dial is better leverage than the off switch.

So when Iran threatens complete closure, it threatens the one thing it has carefully avoided for three months. The threat is the product. The closure is not.

Watch the tankers, not the press release. They tell you where the dial actually is.

The trade everyone is reaching for right now is wrong, and wrong in a specific, expensive way.

The instinct on an oil shock is risk-on for hard assets. Oil up, gold up, silver up, everything real up. Buy the crisis.

That is not how the last flush worked, and it is not how this one works.

When the oil draw actually bites, and the inventory math says weeks not months, it does not resolve into a clean commodity rally. It resolves into a dollar-liquidity squeeze. Everyone needs dollars at once, and to get them they sell what they can sell, which is everything liquid.

The tape from the last one: gold miners fell 12 to 15 percent on flat gold. Silver crashed 30 percent in thirty hours. Not because the thesis broke. Because holders needed dollars, and the metal was what they could sell.

So the first move in a real energy shock is not everything up. It is the dollar up and everything else down, hard, together.

That flush is not the risk. With levels and patience, it is the entry.

Everyone is about to trade uranium exactly wrong.

The headline says energy crisis, so the screen will buy anything that glows, chase the spike, then dump it in the panic alongside everything else liquid when the dollar squeeze hits.

Both moves miss the point, because uranium is not a war trade. Uranium does not move through Hormuz. There is no supply shock for the metal in this conflict. Only sentiment, and a liquidity flush.

What actually moves uranium is a piece of plumbing almost nobody models: the tails assay. When enrichment was cheap, enrichers stripped extra uranium and sold the surplus, and that secondary supply capped the price for a decade. Enrichment is now expensive, SWU sits at 200, up nearly 500 percent from its low, and that surplus is drying up. The bid was there last week. It will be there the day the strait reopens.

So I am not trading the war. I am using the panic it creates to buy a thesis the war cannot reach.

Physics is physics. Let the screen scream.

Here is the consequence of the Hormuz crisis that actually matters, and it printed this morning.

China is tapping deeper into its oil stockpiles as its crude imports hit a decade low.

China is the largest oil importer on earth. When it cannot get the barrels it wants through a disrupted strait, it does not simply pay up. It reaches into its strategic reserve and drains it.

A strategic reserve is a buffer. It exists precisely so a country can ride out a supply shock without the price exploding. China is now burning that buffer.

That is the quiet clock under this whole crisis. Every barrel China pulls from its reserve smooths the price today and is gone tomorrow. The buffer is finite. The disruption is not.

The market is watching the ceasefire headlines. It should be watching the inventory. When the largest importer is draining its tanks to keep the lights on, the V-shape everyone is pricing is not fucking coming.

What happens to the price when the buffer runs out?

Yesterday Iran ended all negotiations and vowed to completely close the Strait of Hormuz. The tape treated it as the death of diplomacy.

Today, Reuters: Iran is eyeing a limited deal with the US to relieve economic strain and buy time.

Read those two sentences together and you have the whole game.

The walk was not the end of the negotiation. The walk was the negotiation. You do not threaten to shut the world's most important oil chokepoint because you want war. You do it because you want a better price at the table, and a sanctioned economy that is bleeding needs the table more than it needs the threat.

Iran is not trying to close Hormuz. Iran is trying to get paid not to close Hormuz, and to buy time while it does.

So when the screen panicked on the closure threat and crude gapped six dollars, it traded the press release, not the position.

The headline is the leverage. The leverage is not the fucking plan.

Let me argue against myself, because objectivity matters.

I am not saying all private credit is fake. I am saying the marks are only trustworthy when something forces them to be.

Here is the clean case. There is a software loan called Cloud Software Group. Performing borrower. Its loan draws live quotes from more than one dealer, a Bloomberg composite, and the fund marks, and all of those numbers cluster within about two points of each other.

When liquidity exists, the marks converge on it. The model works. The system is fine.

That is the whole point. The problem was never private credit as a category. The problem is the specific loans where no dealer quotes, no composite prints, no buyer exists, so the only number is the one the manager wrote down and nobody can check.

Cloud Software Group has a market keeping it honest. Medallia does not. CDK barely does.

The question is never "is the mark too high." It is "is there anything in the world that would force this mark to move."

For a frightening share of these loans, the answer is no.

The US announced this week that a peace deal is near.

Iran's response, on the record: "actions, not words."

That is where the negotiation now sits. One side keeps announcing progress. The other publicly refuses to believe the announcements and demands proof.

This is not a misunderstanding. Iran has watched the US announce a deal, blame Iran for it failing, then announce it again, for weeks. Tehran has learned not to trust the press release. So now it wants acts, not adjectives.

And it is right to. The same week the US said peace was near, it imposed fresh sanctions on Iranian oil sales and kept twelve billion in frozen assets frozen. The actions and the words point in opposite directions.

When one side openly says it no longer trusts a word the other says, you do not have a deal that is nearly done.

You have two countries that have stopped believing each other, and a mediator pretending that is not what is happening.

People keep asking what the trade is. Here it is, for an institution, cleanly.

Long the syndicated loan market. Short the public equity of the private credit funds whose books are heaviest in the loans nobody can price.

That is the whole thing. You are long the asset that has already marked its losses honestly, where the prices are real. You are short the asset carrying the same kind of risk at a number a model invented and nobody has tested.

The beauty is it does not need a crash. It does not need the marks to collapse. It only needs them to converge toward a market that is already visible. The gap closes, you win, in either direction.

And it pays you to wait, because the long loan side earns a yield while you hold it.

One layer down, if you want the most levered version, CLO equity sits on top of the exact cohort of marks I do not fucking trust. I would not touch it here. That is the piece that goes to zero first when the model finally meets the market.

The author of The Art of the Deal has negotiated himself into a box with no good exit.

Walk through his options.

He cannot walk away. He has spent months promising a "great" deal, the midterms are in November, and oil prices are a domestic problem. Walking away means admitting the historic endeavour produced nothing.

He cannot sign a bad deal. He has publicly said it must be "perfect," he must get the uranium, the strait must open immediately with no tolls, and no money changes hands.

And he cannot get a perfect deal, because the one thing he demands, the uranium, is the one thing Iran will not surrender, and the one thing Iran demands, the money, is the one thing he will not give.

Every door is locked. He cannot leave, cannot settle, cannot win.

So what exactly is he going to "soon decide"? You cannot decide your way out of a box you talked yourself into.

Picture nine funds marking the same loan, CDK, to within half a point of each other. That loan has a market price they can all see.

Now watch a loan with no market price.

Medallia is a software loan sitting in those same funds. Ask the Bloomberg terminal what it is worth and the answer is: "No sources are pricing this security." No market. No quote. Nothing.

So the funds make up the number themselves. Here is what they produced, independently, for the same loan, on the same date.

BCRED: 62. Apollo's fund: 58. HLEND: 60.

Three funds, same loan, same day, four points apart.

On CDK, where there is a market to copy, they agree to within half a point. On Medallia, where there is no market to copy, they are four points apart and every number is a guess.

That is the whole thing in one comparison. These marks are only precise when somebody else has already done the pricing. Take the market away and they cannot agree to save their fucking lives.

While everyone reads the "peace is near" headlines, here is a fact from the same day.

The US military turned away a blockade runner trying to reach an Iranian port.

Sit with that. The naval blockade is fully operational. Ships are still being intercepted. The strait is still effectively shut. A fifth of the world's oil transit is still not moving normally. Nothing about the physical reality of this crisis has changed.

And yet Brent settled at a six-week low this week, because a framework nobody has signed, that Iran says does not exist, that Trump says he will "soon" decide on, is supposedly close.

The market is pricing the end of a crisis whose physical facts are exactly where they were a month ago. The blockade is real. The mines are real. The intercepted ship is real. The deal is a press release.

You are short a closed strait on the strength of a fucking maybe. Good luck.

CDK is the jar that got opened.

The rest of the storeroom sits sealed, at the marks of the people who sold it.

The honest question isn't which marks are right.

It's which could ever be shown wrong, and by whom, and when.

Full piece: https://t.co/Q2nZfrbdZj

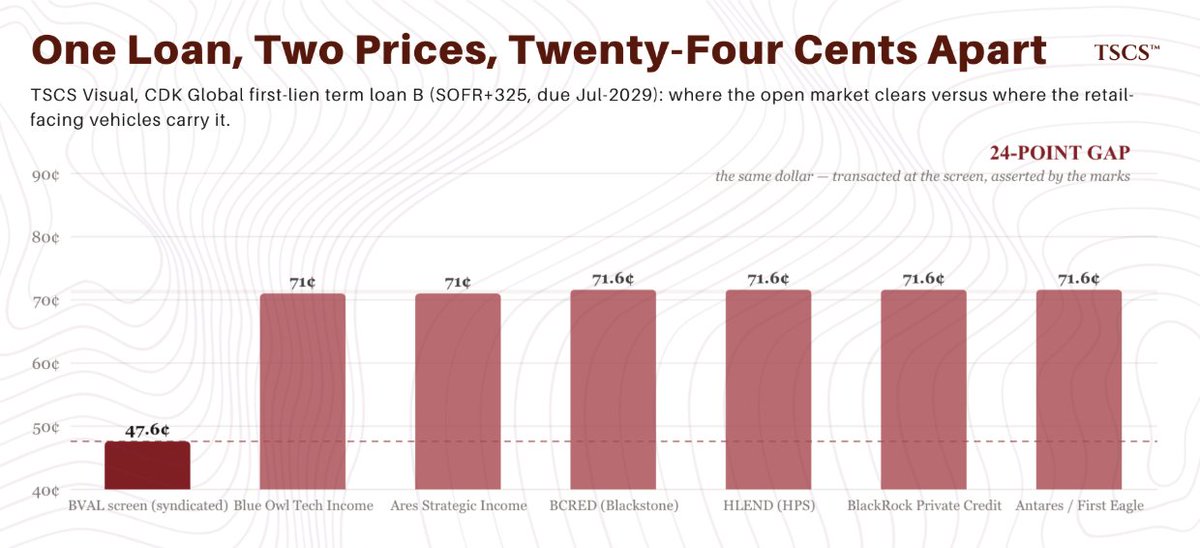

Everyone's watching ServiceNow swing from $211 to $81 and back.

The real story is the loan that never moves.

CDK Global. The market prices it at 47.6 cents.

The retail funds holding it carry it at 71.6.

Same loan. Same day. A 24-point gap nobody is forced to close. 🧵

And the exit is rationed.

These wrappers cap redemptions near 5% of NAV a quarter, pro rata.

Built for the exact moment everyone concludes the same thing at once.

You get a fraction out, at the manager's number, behind the queue.

BCRED ran $1.4B of outflows last quarter.