UNIMECH has Bull Case TP of ₹2248 (+87%). It is strategically positioned to capture structural tailwinds in aerospace & defense, energy & semiconductor equipment sectors. Its ability to offer competitive pricing, combined with favorable tailwinds suggest strong growth potential.

Timepass talk on Sunday

This week, let's revisit some of the names we've discussed before and focus on the key things to watch for in their Q1 results.

1. Rishabh Instruments - Shared on Feb 8, 2026

I presented Rishabh Instruments at ALD event when the stock price was in the ₹200s. My conviction was based largely on management’s stated target of ~₹100 Cr EBITDA for FY26.

Now, looking at 9M FY26, EBITDA has already crossed ~₹93 Cr, a clear sign the management is walking the talk on restoring profitability.

This improvement wasn’t accidental. It also involved consciously cutting low-margin/non-profitable revenues, especially from Lumel Alucast (automotive segment).

While Electrical & Electronic Instrumentation remains the primary growth driver, the company has finally sounded positive on its solar business. After a long period of losses, the segment has turned operating-level profitable and the company has secured fresh orders for its single-phase inverter models. FY27 could become an important year for this vertical.

However, profitability recovery is only step one. The bigger trigger will be growth. Currently the growth engine is still running a bit slow, the day revenue growth starts sustaining ~20–25%, the probability of a re-rating increases meaningfully.

Management teams that go through tough conditions and fix their business models deserve attention. Execution during adversity often tells you more than execution during tailwinds.

Current update: They delivered an EBITDA of ₹126 crore in FY26, exceeding their guidance. The stock price naturally reflected that performance.

What to track in Q1 commentary: How is the U.S. market growing? How are the rest of the international markets shaping up? How fast is the solar inverter business growing? How is the EMS business progressing? And how is Lumel Alucast's (die-casting) profitability shaping up?

2. Sakar Health - Shared on Feb 8, 2026

Sakar Health post fantastic results in Q3FY26 and concall is coming up on Feb 11th.

Founded in 2004, Sakar has evolved from a small contract manufacturer into an API-integrated pharmaceutical company with a growing global presence. The company now operates WHO-GMP and EU-GMP approved facilities in Gujarat, exports to 60+ countries, and has built a portfolio of ~292 product registrations across 75 international partners.

They operate in three verticals: 1. CDMO / CMO Services, 2. Own Brand Exports, 3. Licensing / Product Development. For most of its history Sakar was primarily a generic formulations exporter, but in the last few years it has pivoted meaningfully toward oncology, and that is increasingly becoming the real story.

The company has set up a vertically integrated oncology facility with EU-GMP approval. Its oncology portfolio includes 55 in-house developed products, of which 32 are ready for global launch. It has already secured 11 Marketing Authorisations (MAs) across geographies (six in Europe and the balance across APAC and Latin America).

On the CDMO/CMO side, Sakar manufactures for established Indian pharma companies such as Zydus Life Sciences, Torrent Pharmaceuticals, Indus Pharma, Emcure, Cipla and Glenmark, with ~20 active clients.

Going forward, while their generic formulations unit would continue to grow steadily (primarily in export markets), the two growth engines will be the CMO for these big Indian MNCs and Oncology portfolio.

If execution sustains, Sakar appears to be transitioning from a plain export-generic company into a specialty manufacturing + oncology platform, which is a very different valuation narrative.

Current Update: Sakar posted a solid Q4 and a guided for a promising FY27

What to track in Q1 commentary?

Management has guided for approximately ₹200 crore in oncology sales for FY27 (vs. ~₹96 crore in FY26). Q1 should provide the first indication of whether the company is on track to achieve this target.

Management expects around 25 of the 31 EU dossiers to be commercialized by Q3 FY27. Q1 should ideally reflect the initial commercialization of the first few dossiers.

Capacity utilization at the Bavla oncology facility will also be a key metric to monitor.

3. RBZ Jewellers - Shared on March 8, 2026

RBZ Jewellers operates a unique dual-channel model, combining a strong B2B wholesale presence, supplying to national giants like Titan, Malabar and PNG, with its high-growth B2C retail brand, Harit Zaveri Jewellers, which currently operates an ~11,000 sq. ft. flagship store in Ahmedabad.

A little over a year ago, RBZ had guided for ₹800 crore revenue in FY26 and ₹1,000 crore in FY27. During the Q4FY25 concall, the FY26 guidance was moderated to ₹700 crore, while FY27 guidance of ₹1,000 crore was retained.

However, in the Q3FY26 concall, management further revised expectations, guiding for ₹630–650 crore in FY26 and ₹800–900 crore in FY27.

With multiple factors coming together (guidance coming down, volumes coming down), the market seems to have lost interest in the stock, pushing valuations to what appears to be their cheapest levels so far.

But there may be a silver lining.

The company is on track to open two large retail stores in Surat and Rajkot by Q2FY27. If executed well, these three stores could potentially push retail revenues into four digits, while also improving overall margins.

That said, in the near term PAT may remain under pressure, as marketing spends and other launch-related expenses could weigh on profitability in FY27.

Structurally, the business mix is also evolving. By FY27, volumes are expected to be roughly split 50:50 between retail and B2B, while retail could contribute ~75% of revenues, with wholesale and job work accounting for the remaining ~25%.

Current update: Posted decent Q4

What to track in Q1:

Progress in the launch of new stores.

Inventory and working capital trends.

Promotional spending for newly launched stores and its impact on profitability.

Progress of the daily wear product launch.

Effectiveness of the company's hedging strategy in managing input cost volatility and protecting margins.

4. KSH International - Shared on March 15, 2026

KSH International is a specialized industrial player focused on magnet winding wires and Continuously Transposed Conductors (CTC), high-precision components that are critical for large power transformers, EV traction motors, and generators.

You might ask: there are many companies riding the electrification theme, so why look at this one? Here are a few reasons:

i) KSH is the third-largest manufacturer of magnet winding wires in India and the largest exporter of the same, supplying to 24+ countries. Being an approved vendor for global utilities and OEMs is a high-entry-barrier business, built over years of qualification and trust.

ii) The company serves global heavyweights such as Hitachi Energy, GE Vernova, Toshiba, and Siemens Energy, along with Indian giants like Power Grid, NTPC, and BHEL. It also holds RDSO approval and supplies to several Indian transformer manufacturers. Roughly 40–45% of revenues come from power transformers, grid infrastructure, and HVDC/EHV transformers, making KSH a strong proxy for the broader electrification theme.

iii) While other major players such as Precision Wires India and Apar Industries manufacture CTC and winding wires, KSH International is currently the only Indian company approved and certified to supply CTC specifically for 400kV HVDC transformers. HVDC transformers operate under extreme electrical stress; even a minor defect in the CTC winding can trigger catastrophic grid failures, which is why micron-level precision is critical.

iv) The company has added significant capacity over the last six months, taking total annualized capacity to 43,445 MT. This is expected to increase further to 59,045 MT by FY27, providing a clear runway for volume-led growth. The expanded capacity also positions the company well to pursue opportunities in export markets.

v) With better margins than peers, a near-monopoly position in HVDC CTC, capacity expansion underway, and strong tailwinds from the electrification theme, KSH appears to sit in a favorable strategic position.

Of course, valuations may not necessarily be cheap, and that is ultimately a call each investor needs to make.

Current Update: Lived up to the hype and capped off FY26 with a strong Q4 performance.

What to track in Q1?

Consolidated utilization was at ~70% in Q4FY26. How did Q1 do, particularly Supa plant utilization?

EBITDA/ton sustainability in the range of INR 68,000 and 74,000 in Q4

Export momentum trending towards 40% target?

Any progress on Q4 commentary of "...some of our large transformer clients have also begun to explore long-term multi-year agreements..."

Progress on PEEK and green copper backward integration

5. India’s CDMO Inflection Point - FY27; Shared on March 29, 2026

Clearly, India’s CDMO opportunity is still much smaller than China’s, but relative to where we were a few years ago, the ecosystem has evolved meaningfully. FY27–FY28 could well turn out to be the scale years for the sector.

Acutaas: Guided for ~₹1,000 crore CDMO revenue by FY28, with four products validated in FY26 expected to start contributing to the topline from FY27, providing clear visibility into the next phase of growth. In parallel, the company has taken a strategic step into semiconductor chemicals, specifically raw materials for photoresists, through its South Korea acquisition, adding a new high-growth vertical to the business. That said, the stock has seen a sharp run-up recently and may not offer the most attractive entry point at current valuations.

Navin Fluorine: CDMO revenues of ₹360 crore in 9MFY26, with a target of ₹850–880 crore (~$100 million) by FY27. The company has a pipeline of 10–15 molecules. Beyond CDMO, multiple capacities in other verticals are expected to go live in FY27 offering strong earnings uptick!

Sai Life Sciences: Manufacturing capacity to expand from ~700 KL in FY26 to 925 KL by Q1FY27 and 1,150 KL by Q4FY27 (≈65% increase). Added 7 molecules in FY26 (3 commercial, 4 in Phase III). Sai will be the primary supplier in two of these molecules . They are expected to sustain the margins in the range of 28% to 30%.

Divi’s Laboratories: Three large dedicated projects under execution, with commercial volumes expected from H2CY27. Over 18 MT peptide capacity, including Tirzepatide and potentially Orforglipron post regulatory approvals. GLP molecules are expected to add significant growth!

Laurus Labs: Barring a few logistical disruptions stemming from the Iran conflict, the company is expected to deliver a strong Q4 and maintain healthy growth in FY27 over FY26.

Valuations may not appear cheap, but as the saying goes, value ultimately lies in the eye of the beholder.

Current Update:

All of these companies appear to be on track with their CDMO journey. Acutaas lived up to the hype, Laurus guided for 30% EBITDA margins, and Sai Life nearly doubled its capex plans between FY26 and FY27.

That said, Sai Life's commercialization timeline appears to have been pushed back slightly compared to its original guidance.

What to track:

Management commentary on additional molecules.

Capacity utilization trends across key facilities.

Impact of raw material inflation on margins.

Progress of ongoing capex and commercialization timelines.

Drivers of margin improvement and sustainability of profitability.

That's all for this edition. Have a great Sunday!

Disclaimer: None or buy or sell recommendations. This publicly available information is shared for learning and education purposes.

Must read 2 microcap company

- Anlon health care

- Amanta healthcare

Although first-quarter (Q1) results for the pharma industry tend to be somewhat weak,a breakout has now been observed in the Nifty Pharma Index.

It means strength will be continue.

Don't Miss Oncology segment " Small Cap company"

Dis-i have shared only for knowledge purpose

#silver - Hope the timely update again helped, base formation done after a big fall now awaiting trend reversal, 1st signs of it above 64 & major abv 70.

A quarterly breakout retest is almost done so now once the trend reverses the move can be fast.

Views Invited, what's your take on long term will we see triple digits again in 2027??

Ashish kacholiya sir has survived huge loss at age 27 , He was almost bankrupt.

Recovering from those losses, he went on to earn ₹100 crore and later ₹1,000 crore.

PL capital bullish on #Acutaas chemical

Rating ~Accumlate

New growth avenue:---

- Battery chemicals

- prostrate cancer can be treated using darolutamide

-CDMO

- API

Dis-Investment

Amanta Healthcare Ltd

Why is it interesting?

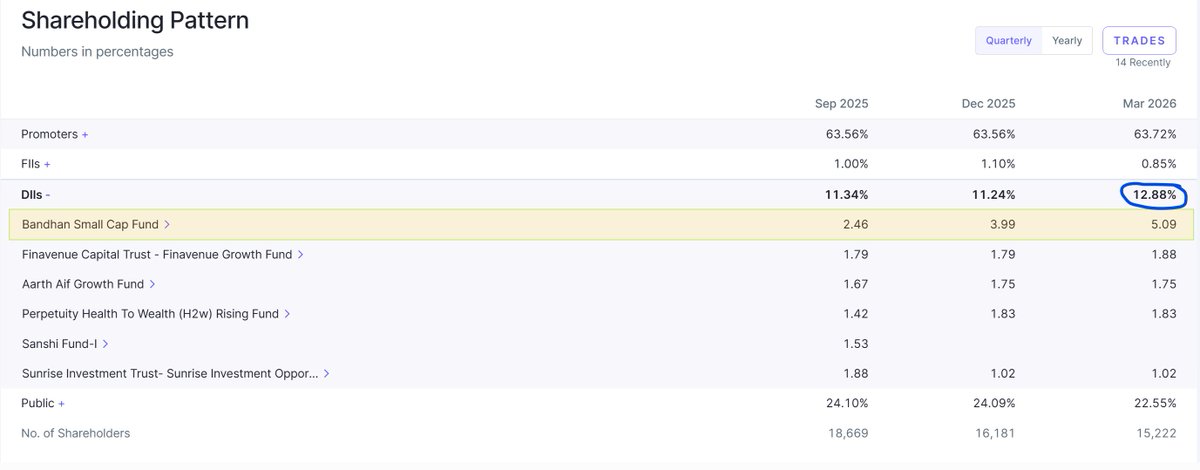

It's a 600cr Marketcap company, yet institutional investors hold around 12.5% of the shares. Notably, Bandhan Small Cap Fund has consistently increased its stake over the last three quarters, reflecting growing institutional confidence.

Another positive sign is that the promoter's last purchase was at around ₹150 per share, while the stock is currently trading near ₹160, indicating promoter confidence at levels close to the current market price.

Amanta Healthcare Ltd

Why is it interesting?

It's a 600cr Marketcap company, yet institutional investors hold around 12.5% of the shares. Notably, Bandhan Small Cap Fund has consistently increased its stake over the last three quarters, reflecting growing institutional confidence.

Another positive sign is that the promoter's last purchase was at around ₹150 per share, while the stock is currently trading near ₹160, indicating promoter confidence at levels close to the current market price.

🔍 Kilitch Drugs India Ltd Expands with New Nutraceutical Plant | Starts June 2026 | MCap 646.79 Cr

- Kilitch Drugs (India) Limited initiates production at its new Nutraceutical Manufacturing Block.

- Facility located at 24/2/1/1, Maldev Village, Pen Taluka, Raigad District, Maharashtra.

- Start date confirmed for 17th June, 2026.

- Stock listed on BSE (524500) & NSE (KILITCH).

Disc: Information provided in above tweet can be inaccurate, verify through the source i.e. attached image(s) & in reply before making any investment decision.

Kilitch Drugs Q4 FY26

Kilitch Drugs (India) Ltd was incorporated in 1978, which means this company has existed long enough to witness multiple pharma cycles, export booms, regulatory shifts, and probably enough FDA paperwork to fill a small library.

Read more - https://t.co/cC0TOLZr1o