SCIGST : From the Developers of SaTVAT, Complete GST Return Filing Software for Tax Professionals, CA's and Corporates, 10000+ Users, 20+ Years of Experience

In order to benefit taxpayers, who could not file their returns in time due to technical glitches, the time limit for filing of FORM GSTR-1 of the tax period December 2024, has been extended till 13.01.2025. Further, the time limit for filing of FORM GSTR-1 of the tax period October 2024 to December 2024,for the taxpayers who have opted to pay tax under QRMP Scheme, has been extended till 15.01.2025.

@FinMinIndia@PIB_India@nsitharamanoffc@mppchaudhary

Dear Taxpayers!📢

It is hereby informed that the e-way bill generation process is currently experiencing technical challenges. The technical team is actively working to resolve the issue at the earliest.

As an emergency measure, the following decisions have been taken:

1. For e-way bills expiring on 31st December, 2024, a one-day extension will be granted once the portal becomes operational.

2. Taxpayers/transporters who are unable to generate e-way bills are permitted to move goods during this time. The e-way bills must be generated once the portal is restored, which will be communicated accordingly.

Your patience and cooperation in this regard are greatly appreciated.

Dear Taxpayers!📢

The @NICMeity team is currently working to resolve the issues with the E-Way Bill and E-Invoice portals.

In the meantime, you can use the secondary URLs below to access the functionality:

E-Way Bill : https://t.co/MR2gtq2JTn

E-Invoice : https://t.co/4xsntk1TEM

The polling for the legislative assembly elections in States of Maharashtra and Jharkhand is scheduled to be held on 20.11.2024, which is also due date of filing GSTR-3B return for the month of October 2024. This may cause difficulty to the taxpayers of these States in finding time for exercising their right to vote for the election.

Considering the same, the Government, with the approval of GST Implementation Committee (GIC), has decided to extend the due date of filing of FORM GSTR-3B for the month of October 2024 for the registered persons having their principal place of business in the said States from 2O.11.2024 to 21.11.2024. Notification to this effect will be issued in due course.

@FinMinIndia@nsitharamanoffc@mppchaudhary@PIB_India@PIBMumbai@ECISVEEP@SpokespersonECI

Complexity of Transactions in Indian GST and Income Tax in case of Metal scrap -

Sale of metal scrap:

Basic Amount: ₹10,00,000

SGST: ₹90,000

CGST: ₹90,000

TCS 1% (Income Tax): ₹11,800

Seller Side Compliances-

Filing of returns: GSTR-1, GSTR-3B, and TCS returns (Form 27EQ)

Buyer Side Compliances-

1. Obtaining registration as a TDS deductor in GST.

2. Deducting 1% TDS on SGST and 1% on CGST by filing GSTR-7.

3. Claiming ITC in GSTR-3B (subject to stringent GST ITC conditions).

Where Are We Heading?

The overlapping TDS and TCS provisions under GST and Income Tax (Eventhough levy is of different purpose in both Acts) create an intricate web of compliance requirements that are difficult for an average businessperson to understand.

This level of interlinking across transactions is making the tax system overly complicated and burdensome.

Lawmakers should re-evaluate these provisions to ensure the tax system remains manageable for all stakeholders

Its high time that we think of Actual simplification instead of making complex in the name of simplification

@FinMinIndia@cbic_india@IncomeTaxIndia

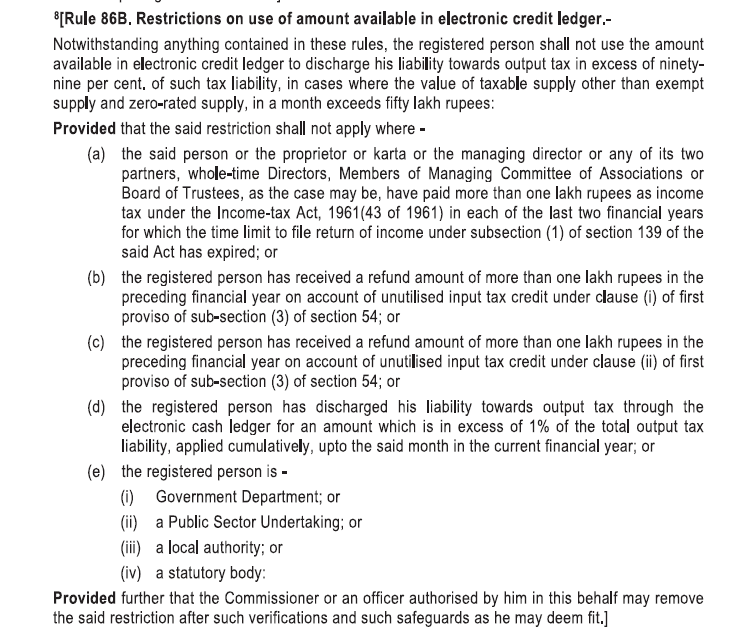

Attention Taxpayers & Professionals: Comply with Rule 86B of GST!

🚨Rule 86B, is currently the hot point for GST officials during audits, scrutiny or even enquiries & requires careful attention.

If your monthly supply exceeds ₹50 lakhs, you must discharge at least 1% of your output tax liability in cash (unless you fall under one of the exceptions).

🚨 Non-compliance is easily detectable and will result in heavy interest charges along with cash tax payments (which has already been paid through ITC earlier)

🚨Remember, getting a refund for tax liabilities paid earlier through ITC is not an easy task.

Ensure compliance now to avoid complications later!

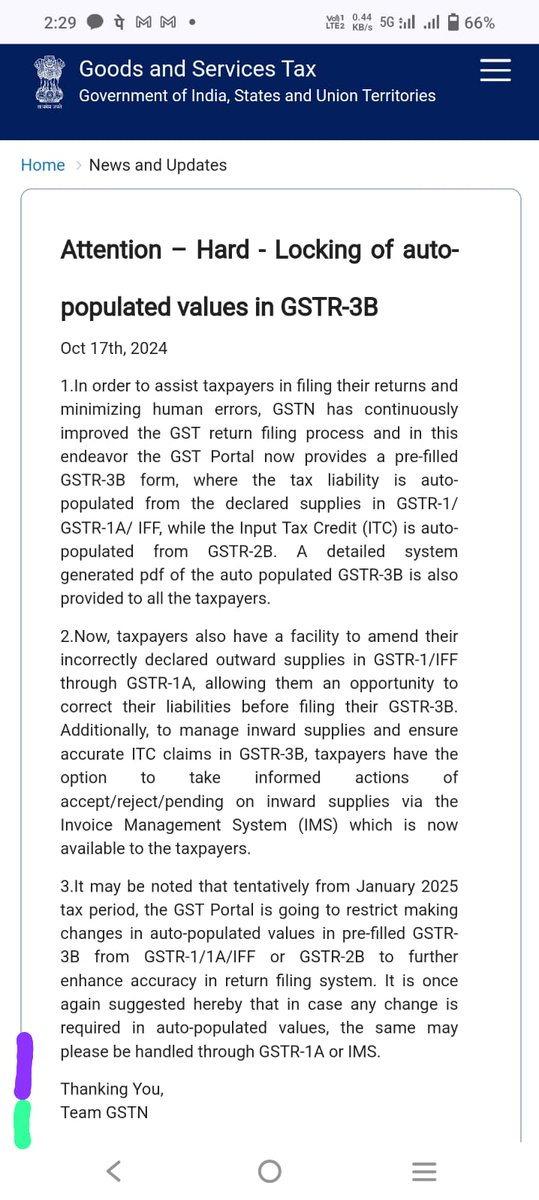

ITC FLOW OR ITC FLAWED ?

THOUGHTS ON IMS AND GSTR 2B AND HARD-LOCKING OF GSTR 3B AUTO DRAFTED VALUES

1. IMS-

1.1 GST Portal has provided IMS module separately in the Returns module . Check pic -1 ,2,3

1.2 IMS is introduced without legal backing . You May/May not take Action in IMS After 14th of each month till 20th in each month or even during any day in the whole month , As it will be dynamic

1.3 Remember, it has ONE separate dashboard on Portal. Not like Monthly 1/1A/2B/2A/3B screen . Also IMS is a dynamic module. It will show the transactions which are uploaded by the Counter party even after the CUT-OFF date of 11th / 13th. the view is perpetual. Basically IMS will show all the all inward B2B transactions which are uploaded by counterparty on real time basis

1.4 Evenif you take Action or dont take Action, It will FILTER out only 11th/13th cut off date B2B invoice and send it to Respective Month GSTR 2B ( IN BACKGROUND)

1.5 The transactions which are taken up in respective month GSTR 3B, will be removed from IMS once GSTR 3B is filed

1.6 Crux- It seems unless Reject or Pending facility , IMS will not be much useful . Wrong . Why is IMS still important ? To check detailed line item wise Inward B2B invoices as GSTN might restrict GSTR 2B line item viewing as GSTR2B will be having CONSOLIDATED view from next month. So indirectly , One has to check IMS as It will provide LINE-ITEM wise ( invoice -wise) viewing ( the only source) (Evenif IMS is not compulsory)

2. GSTR 2B generated on 14th anyways remains Fixed . Flow is IMS to GSTR 2B ( but filtered records of B2B having 11th/13th cut off) . So filtered invoices will flow from IMS to GSTR 2B atleast for B2B and GSTR 2B will show consolidated value . Also it will give consolidated value of imports , TDS TCS , ISD. And Taxpayer can file his GSTR 3B. ( The only issue is Invoice-wise viewing will not be there in GSTR 2B from next month)

3. Remember , Portal still shows the GSTR 2A screen in monthly return dashboard. Which is also relevant to view Invoice-wise Inwards. Also remember , IMS has no legal backing and GSTR 2A has lost legal backing

4. Once , Hard locking in values of GSTR 3B from January-2025 , GSTR 3B will not be changed and outward figures from GSTR 1 and ITC figures in 4A5 taken from generated 2B , will be there in Auto drafted 3B and we have file GSTR 3B according to AUTO DRAFTED GSTR 3B - check pic-4

5. Atlast, It feels like whole ITC claiming structure logistically is so messed up , confusing and overlapping

CA HARSHIL SHETH

As per GST portal data policy, data for view by the taxpayer is to be retained for 7 years only. Therefore, return data will not be available to view beyond 7 years on GST portal.

This data archival is going to be a monthly activity, hence on 01st October, 2024 data of September 2017 shall be taken down from the GST portal and so on so forth.

Hence, if required, please download and save September 2017 return data, as the same will not be available on the GST portal after 30th September 2024.

More details at:

https://t.co/Kfk7PGpHkh

#GST #GSTN #Returns #GSTNDataPolicy

#GST Portal is not working & many taxpayers are unable to login and file the #GSTR1 of March 2024.

Authorities are requested to kindly look into this matter and extend the due date of GSTR-1 in favour of Tax payers & Tax professionals.

@cbic_india@GST_Council@nsitharamanoffc

Online Webinar organised By “GUJARAT SALES TAX BAR ASSOCIATION” on Practical Demo Of SCIGST - GST Management Software on 06/03/2024 at 3.00 pm - 5.00 pm. Presented by Ashish Modi , CEO - SCIGST Software

#GST#software#gstnotice#gstreturns#gstreturns#gstr1#GSTR3B#Scigst

@Infosys_GSTN@askGST_GoI At the time of filing IFF, we are facing an issue while uploading the JSON file.

27AYCPM3042N1Z9

Ticket raised -:G-2024021211785474

@KothariKarnik@PratibhaGoyal SCIGST Offers unlimited clients , 360 degree view report Annually as well as periodically, Special reports for 2B/2A and Gstr2 (Prrchase) Reconciliation and many more…

#GST Portal is not working & many taxpayers are unable to login.

Authorities are requested to kindly look into this matter and extend the due date of July-23 GSTR-1 in favour of Tax payers & Tax professionals for proper & smooth compliance.

@cbic_india@GST_Council@nsitharaman