Cowen TMT memory/storage takeaways:

"DRAM/NAND is becoming a big percentage of CapEx (went from 10-15% to +40%). This requires a meaningful shift in how hyperscalers operate given that they have used to quarterly pricing negotiations."

" $STX and $WDC both indicated that NAND pricing increase should not be a derivative for HDD pricing, and investors are clearly most enthusiastic about the pricing opportunity for HDDs"

"For $SNDK, management highlighted the unique structure of the LTAs it already signed. The floor gross margin is higher than what our checks for DRAM suggest (80% for SNDK vs our checks for 60% in DRAM, here)."

"SNDK already locked in 30% of its capacity next year under LTAs and the goal is to potentially increase that to 80% over time. With this level of margin structure, durability matters more than continued price increases."

DRAM/NAND pricing pressure should pick-up the next 2-3 quarters

To date, $DELL supply chain has deftly managed the sharp increases in both DRAM and NAND and pressure across other components as well. However, the impact of the rising costs are expected to be more severe in the second half of calendar 2026 into the first calendar quarter of calendar 2027. While the rate of change moderates beyond C1Q:27, we do not expect a decline in prices further impacting PC, server, and storage margins for longer.

JPM TMT Conf $QCOM:

"Hyperscaler custom silicon engagement, with revenue starting later in 2026, is expected to add material revenues in FY27."

"For custom silicon as well as merchant accelerators, Qualcomm is set to compete with industry incumbents like $AVGO and $MRVL"

JPM TMT Conf $MU takeaways:

"HBM4 production is ramping 2x faster than HBM3E 12-High did last year. HBM4E development is well under way for a CY27 ramp."

"On SCAs, mgmt confirmed meaningful progress since the first 5-year DRAM SCA disclosed in March, with multiple additional customers in active conversations, and explicitly confirmed SCAs are now being secured for NAND as well – an incremental positive given the structural NAND tightness narrative."

$SNDK

SIG Networking Channel check notes (5/19/26):

$MRVL: Google TPUv9 for inference

$ALAB: UAL delayed 1 yr + win at AMZN

$AVGO: Tomahawk ramp.

COHR/LITE: +ve on 1.6T

Rubin doubles transceiver to GPU count (2:1). Potential InfiniBand peak 2026. First CPO on ASIC switches (prototypes use pluggable opticals).

Feynman copper backplane + CPO inter-rack.

Etc.

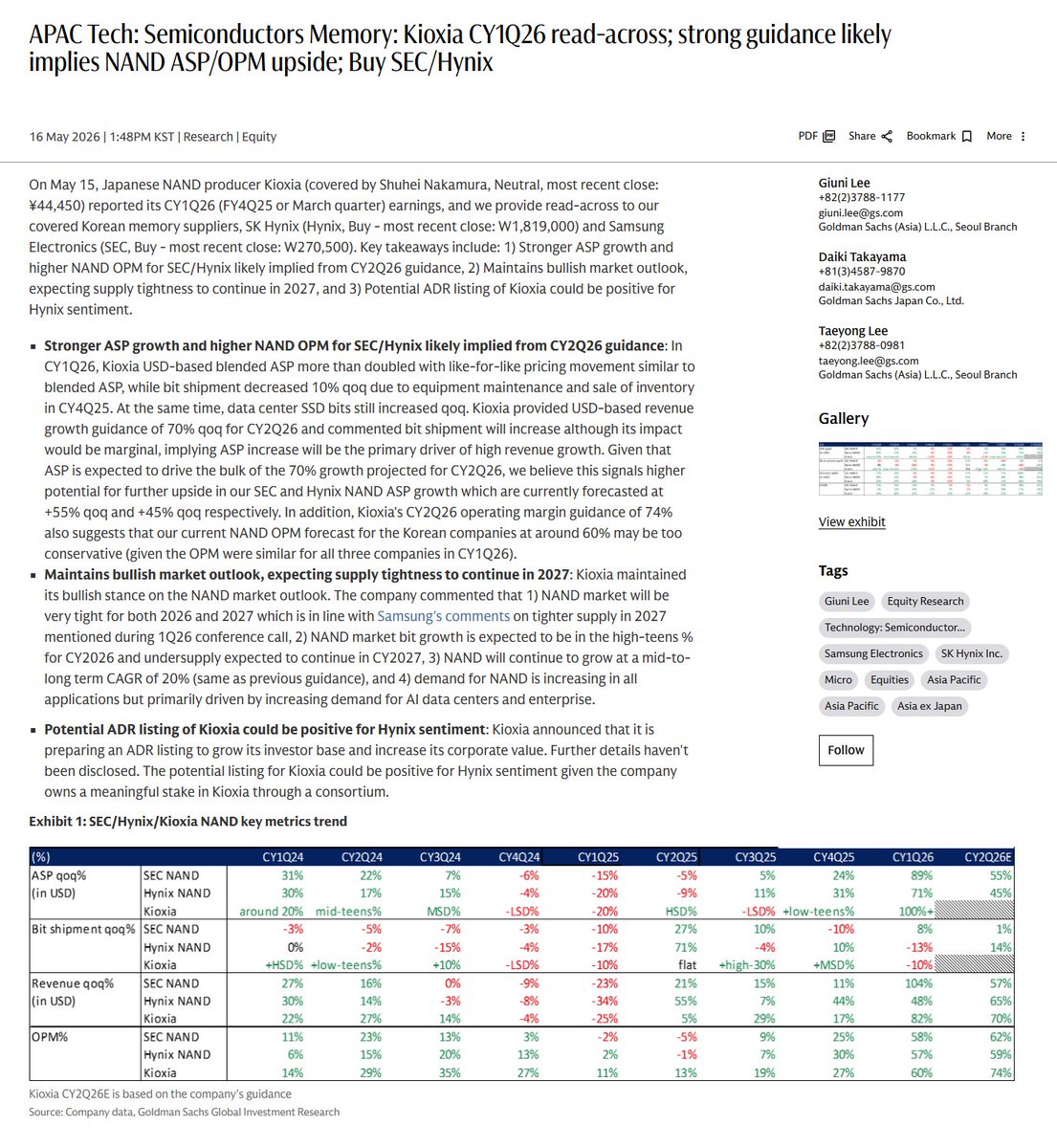

GS on Kioxia ( $MU/ $SNDK): The company commented that NAND market will be very tight for both 2026 and 2027.

Stronger ASP growth and higher NAND OPM implied from CY2Q26 guidance:

"Kioxia USD-based blended ASP more than doubled... ASP is expected to drive the bulk of the 70% growth projected for CY2Q26, we believe this signals higher potential for further upside in NAND ASP growth."

$MU: JPM-strikes

"2Q26 memory contract pricing is tracking well above expectations (DRAM +58-63% q/q, NAND +70-75% q/q vs. JPM's prior +40-50% estimate), which could largely neutralize the labor cost headwind and even make the strike a tailwind for near-term pricing negotiations"

AI inference ramp. "assume 100M Agentic AI users, 10 agentic task drive 1B agentic execution task workloads, need for 500M CPU cores, at least 2-3M incremental server CPUs (industry ~12-14M server CPUs), underlined by $ARM, $AMD and $INTC ...weekly token generation now >26T"

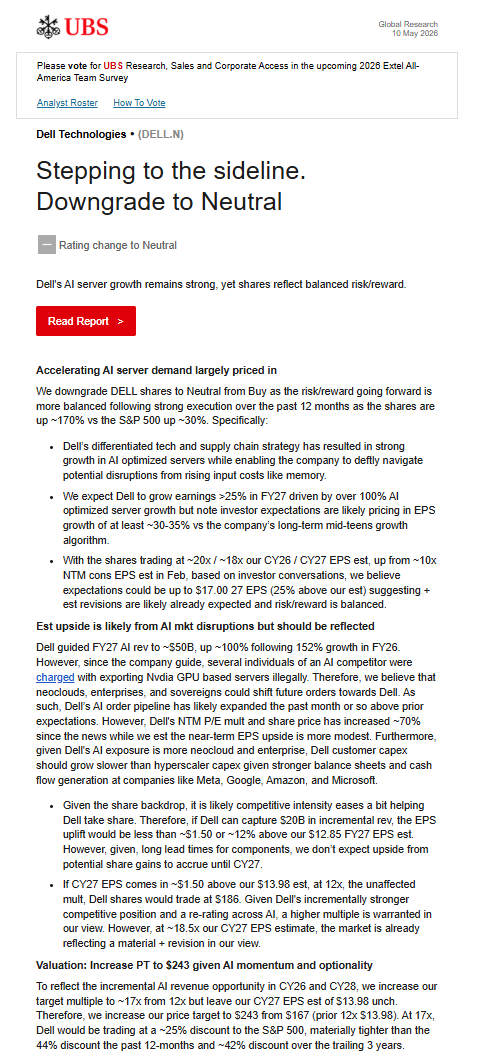

UBS d/g $DELL:

"given Dell's AI exposure is more neocloud and enterprise, Dell customer capex should grow slower than hyperscaler capex given stronger balance sheets and cash flow generation at companies like Meta, Google, Amazon, and Microsoft."

$SMCI, $TSSI

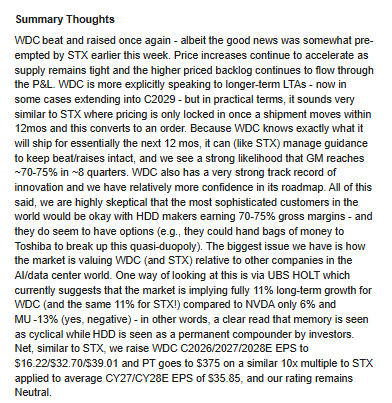

Arcuri on HDD to memory multiples/growth rates:

"market is implying fully 11% long-term growth for $WDC (and 11% for $STX) compared to $NVDA only 6% and $MU -13% - a clear read that memory is seen as cyclical while HDD is seen as a permanent compounder"

JPM d/g $META: "believe full-stack AI competition is intensifying and Meta has a more challenging path to returns on heavy AI capex beyond advertising"