How is this possible?

WhatsApp shows Last Seen: 22:39,

but my 23:25 messages are blue-ticked (✔✔).

Is this a WhatsApp glitch?

Or something related to privacy settings / background sync?

Would love to hear from tech folks and WhatsApp users.

#WhatsApp#WhatsAppBug@WhatsApp

#BiharElection2025

बिहार चुनाव ख़त्म होते ही RJD का असली चेहरा सामने आ गया 👇

नौवीं-फेल नेतागिरी — लोगों के घर जाकर धमकाना, मारपीट करना कि भाजपा को वोट क्यों दिया?

क्या ऐसे गुंडे मुख्यमंत्री बनने लायक हैं? 🤦♂️

जंगलराज लालू परिवार का खानदानी धंधा है, इसलिए लोकतंत्र इनसे कभी बर्दाश्त नहीं होता।

दूसरी पार्टी को वोट देने पर हिंसा — यही इनकी घटिया मानसिकता है 👎

“मोदी चोर” कहने वाले खुद भ्रष्टाचार के ठेकेदार हैं।

जनता विकास चाहती है, और ये सिर्फ कुर्सी की लत में पागल हैं 🪑😵💫

जनता बार-बार चाबुक मार रही है, पर अक़्ल फिर भी नहीं आती 🤦♂️🔥

राहुल गांधी अब पतन के प्रतीक बन चुके हैं।

क्या कांग्रेस इस पर कभी विचार करेगी? 🤔😄

Force Motors strengthens its position again 110 Mob Medical Units flagged off in West Bengal, all built on the reliable Traveller platform. Strong govt trust, growing institutional demand, and a solid push in specialised mobility solutions.

https://t.co/HbwNG0Kj7w

#ForceMotors

Ramchandra Prasad Singh (RCP Singh) — once considered Nitish Kumar’s most trusted man, now busy searching for a new ‘Ram’ of his own. 🤔 #BiharElection2025#ElectionUpdate

Kya se Kya ho gaya

ek dailog yad aagya Tera kya hoga re kaliya

रामचंद्र प्रसाद सिंह (RCP सिंह) — जो कभी नीतीश कुमार के सबसे भरोसेमंद माने जाते थे, आज खुद नया ‘राम’ तलाशने में व्यस्त हैं। 🤔

#BiharElection2025#ElectionUpdate

क्या से क्या हो गया…

एक डायलॉग याद आ गया — ‘तेरा क्या होगा रे कालिया?’”

Ramchandra Prasad Singh (RCP Singh) — once considered Nitish Kumar’s most trusted man, now busy searching for a new ‘Ram’ of his own. 🤔 #BiharElection2025#ElectionUpdate

Kya se Kya ho gaya

ek dailog yad aagya Tera kya hoga re kaliya

Pennar Industries

#PennarInd#PenInd

Not a 100% pure play PEB company

956cr worth new order wins in Q2

To be executed in next 2 quarters

Should track if margins can expand in H2 with incremental revenue uptick

📊Global Giants : Bullish on 🇮🇳

• @HSBC_Global: Reaffirms bullish stance on Indian equities. End-2026 #Sensex target: 94,000 → ~13% upside from current 83,200.

• @GoldmanSachs: Upgrades India to Overweight. Sees #Nifty at 29,000 by end-2026 → ~14% upside from current levels !

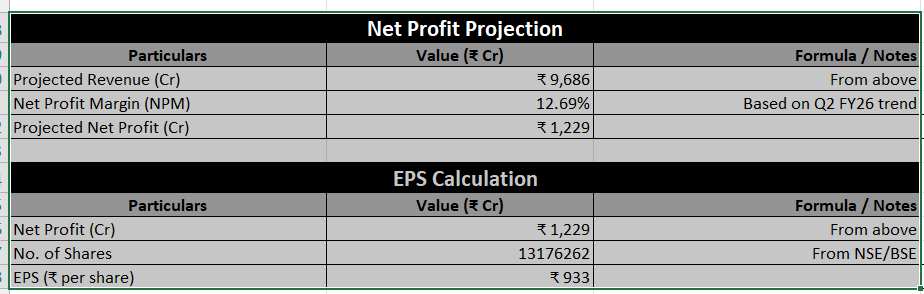

Force Motors FY26 Projection: Profitability Outlook 🔍💰

Building on the projected FY26 revenue of ₹9,686 Cr, Force Motors’ profitability looks strong.

Based on Q2 FY26 trends, the company’s Net Profit Margin (NPM) is estimated at 12.69%, leading to a projected net profit of ₹1,229 Cr.

With 1.3176 crore shares outstanding, the estimated EPS stands at ₹933.

Assuming a forward P/E multiple of 40x — the same valuation the market had already assigned to this stock even before the Q2 results — the projected stock price comes to approximately ₹37,316 per share, reflecting confidence in its growth potential.

These calculations illustrate how sustained revenue growth and stable margins could translate into significant valuation upside. However, it’s important to remember that stock market prices move on actual results, not just projections.

This is a forward-looking estimate based on current trends, not a buy or sell recommendation. Always analyze company filings and upcoming quarters before making investment decisions.

#ForceMotors #FML #Forcemotor #FORCEMOT

Disclaimer: This analysis is purely for educational and informational purposes. It is not intended as financial advice or a recommendation to buy, sell, or hold any stock. These are rough estimates based on my own calculations I’ve personally suffered losses many times in the past from such analyses. Please do your own research and consult a qualified financial advisor before making any investment decisions.

@VIVAANINVESTOR Whether it’s Force Motors or any other stock, prices can’t be predicted through Excel sheet calculations.

But such analysis is informative it helps decide whether to hold, sell, or wait based on valuations like P/E ratio and earnings trends. #forcemotors#ForceMot

Why Suzlon’s Stock Isn’t Rising Despite Strong Q2 FY26 Results

Suzlon Energy #suzlonenergy posted blockbuster Q2 FY26 results — revenue up 85% YoY, EBITDA up 145%, and PAT up 538% (₹1,279 crore). Yet, the stock slipped nearly 6%, trading near ₹57–61, down 23% from its 52-week high of ₹74.3.

Reason:

The market had already priced in optimism. Profit includes ₹718 crore of deferred tax asset — a one-time, non-cash gain.

Core profitability remains strong (EBITDA margin 18.2%), but not as explosive as PAT suggests.

Analysts also flagged limited long-term diversification (solar, storage) beyond FY27. Despite a record 6.2 GW order book, execution bottlenecks like grid and land clearance issues persist.

https://t.co/KZS5JRO9i5

Fundamentally, Suzlon looks solid — ROE 41.4%, ROCE 32.5%, debt-to-equity just 0.05, and promoter holding unpledged.

Though the market cap-to-sales (5.67x) and P/E (24.6x) suggest stretched valuations, Suzlon’s growth runway remains intact.

Hence, short-term correction reflects profit booking, not weakness.

In my experience, whenever all investors start focusing on a stock, that’s usually when its price movement begins to slow down. #Suzlon

Valuation Reset & Market Psychology

Suzlon’s Q2 rally paused due to valuation normalization and profit booking. Before results, it traded near 30x P/E — now adjusting to 24.6x, still above its historical average.

Brokerages like Nuvama and Motilal Oswal trimmed targets (₹66–74), citing DTA impact and limited FY28 visibility.

https://t.co/fv0LE2yvcg

Sector-wise, solar + BESS hybrids are capturing more market share, making investors cautious about pure-wind plays.

However, Suzlon’s debt-free status, 19.1% NPM, 23.6% QoQ sales growth, and ₹1,480 crore net cash ensure financial strength.

Despite short-term volatility, Suzlon remains India’s top wind energy player with 29% market share and a robust O&M base (15.4 GW).

The correction is a healthy consolidation before the next growth phase — not a signal of weakness.

Disclaimer: Educational purpose only, not investment advice.

#suzlonenergy #Suzlon

🧵1/2

If you want to make money, you’ve got to invest money.

The only question is — how to invest. 💭

Fear doesn’t work.

I spent 20 years being cautious…

Now, there’s absolutely no fear left. 💪

What I’ve learned —

👉 Always stay invested

👉 Keep watching results

💸🔥

#ADVAIT

#BASILIC

#INTERARCH

#IFBAGRO

#mamata #CNCRD

#ALPEXSOLAR

#PRIZOR

#EFFWA

#aimtron #SYSTANGO

#OBSCP

#ASMTEC

#Southwest

#ORIANA

#OSELDEVICE

#PURPLEUTED

#RaghavProductivity #RPEL

#DENTA #DentaWater

#SATTRIX

#INFOBEAN

Anant Raj Limited's #anantraj#StockMarket

Consolidated Financial Results:

Revenue from operations climbing 6.5% QoQ to ₹631 Cr from ₹592 Cr in Q1, propelled by robust real estate bookings and data center contributions.

YoY, revenue expanded 23.0% from ₹513 Cr in Q2 FY25,

H1 FY26 revenue rose 24.2% to ₹1,223 Cr, aligning with project launches like "The Estate One" and township expansions.

PAT 9.8% QoQ to ₹138 Cr (EPS ₹4.02), supported by higher margins (EBITDA 26%) and share of associate profits (₹1.3 Cr).

YoY PAT leaped 30.8% from ₹106 Cr, with H1 PAT up 34.1% to ₹264 Cr, reflecting cost efficiencies—finance costs flat at ₹5 Cr for H1 despite expansions—and deferred tax gains.

Employee expenses doubled QoQ due to scaling, but overall expenses grew 5.4% QoQ, maintaining PBT at 25.7%.

Balance sheet expanded 4.1% to ₹5,446 Cr, with inventories down 24% YoY on deliveries (e.g., Project Navya Phase-2).

Net debt reduced post-₹125 Cr prepayment and ₹1,100 Cr QIP; cash at ₹292 Cr.

Operating cash flow strengthened 33.7% YoY to ₹194 Cr.

Data center push to 117 MW by FY28 positions for sustained growth, though regulatory delays could impact.

#CeinsysTech — despite very strong Q2 FY26 results — hit the lower circuit at ₹1,319 (-5%) today.

As per my view 👇

Cash Flow Concern: Trade receivables jumped 65% from March to September 2025 — almost half of sales stuck, which weakens short-term cash flow.

Leadership Change: The resignation of CEO Prashant Kamat (effective Dec 31, 2025) and another WTD’s exit created uncertainty.

In my view, short-term pressure is possible, but the long-term story stays positive given the ₹1,092 Cr order book.

#CeinsysTech #StockMarket #CEINSYSTECH

Disclaimer: As always, this is just my view and not buy/sell advice. Please do your own research.

💥 #ForceMotors posted good result.

▶️Net profit at ₹350.6 Cr Vs ₹135 Cr (YoY)

▶️Revenue up 7.2% at ₹2,081 Cr Vs ₹1,941 Cr (YoY)

▶️EBITDA up 28.3% At ₹362.1 Cr Vs ₹282.3 Cr (YoY)

▶️Margin at 17.4% Vs 14.5% (YoY)

#forcemotors

Force Motors Ltd. has delivered a highly commendable performance for the second quarter of Fiscal Year 2026, ending September 30, 2025. The results demonstrate significant gains in profitability, driven by robust operational efficiency and steady top-line growth.

Key Financial Highlights (Q2 FY26 vs. Q2 FY25)

Exceptional Profit Growth: The company achieved a remarkable 160% year-on-year surge in net profit, which escalated to ₹350.6 crore from ₹135 crore in the prior-year period. This substantial increase highlights enhanced profitability and bottom-line focus.

Steady Revenue Generation: Revenue from operations recorded consistent growth of 7.2%, reaching ₹2,081 crore compared to ₹1,941 crore in the corresponding quarter last year. This growth indicates sustained, healthy demand for our vehicle segments.

Operational Excellence & Margin Expansion: The company's operating performance improved significantly.

EBITDA: Climbed 28.3% YoY to ₹362.1 crore from ₹282.3 crore.

EBITDA Margin: Expanded sharply by 290 basis points, reaching 17.4% compared to 14.5% in Q2 FY25. This critical expansion is a direct result of strategic initiatives enhancing cost efficiencies and achieving higher price realisations.

Sustained Commercial Momentum

The strong performance has continued post-quarter. The company reported a 32.1% year-on-year increase in total vehicle sales for October 2025 (2,835 units versus 2,146 units), underscoring robust demand and a strong start to Q3.

In summary, the Q2 FY26 results underscore Force Motors' strong financial health, its ability to effectively manage costs, and its successful strategy in capitalizing on market demand. The company is well-positioned for continued value creation.

HBL Engineering Limited Q2 FY26 Results

blockbuster #HBLENGINE#StockMarket

HBL Engineering reported a QoQ revenue jump of 103% (₹1,203 crore vs ₹588 crore in Q1)

YoY rise of 131% (₹520 crore in Q2FY25).

Profit before tax 175% QoQ and 380% YoY, reaching ₹520 crore even after ₹23.85 crore of exceptional expense.

Net profit rocketed to ₹387 crore, up from ₹140 crore in Q1 and just ₹80 crore last year — that’s nearly a 4.8× YoY growth!

EPS jumped to ₹13.96 versus ₹5.16 in Q1 and ₹3.13 a year ago.

The company’s electronics segment contributed heavily — ₹794 crore vs just ₹180 crore in the previous quarter — showing a phenomenal operational ramp-up.

Management itself admitted this was an “extraordinarily good quarter” that may not be repeated soon.