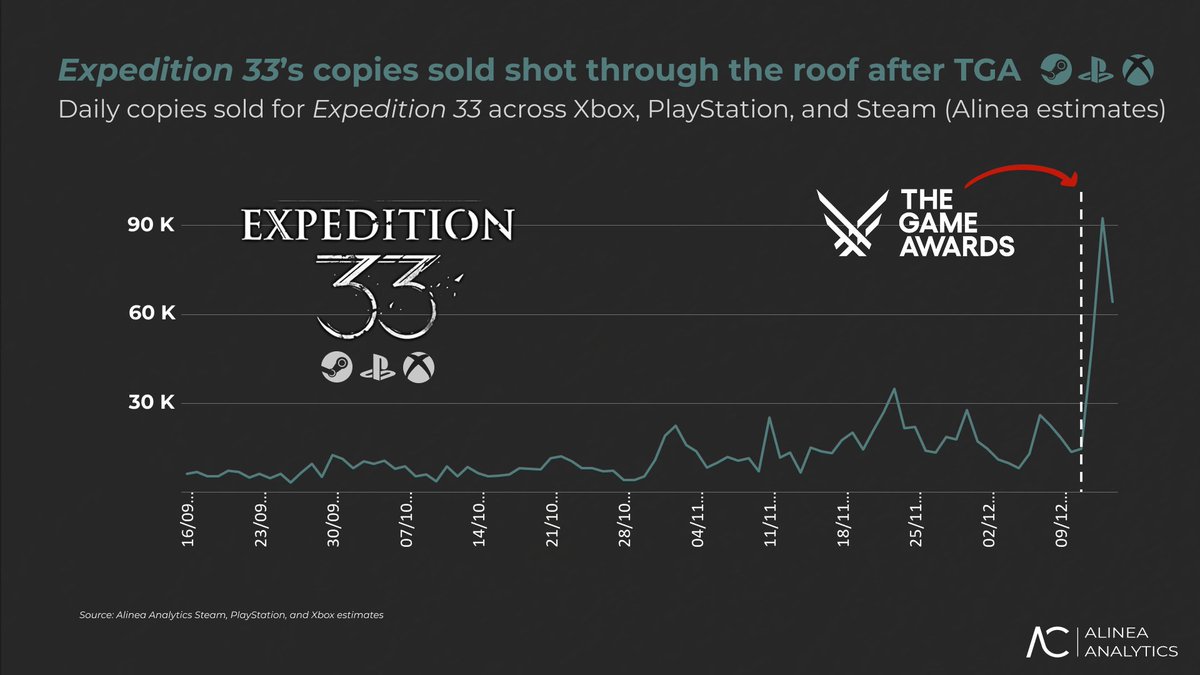

Damn! Huge spike in Expedition 33 copies sold since the Game Awards (@alineaanalytics estimates)

It sold an extra 200K+ copies since: 76% on Steam, 21% on PS5, and 3% on Xbox. Around 52K Xbox players accessed E33 via Game Pass for the first time, too.

Free Substack link in bio.

Steam is having another record year for revenue (@alineaanalytics estimates)

In the first half of 2026, games on Steam generated $11.1B in gross revenue, the platform’s highest-ever half-year. That’s up 14.5% on H1 2025, and up 8% even on the holiday-heavy H2 2025, which is remarkable given the back half of the year usually wins on seasonal sales and holiday buys.

Zoom out over the last decade and things get really crazy. There’s obviously a visible dip as the market normalised after the pandemic sugar-high, but the long arc is relentlessly up, with seven half-years of growth.

Some takeaways:

- H1 2026 is 4.7x larger than H1 2017, so Steam has roughly quintupled its half-year revenue in ten years.

- Steam’s full-year revenue has climbed from around $5.5B in 2017 to roughly $20B in 2025.

- Steam did more in the first six months of 2026 than in all of 2020, a year when the entire world was locked indoors and buying games to cope, and nearly matched 2021.

Another trend worth watching, though, is the one with chunky implications for anyone shipping a game, especially in AAA. There’s a shrinking share of revenue coming from new games (games releasing in a given year):

- H1 2024: 29% of revenue came from 2024 releases.

- H1 2025: 27% came from 2025 releases.

- H1 2026: just 21% has come from 2026 releases

In other words, back catalogue revenue has climbed from 71% to 79%. Obviously, release calendars matter here, but I’ve long covered the fact that publishers are getting savvier with their back catalogues (discounts, bundles, timed sales).

And the sheer volume of releases keeps accumulating. Every new game increasingly competes not with this year’s rivals but with a decade of proven hits available at a fraction of the price.

Adding fuel to the fire for AAA is the diminishing graphical returns (a 2021 game looks close enough to a 2026 one for most players) and the hardware crisis. So that pull toward the back catalogue only strengthens for these sorts of experiences.

When a new release has to compete with a decade of discounted classics, the money pools at the very top (a handful of viral hits, beloved sequels, and big franchises). Meanwhile, the long tail launches into a market that already has more great games than anyone has time to play.

While I’m a firm believer that truly great games will always find their audience, everyone is fighting the catalogue in one way or another. And that’s becoming a harder battle to win.

Deep dive in the new free Substack (link in bio).

Top new 2026 games by Steam revenue (@alineaanalytics estimates)

Forza Horizon 6 has ... driven revenues of $197.7M since launching under two months ago. It's the top new game of the year by Steam revenue. About $4M of that is DLC, including almost $2M from the VIP Membership (double event cash and other perks). Launch-aligned, Forza Horizon 6 is pulling revenue three times faster than 2021’s Forza Horizon 5 did. Horizon 6 is at 3.5M copies sold on Steam now.

Resident Evil Requiem has done $194.5M and 3.4M copies for Capcom on Steam, including $1.3M from the purely cosmetic Deluxe Kit DLC. In total, Requiem has converted just 8.9% of its pre-launch wishlisters so far, which sounds low but signals a long revenue tail, exactly as Resi titles tend to behave on Steam. The slow-burn conversion is the point here, not at all a weakness.

Crimson Desert is JUST behind Requiem at a little over $190M since its March launch. It’s the standout here because it’s a brand-new IP. But it made about $9.2M last month, so those full-price $70 buys are drying up. If I were Pearl Abyss, I’d get a 20%-off promotion running NOW before the autumn (that's fall for my🦅 friends) release onslaught. Requiem took its first 20% discount last month and held revenue essentially flat between May and June as a result, an example of a well-timed discount offsetting this kind of revenue decay.

Slay the Spire 2 is a volume monster. Four months into early access, it’s sold 7.1M copies, more than Forza and Resi combined. But at a $25 price point (and regional equivalents) it sits fourth by revenue with $141.7M. That’s a frankly absurd figure for an indie in early access, and you love to see it. Remarkably, 40% of its pre-launch wishlisters have already converted to buyers, 31% in the first week alone! It launched as a polished, near-content-complete sequel to a beloved game and at a low price, so its wishlist was stacked with players who already knew they wanted in.

Subnautica 2 has pulled in $133.6M so far, roughly $120M of it in May, its early access launch month. The superfans who couldn’t wait for 1.0 have largely already ... dived in. Content was thin at launch (if still great), so we expect a bigger wave of its 5.6M wishlisters converting once it hits 1.0. So far only about 12% have converted vs Slay the Spire 2’s 40%, which is what makes Slay the exception for early access, not the rule.

Meccha Chameleon is continuing to climb, with $71.3M despite a $6 price tag, and 2026’s single top game on Steam by copies sold. It’s had its viral moment, and sales are starting to taper a bit, but it still pulled almost $1M this week, so the two-person team is doubtless still chuffed. A $6 game outselling everything by units while a $70 one tops the revenue chart is the whole modern Steam market in one snapshot.

More in this week's free newsletter!

Steam is having another record year for revenue (@alineaanalytics estimates)

In the first half of 2026, games on Steam generated $11.1B in gross revenue, the platform’s highest-ever half-year. That’s up 14.5% on H1 2025, and up 8% even on the holiday-heavy H2 2025, which is remarkable given the back half of the year usually wins on seasonal sales and holiday buys.

Zoom out over the last decade and things get really crazy. There’s obviously a visible dip as the market normalised after the pandemic sugar-high, but the long arc is relentlessly up, with seven half-years of growth.

Some takeaways:

- H1 2026 is 4.7x larger than H1 2017, so Steam has roughly quintupled its half-year revenue in ten years.

- Steam’s full-year revenue has climbed from around $5.5B in 2017 to roughly $20B in 2025.

- Steam did more in the first six months of 2026 than in all of 2020, a year when the entire world was locked indoors and buying games to cope, and nearly matched 2021.

Another trend worth watching, though, is the one with chunky implications for anyone shipping a game, especially in AAA. There’s a shrinking share of revenue coming from new games (games releasing in a given year):

- H1 2024: 29% of revenue came from 2024 releases.

- H1 2025: 27% came from 2025 releases.

- H1 2026: just 21% has come from 2026 releases

In other words, back catalogue revenue has climbed from 71% to 79%. Obviously, release calendars matter here, but I’ve long covered the fact that publishers are getting savvier with their back catalogues (discounts, bundles, timed sales).

And the sheer volume of releases keeps accumulating. Every new game increasingly competes not with this year’s rivals but with a decade of proven hits available at a fraction of the price.

Adding fuel to the fire for AAA is the diminishing graphical returns (a 2021 game looks close enough to a 2026 one for most players) and the hardware crisis. So that pull toward the back catalogue only strengthens for these sorts of experiences.

When a new release has to compete with a decade of discounted classics, the money pools at the very top (a handful of viral hits, beloved sequels, and big franchises). Meanwhile, the long tail launches into a market that already has more great games than anyone has time to play.

While I’m a firm believer that truly great games will always find their audience, everyone is fighting the catalogue in one way or another. And that’s becoming a harder battle to win.

Deep dive in the new free Substack (link in bio).

Launch sales projections for Ubisoft's Assassin's Creed Black Flag remake look like a huge improvement on Assassin's Creed Shadows, the franchise's most recent release. https://t.co/KUQuPtL16f

Assassin's Creed Black Flag Resynced is on course to be a much-needed hit for Ubisoft.

Resynced looks poised for a HEARTY PC showing, already clearing 300K copies sold on Steam ahead of launch, worth almost $14M in gross revenue (@alineaanalytics estimates)

It’s a ground-up remake of 2013’s Assassin’s Creed IV: Black Flag, still widely considered the peak of the franchise. And while Assassin’s Creed has been a console-first property, it’s been gaining some ground on Steam.

For context, Assassin’s Creed Shadows has sold 5.7M copies globally, splitting 53.6% PS5, 23.8% Steam, and 23.6% Xbox. Resynced has already outsold the entire Steam lifetime run of Ubisoft Singapore’s previous pirate venture, Skull & Bones, before it’s even out.

And our estimates have Black Flag Resynced tracking far above AC Shadows on Steam pre-launch, too. At the same two-days-out milestone, Resynced has sold 5.39x more Steam copies than Shadows did in its equivalent pre-release window. For reference, Shadows has since reached 1.3M lifetime copies on Steam.

From an industry lens, Black Flag Resynced is a timely strategy for a struggling Ubisoft. After a turbulent few years of costly development, delays, and high-profile misses (ironically including Skull & Bones, which spun out of Black Flag’s own naval tech), Ubisoft is dealing with fractured pipelines. Building an unproven new IP from scratch is a six-to-eight-year gamble costing hundreds of millions.

High-fidelity remakes of beloved legacy titles are the low-risk alternative – and one Ubi hasn’t really leveraged much yet. Such remakes reuse a universally praised design blueprint, lowering creative risk while guaranteeing a built-in audience.

For a publisher mid-transition, these remakes are a financial cushion, stabilising the balance sheet and winning back investor and consumer confidence while the long-term bets bake.

It’s similar to the catalogue logic we’ve tracked elsewhere, including with Capcom’s remake-fuelled so-called flywheel. Proven IP is the lowest-risk money in a risk-averse industry.

Because Black Flag carries so much nostalgia for the PS4-era crowd who remember it as a definitive day-one title, and the franchise's PlayStation-first audience in general, it'll perform even better on PlayStation, too.

This is something I’ve been referring to as the amortisation of nostalgia (sorry). In other words, remakes allow a publisher to extract fresh, high-margin revenue from IP whose brand and design were paid off a decade ago (the remake has its own, theoretically smaller new production cost, though).

Also, protagonist Edward Kenway is canonically from Swansea (like me!). Hell yeah.

More in the latest free Alinea Substack. Link in bio!

Dear gaming community,

Following the end of our external finance partnership on Project Fantasy, IOI has regained full ownership of the project and our IP. We will continue to develop and fund it independently amongst our other projects. With this context, we had to find a new balance for the long-term future of the studio, focused on the success of our main internal core titles instead of external projects and potential mobile game derivatives. This has meant making changes as well as proposed changes across our studios: the closure of our Istanbul studio and starting a process to part ways with colleagues who have been a meaningful part of what makes IOI what it is.

Our immediate focus is on supporting those affected as best we can through this period. If you are aware of any opportunities within your network, we would be genuinely grateful for any support you can offer to any of the talented people across IOI who might be looking for new opportunities.

These are hard, but necessary decisions, in order to retain the long-term future of IO Interactive as one of the very few fully independent AAA developer and publisher, as well as to give Project Fantasy the best possible foundation to succeed under our own passion and direction. Project Fantasy is a game, a world, and an IP that we are wholly committed to, and we cannot wait to share the love with you.

This time next week, I'll be en route to lovely Brighton to represent Alinea Analytics!

If you're also heading to @developconf, give me a shout! My DMs are open if you want to chat about games, the games market, data, what Alinea's been up to, or anything else games-related!

Especially looking to meet indies and folks at publishers, but - as always - I'm down to meet anyone with a passion for games.

Fair warning: I'll probably try to get you to play Mina the Hollower or Fields of Mistria, though!

#DevelopBrighton #DevelopConf

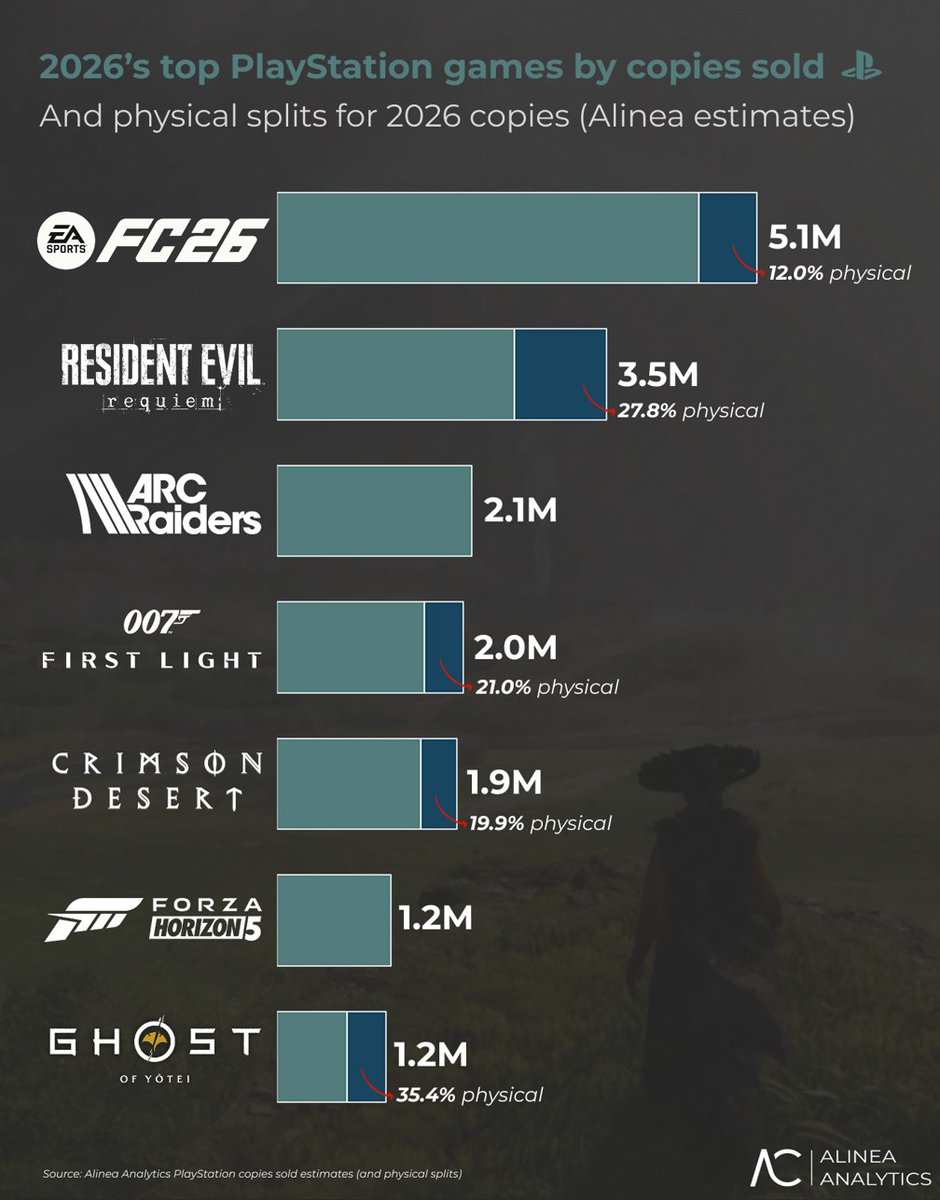

PlayStation's top games by copies sold in 2026, including some VERY topical physical game splits (@alineaanalytics estimates).

FC 26 is #1, in no small part thanks to the World Cup fever currently sweeping the globe (and the marketing around it). We won’t flog that dead horse again, so here’s a couple of new FC 26 estimates: 12% of FC 26’s PlayStation copies sold this year were physical, and 78% were PS5 copies (the rest PS4).

Resident Evil Requiem has sold 3.5M copies on PS5 alone, about 27.8% physical. Capcom, for its part, has been quite gleeful (and gleefully un-quiet) about how much back-catalogue revenue it’s making on PC. It calls this its “flywheel-driven business model.'' With its no-discs-in-2028 decision, Sony wants a bigger piece of that flywheel. Come Resident Evil 10, PlayStation and Capcom will be splitting those back-catalogue revenues between them.

Arc Raiders has sold 2.1M copies ($80M) on PS5 this year, bringing its PS5 total to 4.7M, all digital (no physical version). 1.6M of this year’s 2.1M came in the first three months (almost a million in January alone), when the game was still having its moment. Arc Raiders sold under 100K last month, even with its biggest PS5 discount to date ($30). So it’s all about keeping the existing players engaged now.

007 First Light has shifted (not stirred!) 2M copies on PS5, its biggest platform by players (almost 60%), in just over two months on the market. 007 has made about $142M on PS5, more than Steam and Xbox put together, and around 21% of copies are physical.

Crimson Desert, which launched on 19 March, has sold 1.9M copies on PS5, its secondary platform after Steam, with 19.9% of PS5 copies being physical. Over 1.5M of those PS5 copies sold across March and April. Last month Crimson Desert sold about 112K copies ($8M). To date, Crimson Desert has generated $140M gross on PS5. Units are dropping off, but that $70 price is holding firm. Time for a discount, I reckon.

Forza Horizon 5 just keeps selling on PS5, adding another 1.2M copies this year ($55M) since its PS5 port last May, for a PS5 total of 6.2M. It’s still doing 150K-250K a month. And while the Steam version (2021) has sold more copies (8.3M), regional pricing and discounting mean the PS5 version has already out-earned it via copies sold ($340M versus $314M on Steam). The sequel, Forza Horizon 6, has sold 3.4M on Steam ($192M). One can only imagine how much it’d have made on PS5 day-and-date. It'll sell gangbusters when it hits PS5 later this year, and Xbox will be watching those numbers VERY closely.

Ghost of Yotei (ah shi', here we go again) is holding strong following its October 2025 launch, adding another 1.2M copies ($80M in back-catalogue revenue) this year. Around 35.4% of those were physical, the highest share on this list, and – again – the kind of number PlayStation wants to curb for its first-party games from 2028. Monthly copies have been consistent all year, the mark of a game that just keeps selling, and it’s only had one discount, so most of this year’s copies sold at the full $70. A great sign for Yotei’s ongoing run, and another reason PlayStation wants to own the pricing.

More on the free Subtack (link's in my bio!)

2026's top games by copies sold across Steam, PlayStation, and Xbox (@alineaanalytics estimates).

Meccha Chameleon, the latest in a long line of friendslop hits, launched three weeks ago to enormous viral success and is already approaching 13M copies sold. Despite being Steam-only, it’s still 2026’s top game by copies sold across all three platforms combined. The catch is that copies don’t equal cash. Meccha Chameleon’s $58M-plus in gross revenue makes it the #18 game by Steam revenue this year, because of its $5 launch price (nudged to $6 as it went viral, a smart, quiet bit of price optimisation while demand was peaking).

FC 26 has scored over 9.1M copies this year across PlayStation, Steam, and Xbox. As covered last week, FC has enjoyed a lift from World Cup fever, discounts, subscription additions, and dedicated tournament modes. Over half of 2026’s copies came via PlayStation, and around 19% of those US sales, up from 12% in 2025. Football fandom finally looks to be hitting fever pitch (ayy) in the States, so FC 27’s launch later this year should post the franchise’s best-ever US numbers, one to watch.

Resident Evil Requiem keeps rolling, at 7.6M copies sold across the three, split roughly 46% PS5, 45% Steam, and 9% Xbox. It’s about to cross half a billion in gross revenue across the three, with around $250M on PS5, $200M on Steam (that lower per-copy take reflecting its big share of buyers in cheaper-priced regions), and almost $50M on Xbox. It shifted nearly 400K copies last month alone ($20M). Resi is another one that keeps on selling. And it’ll continue to do so with discounts, becoming another part of Capcom’s formidable catalogue revenue for years to come.

Forza Horizon 6 just misses a podium spot, with 7.4M sold, 4M on Xbox (console, Windows, and Game Pass players who bought the $59.99 Premium Upgrade Bundle) and 3.4M on Steam. It added another 1.4M across the two last months, so it’s well on track (ayy) to hit 10M this quarter. The planned PS5 port should easily push the yearly total past 15M, given how well Forza Horizon 5 did on PS5 (6.2M in 14 months, but the novelty factor might’ve worn off a bit). Outside CoD and Minecraft, Forza Horizon is now comfortably Xbox’s biggest IP, I reckon.

ARC Raiders has slipped out of the core-gamer conversation but keeps shifting copies at a nice clip, another 7.4M this year. A little under half of those came in January, still riding the launch wave. Monthly sales have expectedly cooled a bit (around 250K last month). MAUs are also down from January’s 10.7M peak to 3.7M, but that settling is what a healthy live-service game looks like nine months post-launch (what is time!?). ARC Raiders has done the hard thing, converting a viral launch into a durable, seasonal-update evergreen with a MAU base most publishers would envy.

Lastly, Slay the Spire 2 has slayed 7M copies this year in early access on one platform, generating $140M. Despite a $25 US price, its biggest market by players is actually China (35% of players versus 31% in the US). Slay the Spire 2’s sales curve is heavily front-loaded, with 5.3M of its copies selling in March, launch month. So it’s added roughly 1.7M since (including 270K last month). Slay the Spire 2 is in early access, so there haven’t been any discounts yet, and it’s sitting on 2M wishlists.

More data and insights in the new free Substack (link's in my bio)

CrossCode is SO good, and especially a must-play for any 16-bit RPG fans. It was one of my favourite games of 2018.

Pumped to play through again on PS5.

@JNavok@alineaanalytics Sure, but that's what everybody calls the subgenre at this point, including the audience and some devs themselves.

Just one of those things, I reckon. I was annoyed at it at first as well, but I've just accepted it at this point.