We engineer ASYMMETRY®— defined downside risk and adaptive upside— for business owners, physicians, and families with meaningful capital at stake. @MikeWShell

Record margin debt isn’t automatically bearish. The asymmetric risk is when borrowed buying power, a thin cash cushion, and falling collateral values meet at the same time.

https://t.co/vDSzJyCoj3

@SMB_Attorney Everything is relative.

At just 2.1% of Berkshire Hathaway's record $397.4 billion cash pile, the $8.5 billion acquisition of Taylor Morrison is a mere rounding error rather than a major strategic shift.

Everyone’s worried the IPO wave will drain the market.

Goldman Sachs just opined:

$1.3T in buybacks. $900B in cash M&A. Against $675B in new issuance.

Corporate demand doesn’t just absorb the supply — it buries it.

The asymmetry favors the buyer.

AAA regular gasoline is near $4.43/gal.

That’s well above 2023–2025 at this point in the year, and approaching the 2022 stress zone.

The issue isn’t just the level. It’s the velocity.

Fuel prices have repriced fast enough to hit the consumer before the economic data fully shows it.

The US stock market's 2026 rally has been driven entirely by rising corporate profits rather than increasing equity valuations—and Goldman Sachs Research expects that trend to continue.

They expect a 6% gain from current levels. The higher forecast is driven by upgraded earnings estimates; the team projects S&P 500 earnings per share (EPS) of $340 in 2026, a 24% increase from the prior year, and $385 in 2027, representing 13% growth.

This market isn't only an AI story. It's an earnings-dependency story. Prices can keep rising if forward earnings keep confirming the move, but if that confirmation fades, portfolio risk can show up fast.

https://t.co/KxdQSF0A7K

Stocks Up + Volatility Up: When the Market Starts Paying for Upside by portfolio manager and chief investment officer @mikewshell

https://t.co/ALTFjuZfWy

The market is showing rotation rather than broad deterioration. A massive defensive surge into Utilities (94% above the 5-day MA) and sustained runs in Tech/Real Estate are keeping the index afloat, while the primary uptrend in Energy remains intact despite recent short-term profit-taking.

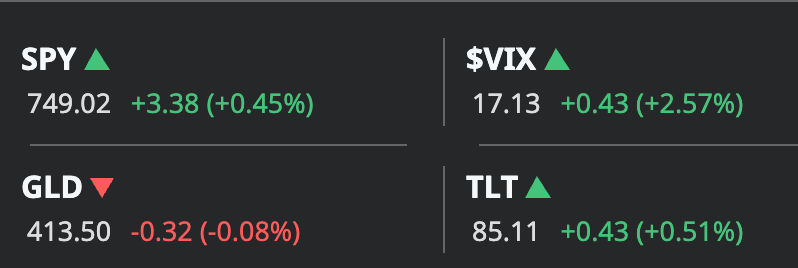

The market is pushing into record territory, but it isn't a blind rally. The simultaneous rise in bonds ($TLT ) and volatility ($VIX) suggests while traders are riding the bullish wave, they are keeping one foot firmly planted near the exit door by buying protection.

Access to alternative investments isn’t the edge.

That may be the most important point in alternatives.

More private funds are being packaged for private wealth management.

More evergreen funds.

More private credit.

More private equity.

More real estate.

More infrastructure.

It doesn’t mean more opportunity automatically.

It means more need for judgment, skilled decisions, and experience.

The family that sold a business doesn’t need Wall Street investment bank inventory.

They need disciplined filtering.

What belongs in the portfolio?

What should be avoided?

What is too illiquid?

What is too crowded?

What is priced for perfection?

What actually improves the portfolio’s risk/reward?

That’s where I see alternative investments differently.

The mission isn’t just access to alternatives to stocks and bonds.

The mission is asymmetric exposure: return drivers selected, sized, and monitored for capital that can’t afford careless complexity.

Investors are told to want a “balanced” portfolio.

I’ve never liked that word.

Balanced upside and downside?

Balanced profit and loss?

Balanced risk and reward?

That’s not the goal.

The goal is asymmetry: more upside than downside, more reward than risk, more potential gain than potential loss.

A 60/40 portfolio is often called balanced, but it’s really just a static mix of stocks and bonds.

And when stocks and bonds start trending together, that so-called balance can disappear exactly when investors need it most.

I engineer ASYMMETRY®.

A “balanced portfolio” may sound safe, symmetry isn’t the same as risk control.

A portfolio can be diversified on paper and still be exposed to the same macro pressure underneath.

Inflation.

Interest rates.

Liquidity.

Credit stress.

Equity valuation risk.

That’s the part investors often don’t see until markets test it.

The goal isn’t to own more categories.

The goal is to own better-shaped risk.

ASYMMETRY® Managed Portfolios are built around the idea that capital with consequences needs defined downside, intentional exposure, and more than one way to earn return.