500 active credit repair clients as of this week

Here's what this week looked like in results:

Stephen A. came in with a 624 on Equifax and a 622 on Experian

Left with 773 on both

+149 on Equifax. +151 on Experian

In one cycle

That's not a typo and it's not a special case. That's what happens when you find every single item dragging a score down and remove them all at once instead of one at a time

John G. came in with a 644 across the board

Left with 679 on Equifax, 679 on Experian, and still climbing on TransUnion

+35 across every bureau simultaneously. Clean movement across all three at once

Carrie W. was already sitting at 713-718 range coming in

Pushed her to 718 Equifax, 697 Experian, 708 TransUnion

Incremental movement at the top of the range is harder than people think. Every point above 700 requires more precise work than the points below it.

Carrie's file needed surgical optimization not broad dispute work. Different problem. Same process

Three clients. Three completely different starting points. Three different challenges on the file. Same outcome every bureau moved in the right direction in the same cycle

This is what 500 active clients looks like operationally

Not 500 people getting template letters sent on their behalf once a month. 500 active files being worked simultaneously across bureau disputes,

direct furnisher disputes under FCRA 623, CFPB complaints, pay for delete negotiations, and shadow bureau cleanups

Every file gets the full sequence. Nothing gets skipped because it seems too small or too hard

Stephen going from 622 to 773 in one cycle means he went from locked out of meaningful business funding to qualifying for $150K-$250K at 0% APR

That gap is not an exaggeration.

A 622 score gets denials and $3,000 limits. A 773 score gets Chase Ink approvals at $50K-$90K on the first application

The number changed. Everything downstream of the number changed with it

500 clients. Results posting every week. This is what we do

(we repair creit in 30-90 days, link in bio)

If you have $10,000 in a regular American savings account right now, you're literally paying the bank to hold your money

You lose $25 a month to inflation

The bank lends your $10K out at 7% and makes $58 a month on it

You pay $25, they make $58, neither of you owns the money

This is the most expensive financial product in America and 80% of households use it

The national average savings account rate in America right now is 0.46% APY. That's what a Chase, Wells Fargo, or Bank of America savings account pays you. On $10,000, that's $46 a year. About $3.83 a month

The current US inflation rate is 3.0-3.5%. So while your account "earns" $3.83/mo in interest, your purchasing power on that same $10,000 declines by roughly $25-29/mo. Net real return: negative $21-25/mo

You're paying the bank $250-$300 a year for the privilege of keeping your money there

Now look at what the bank does with the same $10,000:

Banks operate on fractional reserve. For every $1 of deposits, they can lend out roughly $9-10 in loans. Your $10K becomes the basis for $90K-$100K of bank-issued debt. They lend it out as:

Mortgages at 6.5-7.5% APR

Personal loans at 12-18% APR

Credit cards at 22-29% APR

Small business loans at 8-12% APR

Average net interest margin on every dollar deposited: 3.0-3.5%

On your $10,000 specifically, the bank generates roughly $300-$350/yr in net interest income. They pay you $46. They keep $254-$304

You're not their customer. You're their inventory. They're using you to print money for themselves and selling you back the illusion of being saved

The math on a regular American household:

Average savings account balance in America: $5,300 (median household)

Average checking account balance: $5,400

Total cash sitting in low-yield bank accounts: $10,700

Annual interest paid by bank: $49

Annual loss to inflation: $321

Annual bank profit on this household's deposits: $321

The household loses $272/year holding cash at their regular bank. The bank earns $321/year. The combined wealth transfer per household per year: $593

Multiply by 130 million American households: roughly $77 billion a year quietly moves from regular Americans to their banks via the low-yield savings account product alone

The play (three versions, choose your aggression level):

Version 1: minimum effort. Move everything from your regular savings to a high-yield savings account. CIT Bank Platinum Savings (4.10% APY), Marcus by Goldman Sachs (4.00%), Wealthfront Cash (4.00%), Ally Bank (4.20%), Discover Bank (4.10%). Same FDIC insurance. Same liquidity. Same access. 8-10x higher interest rate. On $10K, that's $410/year instead of $46. Net positive vs inflation: +$110/year instead of -$275

Version 2: medium aggression. Move cash to a HYSA. Open 2-3 0% APR business credit cards through your LLC. Route your monthly business spend through the cards instead of paying cash. Cash stays parked at 4.10%. Cards pay off from operating cash flow each cycle. You're now earning the spread between the bank's free credit and your high-yield savings rate

Version 3: full play. Stack $150K-$250K in 0% business credit. Park the displaced cash in HYSA at 4.10%. Annual interest earned: $6,150-$10,250 on bank money you're holding at 0%. Deploy excess capital into real estate, inventory, or higher-yielding investments. Net annual return: roughly $15K-$45K on capital you didn't own a year ago

The fundamental error most Americans make with money:

They treat their bank as a partner. The bank is a counterparty. Every dollar in your savings account is a dollar the bank is earning 7% on while paying you 0.46%. Every $1,000 in your savings is $65/year of pure profit to JPMorgan that you funded directly

The richest people in this country don't keep cash at banks. They keep cash in money market funds (4.8% yield), treasury bills (4.5% yield), high-yield savings (4.10% yield), or productive assets (real estate, equities, business operations earning 12-25% returns). Their banks see them only as borrowers, never as depositors

Your regular savings account is the bank charging you a 3% annual fee, processed as a hidden discount on what they could be paying you. They sell you "FDIC insurance" and "convenience." Every other bank in America has both, at 8-10x higher rates

You're not saving money in your savings account. You're losing it. Slowly. Politely. With every monthly statement

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

Devon just got approved for $28,000 on Chase Ink Business Unlimited yesterday

That's card one

He already has a Chase Ink Business Cash sitting at $15,000

Chase allows you to combine credit limits across Ink cards.

One call to the reconsideration line and those two cards become one $43,000 credit line on a single card

We also have a Chase Ink Preferred application pending right now. Expected approval: $15,000-$20,000

When that lands we combine again

One card. $58,000-$63,000 in available credit. Same bank. Same personal guarantee he already signed. Zero additional applications needed

This is the part of business funding nobody teaches

Getting approved is step one. Knowing what to do with the approvals after is where the real limits get built

Most people get a $28,000 approval and stop there.

Think that's their ceiling. Don't know that 3 cards at the same bank can become one card at 2-3x the limit with a single phone call

Devon started this week with a $15,000 card

By the time the pending approval lands and we run the combination he'll be sitting on $58,000-$63,000 in available Chase credit alone

Then we hit the other banks and stack 10-25k per bank at 7-8 more banks....

once were done, hes going to be looking at $150,000 to deploy

(This is what the full capital stack build looks like in real time. 720+ score required. Link in bio)

There's a free 5-minute IRS form that banks treat like a second financial identity.

With a clean 720 score, that file can get $250,000+ at 0% interest.

Most people beg for loans at 12% because nobody showed them the other door.

I made the full $250K funding board public.

Like + comment "credit" and i'll send it to you for free (must rt, and be following)

Spent 11 minutes filling out an online credit card application

Walked away with $80,000

The same $80,000 takes the average american 18 months of W-2 work after taxes

Same banks. Same person. Two completely different money systems and 99% of americans only know about one of them

W-2 path:

College: 4 years

Starting analyst job at Goldman: $115K base, $30K-$60K bonus year 1

Years 1-3 (average promotion track): $145K, $185K, $225K

Year 4-5 associate: $260K-$310K

Total gross W-2 income across 5 years: roughly $1.1M

Federal + state + city tax burden at NYC rates: 41-46%

Net take-home across 5 years: $620K-$650K

Real expenses (rent, food, lifestyle, student loans): $480K-$520K

Actual savings retained after 5 years: $130K-$150K

11 years at a Fortune 500 salary path with average promotions and conservative spending nets out around $90K-$110K in W-2 take-home savings net of cost of living. That's an aggressive estimate

11 minute path:

Open Chase Ink Business Cash application online (it's an 11-section form, takes the median applicant 8-13 minutes to complete). Submit. Approval typically lands within 90 seconds for 720+ FICO

Average approval limit at 720+ score with $200K-$400K projected revenue: $35K-$60K. 0% APR for 12 months. No interest. No principal payments required during the promo period (only the minimum, which is 1-2% of balance)

Available capital from the application: $35K-$60K

Cost of capital for 12 months: $0

Time to access: same business day

Education requirement: zero

Years of experience required: zero

Boss approval required: zero

W-2 history required: zero

Two applications across Chase Ink Cash and Chase Ink Unlimited in the same session counts as a single hard inquiry: $80K combined approval

11 minutes of typing for $80K in capital is a higher hourly rate than every job that doesn't require a license. Bezos at his peak was making about $300K/minute on Amazon stock movement. He'd consider this slow. For everyone else, it's the highest paid 11 minutes available in America

The pushback nobody actually counters:

"That's a loan, not income"

The loan is at 0% interest. If you deploy it into anything earning above 0% (a business, real estate, inventory, a savings account, a brokerage), the spread is real net positive cash flow. Loans at 0% are functionally bank capital handed to you for free until the promo ends

"You have to pay it back"

You pay it back from the operating profit generated by deploying the capital. The deployment is what creates the $80K. The application just unlocks the capital that enables the deployment

"What if your business doesn't make money"

Then you cycle the cards to fresh 0% offers using a vendor like Trykashu (6.5% fee, 72-hour funding) to clear balances cleanly between cycles. Annual cost of holding $80K perpetual capital at 0% via cycling: roughly $5,200 in fees. Anything you earn above $5,200 with that capital is net profit

The reason this asymmetry exists:

The American labor market is regulated, taxed, hierarchical, and slow. Every dollar of W-2 income passes through the IRS, state tax, FICA, Medicare, and your employer's HR system. The marginal tax rate on a high earner exceeds 40%. The marginal increase per year of experience is capped by industry compensation bands. Your boss decides your raise

The American consumer credit market is unregulated at the access level, untaxed at the borrowing level (loans aren't income), accessible to anyone with a clean credit file, and instant. The bank's underwriting algorithm decides your approval limit in 90 seconds based on a number you can repair in 60 days

The bank operates by a different rulebook than your employer. Both rulebooks are entirely legal. Both rulebooks are entirely public. One of them moves more money in 11 minutes than the other moves in 11 years

The labor market is the slow path. It was always the slow path. The credit market is the freeway running parallel that 99% of W-2 employees have never used because nobody told them the entrance was free

dm me "funding" and i'll show you how you can qualify for up to 250k in 0% APR funding (if you have a 700+)

There's $42 billion sitting in state government accounts right now with your name on it

The average claim is $1,200 cash

Most americans have between $200 and $25,000 they have no idea exists

You can claim it in 14 days with a $0 fee

The IRS, every state government, life insurance companies, payroll companies, and former employers have all sent money to YOU at some point that never reached your hands. By law, that money goes into state "unclaimed property" accounts where it sits, untouched, waiting for you to claim it. Every state has one. Every state's database is searchable. Every state's claim process is free

Total unclaimed property in US state accounts as of 2024: $77 billion. Annual claim rate: roughly 35-40%. Unclaimed balance growing: yes (more new property added than claimed each year)

What ends up there:

Final paychecks from jobs you left (very common: HR processes the last check after you've moved or closed the bank account)

Security deposits from apartments you moved out of

Refunds from cancelled services (utilities, gym memberships, insurance policies)

Tax refunds that bounced back to the IRS

Stock dividends from companies you owned shares in

Life insurance payouts where the beneficiary couldn't be located

Pension and 401(k) balances from former employers

Bank account balances closed without notification

Safe deposit box contents (yes, including jewelry, gold, and physical assets)

Class action settlement payments

Money orders and traveler's checks never cashed

Refunds from medical bills overpaid

Court-awarded damages from cases you weren't aware of

How it happens:

When a financial entity owes you money and can't locate you (because you moved, changed phone numbers, closed the account, or the company couldn't reach you for a year), state "escheatment" laws require them to turn the money over to the state unclaimed property division after 1-5 years of dormancy

Once it's in the state account, it sits there forever. There's no time limit on claiming it. Money turned over in 1985 is still claimable today

The search:

Step 1: go to unclaimed. org (the National Association of Unclaimed Property Administrators, a real government-affiliated portal)

Step 2: search your name in every state you've EVER lived in (very important: most people only search their current state)

Step 3: search variations of your name (with middle initial, without, maiden name, married name, common misspellings)

Step 4: also search at MissingMoney. com which aggregates 45+ state databases simultaneously

Step 5: for federal unclaimed property, search treasurydirect. gov for treasury bonds, IRS. gov for unclaimed tax refunds, and PBGC. gov for unclaimed pensions

Average search time: 25 minutes

Average matches per searcher: 1-3 unclaimed property records

Average dollar value per match: $200-$2,400 (varies wildly; some are $20, some are $50K+)

Median total unclaimed property per American: $1,200

The claim process:

Every state runs its own claim system but the steps are similar:

Step 1: identify the property on the state website

Step 2: file a claim (online for most states, paper for some)

Step 3: provide ID verification (driver's license, SSN, proof of address)

Step 4: provide proof of connection to the property (former address, employer name, account number if known)

Step 5: state reviews and either approves or asks for additional documentation

Processing time: 2-8 weeks for most states. California is fastest (often 14 days for amounts under $1,000). Texas is slowest (3-6 months for larger claims)

Cost: $0. State unclaimed property divisions never charge fees for claims. If anyone asks you to pay a fee to claim your unclaimed property, it's a scam

Real cases:

A guy in Phoenix searched 4 states he'd lived in (Arizona, Colorado, Texas, California). Found unclaimed property in 3 of them:

Colorado: $340 (security deposit from 2017 apartment)

Texas: $1,840 (final paycheck from 2019 job)

California: $4,200 (stock dividend from a company his uncle had given him 1 share of as a kid)

Total claimed: $6,380. Time invested: 1 hour of search + 12 weeks waiting for checks

A woman in Florida found $18,400 in unclaimed life insurance proceeds from her grandmother's policy (grandmother died in 2009, beneficiary was the woman, insurance company couldn't locate her after multiple address changes). $18,400 sat in Florida's unclaimed property account for 14 years. She claimed it in 6 weeks

A retired couple in Ohio found $52,000 in unclaimed pension benefits from a small employer the husband had worked for in 1981. Company had been acquired, the pension administrator escheated funds in 2003 when they couldn't locate him. The couple discovered it in 2024 during a routine search. Claimed and received in 8 weeks. Their retirement plan got rewritten on a Tuesday afternoon

The reason this exists:

State governments LOVE holding unclaimed property because they earn interest on it (4-5% annually) while it sits dormant. Several states essentially treat unclaimed property as a no-cost loan from their citizens. They have zero incentive to publicize the program. Most state unclaimed property divisions spend less than $200K/yr on marketing (in contrast: most state lottery divisions spend $40M+ on marketing)

The IRS has roughly $1.5B in unclaimed tax refunds at any given time. The PBGC has $300M+ in unclaimed pensions. The major life insurance companies have an estimated $1B+ in unclaimed policy proceeds. None of these institutions are particularly motivated to find you. The money just sits

The 25 minutes to search is the highest-paid 25 minutes in American personal finance. Median return: $1,200. Average return: $4,400. Highest documented single-claim recovery: just over $1.2 million (an heir who discovered an unclaimed life insurance policy from a great-grandparent)

Most Americans don't search because they assume "if I had money owed to me, someone would have told me." Nobody is going to tell you. The system is designed so that nobody tells you. The money sits because nobody is required to find you, and you're never reminded that the database exists

It exists. Your money is probably in it

unclaimed. org

missingmoney. com

treasurydirect. gov

irs. gov/refunds

25 minutes. Free. Yours

(i fix credit in 30-90 days. link in bio)

Dave Ramsey is worth $200 million teaching broke people to cut up their credit cards

He filed bankruptcy himself in 1988 when he was $4 million in debt

Then he built an empire telling poor americans that the tool he could have used to actually become rich is the devil

Read that timeline twice

In 1988, Dave Ramsey owed roughly $4 million to banks and creditors after a real estate empire collapsed. He filed Chapter 7 personal bankruptcy. The federal bankruptcy process discharged most of his debt. He started over with no obligations to the banks who had loaned him millions

Then in the early 1990s he started "Financial Peace University" and built it into a $200M media company over 30 years. His core teaching: avoid all debt, cut up your credit cards, never use credit, pay cash for everything, save for emergencies in a regular savings account, follow the "Baby Steps" plan, become rich slowly through index funds in your 401(k)

The teachings are not designed to make you rich. They're designed to be safe enough for the bottom 30% of financial literacy to follow without hurting themselves

That's a fine product. The problem is the 70% above the bottom 30% who follow this advice and miss every wealth-building tool that the actual rich use

What Dave Ramsey tells you to do:

Save $1,000 emergency fund

Pay off all debt smallest to largest (the "debt snowball")

Save 3-6 months of expenses

Invest 15% of income in mutual funds

Save for kids' college

Pay off your mortgage

Build wealth and give generously

What rich Americans actually do:

Stack $200K-$400K in 0% APR business credit (covered in earlier posts)

Use that capital to buy cash-flowing assets (real estate, businesses, ATM routes, vending machines)

Hold cash in 4.10% APY HYSA earning $8K-$16K/year on the spread

Borrow against assets (Elon style, never sell, never pay capital gains)

Operate through LLC structures with full Section 179 deductions on vehicles, equipment, real estate

Use the Augusta Rule to rent personal residences to their own businesses tax-free

Leverage points and miles for $50K+/yr in tax-free travel

Maintain perfect credit scores to maximize borrowing capacity at all times

Buy distressed businesses with seller financing using $0 of personal capital

Notice the central word: leverage. Rich people use other people's money. Banks money. Sellers' money. Tax credits. Promotional financing. They convert other people's capital into assets they own free and clear over time

Dave Ramsey teaches the exact opposite. Avoid all debt. Use only your own money. Pay cash. The Baby Steps plan, executed religiously, produces a person who is debt-free, owns their house outright, has 3-6 months of expenses in savings, and has accumulated roughly $400K-$800K in retirement accounts by age 65

That's a fine retirement. It's not rich. It's middle-class outcomes with extra steps

The richer outcome:

Person uses 0% credit at age 25 to buy a $80K rental property in Cleveland (covered in previous post)

Cash flow $300/mo. Pays off the credit cards from rent over 12 months

Refinances at month 12 to pull capital for the next deal

Repeats every 12 months

By age 35, owns 10 properties worth $1M+ each producing $40K/mo in passive rent

By age 45, owns 30 properties worth $5M+ producing $120K/mo in passive rent

Same starting income. Different path. Result at age 45: financially independent with $1.5M/yr in passive income. Following Dave Ramsey at age 45: still working a job, $200K saved, paying off the mortgage on a single house

The reason Dave Ramsey teaches what he teaches:

His personal trauma from 1988 (the bankruptcy) shaped his worldview. He associated debt with pain. He built a teaching system that prevents the kind of debt that hurt him. The teaching system works as advertised for that purpose. It also limits every student to growth rates that DEBT-LEVERAGED OPERATORS exceed by orders of magnitude

The financial industrial complex loves Dave Ramsey:

Mutual fund companies love him because his teaching funnels $billions into mutual funds annually

Banks love him because his teaching tells you to save your money in their low-yield savings accounts

Insurance companies love him because his teaching pushes term life policies and whole life avoidance

The IRS loves him because his teaching keeps you in W-2 employment paying ordinary income tax rates instead of operating as an LLC capturing structural tax advantages

The only entity that doesn't benefit from Dave Ramsey teaching: you, if you're capable of running anything more sophisticated than the simplest financial plan possible

Dave's net worth: $200M+

Dave's path to that net worth: built and sold an educational media company. Used debt-financed real estate deals before his collapse. Now lives in a $15M home in Tennessee

Dave's audience's recommended path: avoid all debt, drive a used car, eat rice and beans, retire at 65 with $400K

The path Dave used to become a multimillionaire (entrepreneurship + risk + leveraged growth) is the path he tells you to avoid. The path he tells you to follow is the path that produces minimum viable retirement, not wealth

This isn't malicious. He believes his own teaching. He's not trying to keep his audience poor. He's just teaching from his trauma instead of from his success

But the result is the same: 12 million Americans following Dave Ramsey's plan will end up with median financial outcomes. The 12 million following a leveraged-capital plan with the same income could end up with $5M+ in assets by age 50

The difference isn't talent. It isn't income. It isn't intelligence. It's understanding that the credit card isn't the enemy. The credit card is the most powerful unsecured borrowing instrument ever created. The bank built it to extract interest from people who don't know how to use it. The same instrument is a $200K-$400K capital deployment tool for people who do

Cutting up your credit cards is not the path to wealth. It's the path to safety. There's a difference. Most people don't realize the difference until they're 60

(if you want to fix your credit and actually use it as a tool instead of a trap. link in bio)

Cash back on credit cards is $4,000 a year of free money

The average American household spends $72,000 a year. Roughly $50K-$60K of that runs through some kind of payment method (groceries, gas, utilities, restaurants, online shopping, subscriptions, travel, healthcare). If 100% of that spend went onto cash back credit cards averaging 2.5% rewards, the household earns $1,250-$1,500 a year in pure cash back

That's the floor. The ceiling for an operator who actually optimizes the categories: $4,000-$10,000 a year in rewards income on the same total spend. The difference is which card you swipe at which merchant

Most adults use one or two credit cards for everything and earn 1-2% on average. Optimizers use 5-7 cards rotated by category and earn 4-7% blended. Same total dollars spent. Different routing. The difference is real cash

What the maximum-yield card stack actually looks like:

Citi Custom Cash: 5% cash back on your top spending category each cycle (up to $500/month in spend, automatic detection)

Chase Freedom Flex: 5% cash back on rotating quarterly categories (gas one quarter, groceries another, dining another)

Amex Blue Cash Preferred: 6% on US supermarkets (up to $6K/year), 6% on US streaming, 3% on transit and gas

Capital One Savor Cash Rewards: 4% on dining, entertainment, and streaming

US Bank Cash+: 5% on two categories of your choice (up to $2K/quarter)

Wells Fargo Active Cash: 2% flat rate on everything (the catch-all card)

Discover It Cash Back: 5% rotating categories (alternates with Chase Freedom Flex)

Bilt Mastercard: 1% on rent (no transaction fee), 3% on dining, 2% on travel

How a household earns the max:

Groceries (Amex Blue Cash Preferred): 6% back on $6K a year = $360

Gas (Chase Freedom Flex when in rotation): 5% back on $3K a year = $150

Dining (Capital One Savor): 4% back on $5K a year = $200

Streaming and transit (Amex Blue Cash Preferred): 6% on $2K a year = $120

Top monthly category (Citi Custom Cash): 5% back on $6K a year = $300

Rent (Bilt Mastercard): 1% back on $24K a year of rent = $240

Travel (Capital One Venture X): 2% miles on $5K a year of travel = roughly $100 in travel value

Everything else (Wells Fargo Active Cash): 2% back on the remaining $9K a year = $180

Annual total cash back: roughly $1,650 just on those categories with low-friction setup. Add welcome bonuses on the cards you don't already have ($500-$2,000 each, 4-6 new cards a year): $4,000-$10,000 in additional first-year rewards

A household running this play earns $5,000-$12,000 a year in rewards on spending they were going to do anyway. Multiplied across 30 working years: $150K-$360K of pure cash and travel value over a lifetime, just from being intentional about which card to swipe

How this stacks with business funding:

The same logic applies to business spend. Business cards have higher cash back ceilings on category-aligned spend. Chase Ink Business Cash earns 5% on the first $25K of office supplies and internet/cable/phone (enormous category bonus). Amex Business Gold earns 4x on advertising and gas. Capital One Spark Cash Plus earns 2% flat on everything

A business owner running $200K of business spend on optimized cards: roughly $7,000-$14,000 a year in business rewards, layered on top of the personal-card rewards above. Combined household + business rewards: $12,000-$26,000 a year of rewards income

Real example from a client we set up on the optimized card stack last spring:

Personal household spend: $58K, ran through 5 personal cards optimized by category. Earned $2,100 in cash back during year 1

Business spend: $185K, ran through 4 business cards optimized by category. Earned $5,600 in cash back during year 1

Welcome bonuses across all 9 cards opened during the year: $11,400

Total rewards income year 1: $19,100. He used $12,000 for international travel and converted $7,100 to cash deposited into his investment account

The bank wrote him 9 separate rewards checks over 12 months totaling $19,100 for routing his existing spend through the right cards. Time invested: roughly 4 hours total to set up the system, plus 30 minutes a quarter for ongoing maintenance. Effective hourly rate: $3,200

You were going to spend the money anyway. The only question is whether you let the bank keep the 2-7% they were willing to pay you back

(we get 700+ score business owners $100K-$250K in 0% business funding plus the optimized cash back stack. link in bio)

A 12-minute credit card application is worth $250,000

Most adults will spend more time choosing a Netflix show on a Tuesday night than they will applying for a business credit card with a $50,000 limit. The application takes 12 minutes. The capital it unlocks is $50,000-$250,000 in 0% APR financing. The hourly rate of the time invested is the highest paid hour in your life

A 12-minute Chase Ink Business Unlimited application: average approval $35,000 at 0% APR for 12 months

A 12-minute Amex Business Gold application: average spending power $30,000 with NPSL graduation potential

A 12-minute Bank of America Business Advantage application: average approval $40,000 at 0% APR for 12 months

Stack 5-6 of these applications and you've completed roughly 60-72 minutes of work for $150K-$250K of zero-interest capital. Effective hourly rate of the time spent: $125,000-$250,000

Compare to a job:

A senior software engineer making $200K a year: roughly $96 an hour

A surgeon making $400K a year: roughly $192 an hour

A partner-level attorney billing $1,500 an hour: $1,500 an hour

A 12-minute credit card application earning $50K of capital: $250,000 an hour

The application is the highest paid hour any human being can spend, by an order of magnitude

What the application actually requires:

Personal name, address, date of birth, SSN

Personal annual income (most banks accept your gross household income, including spousal income for personal cards and business income for business cards)

Business name, EIN, business address (a home address works for most online or service businesses)

Business industry (NAICS code or general category)

Business stated revenue (most banks don't routinely verify this)

Time in business

Number of employees (1 is fine)

That's it. 12 minutes of typing fields into a web form. The bank's algorithm runs in 30 seconds. Approval comes back instantly or within 24 hours

What stops most people from doing this:

Misconception 1: "I need to be a real business with revenue and employees." False. Sole proprietors with $0 of revenue can apply with a "side business" categorization. You're not lying if you actually have a side business. Most adults do (consulting, freelancing, ecommerce, content creation, etc)

Misconception 2: "Applying will hurt my credit score." Each application produces a hard inquiry that drops your score 5-10 points temporarily. Score recovers in 60-90 days. Total available credit climbing offsets utilization, often producing a NET positive score change after the dust settles

Misconception 3: "I'll get denied because I don't have business credit." Business credit (DUNS, Paydex) doesn't matter for most business credit cards. The bank underwrites your personal credit profile and a stated business revenue. If your personal score is 700+, you qualify for most products

Misconception 4: "12 minutes can't possibly produce $50,000 of value." The actual conversion does happen. The bank wrote the application form to be exactly that fast. They want you to apply. The friction-to-value ratio is the smallest in modern finance

How you actually run the 12-minute play:

Step 1: Pick the bank. Start with Chase Ink Business Cash if you've never had a business credit card before. It's the most approval-friendly for new business owners

Step 2: Form an LLC if you don't have one. $50-$300 filing fee online. Takes 10-20 minutes. Get an EIN from the IRS for free at irs. gov (instant approval)

Step 3: Open the application. Have your LLC paperwork open in another tab. Fill in the fields. The bank asks 18-22 questions across 3 pages. Total time: 11-13 minutes

Step 4: Submit. The decision comes back instantly (Chase, Capital One, Amex) or within 24 hours (US Bank, Citi, Wells Fargo, Bank of America)

Step 5: Receive the card 7-10 days later. Activate. Start using for business expenses

A client we worked with last fall had never applied for a business credit card before. He spent his Saturday morning applying for 5 cards in a coordinated 11-day window. Total application time across all 5: roughly 65 minutes. Total approved credit: $148,000

His effective hourly rate during those 65 minutes: $137,000 an hour. The $148K of 0% APR capital funded his Q4 inventory cycle. The cycle generated $74K of profit. He paid back the cards before the 0% promo expired

The 12 minutes were the highest paid time he's ever spent in his life. Including the time he spent at his $94K W-2 software job

(we get 700+ score business owners $100K-$250K in 0% business funding through the 12-minute application sequence. link in bio)

banks are hiding $100k in free money from you and i'm about to show you exactly how to take it

actually

i've helped 847 people steal $89.3 million from banks using a loophole they pray you never discover

here's exactly what they don't want you to know:

personal guarantee sounds scary

banks make it sound like personal debt

it's not

pg means: "we check your personal credit to approve you"

but the debt reports to BUSINESS bureaus only

your personal utilization stays at 1%

discovered this reading chase's internal training docs at 3:47am

(public sec filings, completely legal)

they wrote: "pg approvals have 94% approval rate but only 6% of applicants know to request business products"

translation: they HAVE to approve you

they just don't advertise it

the exact pg sequence that prints money:

day 1: chase ink (soft pull if you bank there)

day 3: amex business gold (highest limits)

day 5: capital one spark (approves everyone)

day 7: us bank business (hidden gem)

day 10: wells fargo signify (desperate)

day 12: pnc (regional goldmine)

$100k minimum at 0% apr

all using pg loophole

personal credit untouched

real client examples from december:

uber driver, 681 score:

- applied random: $12k approved

- applied with sequence: $97k approved

- difference: order + pg strategy

teacher, 695 score:

- tried herself: denied 3 times

- our sequence: $89k in 72 hours

- she cried on zoom

bartender, 710 score:

- before: maxed personal cards at 18% apr

- after: $118k business funding at 0%

- personal utilization: dropped to 2%

the math that breaks their system:

banks must lend $X billion per quarter

miss target = executives fired

december 31 deadline approaching

panic mode activated

you + pg application = their salvation

they need you more than you need them

requirements:

- 680+ credit score

- under 30% utilization

- $50 llc (optional but helps)

- pulse

but here's what pisses me off:

rich people use pg daily

they call it "leverage"

poor people never learn

banks keep it hidden

every billionaire has pg debt

zero have personal card debt

now you know why

your personal credit is a weapon

pg is how you aim it

banks are the target

stop applying randomly

stop getting denied

stop using personal cards

use their own rules against them

Ready for $100K at 0% APR guaranteed?

Link in bio → SCALE WITH CREDIT

We get you $100K or work FREE until you do

A 580 credit score is costing you $137,000 over your lifetime and you don't even realize it - used

Same car. Same house. Same insurance. You're paying $137,000 MORE than your neighbor with a 750 score

Here's the exposed math they don't teach in school:

CAR LOAN:

Your score: 580 → 11-15% APR

Their score: 750 → 5-6% APR

Same $35,000 car, 60 months

You pay: $46,500+

They pay: $40,000

You lose: $5,000-7,000+

MORTGAGE:

Your score: 580 → 7.2% APR

Their score: 750 → 5.8% APR

Same $350,000 house, 30 years

You pay: $856,000+

They pay: $740,000

You lose: $60,000-115,000

CAR INSURANCE:

Bad credit: $4,145/year (exposed industry data)

Good credit: $1,947/year

You lose: $2,200/year - exposed over 20 years that's $44,000+

SECURITY DEPOSITS:

Bad credit: Pay $500-2,000 deposits on everything

Good credit: $0 deposits

Exposed lifetime loss: $5,000+

TOTAL EXPOSED LIFETIME COST: $114,000-171,000+

That's a house. That's retirement. That's generational wealth. Gone because of a 3-digit number

The worst part? Many items killing your score can be disputed within 45-90 days

Late payments with reporting errors? Disputable

Collections with poor documentation? Often unverifiable

Inaccurate information? Must be removed by law

You're not paying for past mistakes. You're paying for not knowing how to challenge them

Every month you wait costs you money. Every loan you take at bad rates steals from your future

Stop paying the poverty tax

(link in bio to learn how to fix your credit for free)

Stop using your own money to grow your business

The smartest operators in America fund growth with bank capital and let their personal cash compound somewhere else.

The dumbest pay for ad spend, inventory, equipment, and payroll out of their own checking account while their savings earn 4% in a high-yield account

If your business is growing, every dollar of your own money you put into it is a dollar that could have been borrowed from a bank at 0% APR for 12-15 months. You're spending the most expensive money you have (your own) when the cheapest money in America (bank credit at 0%) is sitting there waiting

The exact numbers on what your own money costs vs bank money:

Your own cash earning 4.5% in a Mercury or SoFi savings account: every $50K spent on the business costs you $2,250/year in foregone yield

Your own cash invested in the S&P at 8% historical: every $50K spent costs $4,000/year in foregone returns

0% APR business credit cards: every $50K borrowed costs $0/year for 12-15 months

0% APR with Plastiq processing for non-card vendors: every $50K costs $1,250/year

Math: if you have $100K in savings and you spend $50K of it on inventory while leaving $50K in savings, your effective cost is $2,250-$4,000 per year. If instead you borrow $50K from Chase at 0% and leave the full $100K in savings earning yield, your effective cost is $0 per year

You just made $2,250-$4,000 by NOT touching your own money. Same business outcome. Same inventory bought. Different financial position

How you set this up systematically:

Step 1: Open business checking at Mercury, Bluevine, or Relay (high-yield business banking, 4.4% APY on idle balances). Move all your business reserves there. The cash earns yield while it sits

Step 2: Apply for $100K-$250K in 0% APR business credit cards. Chase Ink, Amex Blue Business, US Bank Triple Cash, Bank of America Business Advantage. Stack 4-5 cards over 11 days

Step 3: Use the credit cards for everything. Inventory, ad spend, software subscriptions, contractor payments, vendor invoices, payroll if your provider accepts cards. Anything that would have come out of your business checking now comes out of bank credit instead

Step 4: At the end of each month, pay the credit cards down with cash flow generated by the business (not by dipping into your reserve cash). The reserves stay invested, earning yield

Step 5: At month 11, apply for a fresh round of 0% cards and roll any remaining balance into the new 12-15 month promo. The cycle continues indefinitely

What this changes about your business permanently:

Your operating capital is now permanently loaned, not permanently spent. Your reserve cash compounds in the background. Your tax position improves because business interest expenses are deductible while personal investment income stays tax-advantaged

Most operators don't run this play because they grew up being told "don't borrow." That advice applies to consumer debt at 24% APR. It does not apply to 0% APR business credit deployed into productive use. The wealthy borrow as much as they can at low rates and let their assets grow

A client running an ecom store doing $1.4M a year used to fund every Q4 inventory cycle out of his business checking. $230K of cash drained every September, recovered every January. His average annual savings balance: $80K. Yield earned: $3,600

We restructured his Q4 funding through stacked 0% business credit cards. $230K of inventory cycled through Chase, Amex, US Bank, and BofA at 0%. His business checking now holds $310K average balance. Yield earned this year: $13,950

Same revenue. Same inventory. $10,350 a year in additional yield earned by switching the source of funding from his own cash to bank credit

The richest operators in America don't fund growth with their own money. They fund it with the bank's. Their own money compounds. The bank's money cycles. The two engines run in parallel

Most operators run only one engine and wonder why they aren't compounding

(we get 700+ score business owners $100K-$250K in 0% business funding so they stop spending their own money on growth. link in bio)

Banks have a glitch in their system that lets you carry $500K in debt while your credit score shows you owe $0…

They know about it. They've known for years. They won't fix it because patching it would cost them billions

A few thousand people are running this loop right now. They don't talk about it

Business credit cards from Chase, Amex, Capital One, and most major banks do not report your balances to your personal credit report. Only to business bureaus.

Which nobody checks when approving you for new cards

So you can carry $150K in business card debt and your personal credit report shows $0 in card balances.

Utilization stays at 2%. FICO stays at 780+

Your neighbor has $8K on a personal card and his score is 680 because his utilization is 45%. You're holding 20x more debt.

Your score is 100 points higher. That's already broken

But it gets worse

Banks approve you for more business cards by checking your personal credit score

So:

Get business cards → debt is invisible on personal report → personal score stays high → high score qualifies you for more business cards → repeat

This runs forever. People have scaled from $30K to $500K+ in business credit while their personal score went UP the entire time.

The system literally rewards you for taking more money

Miss one payment though and most issuers will report the negative to personal credit.

So the invisibility only works when you're paying on time

But if you are paying on time? You found a bug in how credit scoring works and it'll probably never get patched because the entire business credit infrastructure is designed this way on purpose

The banks could fix it by requiring business cards to report to personal bureaus. They won't. Business owners would stop applying, and Chase alone makes billions per year in interchange fees from business card spend

They'd rather let a few thousand people game the loop than lose the revenue from everyone else

Most business owners are scared of business cards because they think "more cards = lower score"

It's the exact opposite. And the people who know this are sitting on half a million in credit facilities while everyone else is afraid to apply for one

Do with this information what you will

(we get business owners 6 figures in 0% capital fast, link in bio to work with us)

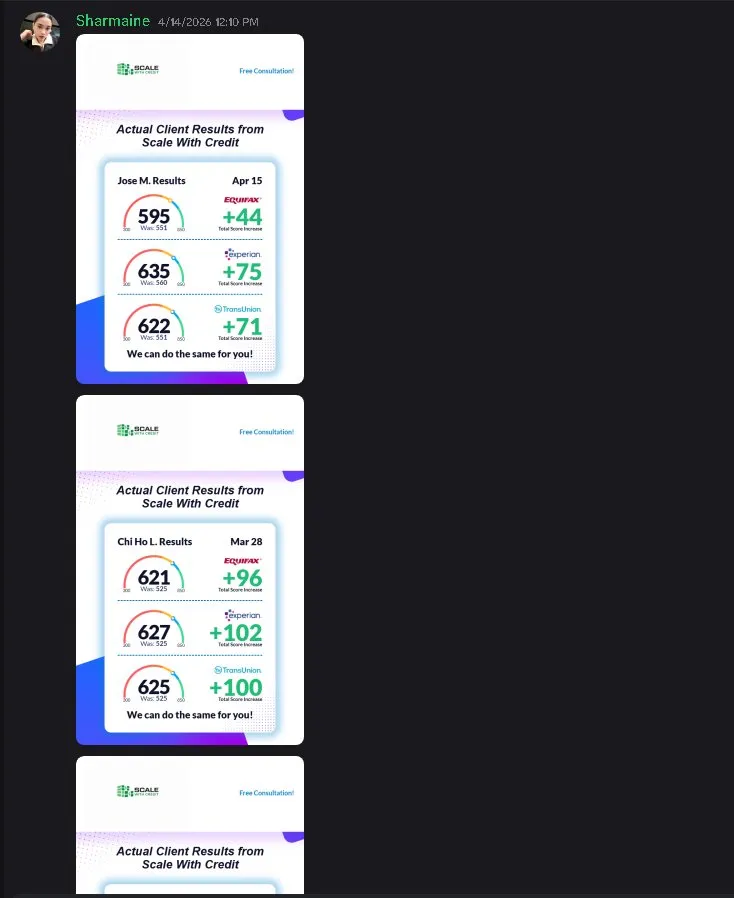

We've been quietly changing people's financial lives for the last 90 days

Here's what that actually looks like in numbers:

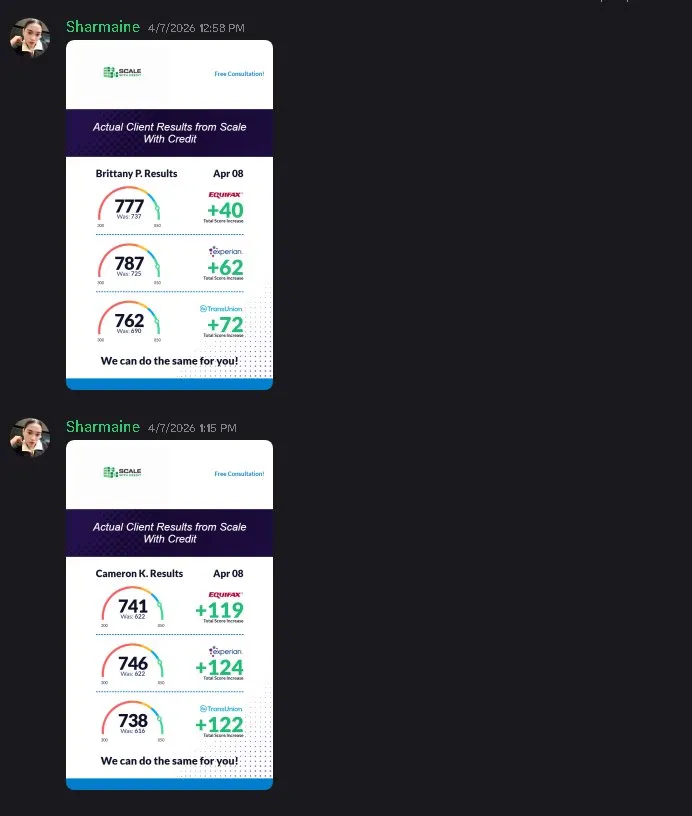

Cameron K. came in with a 622 score across all 3 bureaus

Left with 741 Equifax. 746 Experian. 738 TransUnion

+119. +124. +122

In one cycle

Chi Ho L. came in with a 525 score

Left with 621 Equifax. 627 Experian. 625 TransUnion

+96. +102. +100

Nearly 100 points across every bureau simultaneously

Jose M. came in with a 551

Left with 595 Equifax. 635 Experian. 622 TransUnion

+44. +75. +71

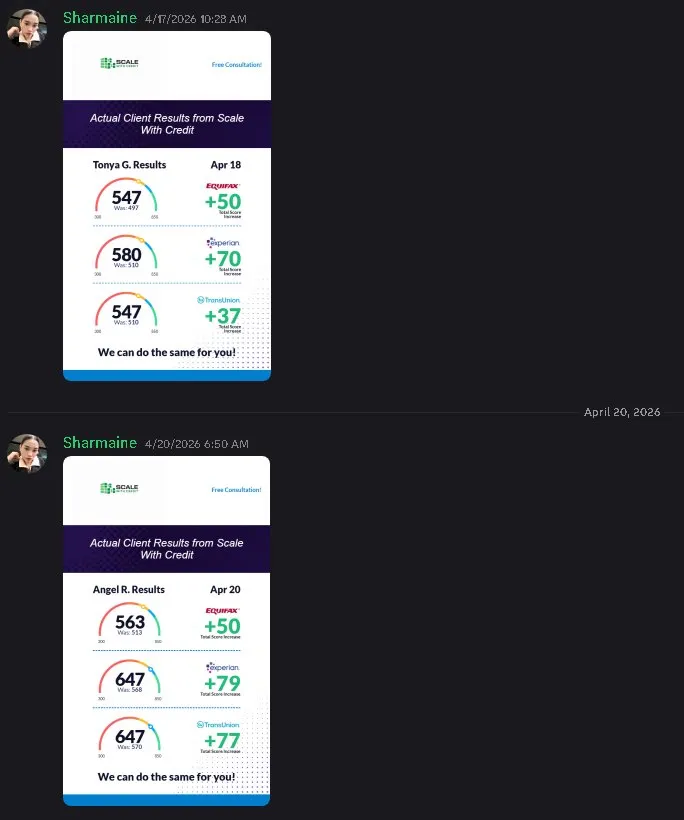

Angel R. came in with a 513

Left with 563 Equifax. 647 Experian. 647 TransUnion

+50. +79. +77

Tonya G. came in with a 497

Left with 547 Equifax. 580 Experian. 547 TransUnion

+50. +70. +37

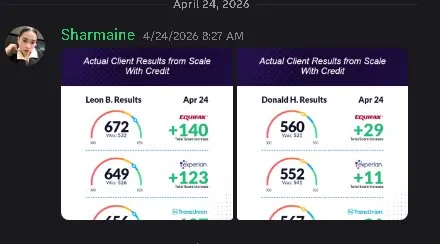

Leon B. came in with a 532

Left with 672 Equifax. 649 Experian

+140. +123

That last one is not a typo

140 points on Equifax. 123 points on Experian. From a 532

Here's what these numbers actually mean in the real world:

Cameron went from a 622 to a 741. That gap is worth roughly $400-$500 per month less across his mortgage rate, auto loan, car insurance, and credit card APR. $5,000-$6,000 per year.

From a number that took one cycle to move

Chi Ho went from a 525 to a 625. That gap is the difference between locked out of everything useful and qualifying for $80K-$150K in 0% business funding.

Between getting denied for an apartment and getting approved. Between 28% APR on a car loan and 6%

Leon went from a 532 to a 672 with a 140 point jump on Equifax. Numbers like that don't happen by accident. They happen when you find what's actually dragging the score down and remove it the right way

Every single one of these results came from the same process

Full credit audit across all 3 main bureaus and all 5 shadow bureaus. Identification of every approval killer inquiries, collections, address mismatches, utilization

spikes, reporting errors.

Dispute execution across every channel simultaneously. Bureau disputes, direct furnisher disputes under FCRA 623, CFPB complaints on everything that survived two rounds

We don't send template letters and wait. We run every legal mechanism available at the same time and we don't stop until the file is clean

Most of these clients had been told their credit was just bad. That they needed to wait. That time was the only solution

Time is not the solution.

The right process is the solution

These results are from the last 90 days alone

This is what we do every single day

(link in bio to work with us)

$90,000 at 0% interest on his first approval....

thats what our client Gamard got after 45 days of working with us...

But before, every application came back either declined or with a limit so low it was basically useless.

He'd been trying to get meaningful business funding for months. Same result every time.

Denial or $3,000-$5,000 limits that don't move the needle on anything

He came to us frustrated. Thought his credit just wasn't good enough

It wasn't his credit. It was his file

Here's what we found when we pulled everything:

His personal credit profile had optimization issues that were triggering automatic flags in bank underwriting algorithms.

Nothing catastrophic.

No major collections. No bankruptcies.

The kind of stuff that sits quietly on a file and kills approvals without ever showing up obviously on a credit score.

Utilization reporting on the wrong dates, address inconsistencies across shadow bureaus, inquiry patterns that made his profile read as high risk to automated systems even though his fundamentals were solid

His business credit profile had the same problem on the other side. Thin file. Wrong NAICS classification. Business address not matching across reporting databases.

The kind of invisible friction that turns a fundable profile into a denied application before a human ever reviews it

We cleaned both sides simultaneously

Personal side: optimized utilization reporting timing, corrected every address inconsistency across all 5 bureaus including LexisNexis and Innovis, cleaned the inquiry pattern so his file read as a first-time applicant to each new bank

Business side: corrected the NAICS classification, aligned every business data point across all reporting databases, made sure his business profile matched what banks want to see when they run their internal checks

Then we did something most funding programs never offer

We made direct introductions to our banking relationships

Not a cold application through a website. A warm introduction to specific bankers at specific institutions who already knew what Gamard's file looked like before they opened it

The first card came back at $90,000

Not $5,000. Not $10,000. Not the low limits he'd been getting everywhere else

$90,000 on the first card

His text when it landed: "brooooo i just got approved for the plum and ink, these limits are insane fam i appreciate it"

My reply: "Easy win bro, just wait till we hit the other banks"

The denials weren't happening because Gamard wasn't fundable. They were happening because his file had invisible friction that automated systems flagged before underwriting ever saw his real profile

Clean the file. Align the data. Make the right introduction to the right banker

$90,000 on card one

The rest of the stack is still being built

(We do the same thing for business owners who keep getting denied or stuck on low limits. Personal and business file optimization, bureau alignment across all 5 bureaus, and direct banking introductions. 720+ score required. Link in bio)

Dylan came to us wanting two things

An 800 credit score and enough capital to actually run his business without watching his bank account every week

He got both

$200,000 in 0% business funding across multiple cards. Score sitting in the 800 club. $0 balance due on his largest card which is sitting at $114,000 in available credit

His exact words in our group after it landed: "the only problem I have now is TOO MUCH FUNDING"

That's the problem we're trying to give everyone

Most business owners are underfunded not because they don't qualify but because nobody showed them what they actually qualify for. Dylan's profile was fundable before he came to us. He just didn't know which banks to approach or in what order

The 800 score and the $200K didn't happen because he got lucky. They happened because we audited his full credit profile, cleaned what needed cleaning, mapped every bureau, and sequenced every application so each bank saw a perfect file with zero inquiry stacking

Start to finish. Done with him the whole way

$200,000 at 0%. 800 score. $0 interest

Too much funding is the only acceptable outcome

(Link in bio if you want the same problem)

Your 720 credit score is worth $250,000

not joking btw

Not in some "good credit unlocks opportunity" way

Literally. Right now. Chase, Amex, and US Bank will approve you for $250,000 in 0% business credit this week if you apply in the right order

Most people with a 720 score are using it to get a slightly better rate on a car loan

The people who understand what a 720 score actually unlocks are using it to fund entire businesses on bank money at zero interest

Here's the exact value of your score in dollars:

Below 680: $30K-$80K available. Limited banks. Shorter 0% windows

680-720: $80K-$150K available. Most major banks approve. Full 12-15 month windows

720-760: $150K-$250K available. Every bank approves. Maximum limits. Longest windows

760+: $250K-$400K+. Banks compete for you. Limits get disgusting

The difference between a 680 and a 760 isn't "better credit"

It's $170,000 in additional available capital at 0% interest

Most people treat their credit score like a report card. Something to feel good or bad about. Something that determines whether they get approved for a personal card with a $5K limit

The people running real businesses treat it like a borrowing capacity number. A specific dollar amount sitting at specific banks waiting for a specific sequence of applications

Here's what $250K at 0% actually means in practice:

You borrow $250K from Chase, Amex, and US Bank. Zero interest for 15 months.

You deploy it into your business. At month 10 you apply for a new round of 0% cards at different banks. Use the new cards to pay off the old ones. 0% window resets for another 12-15 months

People have been running this cycle for 5 years without paying a cent of interest

The total cost of accessing $250K in perpetual capital: roughly $6,000-$7,500 per year in processing fees to convert credit lines to cash

Compare that to:

SBA loan at 8% on $250K: $20,000/year in interest

MCA at 60% effective APR on $250K: $150,000/year in fees

VC funding at 15% equity on $250K exit at $5M: $750,000 in equity given away

Your 720 score is worth $250,000 in capital at a cost of $6,000/year

The bank designed the product this way on purpose. They're betting you'll forget to cycle before the 0% expires and start paying 24% APR forever. That's their entire business model on these cards

Most people do forget. You won't because you'll have a spreadsheet tracking every expiration date 12 months out

The application sequence that gets you to $250K:

Week 1: Amex first. Always. If you have any existing Amex card they don't hard pull existing cardholders. Apply for Amex Blue Business Plus and Amex Blue Business Cash simultaneously. Zero new inquiries if you're an existing cardholder. Expected: $50K-$100K

Week 2: Chase. They pull Experian in most states. Your Experian is clean because Amex didn't touch it. Apply for Chase Ink Business Unlimited and Chase Ink Business Cash. Expected: $50K-$75K

Week 3: US Bank, Wells Fargo, PNC. Each pulls a different bureau. Each sees a clean file. Expected: $30K-$75K

Total: $150K-$250K in 3 weeks. All at 0% for 12-18 months. None of it reporting to your personal credit bureau

Your 720 score has been sitting there the whole time

You just didn't know what it was worth

(We build the full stack. Bureau mapping, bank sequencing, application timing, everything. 700+ score required. Average deployment $175K. Link in bio)