~3k Coinbase Loans users were liquidated this week so far on Morpho, with $65M in Bitcoin collateral liquidated, making it the 2nd highest week by users liquidated and 3rd by value since the product launched.

Liquidations are a normal and expected part of any DeFi lending product and the numbers here are not abnormal relative to the size of the book (around 4% of total collateral). In DeFi, users interacting with lending protocols generally understand the liquidation mechanic and have accepted it as part of the product design.

Nevertheless, the dynamic is different in a consumer crypto lending app. A retail user who deposits cbBTC, borrows stablecoins against it, and gets liquidated during a price drawdown will likely not frame it as a risk they consciously accepted and in many cases, they simply won't come back.

This is especially true when the product lacks mechanics that are more UX decisions than protocol ones: a push notification when approaching the liquidation threshold, an automatic collateral top-up option, or a clear in-app warning showing exactly how far the price can move before the position is at risk.

For crypto lending to make a real dent in consumer finance, the core design challenge is building the UX/UI rails that adapt a protocol mechanic to what a normal consumer user expects from a financial product

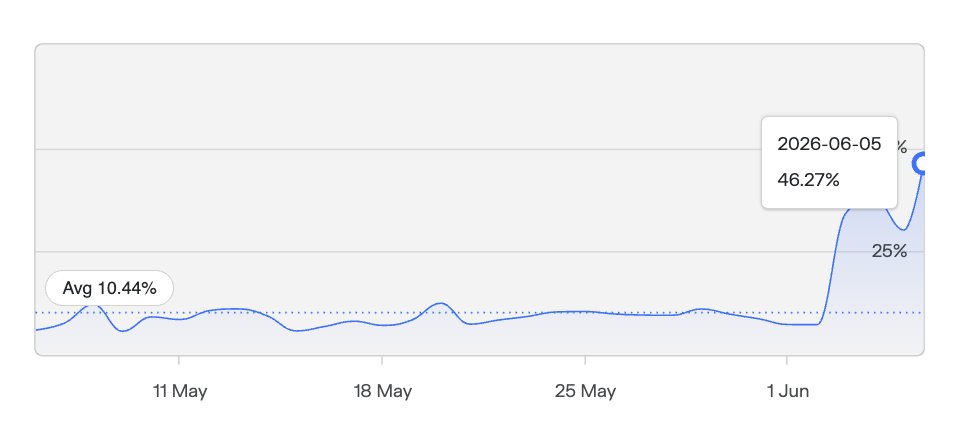

PT-apyUSD-18JUN2026/USDC market on Morpho is the one with higher exposure and showing early stress signs.

$18M market size, down from $34M two days ago and with rates spiked to 46% today against a 7% average.

The biggest borrower, that represents 16% of market borrows, is close to liquidation.

Morpho's largest liquidations on Ethereum this week are also apxUSD-related.

Herd is a great tool to understand protocol risk and potential liquidity windfalls.

We analysed apxUSD through Herd and Pendle has an exposure of $140M, Morpho $25M

At a smaller scale Curve, Royco and Aeordrome also have exposure.

What are all the positions affected by apyx and the STRC depeg?

50+ tokens and vaults are intertwined in apxUSD across pendle, morpho, termmax, infinifi, neutrl, royco, beefy, and more (cross chain too on base and bsc).

I break down the apxUSD balance sheet graph here:

WETH liquidity on @aave Core Market has fully normalized since the mid-April liquidity crunch.

Liquidity is now above pre-event levels and it's the again the deepest liquidity pool for WETH in DeFi.

RWAs is an awful term and I think we’re watching the same dynamic play out that we saw with stablecoins.

“Stablecoins” is itself a loosely applied label that a broad range of assets with very different risk profiles, yet borrows credibility from the least risky examples in the category.

There’s a wide range of assets that can be brought onchain, and they won’t scale the same way. Permissioned assets will likely capture the deepest capital pools, but move slower due to compliance and structuring constraints. More open approaches can scale faster earlier.

Great research from @sealaunch_ highlighting growth of RWAs from $2.6B to $33.7B and what is next.

Its clear to me that all financial be onchain- the question is how fast will that happen.

We built @aave Horizon to support the future of finance. Quickly becoming the largest RWA market for tokenized securities.

"That is why products like @aave Horizon matter as a top destination for RWA collateral: it recently surpassed $520M in market size and $170M in borrows"

We wrote an overview of the RWA asset class showing how it grew from $2.6B to $33.7B in roughly two years, but also how much room is still left to grow and the opportunities that lie ahead.

Aave V4's Hub-Spoke architecture is more relevant now than ever. In a market where LSTs, RWAs, vaults, and synthetic assets are multiplying, it fundamentally changes how DeFi lending manages risk at scale.

Users interact with @aave directly with Spokes, while the Hub is where liquidity sits.

Every spoke encodes a specific borrowing intent (ETH leverage, stablecoin strategies, gold, forex) each with its own caps, liquidation parameters, and oracle scope.

This matters because in V3, every new asset listing competed for the same cap budget inside a shared solvency boundary, forcing more conservative defaults across the entire venue.

In V4 each hub has a different risk profile. Core handles general-purpose depth, Prime isolates bluechip collateral for suppliers who don't want utilization risk on their ETH or BTC, and Plus Hub lets Ethena strategies scale behind their own solvency boundary without touching Core's parameters.

The diagram below maps how liquidity flows between them.

Total crypto protocol revenue (excluding stablecoin issuers and chains) is now a $5.5B/year industry, +10% YoY.

In the past year, new revenue-generating categories emerged (launchpads, derivatives, Telegram bots, prediction markets) all reaching revenue PMF.

The pie has grown but it's still small relative to what's coming. If crypto keeps disrupting industries with 10x better solutions, the case for charging fees gets stronger, not weaker.

Tokenization unlocks new verticals and composability effects that don't exist yet and will have a positive n effect in revenue generating protocols.

→ https://t.co/2bFrME8XeC

The "revenue is bad" story is usually just cope (with some interesting exceptions).

It's powerful and often smart to minimize fees and subsidize growth, but you need to test pricing and learn where you can consistently take revenue.

Crypto is learning.

Liquidity on @aave is now back at normal levels.

On Core Market, WETH has $448M available and USDC and USDT combined have $400M liquidity.

Utilization is back in the 89-92% range across all three.

Across other major reserves, utilization is also back to healthy levels.

Most borrowed assets on @aave v3 Ethereum Core market are seeing liquidity come back.

Stablecoins were first now WETH is following.

Next step should be an increase in WETH liquidity on L2s

The Commerce Payments Protocol by @Coinbase and @Shopify saw a sharp surge in activity starting in the beginning of April, driven by a new operator scalling payments on that date.

Volume across all size tiers increased activity, with the pattern suggesting permanent merchant onboarding rather than a one-off event.

The most likely hypothesis: Coinbase Business, which operates directly on the protocol, absorbed merchants migrated from the Coinbase Commerce shutdown, which happened on that exact date.

Commerce Payments Protocol is an open-source, onchain payment system that brings programmable escrow, delayed capture, and conditional settlement to commerce.

Great work from @PanteraCapital by @sui414, @0xallyzach and @FranklinBi mapping the $ 320B tokenized asset market.

The Tokenization Progress Index scores assets across issuance, transferability and composability, a useful framework to better understand tokenized assets in a market where every bank now has a tokenization strategy.

A reminder that not all tokenized assets have the same characteristics or onchain maturity.

Today, 77.6% of tokenized assets score below 2.5/5, meaning they are distributed onchain but not onchain native.

Happy to have contributed a little feedback during the review process.

Proud to launch Pantera's Tokenization Portal and Q1 Report with @0xallyzach@FranklinBi!

The biggest surprise from our study of the $320B market: Most tokenized assets are still Wrappers — by design, not by accident.

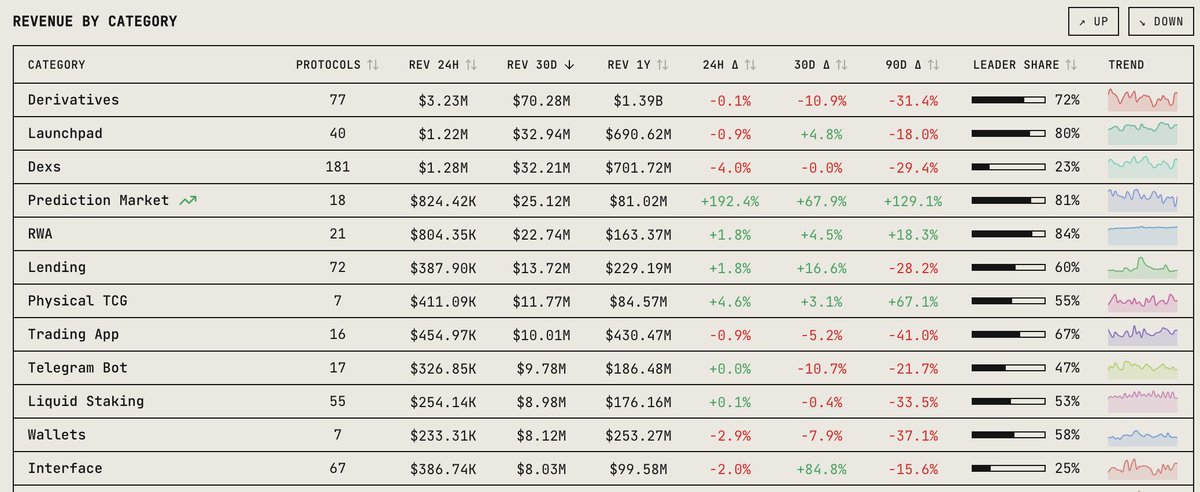

Among the top revenue-generating categories in crypto over the last 30D, growth is concentrated in a few:

→ Interface +84.8%

→ Prediction Market +67.9%

→ Lending +16.6%

→ DEX Aggregator +11.8%

→ Launchpad +4.8%

→ RWA +4.5%

Derivatives, DEXs and Trading Apps, historically large revenue generating categories, are all shrinking.

Prediction markets are now the 4th largest category in crypto by revenue, generating as a category $25.1M in the last 30 days.

The main driver is @Polymarket that generated +$20 in 30 days, 82% of the category.

Prediction markets are now the 4th largest category in crypto by revenue, generating as a category $25.1M in the last 30 days.

The main driver is @Polymarket that generated +$20 in 30 days, 82% of the category.