I have been alerted to the existence of fake profiles across @X and @Meta that fraudulently impersonate me to send out investment advice via DM. I have reported them, but please be aware that @smerler is my only legitimate X handle and I never offer investment advice in any form.

As Kevin Warsh takes over the Fed, he inherits an energy shock and Jerome Powell, who stays on the board. Warsh’s view of Al being structurally disinflationary is where conceptual frictions may emerge, as we learn more about AI and productivity. It will be interesting to watch.

The European Commission published its energy crisis plan (AccelerateEU) which is being discussed at the summit of EU leaders taking place on April 23/24. The fiscal response so far is crawling compared to what countries did in 2022:

https://t.co/XZcdKhKgkI

Two striking findings from the IMF World Economic Outlook just published - looking at who pays the cost of war and how big the macroeconomic impact of conflicts is.

Full slide set:

https://t.co/7iIziNVyx5

US March CPI recorded the largest monthly jump since June 2022 - entirely driven by energy. At the same time, consumer confidence hit a historic low and nominal wages grew at the slowest pace since May 2021. The Iran shock is squeezing real incomes.

Is this the same Commission who argued it was imperative to scale back the EU sustainability regulatory framework via the Omnibus, because green tape was supposedly killing European competitiveness?

🚨 BREAKING: The European Commission has urged people to work from home, drive and fly less, and for EU countries to urgently roll out renewables, as it warned of a prolonged energy crisis as a result of the conflict in the Gulf.

Full story: https://t.co/0IU3HD1E8u

A wild day in energy markets, with Brent breaking through $119 before dropping below $90 on Trump’s comments hinting at a potential offramp. So far, the conflict has pushed oil prices almost 30% above baseline - to be seen whether this reversal proves stable.

Want to know why Europe lags in innovation? Exhibit 1: less than 5% the EU Innovation Fund established in 2021 has been paid out, because companies spend up to 3’000 hours and an average 85’000€ in administrative costs to apply.

https://t.co/iiw6JjfBA7

The debate on the Euro is shifting. A growing number of mainstream economists point out that ECB backstops for high-debt countries put debt on an unsustainable path. That shouldn't need saying, but in the Euro zone it does. The ECB needs deep reform and must exit debt markets...

@robin_j_brooks There’s nothing personal and I did not call you any names. I think you are wrong to make the claim you make the way you make it, and think it’s fair to say as much.

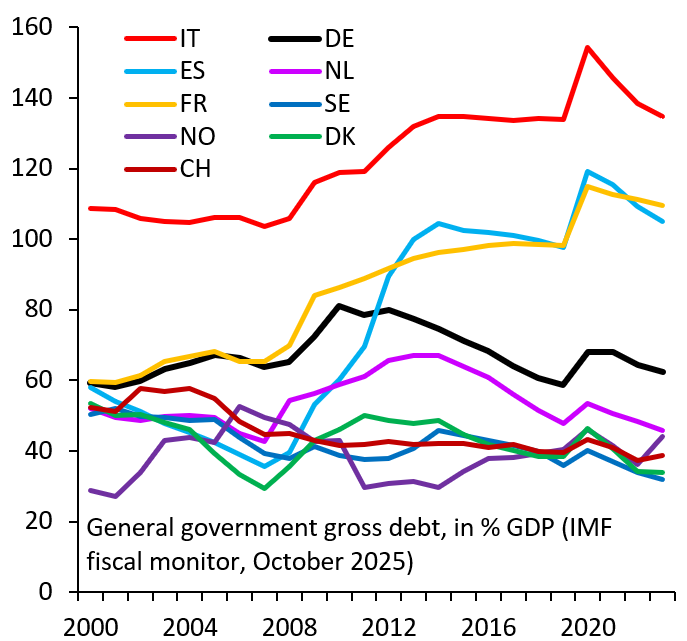

Come on Robin… the 10 year BTP-Bund spread is at its lowest since 2010 and Italy in 2024 went back to a primary surplus (as it did for almost two decades consistently, before COVID). Don’t cry wolf where there isn’t one, it’s irresponsible.

There's first signs of contagion from France to Italy and flight to safety into Bunds. Italy is the Euro zone Achilles heel. Without it, ECB could let French yields rise, helping France get its budget under control. But that's not possible with Italy always on the brink of crisis

Italy ran primary surpluses for almost 20 years continuously before COVID and returned to a primary surplus in 2024. Last time France ran one was in 2006.

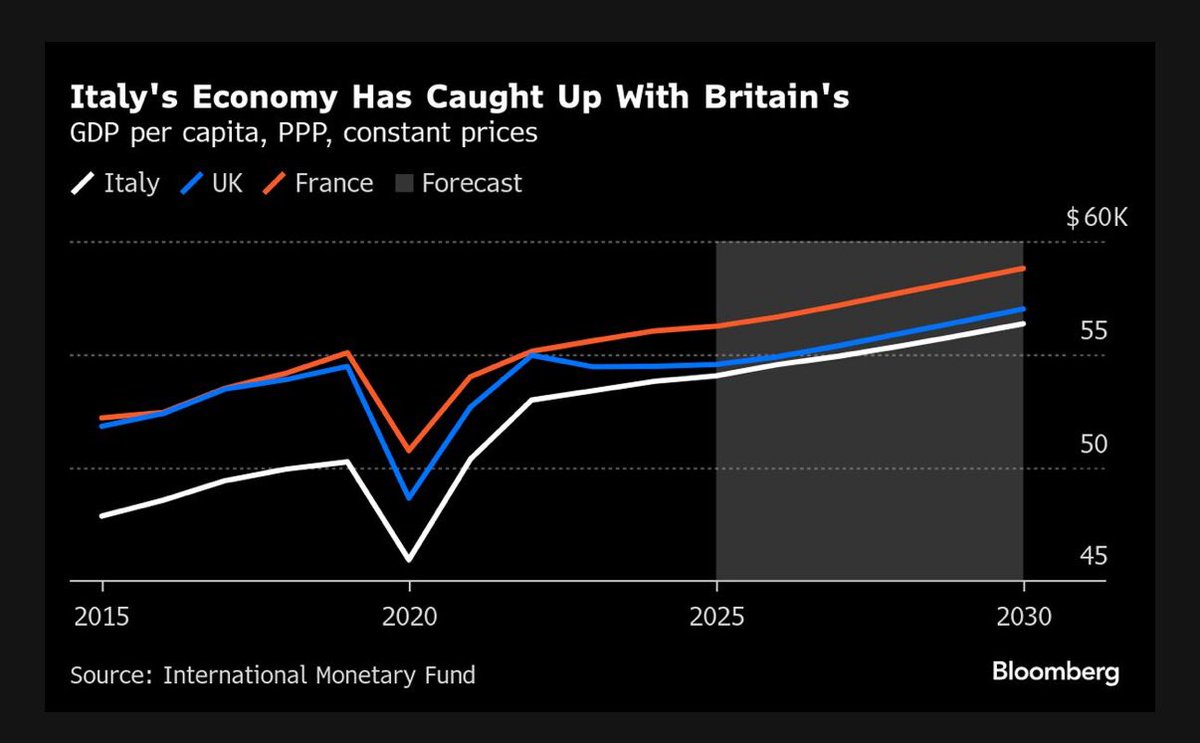

And this despite the Pound devaluing by 15-20% against the Euro since Brexit. Evidence that the Italian stagnation was not the fault of the single currency, as the nostalgic of competitive devaluations liked to argue in the aftermath of the Eurozone crisis.

Per Bloomberg:

“Italy, long a symbol of European economic stagnation, has almost completely closed a gap with the UK that was around $4,000 per head just before the 2016 Brexit vote, International Monetary Fund data based on purchasing power parities show.

Back then, the UK was also roughly level with France. Now, with a per capita output of $54,556, Britain is estimated to be just $500 ahead of Italy and almost $1,700 behind France.”

#economy #uk #france #italy

Bruegel is republishing the classics and I’m super proud that this paper by @pisaniferry and myself made the cut. It took a lot of work on then-obscure central bank liquidity data, but it changed the way we look at capital flows within monetary unions.

https://t.co/F8aKBMAsHl

Thank you to Jon Hay for featuring my comments in this extensive article on the UK’s decision to scrap plans for a Green Taxonomy. Great insights also from the other people quoted in the piece!

https://t.co/ytWSu9wuth

🪖 Can #defence#investment be sustainable? The European Commission thinks so.

My latest, looking into the Commission's recent efforts to incentivise greater defence investment.

https://t.co/gzKpv8myLn

Germany and Italy pressed to bring $245bn of gold home from US. A survey of more than 70 global central banks showed more were thinking of storing their gold domestically amid concerns about their ability to access their bullion in the event of a crisis.

https://t.co/9WiUkKEuUT

Great piece by @MESandbu in today’s FT. As I wrote back in April, the EU’s best response to Trump’s tariffs would be to issue more EU debt. My preference however is for ramping up genuine EU debt issuance, not settling for synthetic asset solutions.

https://t.co/N0Q4DRPhoP