NEW Crypto Yield Curve podcast!

🎙️ How Should We Value Crypto? (~17 mins)

A recent debate between @hosseeb and @santiagoroel exposed industry pricing doubts

Rheo core explains why spreadsheets misprice crypto, exponentials overreach – and which onchain signals truly matter

1/ DeFi runs on credit, but most lending floats with utilization.

@SizeCredit prices credit by date, so borrowers lock costs and lenders lock cash flows.

Bond-style funding you can enter and exit before maturity.

🧵👇

🎙️ The Crypto Yield Curve podcast returns!

🐋 Scaling Size

Tune in as we explore how to scale the multi-trillion-dollar fixed-rate credit market, what’s new and upcoming for the protocol, and fresh Earn / Very Liquid Vaults alpha 👇

NEW PT MARKET 🐋

Juice moar profit from your @ResolvLabs PTs by sniping a low fixed rate against them

Move fast and you’ll pay just 6.28% APR to borrow until Sept 24

Collateral Asset: PT-wstUSR-25SEP

Borrow Asset: USDC

https://t.co/fnkc252PtB

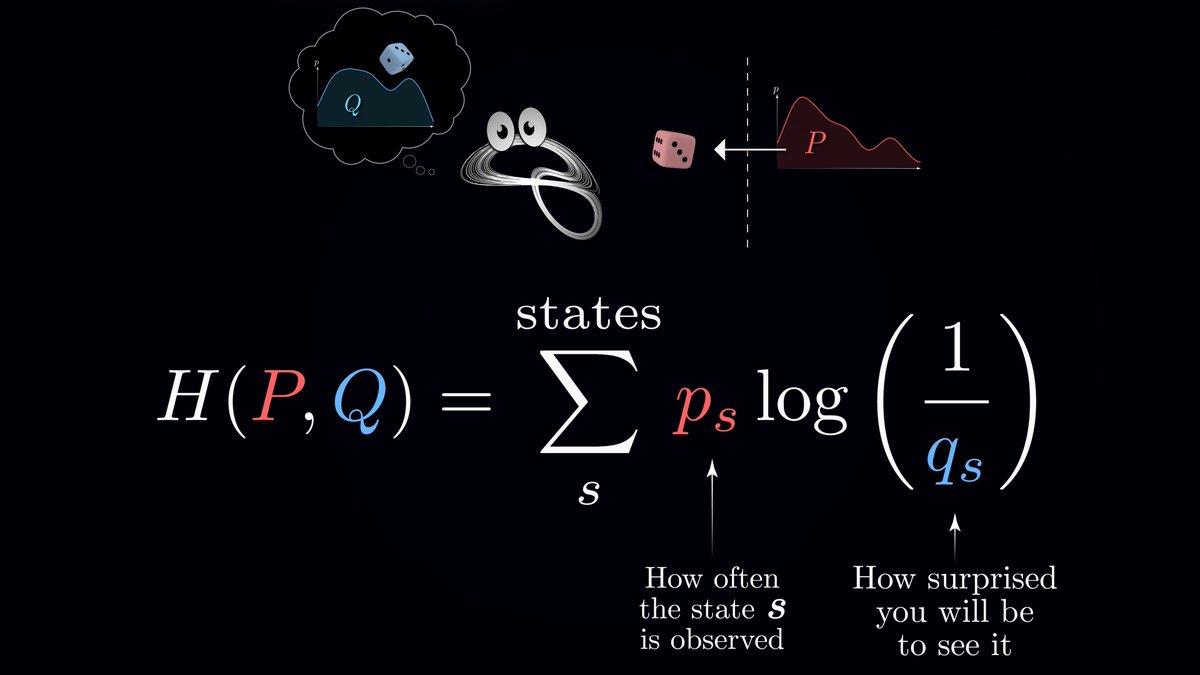

8/12 Cross-entropy measures the average surprise when we use our model to predict outcomes from the true (unknown) distribution. A key property: it's always greater than or equal to the true entropy. This means that an imperfect model can only increase our average surprise, never decrease it

Let’s get a measure of Size Credit and what it does!

While variable, pool-based protocols like @aave found PMF, fixed-rate products have met limited success due to fractured liquidity across dedicated AMMs.

This resulted in high slippage and poor UI, with users being forced to pick pre-set maturities.

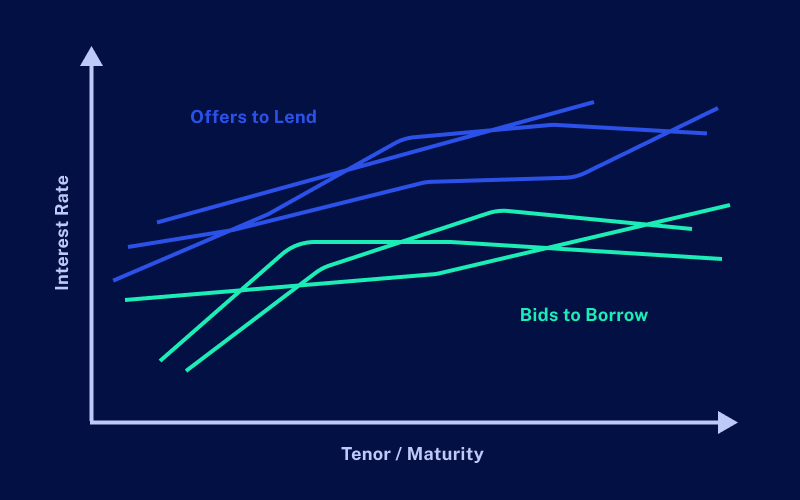

Size Credit is built on an order book model where offers are expressed like yield curves to enable the efficient pricing of fixed-rate products, while maintaining unified liquidity across the full maturity spectrum.

In other words, users can choose any rate or duration, down to the hour, when lending or borrowing.

Lending on Size

Lenders can currently deposit $USDC to lend at market rates. Or… they can create their own yield curves by specifying the rates they want to receive at different maturities (i.e. limit orders).

For example, a lender may specify a continuous curve defined by the points (1 month, 2.5%), (3 months, 3%), and (1 year, 5%). If a borrower then wanted to borrow for 4 months, they would pay ~3.2% if matched with this lender.

Any unmatched capital earns a variable interest rate through @aave and lenders can exit any time via the order book.

Borrowing on Size

Borrowers, again, can borrow at market rates using $ETH as collateral. Or… they can also create their own yield curves to define the rates they want to pay at specific maturities.

Large-sized loans may span multiple lender offers and liquidity will be automatically aggregated with a weighted average rate.

Borrowers may take multiple loans and only need to maintain one collateralization ratio across all of their loans. Collateral may be added or withdrawn, permitted the minimum collateralization ratio thresholds are not exceeded.

Complex Credit Strategies

In addition to the above, the credit order book can be used to conduct more complex credit operations. For example, bids to borrow also double as offers to sell credit, and can be used to structure active or passive credit dealing strategies.

Ready to get started on Size Credit? Head to the app today!

The continuity of spacetime is not simply an observation, it is the mathematical fiction that continua can exist, combined with the intuitions of a human brain that has entrained a smoothly scaling 3D engine as part of its world model on itself.

@thrice_greatest emotions also as meta data of how your brain is responding to, system 2 / higher thinking has your own thoughts being perceived. I think a lot of things get freaky when you let a model perceive itself