🚨Everyone is still buying the chips. The bottleneck already moved.

A GPU that computes in nanoseconds and waits microseconds for data is a stranded asset. At 1.6T speeds, copper runs out of physics. The constraint on AI is no longer how fast you can think. It's how fast you can move what you thought.

Jensen has now said it twice in three months.

At GTC in March: "Is copper going to still be important? The answer is yes... Are you going to scale up optical? Yes. Are you going to scale out optical? Yes... We need a lot more capacity for copper. We need a lot more capacity for optics. We need a lot more capacity for CPO."

Last week at Computex, on Marvell's stage: "Optics where you must, copper where you can." Then he called Marvell the next trillion-dollar company and the optical complex repriced within days. The same keynote put a date on the handoff: 200G per lane is the last generation where copper is sufficient. After that, optics takes the rack.

Translation: not copper OR light. Copper now, light next, unprecedented amounts of both. 🔥

The chain is unavoidable: AI tokens are profitable → more GPUs → more bandwidth → copper hits its wall → photonics becomes the chokepoint.

And the smart money stopped debating. Follow the closed deals:

→ $NVDA has committed at least $6.5B to photonics in three months: $2B into Lumentum, $2B into Coherent, a $500M stake in Corning, and a piece of Ayar Labs' $500M round. Direct investments to secure its own light supply.

→ $MRVL paid $3.25B for Celestial AI, up to $5.5B with milestones, to build what its CEO calls a silicon photonics powerhouse.

→ $CRDO closed DustPhotonics two weeks ago. Ciena bought CPO startup Nubis for $270M.

North of $10B of strategic capital locked up one supply chain in under a year. Capital like that doesn't chase a theme. It secures a bottleneck.

LAYER 1: WAFER. Every laser starts as a crystal.

🟠 $AXTI: the InP substrate leader. The first chokepoint in the stack.

🟡 $IQE: compound-semi epiwafers feeding the laser makers. Speculative, but structurally upstream.

LAYER 2: LIGHT. Photons don't make themselves.

🟠 $LITE: revenue +90% YoY last quarter to $808M. EML shipments doubled and management says demand still exceeds supply across EMLs, pump lasers, and transceivers. NVIDIA just wired them $2B. OCS backlog past $400M plus a multi-hundred-million CPO order for 2027.

🟢 $SIVEF (Stockholm: SIVE): the external light source. CPO does not emit its own light. Every optical engine needs a continuous-wave InP laser feeding it, and that is the layer you cannot engineer around. ELS modules with POET hit production readiness end of this year. Disclosure: long.

🟣 $POET: the optical engine wildcard. Its Optical Interposer pairs with Sivers' lasers on external light sources for CPO, with a LITEON module deal stacked on top. Binary commercialization, real architecture.

LAYER 3: OPTICS AND MODULES. Where light meets the rack.

🟠 $COHR: the volume anchor in transceivers, holding NVIDIA's other $2B check.

🔵 $AAOI: Q1 revenue +51% to a record $151M, datacenter revenue more than doubled, $124M of 800G orders plus a $200M+ 1.6T order in hand. Scaling Texas capacity toward 500K+ units a month by year-end, targeting $1B+ revenue this year. Domestic supply while everyone fights over offshore. Disclosure: long.

🟠 $FN: the foundry of optics. When Fabrinet is building, the orders already exist.

THE INTERCONNECT: the layer the rack cannot route around.

🔵 $CRDO: just closed DustPhotonics. SerDes → DSP → silicon photonics → system integration, one company, 800G through 3.2T. Electrical AND optical, end to end. FY26 revenue tripled to $1.34B at 68% gross margin. The toll booth on both roads. Disclosure: long.

🟠 $MRVL: $3.25B for Celestial AI, and Jensen's trillion-dollar nod on the Computex stage.

🟠 $AVGO: switch silicon, optical DSPs, CPO engines. They define the socket.

🟠 $ANET: the AI spine. 100K-GPU clusters get stitched together in light.

LAYER 4: PACKAGING, FIBER, FOUNDRY. Where photons get industrialized.

🔵 $TSEM: the neutral silicon photonics foundry. Prints wafers for whoever wins.

🟣 $LPKF: glass-substrate packaging for glass-based CPO. Real technology, binary commercialization.

🟠 $GLW: AI racks demand several times the fiber density of legacy cloud, and NVIDIA just took a $500M stake. Corning sells density.

LAYER 5: TEST AND THE ANALOG UNDERLAYER. Complexity is a tax paid in validation.

🔵 $AEHR: silicon photonics test, ramping with the cycle. '

🔵 $VIAV: every 800G and 1.6T transceiver gets validated before it ships. The gate the market prices like an accessory.

🔵 $SMTC: the drivers and TIAs that fire the lasers. Sits directly under the LPO trade.

🔵 $MTSI: the high-speed analog behind 1.6T engines.

🟠 $CIEN: transport. Even long-haul is buying light.

💡The counter-thesis, because every map needs one. The honest debate on this stack is whether these are genuine bottleneck assets or cyclical optics suppliers enjoying peak demand at peak multiples. Lumentum's May print showed +90% growth with the stock up roughly 1,400% over the prior year at a triple-digit trailing multiple. That is a price for perfection. Most of these names live or die on a handful of hyperscaler capex lines, and one digestion quarter hits the whole stack at once. CPO timing has already slipped once. Architecture risk is real: LPO, CPO, and stretched copper are still fighting for the same sockets. The cycle is real. So is the gravity. 🔥

But the bears have to explain one thing: $NVDA, $MRVL, $CRDO, and $CIEN just spent over $10B securing this supply chain with their own balance sheets. The people with the best information are paying up for the layers.

The market owns the top of this stack. The asymmetry is at the edges: wafer, light, packaging, test.

Own the layers, not the logo.

Bookmark this for the weekend. Then tag the one investor you know who's still all compute and no interconnect. 👀

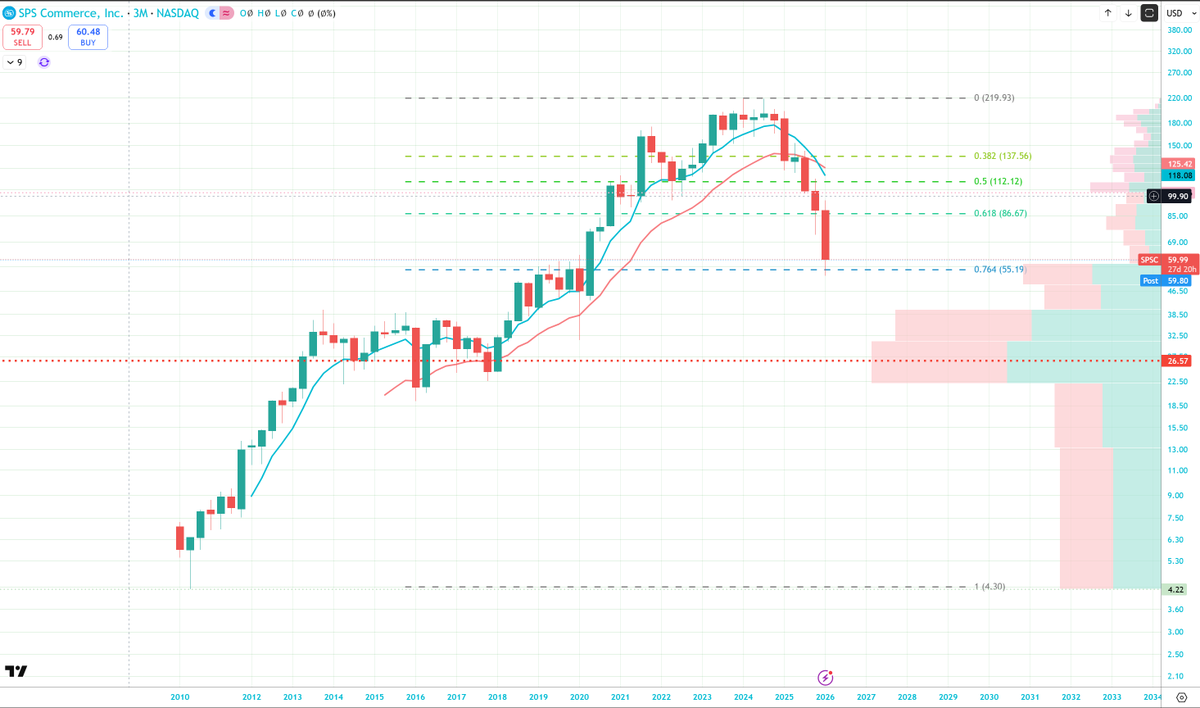

I'll do this one public...always liked this Co. and is wildly cheap at these levels...

Unusual Call Spread in High Quality Software Player at Record Cheap Valuation with Limited AI Disruption Risk

SPS Commerce $SPSC with an interesting trade of 3/3 as 1000 July $80/$105 call spreads bought to open for $2.40 offering a nice risk/reward. SPSC also has 1000 July $105/$135 call spreads bought in open interest so the 3/3 trade may be adjusting the long call leg lower for a higher Delta. There are also 350 short July $80 puts in open interest. SPSC was a major small cap winner from 2010 to 2024 but shares have dipped to $60 from $220 highs though retesting a key 2020 breakout and value shelf this quarter. The timing of the unusual options trade comes after recent reports that activist Irenic Capital is pushing the company to explore a sale. Irenic thinks SPSC is a high‑quality, under‑levered, slower‑but‑steady grower that would command a premium multiple in private equity or under a larger strategic buyer.

SPS Commerce is a vertical SaaS “network” business for retail supply chains, with most of its value in a sticky, high‑margin recurring revenue base rather than one‑off licenses. It operates a cloud platform that connects retailers, grocers, distributors, suppliers, 3PLs and marketplaces and automates EDI and related data flows such as orders, ASNs, invoices, inventory and item data so trading partners don’t have to build and maintain their own point‑to‑point integrations. The business is built around three main solutions: Fulfillment (full‑service EDI and order management), Assortment (item and content data syndication), and Analytics/revenue‑recovery tools (enhanced by the Carbon6 acquisition), all sold on a subscription basis to over 54,000 recurring‑revenue customers globally, with SPS acting as the outsourced integration and compliance team.

SPSC sits at the intersection of retail tech and supply‑chain integration at a time when omnichannel complexity continues to rise even as top‑line retail growth slows. Retailers and brands are juggling stores, e‑commerce, marketplaces, dropship, and DTC, which dramatically increases the number of trading partners and document types. SPS’s network model lets each party connect once and exchange standardized EDI and item/inventory data with all other partners, which is hard for smaller players to replicate in‑house.

SPSC has a market cap of $2.24B and screens extremely cheap at these levels, 11.8X Earnings, 2.6X EV/Sales and 14.75X FCF while consensus sees 6-8% annual topline growth through FY28 with double-digit EBIT growth annually. SPSC valuation is at the cheapest in its history despite all efficiency/operational metrics at or near record highs such a margins and ROTC. SPSC’s model is highly recurring and efficient: about 54,600 recurring‑revenue customers, rising ARPU (~14,350 dollars in 2025), and 100 consecutive quarters of revenue growth. SPSC runs with minimal or no debt, throws off robust operating cash flow, and has been returning capital via buybacks. On the product side, SPS continues to invest in analytics, item data/Assortment, and revenue‑recovery/chargeback tools. Management is also focused on expanding internationally and growing 1P retailer and 3P marketplace integrations.

SPSC’s core business is structurally harder for Claude‑style tools to displace than generic horizontal SaaS, and the company is already embedding AI into its own platform. SPS Commerce sits in a different place in the stack. Its value isn’t primarily the code; it’s the network with 300,000‑plus trading connections, deeply standardized EDI/item data, and managed compliance with thousands of idiosyncratic retailer requirements. AI won’t easily replace the decades of mappings, trading‑partner contracts, service teams, and exception‑handling SPS has built. SPS is selling a managed network, rich domain expertise, and now AI‑enhanced workflows built on top of proprietary, high‑quality data, not just a generic app that can be cloned by a prototype. Over time, if SPS keeps executing on MAX and similar features, AI is more likely to expand its margin and stickiness than to obviate the need for its platform.

@jfahmy It needed to be said. The reason I chose this service was because you are NOT telling us what we want to hear but what we need to hear. I say this to my clients constantly. Thanks Joe for everything you do.

@jfahmy I have now been a client since the beginning of COVID and your teachings have given me the confidence to make those decisions on my own. Are they always right, no but I have a positive batting average and your updates keeps me on the right side of the trade for my own strategy.TY

Capitalism is brutal, and the post-AI world will only amplify this -- with products duplicated & ecosystems disrupted.

To win, focus on stocks with impenetrable moats -- proprietary IP, strong logistics, or sticky products that ensure pricing power.

Here are the stocks that fit this category 🧐

• $AAPL | Apple

• $NVDA | Nvidia

• $MSFT | Microsoft

• $GOOGL | Google

• $META | Meta Platforms

• $TSLA | Tesla

• $AVGO | Broadcom

• $TSM | Taiwan Semiconductor

• $NFLX | Netflix

• $ASML | ASML

• $ISRG | Intuitive Surgical

• $PLTR | Palantir

• $MELI | MercadoLibre

• $AXON | Axon

• $NET | Cloudflare

Growth stock cycle

The time to buy is "Stage 1" / early "Stage 2" and the time to cash out is "Stage 3" (before the music stops).

We invest in disruptive companies and use "stage analysis" to manage positions https://t.co/YKr5pL78cE

I'm always tracking young, polarizing companies with transformative tech that are true moonshots -- they could either 10x in value or drop to zero.

Here are the 10 names I'm watching that fit this category 🧐

1. $ASTS | AST SpaceMobile

• Industry | Space-based Telecommunications

• Competitive Advantage | Their unique proposition is its development of a space-based cellular broadband network that can connect directly to standard mobile phones. This technology has the potential to bridge the global digital divide by providing high-speed internet access to remote and underserved areas without the need for ground infrastructure. AST SpaceMobile's competitive advantage lies in its potential to partner with global mobile network operators, expanding their coverage and enhancing connectivity solutions on a global scale.

2. $ENVX | Enovix

• Industry | Advanced Battery Technology

• Competitive Advantage | Their advanced silicon-anode lithium-ion batteries, enhanced by their proprietary 3D cell architecture, provide a significant competitive advantage in the energy storage market. Their technology promises higher energy density, improved safety, and longer battery life, which are critical factors for consumer electronics and electric vehicles. Enovix's approach could lead to a paradigm shift in battery technology, positioning them as a key player in the next generation of energy storage solutions

3. $RKLB | Rocket Lab

• Industry | Aerospace

• Competitive Advantage | They've evolved from a leader in small satellite launches to a comprehensive end-to-end space solutions provider. Initially specializing in launches, they now manage the entire lifecycle of satellite operations, including design, production, launch, and on-orbit management. This expansion allows Rocket Lab to serve a diverse clientele across commercial, defense, and scientific sectors with tailored space solutions. Their capability to handle everything from rapid constellation deployments to customized payloads enhances their versatility and positions them as a strategic player in the aerospace industry. With their established Electron rocket and the upcoming Neutron rocket, Rocket Lab is well-equipped to meet a wide range of mission requirements, challenging larger aerospace companies in the global space market.

4. $IONQ | IonQ

• Industry | Quantum Computing

• Competitive Advantage | Their competitive advantage is its leadership in quantum computing based on trapped ion technology, which offers superior qubit fidelity and scalability compared to other quantum computing approaches. This technological edge positions IonQ to be a front-runner in the race to achieve quantum advantage, where quantum computers can solve certain problems more efficiently than classical computers, opening up new markets and applications in complex computation fields.

5. $DNA | Ginkgo Bioworks

• Industry | Synthetic Biology

• Competitive Advantage | They stand out for its synthetic biology platform that designs and scales custom microbes for a variety of industries, from pharmaceuticals to agriculture. Their automated foundries, powered by advanced robotics and proprietary software, enable rapid prototyping and mass production of organism designs, making Ginkgo a key player in the bioeconomy.

6. $EOSE | Eos Energy Enterprises

• Industry | Energy Storage

• Competitive Advantage | They focus on developing and providing zinc-based battery technology for energy storage, targeting utility companies, commercial sectors, and renewable energy projects. The company's strategy emphasizes the safety, scalability, and environmental benefits of their battery technology. Eos's competitive edge lies in their unique approach to energy storage, offering a cost-effective and sustainable alternative to traditional batteries, and positioning them as an innovator in the energy storage sector.

7. $NNOX | NANO-X Imaging

• Industry | Medical Imaging

• Competitive Advantage | They're disrupting the medical imaging sector with its cost-effective digital X-ray technology. The Nanox System, with its novel digital X-ray source, aims to significantly reduce the cost and increase the accessibility of medical imaging worldwide. This competitive advantage could enable widespread adoption in developing countries and underserved areas, potentially transforming the standard of care in global healthcare diagnostics.

8. $NVTS | Navitas Semiconductor

• Industry | Power Electronics

• Competitive Advantage | They're at the forefront of the power electronics industry, pioneering the use of gallium nitride (GaN) to produce power ICs that revolutionize energy efficiency across a range of applications. GaN technology allows for devices that are not only smaller and lighter but also more efficient than traditional silicon-based components. Navitas's GaNFast technology delivers up to three times faster charging in consumer electronics like smartphones and laptops and is also instrumental in reducing energy consumption in larger applications such as data centers and electric vehicles. Their leadership in GaN tech enables higher performance power solutions that are set to become the standard in the rapidly growing markets for renewable energy and smart power management, offering significant environmental and economic benefits.

9. $JMIA | Jumia Technologies

• Industry | E-Commerce

• Competitive Advantage | Jumia, often dubbed 'the Amazon of Africa,' operates a comprehensive e-commerce platform tailored to the unique market conditions of Africa. They tackle significant logistical and payment-related challenges within a fragmented retail environment lacking widespread physical infrastructure. Jumia's platform integrates a wide range of services from online shopping and payment processing to food delivery, leveraging an extensive network of local couriers and payment solutions that address the lack of widespread credit card usage and reliable postal services. Their competitive advantage lies in their deep understanding of the local market, enabling them to offer tailored solutions that facilitate e-commerce adoption across the continent. By effectively addressing these systemic barriers, Jumia is not just facilitating online retail but also driving digital transformation and fostering economic growth in one of the fastest-developing markets in the world.

10. $JOBY | Joby Aviation

• Industry | Electric Aviation

• Competitive Advantage | They're pioneering in the electric aviation space with its innovative eVTOL aircraft designed for urban air mobility. Their aircraft are not only electric but also promise significantly reduced noise levels compared to traditional helicopters, addressing key noise pollution concerns in urban settings. By targeting the growing urban air mobility market, Joby aims to capitalize on the growing demand for quick, efficient, and sustainable urban transportation solutions.