2/

That is also the risk.

At this valuation, the market is not paying for SpaceX as it exists today.

It is paying for a long sequence of future outcomes:

Starlink scaling globally,

launch dominance continuing,

Starship reducing orbital costs,

defense demand expanding,

satellite connectivity becoming a major telecom layer,

and future space infrastructure becoming commercially relevant.

This may be one of the most important companies in the world.

But an IPO at this scale is not only a validation of the business.

It is a test of how much future dominance public markets are willing to price upfront.

The question is not whether SpaceX is exceptional.

The question is how much of that exceptionalism is already in the valuation.

1/

The SpaceX IPO is not a normal space listing.

If current reports are accurate, SpaceX is targeting one of the largest IPOs ever, with a valuation around $1.75 trillion and at least $75 billion raised.

Investor demand is reportedly close to 4x oversubscribed.

That tells us something important.

The market is not only trying to buy rockets.

It is trying to buy the infrastructure layer behind launch, satellite internet, defense, connectivity, and potentially space-based compute.

SpaceX is being priced less like an aerospace company and more like a strategic infrastructure platform.

This matters because index weight and risk contribution are not the same thing.

A stock that weighs 5% in the index does not automatically represent 5% of the risk.

Risk contribution depends on:

volatility,

correlation,

market beta,

and exposure to the same underlying narrative which is today AI.

That is where concentration becomes dangerous if you want to be diversified.

Buying the S&P 500 feels like diversification.

Today, the top 10 companies in the S&P 500 represent roughly:

40% of the index

32% of index earnings

48% of total index risk

That gap is the problem.

The largest companies do not only represent a large share of market value.

They represent an even larger share of the risk.

$60K is not the bottom.

And if you believe negotiations will suddenly end the war and send everything up, you are completely wrong.

Markets do not bottom on wishful thinking.

They bottom when pain is fully priced in.

We are not there yet.

Many of you will lost everything

IRAN AND OMAN DISCUSSING A PERMANENT HORMUZ TOLL:

IRANIAN ENVOY RE-OPENING STRAIT WILL ENTAIL COUNTRIES PAYING: AMIN-NEJAD

🔴Let me explain the consequences:

If the toll is charged per barrel, the math is direct.

If it is charged per ship, you divide the fee by cargo size.

For a VLCC carrying 2 million barrels:

- $0.5M toll = **$0.25/bbl**

- $1M toll = ~$0.50/bbl

- $2M toll = ~$1.00/bbl

- $5M toll = ~$2.50/bbl

- $10M toll = ~$5.00/bbl

So yes, the direct impact on Gulf barrels can become meaningful very fast.

🔴Market impact is bigger than the toll itself

Why?

Because the toll would sit on top of:

- war-risk insurance

- freight

- delays

- rerouting costs

- legal / sanctions risk

- and a higher scarcity premium on alternative barrels

A $1/bbl toll on Hormuz flows does not mean +$1 on all global oil.

Markets will look at:

- the marginal barrel

- the prompt spread

- physical tightness

- freight

- cracks

- and the risk that some buyers simply step back

🔴So the real takeaway is simple:

A Hormuz toll is not just a transport fee.

It is a new geopolitical cost layer on one of the most systemically important oil chokepoints in the world.

It's a new Gulf risk premium on OIL.

As always GOLD is the number one competitor of Treasuries when you want to be risk off you buy gold or bonds but if bonds are yielding 5.18%, gold become less interesting

The incentive to be risk off is becoming stronger, and everybody is full risk on now.

In other words it's time to consider taking some profit

🚨 US long-term rates are exploding at 2007 levels

The 30Y Treasury yield has pushed above 5.17%, the highest since 2007.

The 10Y is back around 4.6–4.7%.

🔴 Why yields are rising:

- sticky inflation

- oil/geopolitical risk

- massive Treasury supply

- rising term premium

- deficits the market no longer wants to finance cheaply

🔴CONSEQUENCES:

2/ Housing

30Y mortgage rates above 7% keep crushing affordability, slowing sales, and pressuring builders.

3/ US fiscal position

Interest expense is becoming one of the largest line items in the budget and is eating into federal revenue fast.

4/ Equities

Higher discount rates are a direct headwind for stocks, especially long-duration growth names.

If Treasuries yield 5%+, why you would risk to buy stocks ?

5/ Gold

GOLD is the number one competitor of Treasuries when you want to be risk off you buy gold or bonds but if bonds are yielding 5.18%, gold become less interesting

🔴What we think of the situation:

The incentive to be risk off is becoming stronger, and everybody is full risk on now.

In other words it's time to consider taking some profits.

This chart gets more interesting when you compare it to current market-cap rankings.

Institutional ownership rank:

1. Microsoft — 73.8%

2. Nvidia — 67.4%

3. Meta — 67.2%

4. Alphabet — 65.2%

5. Apple — 64.0%

6. Amazon — 63.1%

7. Tesla — 43.4%

But by market cap, the order is different.

🔴The biggest divergences:

- Microsoft is #1 in institutional ownership, but only #4 by market cap

- Meta is #3 in institutional ownership, but only #6 by market cap

- Alphabet is #2 by market cap, but only #4 in institutional ownership

- Apple is #3 by market cap, but only #5 in institutional ownership

🔴And then there is Tesla:

Still the smallest in the group by market cap, but dramatically less institutionally owned than every other Mag 7 name.

🔴The conclusion is simple:

Institutions are not equally bullish across mega-cap tech.

They appear far more concentrated in names like Microsoft, Nvidia and Meta, while names like Tesla still screen as structurally under-owned relative to the rest of the group.

So market-cap leadership tells you who is biggest.

Institutional ownership tells you where big money is most comfortable being long.

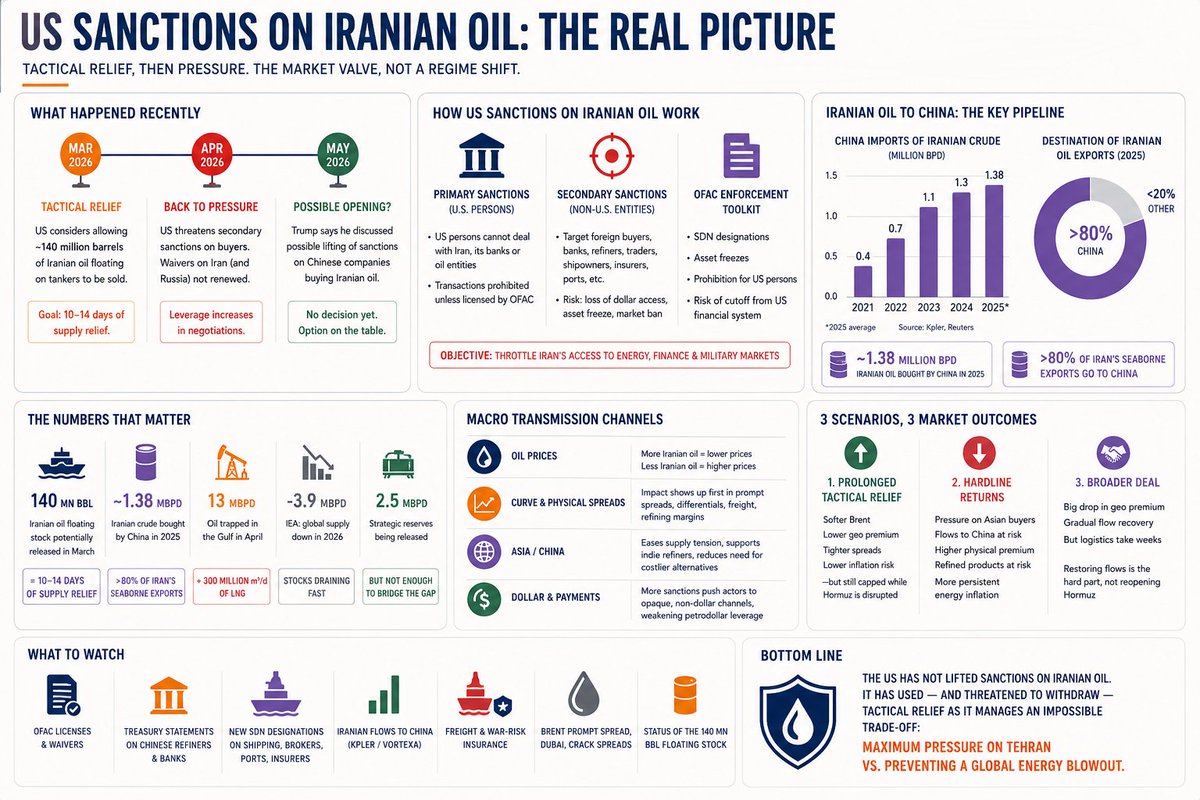

🚨 The US did not broadly lift sanctions on Iranian oil.

🔴1/ What happened was far more tactical:

- In March, Washington considered letting roughly 140mn barrels of already-floating Iranian oil reach the market

- In April, the tone flipped back to secondary sanctions threats

- In May, Trump signaled possible relief for some Chinese buyers, but nothing structural has been fully reset

🔴2/ That is the key point:

US sanctions on Iranian oil are no longer just a pressure tool on Tehran.

They are also a market valve.

🔴3/ Why it matters:

- China bought ~1.38mn bpd of Iranian oil in 2025

- That was >80% of Iran’s seaborne exports

- So even small tactical changes in sanctions enforcement can move physical balances at the margin

But none of this solves the real problem:

Hormuz is still the bottleneck.

So the market is stuck between:

- geopolitical pressure on Iran

- and the need to stop energy prices from blowing out

🔴4/ Conclusion

This is not a clean sanctions regime anymore.

It is a real-time attempt to manage an oil shock without admitting it.

🚨 The US did not broadly lift sanctions on Iranian oil.

🔴1/ What happened was far more tactical:

- In March, Washington considered letting roughly 140mn barrels of already-floating Iranian oil reach the market

- In April, the tone flipped back to secondary sanctions threats

- In May, Trump signaled possible relief for some Chinese buyers, but nothing structural has been fully reset

🔴2/ That is the key point:

US sanctions on Iranian oil are no longer just a pressure tool on Tehran.

They are also a market valve.

🔴3/ Why it matters:

- China bought ~1.38mn bpd of Iranian oil in 2025

- That was >80% of Iran’s seaborne exports

- So even small tactical changes in sanctions enforcement can move physical balances at the margin

But none of this solves the real problem:

Hormuz is still the bottleneck.

So the market is stuck between:

- geopolitical pressure on Iran

- and the need to stop energy prices from blowing out

🔴4/ Conclusion

This is not a clean sanctions regime anymore.

It is a real-time attempt to manage an oil shock without admitting it.

🚨ENERGY CRISIS IN A DANGEROUS PHASE

🔴1/ Here is what you're missing:

- The IEA estimates global oil demand is running roughly 6mn bpd above production

- Analysts think the shortfall is closer to 8–9mn bpd

- Over 2mn bpd of emergency SPR barrels are filling the gap, but many of those releases end in July

- Since the war began, global reserves have already fallen by nearly 380mn barrels

- The IEA says 76 countries have now introduced emergency measures, up from 55 at the end of March

🔴2/ That is the key point:

A large share of “stocks” cannot be fully drained without breaking the system:

Pipelines need pressure, refineries need continuity, storage tanks have minimum operating levels.

So the real risk is not “when do inventories hit zero?” But: when do markets hit operational stress first?

If Hormuz is not reopened soon, the next phase is not just higher oil.

It is:

- broader fuel rationing

- industrial shutdowns

- supply chain stress

- stickier inflation

- and rising recession odds