Really happy to have gotten this opportunity to present my framework with the SOIC tribe.. will hopefully add value to the community 🙂

Thanks team @soicfinance for trusting me with this!

A must read case study for any special situations enthusiast👇🧵

Tanfac Industries has become the talk of the town partly led by their big capex plan of 400-500 Crs on a 100 Crs gross block or the fact that marquee investors participated in their recently concluded open offer..

However, after recent reduction in the pref fund raise size (with many speculating anupam rasayan’s possible intentions behind reducing their commitment to the fund infusion),

This is now emerging as very interesting case study of interpretation of SEBI (Sast) regulations~

First lets understand the SEBI regulations on takeover-

As per law, 1)any promoter having 26%+stake can ⬆️his stake upto 5% without triggering a compulsory open offer but

2) Any shareholder owning less than “25”% shareholding in a company will see a compuslory open offer triggered if the stake rises beyond 25%

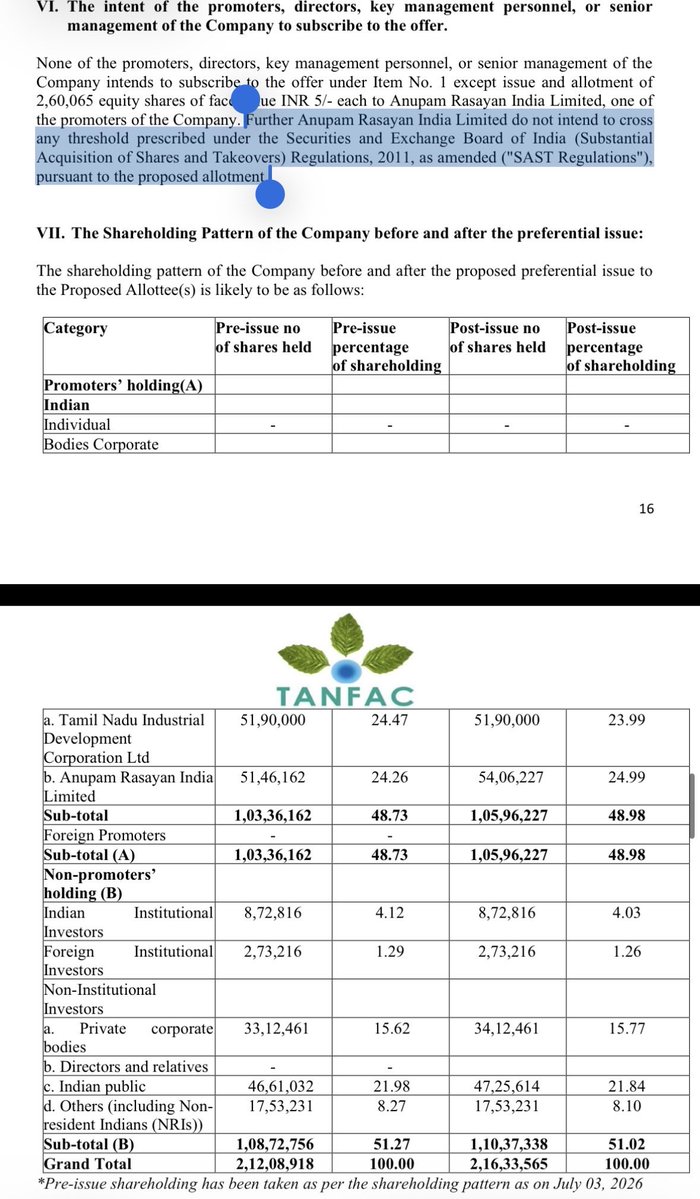

In the current case, below is the chain of events~

A) Tanfac Industries raised 250 Crs via QIP~ leading to dilution in shareholding of existing promoters- Anupam rasayan & TIDCO (who earlier held almost 26% stake each) to below 25% (around 24.5% now)

B) Followup preferential allotment fund raise where Anupam rasayan was supposed to infuse 135 Crs which would have led to shareholding rising beyond 25% (26.07%) leading to trigger of a compulsory open offer “in most cases”

Except here comes a liberal/lenient interpretation of the statute which states that any dilution due to a fund raise (Vs transfer of shares) can be disregarded for the calculation of the base limit (25%)

Simply put, if we take lenient interpretation of the statute, Anupam should ideally not face brunt of the compulsory open offer

But 2 key questions that must brew in~

A) Why did Anupam then possibly reduce the fund infusion sum by 75 Crs, (afterall, lenient interpretation suggests that an open offer won’t get triggered?

Ans- First it’s important to understand what happens when a compulsory open offer is triggered-

One has to hire a banker to give an open offer tender, the company has to put a certain sum in an escrow account of atleast 26% of the overall shares (i.e. 26% of total shares * open offer price) in an escrow account until open offer is not completed

If supposedly, exchange didn’t take a lenient interpretation & triggered an open offer, then Anupam rasayan would have to arrange atleast 1000 Crs (based on current pricing) to be put into an Escrow account & possibly affect several other clauses in their JV agreement with TIDCO (afterall TIDCO will get diluted further & promoter itself can gain complete control)

B) Why didnt anupam simply do a pref allotment 1st & later do QIP?

Afterall, if one’s shareholding is above 25%, then they can do creeping acquisition of upto 5%, & post the QIP led dilution, they could have still maintained 26% ownership?

Honest Answer- I think they butchered this up.. One can put blame on promoters or their Legal team or even their banker responsible for the fund raise..

But this sounds more of a technical error Vs lack of conviction on the company’s business prospect be it for the new R32 project or anything beyond that.

With that being said, while this is a small setback in terms of arranging funds (afterall they did have willing investors who wanted to participate in the pref as per my scuttlebut but couldnt get allocation), but until then, they seem to have enough comfort on the B/S front to take debt for the 75 Crs sum (unless promoter later does some share transfer without triggering any open offer & then proceeds to issue equity shares)

In meantime, this is an amazing live case study on SEBI (Sast) regulations that can trigger a seemingly normal fund raise into a potential open offer takeover 🙂

(discl- Have holding, No reco), idea was to discuss this as a case study on open offer related laws Vs a company specific view!

Talked to a BHEL engineer about the Chinese power equipment tender news.

His response: "WE ARE BOOKED FOR NEXT 10 YEARS."

Yet Hitachi Energy, Siemens Energy, GE Vernova, BHEL, T&R, CG Power — all fell 5-9% in one session.

Here's why fundamentals and stock price can diverge

These stocks didn't rerate from 20 PE to 80-100+ PE because of order books alone.

SENTIMENT did the heavy lifting. "China can never compete here again" was the story markets paid up for.

That story just got a crack. Four Chinese-linked entities now cleared to bid.

Even if the actual order impact is small, SENTIMENT — the very thing that inflated the multiple — is what's now under question.

We've seen this movie before: Solar sector.

Real growth story. Real government push. Also real PE derating that wiped out latecomers who bought the narrative at the top.

Moral: "Booked for 10 years" is a business statement.

It is not a valuation statement.

When PE expansion is driven by sentiment, PE compression can also be driven by sentiment — regardless of the order book.

Entry price still decides your outcome.

Disclosure: Still evaluating the extent of the impact before drawing firm conclusions. This requires more clarity on tender volumes, competitive response, and margin impact over FY27-29.

Caution: Any fresh allocation in this space, if considered, will be strictly valuation-driven — no compromise on entry price regardless of narrative strength.

we've been reading a lot about advanced packaging (thanks to citrini year's start blog) and how we can play it via Indian players.

we are pretty much stuck at OSAT on ground level given we have been a little* behind in terms of getting those capablities (a little😅)

posting on substack today about the space - what are our thoughts and more from purely understanding the industry and space POV - and where each player sits.

nvidia recently dropped a paper that's been doing the rounds - all about something called 800 vdc (we'll get to what it is). inside there is list of 29 companies it's partnering with to actually build it - indian names on that list? common you know it!

meanwhile the copper bros have spent the last year yelling ai = copper, copper is the new oil, copper to the moon. 800 vdc says hang on! and the funny part is - copper does not give a single fuck about ai data centres. that whole demand story is a rounding error

quick context on what 800 VDC is - an AI rack today uses more power than a small building - you physically cannot push that much through the old low-voltage AC wiring without wrapping the whole rack in copper (not literally). so nvidia said - what if we just cranked the rack up to 800 volts DC?. higher voltage, lower current, and suddenly you need a fraction of the copper, half the conversion boxes, and a bunch of tiny silicon carbide chips doing the job clunky transformers and fat copper busbars used to - every company on that list makes one of those chips or boxes.

the real value here - the chips, the converters, the solid-state transformers - none of it gets made in india at any real scale.

so we did the boring thing and followed the copper instead - the spend nvidia is deleting inside the rack doesn't goes away comepelty - it just walks one step upstream - onto the grid that has to feed these data centres. hvdc links, extra high voltage cable, bushings, reactors, storage. and that, finally, is stuff india actually builds. Qpower in reactors and insulators, yash highvoltage in bushings, KEI tooling up for india's first hvdc cable line, plus the listed indian arms of the grid names that did make nvidia's cut. even cummins and KOEL are fine - they sit on the backup layer and could not care less what voltage the rack runs at.

now the interesting part is - a big chunk of the street is long this whole theme through copper and plain vanilla transformers, and funny part is 800 vdc is engineered to use less of both. check out Ambit’s note on schneider – it also says that just lifting the distribution voltage cuts the copper and cable you need by 8-10x for the same load (just take a moment to comprehend this). some sell sides data-centre copper forecast peaks in 2028 and then rolls over. But the most funny part is - data centres are barely 1% of data centre demand globally as of now, and it will not move more than 3% by even FY31.

(before someone replies with the copper chart - yes copper's up ~40%. But talk to some of these copper recycler and they will tell you that's tariffs and stockpiling - not data-centre demand. Infact the market literally ran a surplus last year and the price still ripped)

what it boils down to? if you wanna play this theme - the winners of 800 vdc aren't aren't in india - india's real place is one layer up - on the grid, where the deleted copper gets reborn as something higher up the chain. and one or two names everyone already owns are quietly long the exact assumption this architecture was built to break.

everyone got long copper when the racks demand jumped - but being long copper depending on data centres which are built to delete copper feels strange, so we're rather bullish on the grid side of things.

Special situation plays coming this decade.

Many next-generation promoters are losing interest in running traditional family businesses due to differing ambitions, while others face succession challenges. These companies could become attractive targets for takeovers. Keep an eye on foreign giants or strong Indian promoters acquiring quality Indian assets. Such moves often bring better management control, sharper focus, and a clearer growth path.

Open Offer Examples:

1) Kubota acquired Escorts.

2) Anupam Rasayan acquired Bliss GVS Pharma.

3) Mahindra acquired SML Isuzu.

Successful Takeovers by Intelligent Capital Allocators:

1) Safari – Sudhir Jatia

2) APL Apollo's Sanjay Gupta (well known name)

3) Murugappa Group (well-known for value-accretive acquisitions)

Many legacy family-owned businesses with strong networks, capital, and experience are restructuring operations to achieve focused growth, often resulting in significant value creation.

Business Restructuring Examples:

1) Kirloskar Group.

2) RPSG Group.

3) TVS Group.

Many legacy leaders continue to trade at premium valuations despite stagnant growth. These companies are increasingly demerging high-growth verticals from their stable or struggling businesses. This creates leaner balance sheets and allows focused management to drive each segment. Investors can then choose the business vertical that best aligns with their preferences.

Notable Demergers Examples:

1) Astral (recently announced)

2) Vedanta

3) Raymond

A new trend is emerging where reputed business houses or family offices identify and back talented management teams in sunrise sectors. This model combines strong promoters, business networks and mentorship from family offices, and patient capital - often leading to high-growth outcomes. These opportunities carry significant risk but have delivered favourable results in several cases. Participation for retail investors remains rare, as most activity occurs in the unlisted space.

Keep a close watch on such special situations.

gaudiam and indra have been talk of town given only pure play IVF IPO. we'd rather own the molecule every cycle burns.

these are the first pure-play fertility IPO – we got pitch from banker saying "USD 800mn to 5bn by 2033," sub-5% penetrated, the #1 chain. and the from lifestyle pov it makes sense - late marriage, sperm counts WHO keeps revising down.

we just think everyone's looking at the wrong slice of it.

the clinic is the most contested, thinnest-moat node in the entire chain - 25 organised chains now where there were 5 just few years back. CAC running ₹15,000-45,000 and climbing every qtr - metros are saturated - even rainbow which own IVF, told its own analysts the referral channel is dead: "B2B remains very negligible because obstetricians often see us as competitors, so they hesitate to refer their infertility patients to Rainbow." the dedicated IVF sales teamdid not work.

so we stopped arguing about the IPO and mapped the whole chain – 5 layers, who sits where, and the only question that matters for a us as investor - which node has the moat, and which one can you actually buy. it's not the clinic.

layer 1 - the clinics (most noise, least moat)

great economics in isolation (₹3.5-5 crs a center, 50-70% gross margins, 100% cash because fertility isn't insured), which is why PE rushed in - the players: indira (#1, BPEA EQT, IPO-bound), nova (AHH/TPG), birla (CK Birla), apollo fertility, oasis, ferty9, cloudnine. listed is basically just rainbow (Mother & Child + IVF) and apollo (diversified), plus gaudium (SME). the pure-play arrives only with indira - at peak narrative, so it's a price-discipline game.

layer 2 - the hormones (the pick-and-shovel, and the actual moat) ⭐

every time a woman does one round of IVF, she has to take a course of fertility hormone injections. that's a fixed ₹15-30k of drugs per attempt - every patient, every clinic, no way around it - so forget which clinic wins the price war. the company that makes those hormones gets paid every single time anyone does IVF, anywhere. they sell the shovels while the clinics fight over the gold. it's an oligopoly, 55-65% gross margins, and a biosimilar tailwind (penetration went 50%→75% in three years, handing share to the indian makers). and you can own it four ways, at four sizes - this table is the whole post:

Mankind via BSV(bharat serum acquired): Foligraf (recombinant FSH) +52%, HMG +40%, dydrogesterone +20%. the kicker management said out loud: "we now cover 90% of the IVF centers, more than 3,000 centers." plus Anti-D, a 100%-share recombinant monopoly (>₹200 cr brand, only ~5% penetrated) and #1 rank in gynaecology nationally. IVF is a small but fastest-growing sliver segment

Corona Remedies - the women's-health compounder. WH is its #1 therapy (~₹488 cr, ~33% of revenue, growing 20%, #5 in IPM). FY26 ₹1,403 cr (+17%), 21% EBITDA, ₹199 cr adjusted PAT. the infertility piece is new optionality - the IVF taskforce was created only in Q4FY26, arrowhead brands Menodac (HMG) and Fostine R (recombinant FSH) - sitting on a genuinely differentiated backward-integrated hormone API plant (La Chandra). "Think Hormone, Think CORONA."

Gufic Biosciences - the Ferticare franchise (Puregraf gonadotropin, Cetrocare antagonist, Guficin Alpha which is the category leader in recurrent implantation failure) is ~₹100 cr+, ~11-15% of revenue, growing ~16-18% - and the stated strategy is literally "increasing share of cycle in IVF." recombinant FSH in Phase III. sitting on a lyophilisation moat (largest indian lyo capacity) that also lets it CMO gonadotropins for others. (FY26 PAT dipped on the Indore ramp - the fertility strength is masked at the consolidated line.)

Beta Drugs / Nivian - the one nobody's looking at. a listed oncology small-cap that just bought 66.1% of Nivian for ₹69.4 cr (₹105 cr for 100% ≈ 13x EV/EBITDA) - a near-pure IVF-pharma franchise: ₹43 cr, ~31 products already inside 1,500+ fertility clinics and 1,500+ IVF labs, fully asset-light (11 third-party manufacturers), ~4.5% of the ₹1,000 cr non-recombinant segment, with recombinant in-licensing as the next leg. management's own line on why it's not a clinic bet: "they are into services; we are into products… branded business." highest purity, highest beta, smallest base.

layer 3 - the lab (the import-substitution white space)

~₹15-25k of consumables per cycle - culture media, ICSI needles, catheters, vitrification kits - almost all imported (CooperSurgical, Vitrolife, Kitazato; KARL STORZ on OT). no clean listed indian play yet. which is exactly why it's the white space to watch - the day a credible indian consumables maker shows up, it's the rPET/defence-components arc all over again.

layer 4 - diagnostics & genetics (the steepest runway)

PGT/genetic screening of embryos: only ~5% of indian IVF patients do it vs ~25% in the US. that's the steepest penetration ramp in the whole chain, pure attach-rate margin on each premium cycle. own it via the listed labs -Metropolis (bought Core Diagnostics for oncogenomics), Dr Lal, Thyrocare. they compound off every cycle, agnostic to which clinic ran it.

layer 5 - the continuum (M&C lifetime value)

an IVF pregnancy is high-risk → NICU → pediatrics → vaccination. the "fertilisation to immunisation" loop. listed proxy: Rainbow - whose own IVF is ₹61 cr (3.7% of revenue), captive and B2C, growing ~25%, inside a ~32% EBITDA M&C compounder. if you want the services side with an actual moat (pediatric super-specialty is far stickier than an IVF cycle), rainbow is the way - not a pure clinic.

so how do you play it?

cleanest moat is the hormones, not the clinics. four listed ways to own it. want the services pure-play? wait for indira's IPO and be ruthless on price, or own rainbow now or go w gaudiam.

want the longest runway? diagnostics/genetics (metropolis) at 5% PGT vs 25% US, and keep a file open on the consumables white space.

none of this is a bear call on fertility. the demand is structural, the organised share from 40% heading to 70-75% over a decade - same path pathology took ten years ago, eyecare five. we just think the chain is a lot bigger than the clinic. and when everyone's queuing for the storefront, we'd rather own the molecule every cycle has to buy.

the boring derivative usually beats the hyped direct play. we've said that before.

we wrote about zepto - the bit where aadit's narrative had shifted from "we focus on premium, dont compare us w dmart" to "we sell atta/rice/staple, we are in competition with dmart."

lets talk about the WHY part (its bear thesis) - lets check

zepto's strategy in one line: focus on densitywhich enables higher discounts which leads to higher frequency which again make density approach sensible.

they have the highest dark store density of any QC player - ~21 stores per city across 61 cities, vs blinkit's 9 across 243. 77% of stores are in top-8 metros (vs 57% for blinkit, 61% for instamart). they're also the most aggressive discounter (read value customers) - 21-26% headline discount on products since oct '25, vs blinkit at 14-17%.

this works in metros. and only in metros.

zepto's serviceable pincodes average 14k people/sqkm - basically identical to overall metro pincodes at 16k - tier-1 is 6k. tier-2 is 4k. tier-3 is 3k. metros are 3-5x denser than where zepto hasn't gone yet. the value prop of QC (saving time, reducing friction, instant gratification) is also at its highest in metros - traffic + apartment buildings + affluent customers used to digital shopping. all of that softens in T1/T2/T3 - kirana is a 3-5 min walk, apartment density drops, customers get price sensitive.

now the cost side - typically QC has a hard floor of ~₹95-100/order on variable + other-direct costs. even with OPDPR of ~30, OPDPS of ~2,500 and sub-2km customer distance - you can't realistically compress below that. and all the inputs (rider salaries, rentals, packaging, picker wages) are inflationary. so the floor drifts UP over time. there's no scenario where this number goes down meaningfully.

unit economics (4Q26):

blinkit: net AOV ₹525, adj EBITDA +₹1/order (PROFIT)

instamart: net AOV ₹504, adj EBITDA -₹76/order

zepto: net NOV ₹357 (32% lower than blinkit), adj EBITDA -₹59/order

zepto's NOV per order is 32% below blinkit. that's the cost of EDLP. they're trading basket size for frequency - MAU plateaued at ~60mn since aug '25; sessions/user/week up from 8 to 11; delivery partner app MAU growing 2-3x faster than user app MAU (implies orders per user are rising).

so the engine works as designed. the question is - can it scale beyond top-8, where the next leg of penetration has to come from?

the value proposition may need to evolve. and a new value proposition may bring new economics. translation - the playbook is metro-specific. the T1/T2/T3 leg is a different business.

how long we gonna play discount/cash burning game?

how much cash these guys holding? eternal ₹18,000 crs, swiggy ₹15,100 crs, zepto ₹5,700 crs - zepto is 3x outgunned. ANNNDDD amazon now + flipkart minutes are spending parent-co money for share – we don’t see any breathing space in competitive intensity for CY27 atleast.

overlay the WAU data CLSA published 25 jun: blinkit/bigbasket/jiomart at 51.2/20/9.7m WAUs. jiomart's WAU fell below 10m for the first time since dec '25 (another quick commerce bet of reliance falling, after Dunzo) - blinkit's YoY user additions in 4QFY26 were higher than the next three players combined (flex!). metro pincodes are 99% covered by at least one QC player - top-4 cities (NCR, bengaluru, Mumbai, hyderabad) = 73% of all dark stores across the top-8 metros.

so where does this leave zepto?

bull case: density flywheel keeps spinning in metros, IPO funds the T1 build-out, they figure out a different unit econ model for T2/T3

bear case: business continues as it is

this isn't a undiscovered name (moti has sold ₹25 crs block to multiple FOs) - it isn't a comfortable-valuation setup (IPO premium), and the catalyst (IPO itself LOL) is also the timing risk - it's a great case study on what happens when a discount-led flywheel meets a hard cost floor (snapdeal?).

again, as we said earlier - zepto is a phenomenal operating story. team has built something genuinely impressive - we are not the bear case here. we're just saying - when the math forces the story to change, the new story isn't the original thesis. and when you need money, you change story. we've said that before.

This is new from Vedanta group.. post the corporate restructuring initiative - led by demerger of oil, aluminium,steel,power among others, group has announced a foray in "REAL ESTATE" space by creating a subsidiary - "Vedanta Property Platforms"👇

When portfolios were hitting all-time highs and returns were beyond everyone’s imagination, I told a few friends one thing again and again

Clear your debt first.

I rarely say this.

Few listened. Few didn’t.

Market profits are temporary screenshots.

Debt is a permanent barking dog at your gate.

for us, one of the major takeaway from aadit's IPO conference is - in last 2 years, the commentary of quick commerce have shifted from

"oh boy we aint servicing the value segment, we focus on the premium one, one who prefers convinience - dont compare ourself w dmart"

to

"we sell majorly atta, rice, staple and oil on our platform - we are focusing on value segment, India doesnt buy grocery once in a month, we are in competiton to dmart"

(we are not demeaning anyone, or trying to drag anyone. we have huge respect for what zepto has become over last few years - we are trying to point that when you need money, you change story)

"i don't know what happened in hospital space this quarter" - no stress, we got you!

we read 17 listed hospital concalls (a few the prior quarter too) to know what's cooking on ground - at blindspot, we track this space closely.

what's inside?

- whose revenue grew the most and why, whose occupancy climbed, whose fell, and the real reason behind each with mgmt quotes.

- the trends we picked up - like every chain has a different read on mother & child (with genuine beef b/w apollo & rainbow) - one govt scheme that helped some hospitals and screwed others.

- the big one: are ARPOB, ALOS and occupancy even the right way to track a hospital anymore?

a lot more to unpack guys

link: https://t.co/W1B7KpfNZo

"i don't know what happened in hospital space this quarter" - no stress, we got you!

we read 17 listed hospital concalls (a few the prior quarter too) to know what's cooking on ground - at blindspot, we track this space closely.

what's inside?

- whose revenue grew the most and why, whose occupancy climbed, whose fell, and the real reason behind each with mgmt quotes.

- the trends we picked up - like every chain has a different read on mother & child (with genuine beef b/w apollo & rainbow) - one govt scheme that helped some hospitals and screwed others.

- the big one: are ARPOB, ALOS and occupancy even the right way to track a hospital anymore?

a lot more to unpack guys

link: https://t.co/W1B7KpfNZo

Data Patterns GaN HAWK I Radar can track 1m2 Target at 200Km

For academic purpose we can calculate the Detection Range for low RCS targets using available data

Detection Range for

0.01 m2 Target ~63 km

0.001 m2 Target ~35 km

This is why stealth technology is so effective

The "slavery" framing is lazy. Delhi's minimum wage for unskilled labor is around Rs 18,000 a month, which works out to roughly Rs 70 per hour over an 8-hour day. Carrymen is paying 2x that for ad-hoc gig work.

Porters have existed at Indian Railways forever. Caddies at golf clubs. Bellhops at hotels. Coolies at every mandi in the country. The only thing new here is a brand that takes ownership of experience and hourly pricing instead of a tip economy.

What's actually happening is informal labor moving onto a platform. That means ratings, dispute resolution, predictable demand, and eventually PF/ESI coverage.

Organizing the supply side has compounding benefits. Urban Company partners can now show platform income to qualify for personal loans. Rapido and Swiggy riders get accident cover and access to phone and two-wheeler EMIs. India's informal sector is around 80% of total employment. Every platform that drags a slice of that into the formal economy widens the tax base, raises measured productivity, and shifts margin from the contractor or household back to the worker.

Slavery means coercion, no exit, no wages. India has actual bonded labor in brick kilns and agricultural debt traps. Applying the word to a consensual gig porter app trivializes the people who are genuinely trapped.

If you're uncomfortable with someone being paid Rs 149 to carry your shopping bags, the discomfort is yours to sit with. The work was always being done. It was just being done by domestic help paid in cash with no rights.