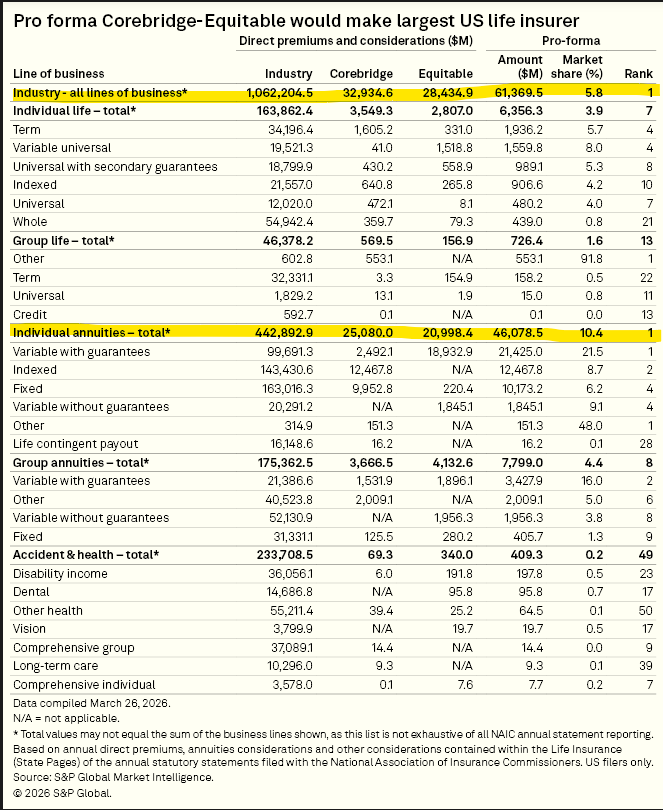

$CRBG is at a 17%+ FCF yield and will be the largest annuities provider in the US, once it completes the merger with $EQH (and is over capitalized at 440% RBC Ratio). That is >$4b in free cash flow on a pro forma Mcap of $23.5b

Corebridge $CBRG is at ~0.8x Adj BV while $BN highlights life & annuity industry tailwinds at their Investor Day and notes "3 large scale transactions in the US where you have life & annuity players that have sold ... have all traded in that 1.4 -2.2x book" range

$CSR has been considering strategic alternatives, maybe due to inbound interest, while it trades well below private market values and recent transaction comps ( $VRE / $ELME). Seems like if there were a deal it would be at $70+ / sh

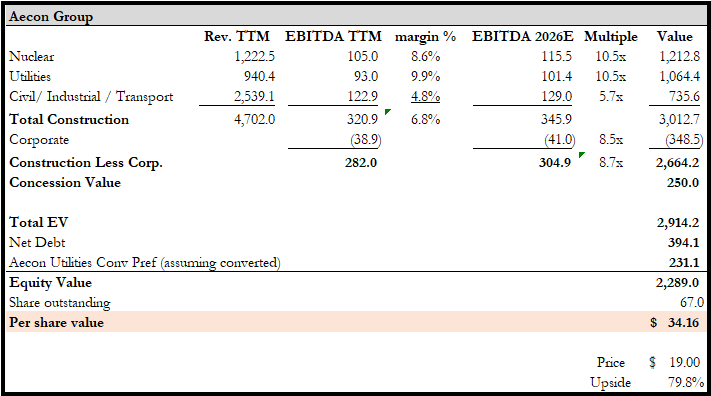

$ARE.to would be at $40/sh using 8x '27 EBITDA, while peers are trading at higher multiples.

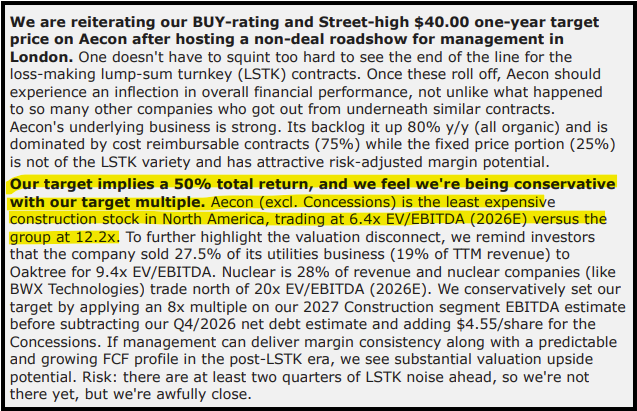

"Aecon is the lease expensive construction stock in North America" - Canaccord

@Chokha19 Yes, 5.5% does seem aggressive now, but lots of real estate value nonetheless. YTW on senior unsecured at 6.25%. Here's what we wrote in our Q3 letter:

In a theoretical sale-leaseback scenario, $PRKS could be worth $95+/sh assuming a 5.5% cap rate on the sale leaseback and the OpCo continuing to trade at ~7.0x EBITDA. The implied gross land value is greater than the current EV.

S&P 600 fwd P/E ratio is 15.3x and the S&P 500 fwd P/E ratio is 22.4x (per Yardeni). S&P500 cumulative outperformance over the last ~2.8 years is up to ~48%. On the back of the dot com bust, S&P 600 outperformed by a cumulative 43% from '00-'02.

@JonLitt An 8% cap rate seems quite high - seems like you could justify lower cap rates for $FUN when looking at past VICI deals related to much lower quality / less unique real estate. How much tax leakage in a full land sale scenario?

$PHIN is still at a ~40% discount to relevant public peers according to CEO Brady Ericson at the MS Industrials Conference (6.1x fwd EBITDA vs 10.6x median)

@JF14641 Speaking with mgmt, they have implied margins in nuclear are near double digits and c$100m. Aecon discloses the Utilites EBITDA, so Civil, Industrial, and Transport combine for the remainder.

This seems like a fair way to value Aecon https://t.co/anlglFbFbf. The company is not getting credit for its strong Nuclear and Utilities busineses, IMO. Sell side still seems focused on the very tail end of legacy fixed price contract losses and ignoring DD%+ growth in nuclear.

Given most other nuclear related stocks have performed very well recently, I'm surprised $ARE.TO has languished. Aecon's Nuclear related revenue has doubled over the last 3.5 years.

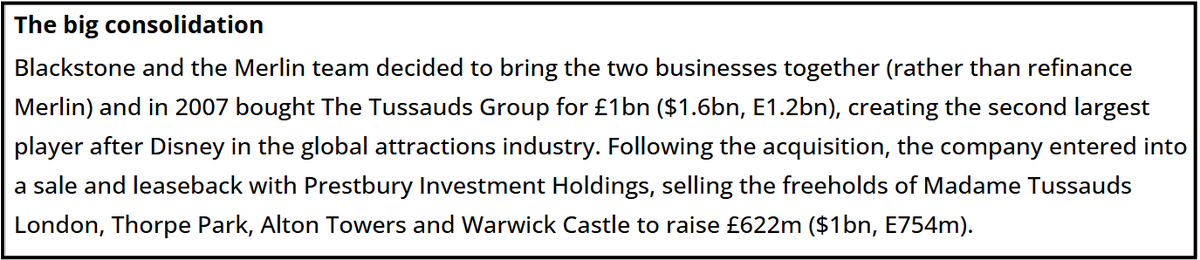

Any opinion if $BX owned Merlin is clearing the way for a $PRKS acquisition with their plan to divest its aquarium assets (Sea Life)? A combination seems to make a lot of sense, and $BX could monetize the real estate as well as anybody.

https://t.co/Iuprmyk4S9