$PSC Country Manager Mwelwa Manda sat down with @FinInsightZam to discuss our recently upgraded Mineral Resource Estimate at the Mumbezhi #Copper Project in Zambia. Watch the full interview here: https://t.co/mtoOWSqKqz

$PSC MD & CEO @SamHosack recently spoke with Financial Insight Africa at Mining Indaba 2026 on Zambia’s copper sector, local workforce development, community engagement and the long-term opportunity at the Mumbezhi Copper Project. Read more: https://t.co/2OVu170VRs

$PSC Country Manager Mwelwa Manda spoke with Clarence Chongo from Financial Insights Zambia on the recently upgraded Mumbezhi Copper Project MRE (208Mt @ 0.49% CuEq). Watch the short snippet below.

$PSC MD & CEO @SamHosack provides video commentary on our upgraded Mumbezhi Copper Project MRE in Zambia, now 208Mt @ 0.49% CuEq, and the start of Phase 3 drilling. Thank you to our shareholders for your ongoing support as we advance Mumbezhi: https://t.co/ySXWBotPag

$PSC MD & CEO @SamHosack provides video commentary on our upgraded Mumbezhi Copper Project MRE in Zambia, now 208Mt @ 0.49% CuEq, and the start of Phase 3 drilling. Thank you to our shareholders for your ongoing support as we advance Mumbezhi: https://t.co/ySXWBotPag

The scale of the Mumbezhi Copper Project is accelerating. Contained copper is nearing 900 kt and gold now totals 262,000 oz, with all three deposits showing clear growth potential. Combined with this year’s regional drilling, the broader opportunity at Mumbezhi is becoming increasingly compelling.

Gold re‑assaying has significantly lifted the Nyungu Central MRE, confirming that gold and cobalt by‑product revenues can materially lower future operating costs. We expect to define this further over the next 6–12 months.

Our Phase 3 (2026) drilling has begun, targeting shallow southern extensions at Nyungu Central before testing the wider Nyungu Hub and high‑priority regional targets. These include the large Chipimpa and Sharamba EM conductors—each over 2 km in strike and showing signatures comparable to Nyungu Central.

Updated MRE at the Mumbezhi Copper Project has increased to 208.1Mt @ 0.42% Cu (0.49% CuEq) for 877kt contained copper, with gold resources up 106% to 262,100oz. Phase 3 drilling is now underway targeting further growth across the project: https://t.co/vBjkG6AIWY

$PSC

📈 Strong demand from global electrification, alongside a stockpile rush caused by reduced supply and geopolitical uncertainty, pushed #copper prices to an all-time high of $6.44/lb over the past 24 hours.

Supply shocks, like stockpiling, are exacerbating the need for new copper sources, like the Vizcachitas Project, to come online.

Read more here ⬇️https://t.co/UjSs89by8F

Copper is approaching record highs as rebounding Chinese demand collides with tightening global supply conditions.

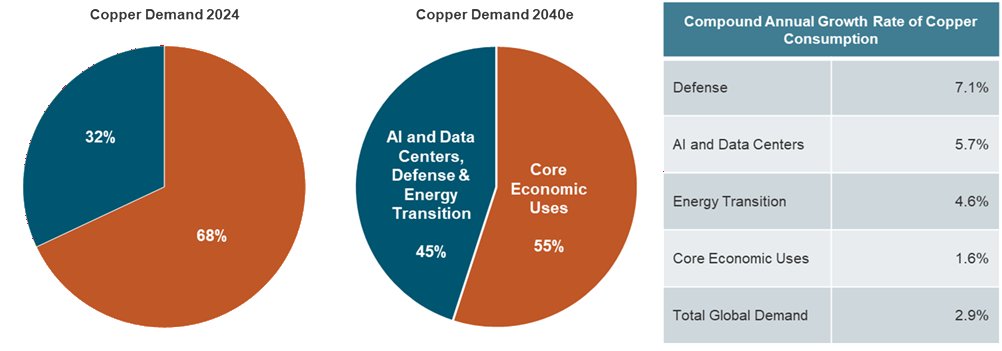

As prices recently breached the $14,000/t mark, electrification is becoming an increasingly important driver of demand. Data centers and other strategic uses are projected to reach 45% of total copper demand by 2040.

▪️The Supply Shock: Middle East disruptions have triggered a global sulfuric acid shortage — a key input for roughly 20% of copper production. With acid prices nearly doubling and inventories in China falling, production costs are being reset in real-time.

▪️The Strategic Shift: Electrification is now the fastest-growing end-use, shifting demand away from cyclical construction toward long-term energy security and power systems.

▪️The Sprott Outlook: Analysts highlight that these strategic segments are set to jump from 32% to 45% of total copper demand over the next 15 years, significantly outpacing traditional industrial growth.

BREAKING: Copper prices have surged to a record $6.58 per pound, now up +75% since October 2023 and over +40% in 12 months.

The surge comes amid tight supply, declining inventories in China, and surging demand for data center construction.

Furthermore, supply disruptions at the world's 2nd-largest copper mine in Indonesia are adding to the pressure.

Meanwhile, China's exports jumped +14% YoY in April, led by booming clean-tech shipments, components that are materially copper-intensive, tightening the market even further.

The global economy is scrambling for copper.

I haven't been this excited about a drill season for a long while. The team on the ground at Mumbezhi are geared and primed for an ambitious and well planned 2026. Keep an eye on progress.

Phase 3 drilling has commenced at the Mumbezhi Copper Project in Zambia, with ~26,000m of diamond, RC and aircore drilling planned to target further resource growth at Nyungu Central and key regional prospects: https://t.co/3D5z5nVR1B

$PSC

Another strong quarter from your PSC team, we have significant funding for 2026 and a very attractive program to deliver. MRE update in a couple weeks, and drilling starting around the same time. Fantastic platform to launch 2026 from.

$PSC reports a strong March quarter, with contained copper at Mumbezhi increasing 50% to ~772kt, growing polymetallic upside and ownership rising to 90%. Well funded to accelerate drilling, resource growth and development through 2026: https://t.co/8Pbw1uCruf

Whilst there are no published academic studies that formally document systematic poly-metallic discounting of copper equities, in reality market evidence suggests that one exists.

The observation is that when by-product metals lack confirmed recovery data, market analysts face a binary choice: Model them at risk-adjusted value; or Ignore them. The reality is that most choose to ignore them.

The result is that by-product upside on projects like Mumbezhi is excluded from valuation models until testwork forces inclusion. The discount is not irrational … it is a rational response to unconfirmed data. But it creates a persistent and exploitable gap between intrinsic value and market price.

CRU formally acknowledged in its 2020 report for the International Seabed Authority that "determining a fair value for polymetallic resources is highly challenging." A 2025 Nature Communications paper demonstrated that traditional models systematically undervalue poly-metallic mine outputs, with by-product economics creating non-linear interdependencies that single-metal valuation frameworks fail to capture.

The data from M&A transactions supports this too – here’s what major producers actually paid:

- BHP paid a 49.3% premium for OZ Minerals' copper-gold-nickel assets.

- Zijin paid 57% above market for Nevsun's Timok copper-gold project.

- BHP and Lundin paid a 32.2% premium to acquire Filo del Sol's copper-gold-silver resource in 2024.

In every large copper transaction since 2010, the highest premiums went to assets with material by-product credits. Acquirers price poly-metallic inventories at full value, whereas public markets discount them until testwork resolves the uncertainty.

The re-rating catalysts are identifiable and sequenced:

- Maiden resource delivery: 30-60% valuation appreciation observed across comparable projects.

- Economic study completion incorporating by-product economics: 40-100% re-rating as projects transition from geological potential to quantified economics.

These are documented patterns across the exploration and development lifecycle.

The window is the period between by-product identification and by-product confirmation for @ProspectResLtd. That is where the gap between market price and intrinsic value is largest.

PSC.ASX Gold re‑assays at Nyungu Central show wider, continuous mineralisation across the Nyungu system, including the northern zones. Supports a stronger MRE and potential operating‑cost benefits. Updated MRE incoming; Phase 3 drilling on track for early May.

Gold re-assays at Nyungu Central confirm widespread gold mineralisation,with intersections in 29 of 32 holes. Results support strong by-product potential (with cobalt) alongside copper.Further assays due this month; MRE update in Q2: https://t.co/dwgLhA1iC6

Capital intensity – why African Copperbelt projects occupy a different universe: The global copper development pipeline has a capital intensity problem that most market commentary underweights.

S&P Global's December 2025 analysis of 26 upcoming copper projects starting by 2030 found a weighted-average capital intensity of $22,359 per annual tonne of copper production:

-Los Azules in Argentina: $20,200/t

-Reko Diq in Pakistan: $23,000–25,000/t

-Others as high as $38,285/t - built, closed … a monument to the upper bound of what capital intensity can look like when jurisdiction, altitude, and process complexity compound.

African Copperbelt sediment-hosted projects are not in this conversation:

-Kamoa-Kakula across all phases: $10,177/t

-Čukaru Peki Upper Zone in Serbia, the highest-grade copper discovery in decades: $5,200–7,500/t

-Khoemacau expansion in Botswana: $6,923/t.

BHP stated explicitly in September 2024 that African greenfield projects deliver "highly competitive capital intensities" – driven by high grades, concentrated mineralisation, and improving infrastructure. 8 of the 10 highest-grade copper deposits discovered since 1990 are in Africa, predominantly sediment-hosted systems.

The implication for project valuation is significant. Capital intensity determines whether a project can be financed. It determines the copper price required to justify development. It determines where the project sits on the global cost curve in perpetuity.

@ProspectResLtd in the Zambian Copperbelt, with sulphide mineralisation, grid power access via established transmission infrastructure, proximity to existing processing capacity, and proven metallurgy such as Mumbezhi Copper Project, does not belong in the same valuation framework as a high-altitude Andean porphyry requiring bespoke water logistics, heap leach chemistry, and a decade of permitting.

The market is slow to price this distinction at the exploration and pre-feasibility stage.

By the time a scoping study quantifies it, a meaningful portion of the re-rating has already occurred.

$5bn Lobito Corridor rail = game changer.

Zambia copper → Atlantic coast via Angola.

Shorter route. Lower costs. Strategic shift in global supply chains.

This is infrastructure + geopolitics + critical minerals all in one.

#africa#copper#mining

https://t.co/T8qSV6aupd

The real cost of adding gold and cobalt circuits: Most investors treat poly-metallic complexity as a binary - either the by-products are recoverable, or the processing is too complex to model with confidence. The engineering data tells a different story.

Adding a gravity gold circuit to a conventional copper sulphide flotation plant costs between $2 million and $10 million at typical development scale. That is 1–1.5% of total plant capex. It recovers free gold directly to doré, achieving 99% payability versus 85–93% if gold is left in copper concentrate. At $3,000/oz gold, that payability gap is worth $150–435 per ounce … every ounce, every year, for the life of the mine.

The cobalt data point is equally specific. Glencore's Kamoto Copper Company in the DRC publicly approved a cobalt debottlenecking project at $15.8 million in December 2017 … 3.6% of their $437 million base processing plant. Full cobalt product dryers added a further $49 million. These are formally published board-approved figures, not estimates.

The conclusion is direct. For a copper-gold-cobalt sulphide project, like our @ProspectResLtd Mumbezhi project, the capital required to unlock full by-product value is modest … in the range of 3–15% of total plant capex depending on product specification. Against a by-product revenue stream that can compress C1 cash costs by tens of millions of dollars annually, the return on that incremental investment is among the highest in mining.

What the market prices as processing complexity is, in most cases, a recoveries confirmation problem … not an engineering one. The circuits are standard. The reagents are proven. The cost is known.

The gap closes when metallurgical testwork publishes the recovery numbers. That is the relevant catalyst … not a change in the engineering, but a change in the market's willingness to price what the engineering already shows is achievable.

$PSC reported final Phase 2 drilling assays from the West Mwombezhi prospect, confirming near-surface copper sulphide mineralisation over 1km of strike. Results incl. 8.9m @ 0.78% Cu from 54.6m (incl. 7.0m @ 0.93% Cu), with maiden MRE targeted for Q2 2026: https://t.co/8HXz9UEovP

In a well-engineered poly-metallic system, gold and cobalt credits do not simply sit alongside the copper economics. They are structurally embedded within them - functioning as a floor on the C1 cash cost and determining where the project sits on the global production cost curve.

First and second quartile producers remain cash-generative when copper prices fall. Third quartile producers do not. The financing institutions, streaming counterparties, and strategic acquirers who determine whether a project gets built make that distinction explicitly - and by-product credits are a primary input into their calculation.

A project carrying a meaningful gold and cobalt inventory is not a copper project with upside. It is a fundamentally different economic proposition.

The work that matters right now for @ProspectResLtd on the Mumbezhi Copper Project - establishing gold recovery rates, characterising payability across new mineralised zones, building the by-product case with rigour before the Scoping Study - is not overhead on the path to a feasibility study. It is the work that determines cost curve position, which determines whether institutional financing is available, which determines whether the project gets built.

Most of the market will price that when the test work is published. The window before that happens is the relevant one.

Where we’ll ultimately sit on the curve remains to be seen. In any case, our by-product credits will be key to our margin architecture.

$PSC acquired an additional 5% of the Mumbezhi Copper Project for US$4.25M, increasing ownership to 90%. Phase 3 drilling is expected from early Q2 2026, with the expansive program targeting resource growth, regional copper targets & cobalt-gold upside: https://t.co/vsbLEzPCZH