No one’s talking about this, but the dollar just hit its lowest level since mid-November.

Ironically, maintaining the dollar’s role as a reserve currency almost depends on weakening it.

As Bessent put it best:

Keeping the USD as the world’s reserve currency and devaluing it against other currencies are not mutually exclusive.

We’re at a key inflection point, and the dollar is likely entering a long-term downtrend in my view.

Ouch.

Another sharp drop for the dollar today.

The DXY index is now retesting its 2023 levels.

This is a significant breakdown, in my view, especially with most investors still heavily long the US dollar.

I see more downside pressure likely ahead for the USD.

Gold prices have surged far beyond production costs over the past few years, creating some of the strongest margins mining companies have seen.

Keep in mind:

The gold-to-oil ratio — especially crucial for open-pit mines — is now at its second-highest level in history, further enhancing profitability.

The recent earnings beats from some major mining companies that have just reported are only the beginning of what’s likely ahead in the coming quarter, in my view.

Possible Capital Rotation Event JUST around the corner.

Gold VERY CLOSE to a breakout against the most important stock market.

I'd expect a market sell-off to happen on this breakout and possibly a recession afterwards.

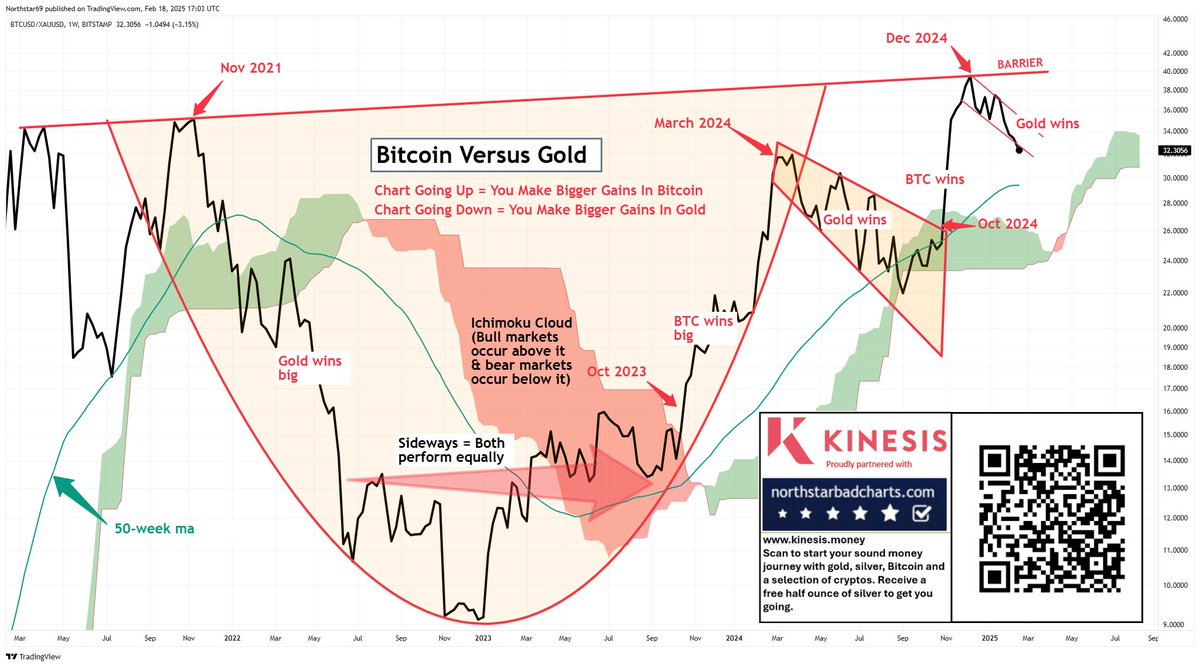

BITCOIN falling further versus GOLD. No go for Bitcoin until/unless it breaks through the barrier. As soon as the CRE arrives, it's over for Bitcoin & crypto, so the clock is ticking if we want to see $140k+

Gold closes at an all time high above $2,930 as another 160,000 oz of physical gold are delivered to Comex vaults, bringing total to 37.6 million troy oz, with "big 3" vaults at all time high

Nvidia Under Attack

The release of China’s open-source DeepSeek R1 may get the credit for bursting the Nvidia bubble, but a potentially even more relevant Nvidia threat is an innovative US AI-semiconductor private company called Cerebras that invented a new chip that outperforms Nvidia’s most advanced GPUs. Cerebras claims a single wafer-scale chip with 900,000 AI-optimized cores and 4 trillion transistors, making it ~56x larger than NVIDIA’s largest GPUs.

Crescat may or may not hold positions at any given time in the securities referenced. This is not a recommendation or endorsement of any secure or other financial instrument.

We identify multiple potential catalysts that could trigger a reconciliation of these imbalances:

· China DeepSeek’s bursting of the US megacap tech bubble.

· Tariffs: While a potentially viable negotiating play, Trump/Bessent tariffs threaten trade, corporate profitability, and the overvalued US stock market.

· Tariffs: Consider that the 1929 stock market collapse began on October 28 when news spread that the Smoot Hawley Tariff Bill would become law. The front-page New York Times article read: “Leaders Insist Tariff Will Pass.”

· Tariffs: Now consider this weekend's lead Wall Street Journal Story: “Trump Threatens Widening Trade War as First Tariffs Loom”.

· Liquidity: The lag-effect of Jay Powell’s higher interest rate hikes to fight inflation as low-interest-rate Covid debt is starting to roll over and needs to be refinanced.

· Liquidity: The draining of almost all the excess liquidity from the Fed’s Reverse Repo Facility, an incoming gift to the Trump Administration from Janet Yellen and Jay Powell.

· Liquidity: China and the East are challenging the supremacy of the US dollar as the world reserve currency for trade at the same time as a rising US dollar versus other fiat currencies poses a global liquidity squeeze, a Triffin Dilemma.

Importantly, global central bank assets have contracted to their lowest level in over four years. This is largely due to the strength of the dollar, which is suffocating the global economy. We believe a USD devaluation, whether coordinated or organic against other currencies, is inevitable.

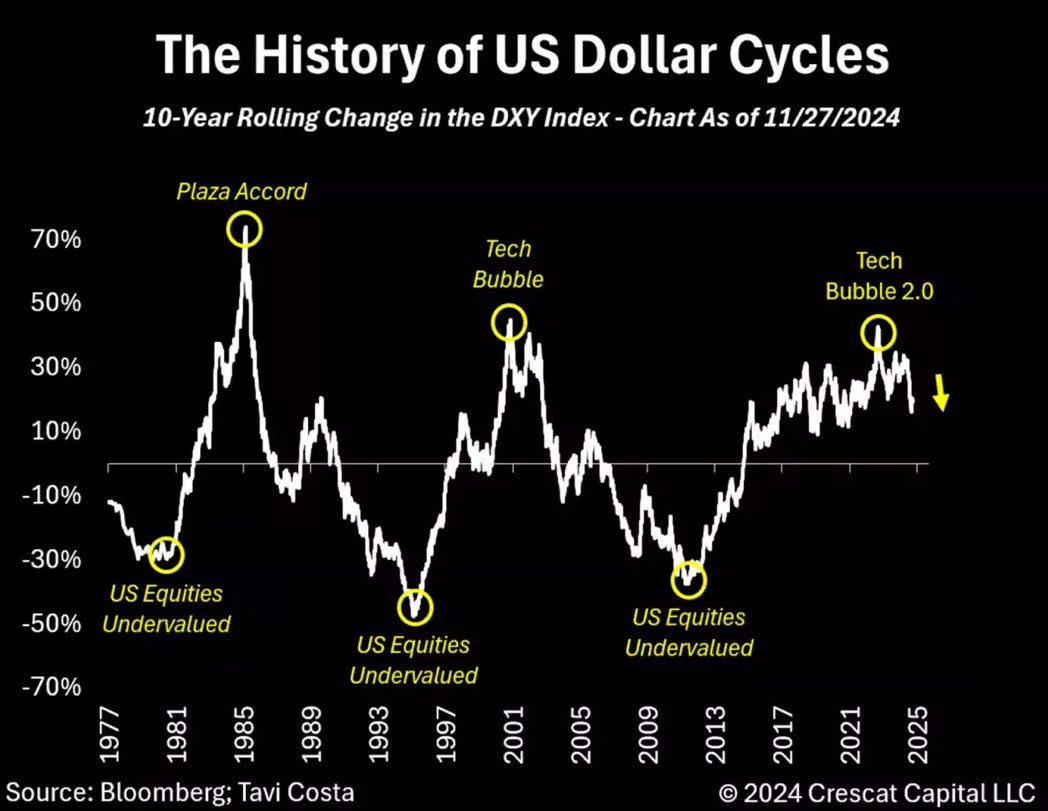

As we start the year, we have been reflecting on what we consider to be one of the most consequential macro trends likely to unfold in 2025 and beyond. We contend that the US dollar is approaching a cyclical peak, with its long-term decline already evident on a 10-year rolling basis.

In our assessment, the interplay of declining fiscal stimulus and structurally lower interest rates—partially designed to alleviate the government’s debt burden—is poised to serve as the primary catalyst for the dollar’s depreciation in 2025. However, currency movements are inherently relative. Notably, no other major economy—whether Japan, Canada, the Eurozone, the UK, or Australia—faces the same imperative as the United States, which must sustain GDP growth of nearly 5% merely to service its debt.

An often-overlooked factor in the dollar’s recent strength is the potential impact of trade policies, particularly the enduring effects of Trump-era tariffs. While these measures could generate a short-term shock, they represent only one facet of the broader policy agenda of the new administration, in our view. As newly appointed Treasury Secretary Scott Bessent has articulated, Trump’s vision of a weaker dollar coexisting with its reserve currency status is not mutually exclusive.

Overall, the risks to the U.S. dollar appear asymmetrically skewed to the downside. Even if short-term fluctuations result in an initial appreciation, the broader and more consequential trajectory is likely to be one of long-term depreciation. If this scenario materializes, this shift could represent one of the most profound transformations in the macro landscape since the Global Financial Crisis.