During last month, I executed a crypto arbitrage trade involving the ARIA token between @KCEX_Official and @Bybit_Official .

The strategy involved purchasing approximately 180,000 ARIA tokens on one exchange at a lower price and simultaneously selling on another exchange at a higher market price in order to capture the spread difference.

The trade achieved an arbitrage spread of approximately 1.59%, with the transaction completed successfully through market execution and liquidity balancing between exchanges.

This trade was part of my regular digital asset trading and arbitrage activity focused on exploiting temporary price inefficiencies across cryptocurrency exchanges.

🚨 ARIA Arbitrage Trade

Spotted a spread between @bitget Spot and @kucoincom Futures.

📈 Long ARIA on @bitget : $0.03566

📉 Short ARIA on @kucoincom Futures: $0.03607

💰 Entry spread: 1.39%

At first glance, 1.39% may not seem like much, but when combined with funding payments, these small inefficiencies can add up over time.

Additional edge:

💸 Funding Rate (@kucoincom Futures): +0.4439%

The strategy is simple:

✅ Buy the cheaper market

✅ Short the more expensive market

✅ Collect funding when available

✅ Wait for the spread to converge

No need to predict whether ARIA will pump or dump.

The profit comes from the price difference between exchanges and funding-rate inefficiencies.

Trading spreads, not predictions. 📊

🚨 95% Price Spread Arbitrage Opportunity on ethereum:0xcf5104d094e3864cfcbda43b82e1cefd26a016eb 🚨

Massive inefficiency spotted between two futures markets:

🔻 Buy @binance Futures: $0.0857

🔺 Sell @okx Futures: $0.1679

📊 Spread: +95.38%

💰 Potential profit: $616.75

📦 Trade size: 7,550 H

💸 Trading fees: only 0.14%

How the trade works:

1️⃣ Go LONG on @binance Futures where ethereum:0xcf5104d094e3864cfcbda43b82e1cefd26a016eb is cheaper.

2️⃣ Go SHORT on @okx Futures where ethereum:0xcf5104d094e3864cfcbda43b82e1cefd26a016eb is almost 2x more expensive.

3️⃣ Wait for the prices to converge and close both positions.

You don't need to predict whether the market goes up or down — the profit comes from the price difference between exchanges.

Even better, both sides have negative funding:

@binance : -0.0497%

@okx : -0.702%

This means funding can further improve the trade depending on the exact long/short funding mechanics.

This is how professional arbitrage traders exploit market inefficiencies — hunting spreads, managing risk, and letting the market close the gap.

What is Price Spread Arbitrage? 🤔

Price spread arbitrage is a strategy where you buy an asset on one exchange where it's cheaper and simultaneously sell (or short) it on another exchange where it's more expensive.

Example:

📈 Long lab:native at $15.00 on Exchange A (FUTURES)

📉 Short lab:native at $16.00 on Exchange B (FUTURES)

Spread = 6.67%

When prices converge, you close both positions and capture the spread.

The goal isn't to predict whether the market goes up or down — it's to profit from price differences between exchanges.

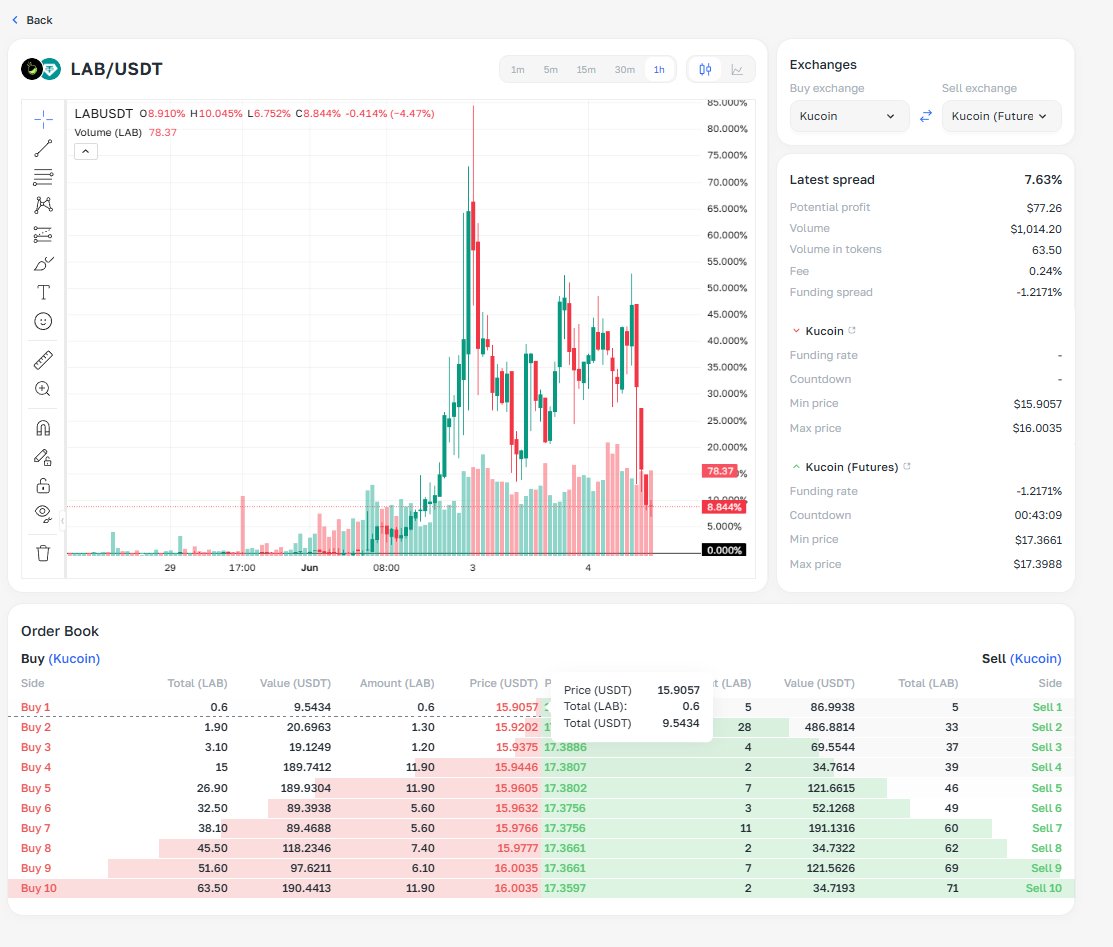

🚨 lab:native arb alert hitting different rn

@kucoincom Spot vs @kucoincom Futures spread: 7.63%

💰 Potential profit: $77.26

📦 Volume: $1,014

💸 Fee: only 0.24%

Spot sitting at $15.90 while futures are at $17.37 — that's a $1.47 gap waiting to be closed

Funding rate: -1.2171% (shorts getting paid)

This is the kind of inefficiency that doesn't last long 👀

🚨 lab:native Futures Arbitrage Trade

Spotted a 6.04% spread between two futures markets:

📈 Long lab:native on @Aster_DEX Futures at $15.05

📉 Short lab:native on @kucoincom Futures at $16.00

💰 Entry spread: 6.04%

The goal wasn't to predict whether lab:native would pump or dump.

The strategy was simple:

Buy the cheaper futures contract.

Short the more expensive futures contract.

Wait for the price gap between exchanges to converge.

Additional edge:

🔄 Funding on @Aster_DEX : -0.9574%

🔄 Funding on @kucoincom : -1.3875%

When spreads like this appear, price direction becomes far less important than the convergence itself.

That's why futures-to-futures arbitrage remains one of my favorite market-neutral strategies.

🚨 New Arbitrage Opportunity Spotted

$LAB showing a 30.71% spread between spot and futures on KuCoin.

📈 Buy Spot: $12.57

📉 Short Futures: $16.67

Spread: +30.71%

The idea is simple:

Buy LAB on the spot market.

Open an equal-sized short position on LAB futures.

Wait for the spread between spot and futures to converge.

At the time of the setup:

💰 Potential spread capture: ~30.7%

📊 Futures funding: -2% (additional edge for shorts if maintained)

This is a market-neutral trade. The goal isn't to predict whether LAB goes up or down — it's to profit from the price difference between the two markets.

Always manage:

✅ Position sizing

✅ Exchange risk

✅ Liquidity risk

✅ Funding rate changes

Another trade test-3:native

Entry spread: 2.40%

Long on @KCEX_Official at $0.014145

Short on @GateFutures at $0.014484

Position size: 1,248,000 TST

As the spread converged:

📈 Long PnL: -$394.60

📉 Short PnL: +$1,036.04

💰 Funding: +$225.86

Net Profit: +$641.44

The direction of the token didn't matter. The goal was simple: capture the price difference between exchanges and collect funding while waiting for convergence.

That's the power of exchange arbitrage. 🔄

🏆 Congratulations to solana:5eyib4qghYGHNh7VvxSFGYLFJSanjq9hug9fR52kksnm on winning the Champions League!

While everyone was celebrating the victory, I was celebrating an arbitrage opportunity on the solana:5eyib4qghYGHNh7VvxSFGYLFJSanjq9hug9fR52kksnm fan token.

Right after the final whistle, the market went crazy. The same token was trading at significantly different prices across exchanges:

📈 @binance : around $0.985–$1.10

📉 @Bybit_Official : around $0.8372

I immediately sold 716 solana:5eyib4qghYGHNh7VvxSFGYLFJSanjq9hug9fR52kksnm tokens on @binance for approximately $705.89 and bought back the exact same amount on @Bybit_Official for just $599.43.

💰 Profit: +$106 USDT in under 2 minutes.

The number of tokens I owned didn’t change at all — I simply took advantage of the price difference between exchanges while the market was reacting to solana:5eyib4qghYGHNh7VvxSFGYLFJSanjq9hug9fR52kksnm ’s historic win.

Football fans got a trophy. I got an arbitrage trade. ⚡

Case of perpetual arbitrage on $SPA with closed withdrawal +$1300 or 25% for small capital

Executed a $SPA spot + perpetual futures arbitrage after identifying a massive pricing inefficiency between spot and futures markets 📊

Trade setup:

• Bought $SPA on @HuobiGlobal spot around 0.0128 average

• Opened short perpetual positions on @GateFutures around 0.01682 average

That created an entry spread of roughly 31% between spot and futures pricing.

Positions were built gradually in parts to manage execution and liquidity more efficiently. As the spread compressed and futures prices converged closer to spot, positions were closed step by step.

Final result:

✔ ~25% return on deployed capital

✔ fully hedged exposure

✔ profit generated from spread convergence instead of market direction

This is why futures arbitrage is so powerful:

When pricing inefficiencies become extreme, the goal isn’t predicting whether the coin goes up or down — only waiting for the spread between markets to normalize.

Pure market-neutral arbitrage execution ⚡

+34% while $ARIA crashed 80% in an hour

April 2026. $ARIA token: minus $105M in market cap within 60 minutes. Auditors called the smart contract a "black box," followed by a coordinated dump of 45 million tokens. Panic.

What was happening on my end?

I was calmly closing positions in profit at that exact moment.

I got a notification that the ARIA price differed slightly between two exchanges. I went short (betting on a drop) where it was more expensive — and long (betting on a rise) where it was cheaper.

Like buying a dollar at one exchange office and immediately selling it at another for slightly more. Price risk = close to zero, profit comes from the spread between exchanges.

Result:

⬇️ Short: $0.794 → $0.426 — +141.7%

⬆️ Long: $0.748 → $0.459 — −107.1%

Net: +34.56% or $1,757

Why did it work?

ARIA's futures volume was 51x its spot volume — the market was skewed, and spreads between exchanges became massive.

Here is another profitable market-neutral arbitrage opportunity on $BROCCOLIF3B from April📊

Trade setup was based on both:

✔ price spread inefficiency between exchanges

✔ funding rate imbalance on perpetual futures

Exchanges used:

@KCEX_Official ↔ @GateFutures

Entry spreads:

• 1.85% on first setup

• 1.56% on second setup

Execution:

Opened hedged positions where the token traded cheaper on one exchange and more expensive on the other, while simultaneously collecting positive funding payments from the futures side.

Result:

💰 Spread convergence profit

💰 Additional funding income

💰 Fully hedged exposure against market direction

Trade results:

• +777 USDT on first execution

• +686 USDT on second execution

What makes this strategy powerful is that profit doesn’t rely on predicting whether the market goes up or down.

The edge comes from:

→ temporary pricing inefficiencies

→ funding rate imbalance

→ convergence between exchanges

Pure cross-exchange arbitrage execution ⚡

$93,750 per day — without any price direction predictions

A whale bought $7.5 million worth of aster-2:native and simultaneously opened a short position for the same amount. The price can go up or down — it doesn't matter to them. It's like renting out an apartment while betting against rent increases: one offsets the other, and money flows in from the difference.

The mechanics are simple: when the market is overheated and everyone wants to go long (betting on price increases), the exchange charges them a fee — funding — and gives it to those holding short positions. The whale holds a short → receives payouts from the crowd of long traders every hour. No directional price risk.

Numbers:

— Spot purchase: $7,500,000

— Short perpetual (with 3x leverage): 6,486,000 aster-2:native

— Funding rate: ~450% APR (peaks up to 1000%)

— Profit: ~$93,750/day → ~$2.8M per month

These opportunities last only hours or days — until the rate normalizes to around 0.01% per 8 hours.

This strategy can be used with both small and large capital.

The advantage of spot + futures arbitrage is that the trade is hedged, meaning the focus is not on predicting market direction but on capturing the spread difference between exchanges.

Smaller accounts can scale slowly with lower risk, while larger accounts can benefit from bigger funding payments and larger spread opportunities.

The bigger the market inefficiency, the bigger the opportunity 📊

Executed a futures + futures funding rate arbitrage on $ID between @binance and https://t.co/fNP1Q3jMG4 📊

Trade setup:

• Long $ID perpetuals on @binance where funding reached -2.0000%

• Short $ID perpetuals on https://t.co/fNP1Q3jMG4 where funding reached +2.0000%

At the same time, https://t.co/fNP1Q3jMG4 perpetuals were trading at a premium compared to @binance , creating a strong market-neutral arbitrage opportunity.

This setup allowed profit from:

✔ funding payments

✔ spread convergence between exchanges

The trade was fully hedged, meaning direction mattered far less than the spread itself.

As long as the funding imbalance normalized, the trade stayed profitable regardless of market direction.

Pure cross-exchange futures arbitrage ⚡

500$ in just 5 minutes with a spot + futures strategy

Executed a $MOBILE spot + perpetual futures arbitrage between MEXC and ByBit after identifying a temporary 2.13% spread between markets.

Trade setup:

• Shorted $MOBILE perpetuals on @Bybit_Official around 0.430

• Bought $MOBILE on spot market on @MEXC around 0.421

The goal wasn’t to predict direction — only to capture the spread convergence between spot and futures markets.

If price moved higher:

The spot position gained value while the short hedge lost less, keeping the trade profitable overall.

If price moved lower:

The short perpetual position generated profit while spot lost value, again keeping the overall position positive.

Once the spread narrowed and prices converged, both positions were closed for profit.

This is why spot + futures arbitrage is one of the most powerful market-neutral strategies in crypto:\

✔ hedged exposure

✔ reduced directional risk

✔ profit from inefficiencies instead of predictions

✔ scalable execution across exchanges

Pure spread capture 📊

vanar-chain:native arbitrage is getting interesting right now.

Current spread between @MEXC spot and @bitget futures is around 9.8%, which is massive for a relatively liquid market.

At the moment:

Buy side liquidity is sitting on @MEXC spot

Sell side liquidity is on @bitget futures

Funding spread is minimal

Main opportunity comes from the price dislocation itself

The important part is that this spread likely won’t fully converge until withdrawals on the vanar-chain:native network are enabled again on @MEXC .

Right now, capital and tokens cannot move efficiently between exchanges, so the market becomes fragmented:

spot price on one venue trades independently,

futures/perp market on another venue trades at a premium,

arbitrage capital gets trapped.

Once withdrawals reopen, market makers and arbitrage traders will probably compress the spread very quickly through cross-exchange balancing.

Until then, the inefficiency can persist much longer than most traders expect.

📊 Few Crypto Arbitrage Trades from March and April

Real cross-exchange arbitrage executions across MEXC, GATE, KuCoin, BitGet, KCEX & Binance.

✔ Funding rate capture

✔ Hedged spread trading

✔ Market-neutral setups

✔ Transparent PnL tracking