This Memorial Day, we honor and remember the brave men and women who gave their lives in service to our country. 🇺🇸

We are forever grateful for their sacrifice and the freedoms they helped protect.

Cinco de Mayo isn’t about one big moment—it’s about resilience and showing up when it counts.

That’s how financial plans work too.

Not one perfect decision… but a series of good ones over time.

The housing market didn’t crash. It froze.

Here’s what’s happening:

• Millions locked in ~3% mortgages

• New buyers facing 6–7% rates

• Homeowners not selling

• Inventory staying tight

👉Prices don’t fall like people expect

This chart explains why.

S&P 500: 7,000

It took ~70 years to go from 0 → 1,000

Just ~1.4 years to go from 6,000 → 7,000

That’s not luck.

It’s compounding.

As markets grow, each 1,000-point move requires a smaller % gain—so milestones come faster over time.

The catch?

It never feels easy when it’s happening.

Time in the market > timing the market.

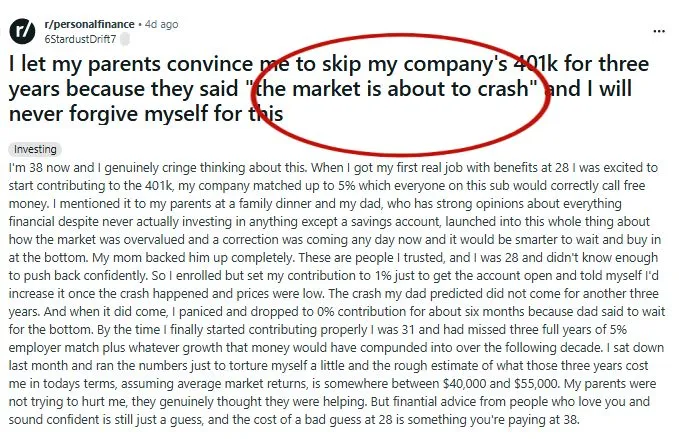

“The market is about to crash.”

Those words may be more expensive than people realize.

Miss a few early years of 401(k) investing and you may lose far more than returns:

• Employer match

• Compounding

• Time

Biggest risk for long-term investors?

Not volatility. It's sitting out.

Fear can be expensive.

Link in comments.

“I can’t touch my Roth until 59½.”

Common myth. Incomplete answer.

Roth IRAs have 3 layers:

✅ Contributions (often accessible anytime)

✅ Conversions (5-year rules apply)

✅ Earnings (where 59½ often matters)

Knowing the difference can be a planning advantage.

2026 is yet another reminder that investors who maintain a long-term perspective and hold a balanced portfolio are often rewarded for their patience.

The S&P 500 has fully erased its ~10% drawdown from the Iran conflict and is probing new all-time highs, despite ongoing uncertainty, poor sentiment, and higher energy prices.

The reality is that staying invested, and staying the course, remains the best option for most investors!

Today I joined @NPetallides on @SchwabNetwork to discuss:

-stock market's resilience in 2026

-the sentiment recession

-bifurcated Tech trade

So much fun! More below 👇

https://t.co/wX6I61Vts6

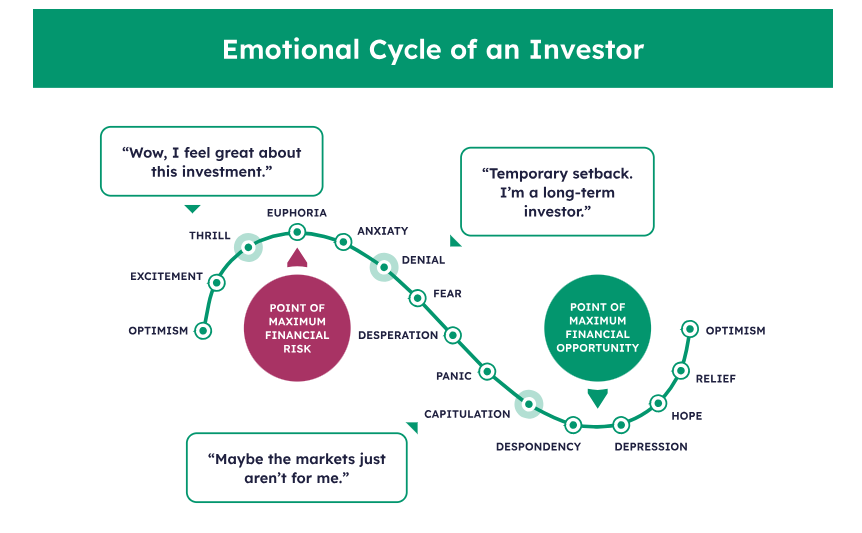

Every bear market feels different.

But the emotional cycle never changes.

Some investors panic.

Some stay disciplined.

A small group leans into opportunity.

The market rewards behavior, not predictions.

This is where long-term wealth is actually built.

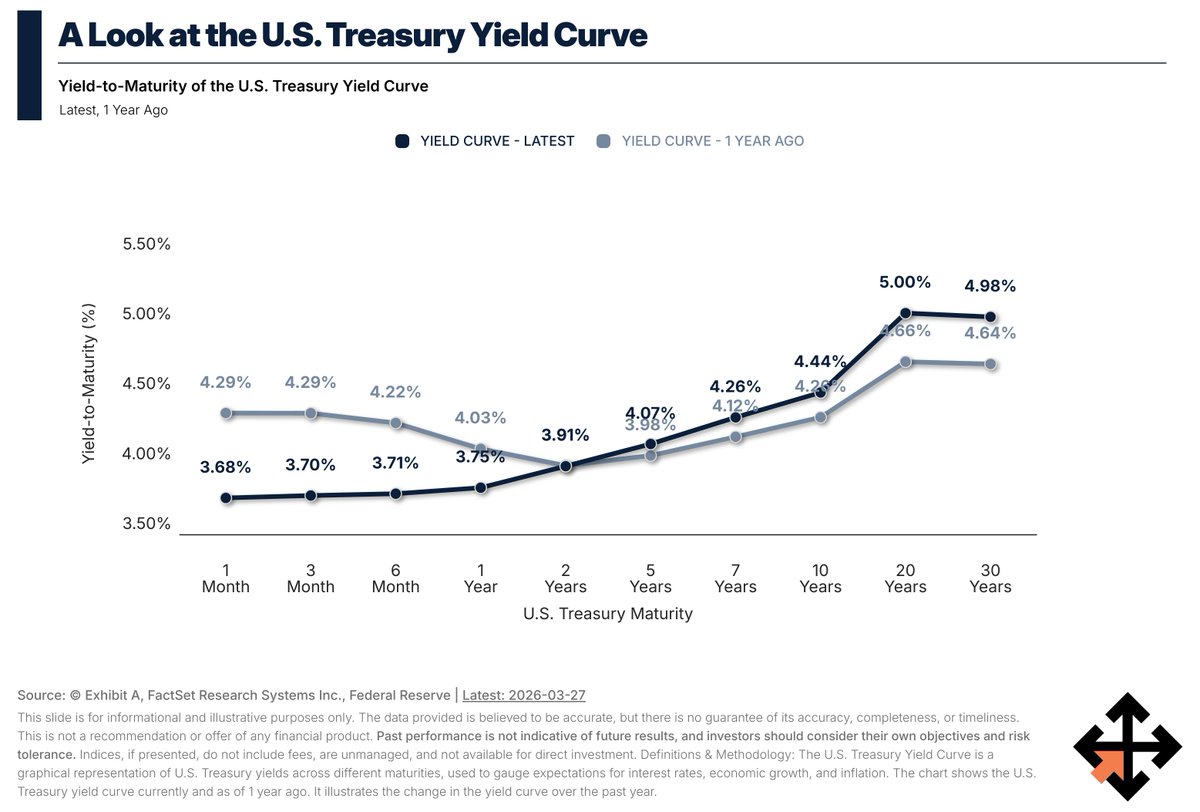

The yield curve is no longer inverted.

That’s a shift.

But this isn’t a “green light” moment.

With higher oil, global tension, and sticky inflation, the risk is more complex:

Slower growth + higher prices.

Interest rates reflect expectations, not certainty.

Stay disciplined.

Grateful to the @MarketsGrp to join DMV-based investments professionals at the Private Wealth DC Metro Forum and inviting me to speak/share @Sandbox_FP insights on equities during this tricky and turbulent market tape in 2026.

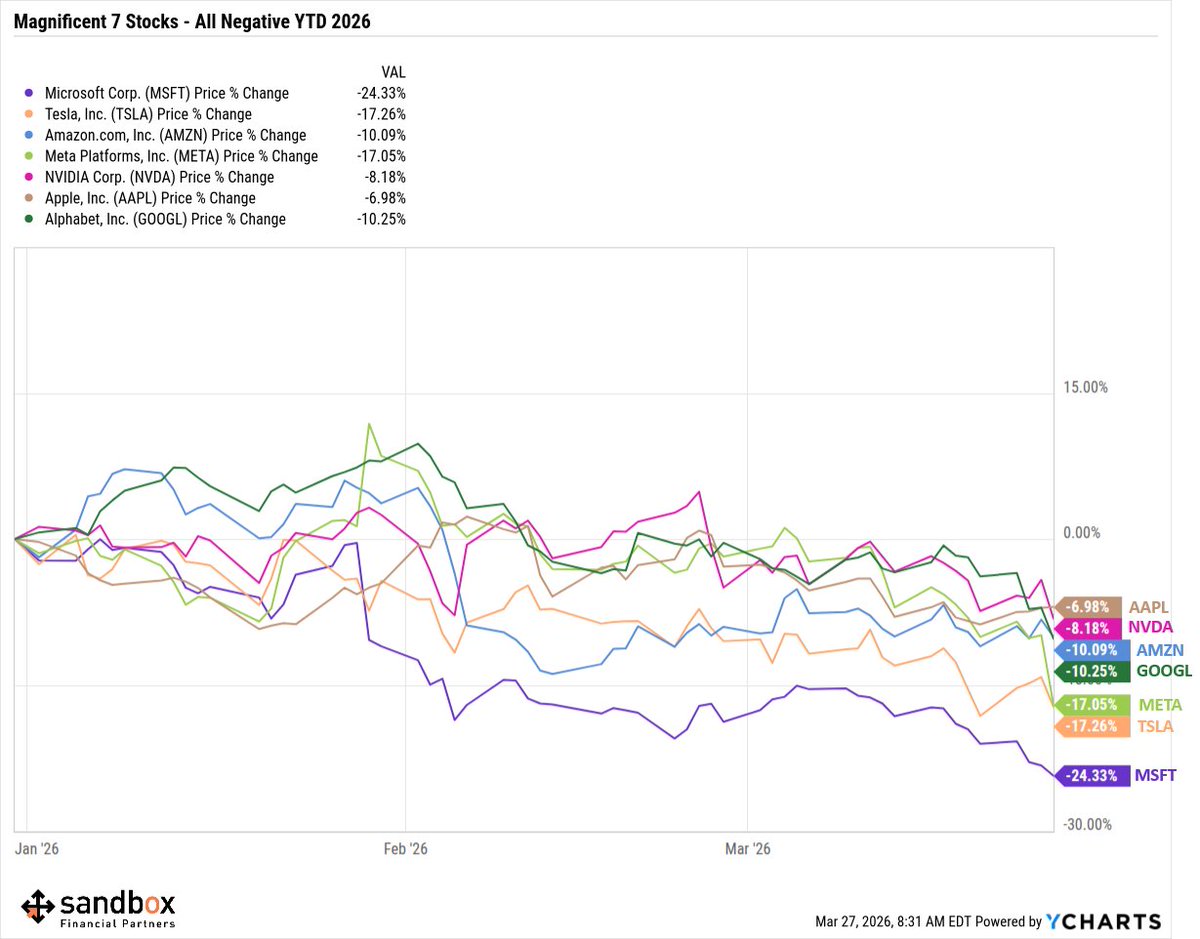

The Magnificent 7 are all negative in 2026.

The same stocks that carried the market… are now dragging it.

$MSFT -24%

$TSLA -17%

$META -17%

$GOOGL -10%

$AMZN -10%

$NVDA -8%

$AAPL -7%

Leadership changes. Fast.

If your portfolio = yesterday’s winners, than you might be taking more risk than you think.

📉 Investors forget this every time markets get volatile.

Since 1950, the S&P 500 has seen:

• 72 pullbacks (5%+)

• 26 corrections (10%+)

• 11 bear markets (20%+)

• 6 drops (30%+)

Volatility isn’t unusual.

It’s the price of long-term returns.

The real risk?

Making emotional decisions during it.

Midterm years are historically the most volatile in the presidential cycle.

Since 1950:

• Avg midterm drawdown: -17.5%

• Avg full-year return: +4.7%

In other words:

📉 Big pullbacks can happen

📈 And the market can still finish the year positive

If markets get choppy in 2026, history says that would be normal.

As a financial planner, I remind clients of this often:

The key isn’t avoiding volatility.

It’s staying invested and sticking to your long-term plan.

For a few days each year…

South Beach becomes the center of the investment world.

That’s what Future Proof Citywide @FutureProof_HQ does.

Thousands of advisors, asset managers, and innovators all in one place talking about the future of wealth management.

Great spending time here with Andrew, @BlakeMillardCFA , and myself from @Sandbox_FP.

The big theme this year:

Artificial intelligence isn’t just another tool.

It’s quickly becoming the operating system for how firms invest, serve clients, and run their businesses.

But one thing won’t change.

The firms that win will still be the ones focused on helping clients build:

• clarity

• confidence

• and long-term financial security

Great conversations, great people, and a lot of ideas coming back with us to the DMV.

Everyone is talking about AI.

Very few people understand how big the shift could actually be.

At Future Proof Citywide this week, I had the chance to catch up with Dan Ives, one of the most recognizable voices covering the technology sector.

His message was pretty simple:

Artificial intelligence isn’t a hype cycle.

It’s the next major technology platform shift — and it may end up being even bigger than the ones before it.

Think internet in the 90s.

Mobile in the 2000s.

We’re still in the early innings of what AI will do to companies, productivity, and markets.

For investors, the challenge isn’t reacting to headlines.

It’s identifying which businesses will actually monetize the AI transformation over the next decade.

Also… credit where it’s due.

Dan might be the best dressed person on South Beach this week. 😄

@FutureProof_HQ@DivesTech@Sandbox_FP

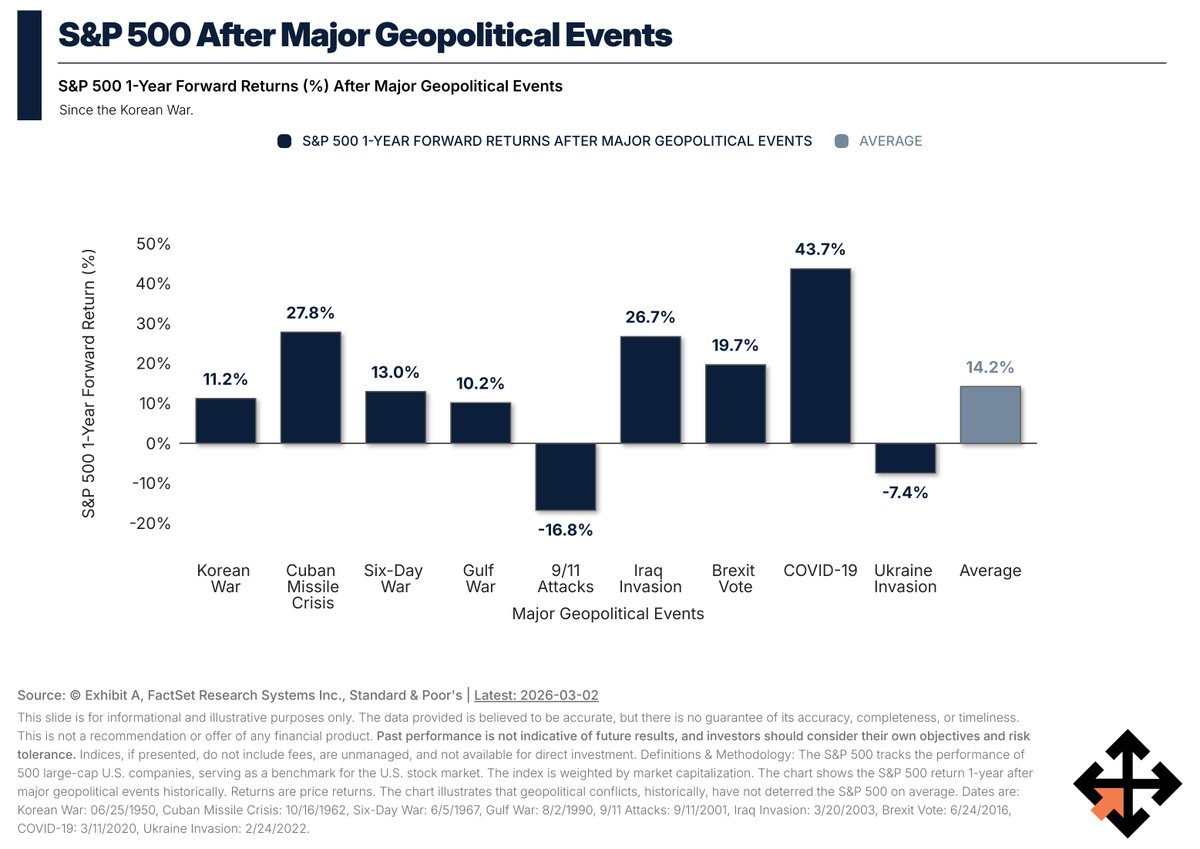

Conflict escalated in the Middle East this weekend.

From an investing lens:

☑️ S&P 500 avg +14% 1-yr after major geopolitical shocks

☑️ Short-term volatile

☑️ 12-month returns positive most of the time

Markets price fear fast.

They recover before headlines improve.

Stay disciplined.

A client told me:

“I want to start picking individual stocks.”

They were also taking 401(k) loans and carrying 22% credit card debt.

Excitement isn’t readiness.

Before stock picking:

• Emergency fund

• No high-interest debt

• Consistent saving

• Long-term plan

Foundations build wealth. Fireworks don’t.

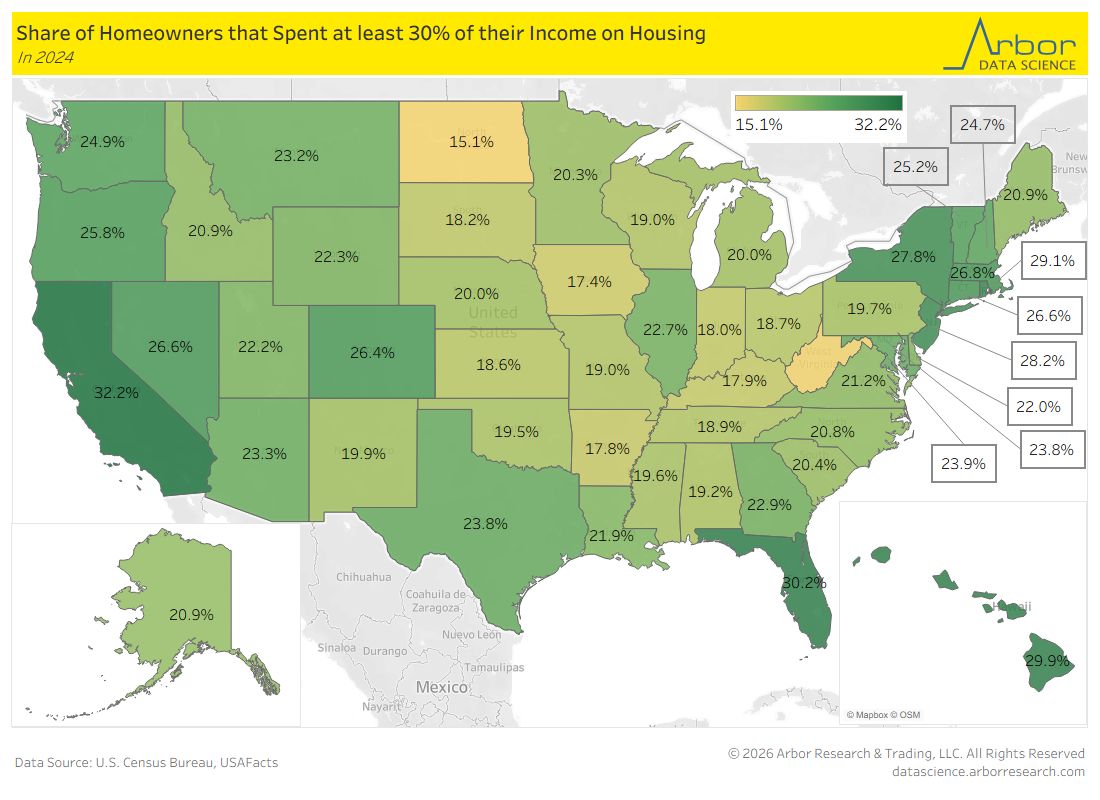

🏡 Where you live can determine how financially stressed you feel.

California: 32.2% of homeowners spend 30%+ on housing.

Florida: 30.2%.

North Dakota: 15.1%.

Nationally? 1 in 4 homeowners now spend 30%+ of income on housing.

That’s how people become house poor.

Housing should build wealth — not pressure.