@CAHimankSingla@theicai So, no CA can generate more than 60 UDINs for tax audits in a FY (except for tax audits of presumptive assessees declaring lower profits). Is that so?

@AbhasHalakhandi Why argue for tax cuts for firm/LLP by comparing them with companies? Standalone, there is compelling case for reducing tax rates for firms, LLPs and companies to effective rate of 17%.

Kalidas in his Raghuvamsh records that when Sri Rama's ancestor King Dileep ruled,+++

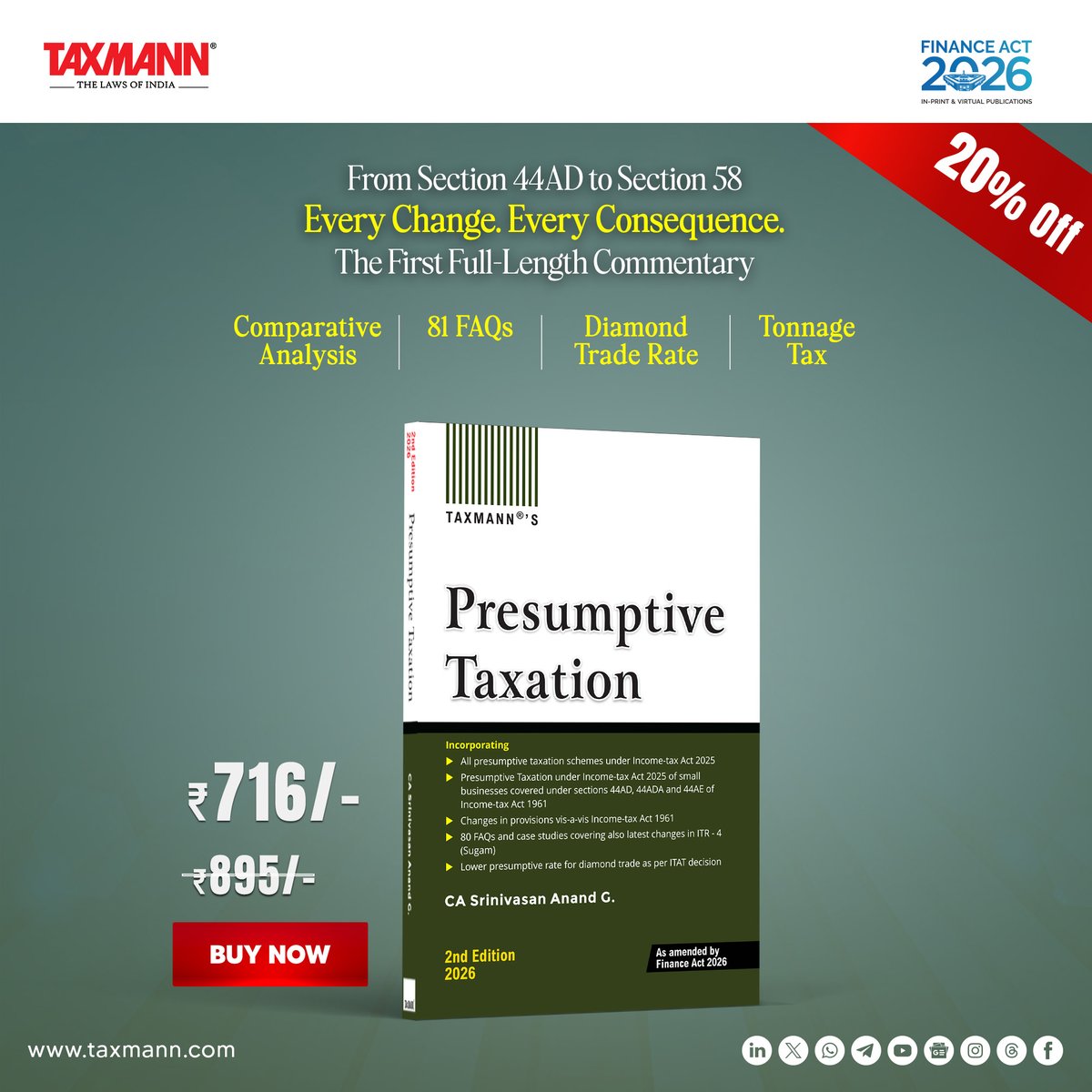

Section-wise Commentary on Presumptive Taxation under ITA 2025—Section 58, Section 61 & Tonnage Tax (Sections 225–235) with Comparative ITA 1961 Analysis, 81 FAQs, Rule 48 CBDC, Diamond Trade Rate & 4 Appendices

Preview: https://t.co/OXg3fInt2I

Like it? Buy now with Free Expedited Shipping & get a Limited Period Discount! https://t.co/hSwPJ7535x

#TaxmannBooks #FinanceAct2026 #IncomeTaxAct2025 #PresumptiveTaxation #Section44AD #TonnageTax

@KUNGFU_PANDYA_0 Hardik Pandya still has everything . He is winner of back to back T20WCs.

What he does in IPL or gully 🏏 is irrelevant. He has always performed where it matters.

This has been addressed by the IT Act,2025. Facility of lower TDS or NIL TDS extended to all TDS provisions. Partners can obtain lower or nil TDS for Sl. No.7 of the Table in Section 393(3) (corres. to 194T). TDS on payment basis incentivising partners to reinvest in firm

The situation in most Small Partnership Firms due to #194T is like this:

1. TDS of 10% being deducted on per partner having 20001 to 10 Lakh Business Income.

2. Majority of these partners are having personal income <= 12 lakh.

3. Most of them will take refund of this TDS deducted.

This is causing working capital blockage of TDS for 3-6 months.

Either the TDS rate needs to be reduced, or it needs to go away entirely.

#incomeTax

@CAHimankSingla@Abhinavaag Problems have been addressed in ITA 2025. Lower or nil TDS certificate can be obtained for SL. No. 7 of Table in Section 393(3) .

Further, TDS deductible under ITA 2025 on interest or remuneration to partners only on payment basis...meaning incentivising partners to reinvest more

Yes. How to determine actual profit when assessee does not maintain books ?

If he is to show actual profit,then he might as well maintain books and get them tax audited.

Presumptive is estimated basis & not accurate. That is why++ (1/2)

+ Section 44AD(4)/58(7) requires assessee to avail Section 44AD/ Sl. No.1 of Table in Section 58(2) for 6 consecutive years before opting out so that assessee benefits in some years and ITD in others and there is averaging out. (2/2) #PresumptiveTaxation