The next level of growth might look a little different than expected. We'll help you chart the course. This is just a highlight of what our network has to offer, all actively hunting buyouts and partnerships.

Let's expand your surface area for luck: https://t.co/yWC6ajPAHe

Sports is institutionalizing, but the opportunity ladder has distinct rungs. The capital that understands risk-adjusted returns is building infrastructure around them. Where you enter depends entirely on your access, capital base, and risk tolerance.

https://t.co/KenyA1dHGU

Markets under information overload don't reward those who require additional evaluation. They reward those who are immediately understood. That's why signal is important.

We launched a new partnership to give you the free resources to build authority.

https://t.co/23j2uXFkUU

Inbound interest is not a term sheet. Treat those first emails as discovery, not destiny: qualify the buyer’s mandate, timing, and capital before you ever start educating them on your business in detail.

https://t.co/6yyu2yCutS

Private credit has exploded as an alternative to bank lending. More flexibility, larger amounts, personalized underwriting. But that comes with deeper scrutiny. The difference between a 60-day close & 6-month runaround is the quality of your preparation.

https://t.co/2Dt3ZnPipz

most venture-backed companies end up in the same place:

raised 3-4M seed (or 10-15M series A)

built real product

got to 300-500K ARR (or 2-3M ARR)

VCs stopped caring

founders stuck with high pref stack, can't raise more, can't exit, can't even shut down cleanly

these aren't bad businesses

they're just wrong cap tables

the companies could throw off 500K-1M in profit annually

hire 2-3 more people and grow to 2-3M ARR

actually build something valuable

but they're trapped in venture math that doesn't work anymore

the discourse only covers two outcomes: unicorn or failure

nobody talks about the third path: decent business, wrong structure

thousands of quality founders stuck running companies VCs wrote off

not because they're bad operators

because they picked wrong market size or wrong cofounder or raised too early

We've talked to 100+ searchers, independent sponsors, and holdco builders.

Here's our unpopular opinion: Many think they have a dealflow problem when they actually have a clarity problem.

This workbook helps provide strategic clarity in <90 minutes

https://t.co/7GxvZE0gK1

The future of GTM is here! 🚀 Our final demo day of 2025 is featuring some incredible startups that are redefining how businesses go to market.

We've also got a killer chat for networking and exclusive discounts from our partners. Don't miss out!

Link - https://t.co/TdvkyKBpEl

If you're searching for deals in your spare time, you're not alone, but you might be falling behind.

Let us help you level the playing field:

✅ Dedicated advisor

✅ Curated deal pipeline

✅ Managed initial due diligence

Learn about our Buyer Solutions: https://t.co/HQrzH3uxZa

Here’s how Family Offices are using #AI across the globe. No surprises that the East is leading the way but are those in the Americas still not sold or just not sure how to implement?

Heard a true horror story from a gentleman who today manages a great eight-figure portfolio, but he said that if he had bought just one company and given it all his attention, rather than hiring a buy-side broker to build deal flow to buy next 2 bizs he would be back at his 9-5.

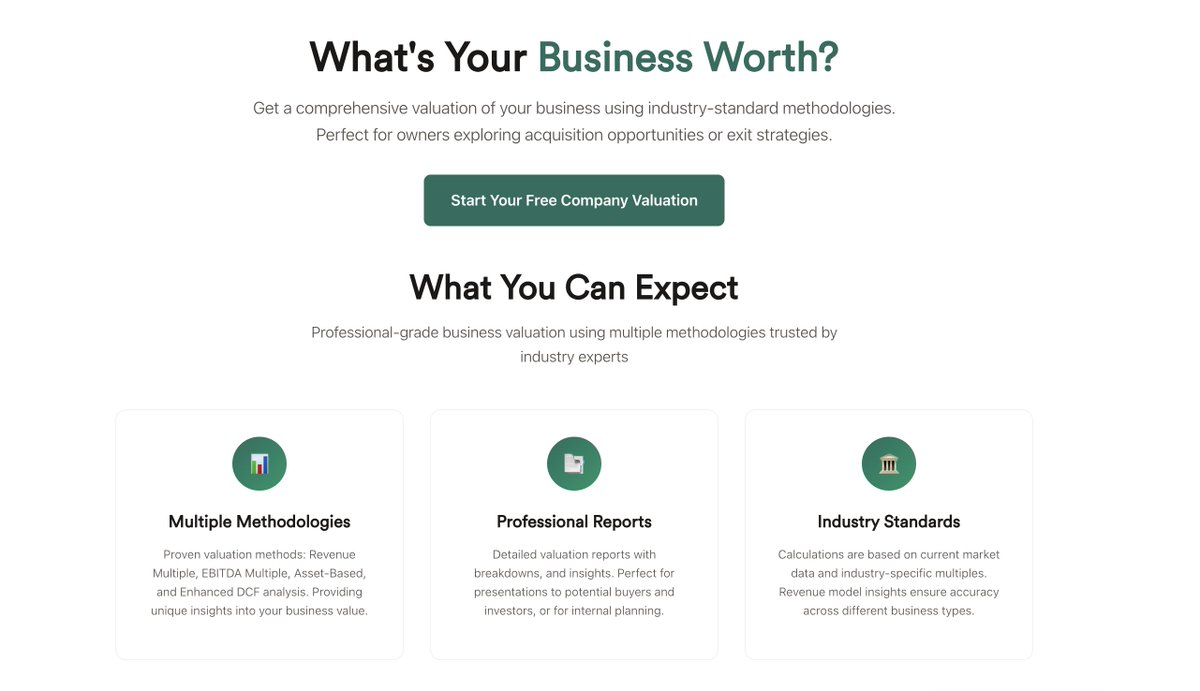

Second is the beta of our free Company Valuation tool. Generate a report to help set a baseline for conversations with potential buyers, investors, or internal exit planning.

Learn more and get your valuation: https://t.co/tqcy6CtfaD

First is our Partner Portal. These are vetted service providers and platforms that can help you be successful at any stage of your journey. Spend less time searching for the right tools or vendors and more time focused on what matters. Meet our partners: https://t.co/53VA21VoWM

Breaking Update:

The SBA has just released its long-anticipated technical corrections to its SOP, and search fund lending is on the radar.

Before the hot takes start flying, take a moment to actually read the update… because if your take isn’t “technically”correct, you’ll be spreading inaccurate information.

Here’s what’s important:

The SBA is not banning all search fund deals. In fact, the traditional model where an entrepreneur raises capital from investors to acquire and actively operate a business remains eligible.

The problem arises when that structure is modified in ways that violate SBA requirements.

Two practices are now expressly disallowed:

1: If the entrepreneur lacks actual control of the business, particularly due to a side agreement giving control to a non-guarantor investor, the loan is ineligible.

2: If investors require their capital to be repaid (or receive preferential distributions to recover their investment) before the SBA guaranty is released, that investment is treated as debt, not equity… and that can jeopardize the loan’s eligibility.

The SOP now makes it clear:

If someone who is not personally guaranteeing the loan (typically under 20% ownership) ends up controlling the business through a separate agreement, the deal does not qualify.

Makes sense…

Likewise, any “equity” that walks, talks, and behaves like debt… such as redeemable preferred stock or structured return-of-capital agreements… will be treated as debt for SBA purposes.

This could impact some structures.

That said, this does not mean investors are prohibited from receiving profits. Standard dividends or discretionary profit distributions remain permissible… what matters is the absence of a guaranteed payback.

Most lenders I work with serve “self-funded searchers,” a structure that remains fully viable.

The key is that the searcher must be the guarantor, maintain control, and hold an appropriate ownership percentage.

Bottom line:

Well-structured search fund deals are alive and thriving, but if you’re operating in the gray zone, now is the time to reassess.

Let’s lead with clarity instead of clickbait.

2025 isn’t slowing down…

… and neither are we.