Private Person,

Financial Analyst, Qualified Accountant, Precious son of the most-high, Content Writer and Developer, Tutor, lover of music, and a United fan.

The other day, we celebrated a credit rating upgrade by the international credit agency, S&P. The events over the past few days just explains how the government (across all arms and tiers) make one step forward and two steps backwards.

A country does not become a $1 trillion economy simply because oil prices rise or because GDP numbers look bigger on paper.

A trillion-dollar economy is built when millions of people can safely learn, work, move, invest, build companies, transport goods, and plan for the future with confidence.

Industrial economies are built on efficient movement:

of people

of goods

of raw materials

of labour

of capital

Insecurity disrupts all of them.

It's crazy when the basic necessity becomes luxury.

Production and productivity will be low when basic infrastructures and amenities are not adequately supplied. Well we are used to seeking for alternative but what's the real work of the govt?

You are a young lady finance professional? Consider reading and watching videos about these two remarkable C-suite female executives. Proper gargantuans. I have watched tons of videos about these two.

Indira Nooyi

✑ Indira Nooyi's emergence as CEO of PepsiCo in 2006 was symbolic. Although she was not the first person of colour to lead a Fortune 500 company, she was one of the longest-serving and most influential during her time.

✑ She started out in strategy consulting at Boston Consulting Group (BCG), had a stint at Motorola in the corporate strategy and planning team, and then joined PepsiCo in 1994. From there, she rose to head of corporate strategy, then CFO (2001 to 2006), and then CEO (2006 to 2018).

✑ During her tenure as PepsiCo's CEO, the franchise shifted from "soda company" to a diversified food and beverage giant. She particularly led the acquisition of Quaker Oats Company. Learn from her story (she is an excellent speaker too).

Jane Fraser

✑ She was the first woman to lead a major Wall Street bank. Fraser broke into the core power seat of global finance by joining Citigroup at a time when the bank underperformed peers like JPMorgan Chase and Goldman Sachs.

✑ The business had become overly complex and fragmented globally, and Jane Fraser came in to transform the bank.

✑ Her efforts include exiting consumer banking in multiple countries and refocusing on core strengths: institutional clients, cross-border banking, and wealth management.

✑ Fraser studied Economics at the University of Cambridge and secured an MBA from Harvard Business School. She started her career at McKinsey, where she rose to Partner.

✑ She joined Citigroup in 2004 and rotated across investment banking, Latin America head, CEO of U.S. Consumer Banking, and CEO of Global Consumer Banking.

✑ A key achievement remains navigating Citigroup through the Global Financial Crisis.

———————————————————————

Funny how both women started in strategy consulting (eyeing you folks that like to parrot it that consultants do not make good CEOs).

I can write on the Nigerian FX market all day and will not get bored. I want to provide clarity on some of the comments from my previous post, especially those on the CBN's FX intervention and FX liquidity.

1. Is CBN’s FX intervention in the market economically sensible?

Background story, the CBN recently allowed the BDCs to start accessing dollars ($) at the official market, selling 150k per week to each of the BDCs. Some have questioned the reasonability, suggesting that the CBN may be force-fitting the currency or intentionally forcing an appreciation. What does basic economics suggest? There are different types of FX regimes, and Nigeria currently runs a managed float regime. Under this regime, currency changes daily based on market demand, but occasionally, the central bank is permitted to intervene, especially when the currency is drifting from its fair value either because of low $$ liquidity or excessive liquidity.

2. Is there adequate $$ liquidity in the Nigerian FX market?

To get this, check daily FX turnover (averaging over 538 million in 2026 vs $400 million in 2025). Also, check major sources of FX inflows into the country; you will notice that FPI and remittances are stronger, and trade is in a surplus position. Additionally, the FX reserves are currently at over $50.0 billion, the highest in over a decade. So, the market is adequately liquid and not encumbered.

3. So, why is there a disparity between the parallel market and the official market?

FX liquidity drought in the parallel market, as most FX supplies are not channelled through the official market.

KYC requirement and the process for getting $$ from the official market is not easy, filling form M and the like. You can't blame the CBN, which continues to make sure all dollar demands are genuine and not for speculative purposes. As such, some corporations and retailers have had to depend on the parallel market for suppliers.

4. On a final note

- CBN’s monthly FX supply to BDCs is like $50.0 million. This is materially small, compared to pre-covid supply of around 770 million (average between 2017 and 2019)

- The market is still largely determined by demand and supply.

-Just to mention, the parallel market was largely stable before the CBN announced plans to increase intervention.

The NGX Tollgate Economics: Paying Rolls-Royce Prices for a Camry Ride

Let us be honest. We Nigerians love a good hustle. We love the idea of making our money work for us while we sleep. It is the capitalist dream, isn't it? You save some Naira, identify a solid company like Dangote Cement, SEPLAT, MTNN, Aradel, Vitafoam, FBN or Zenith Bank, et al, buy a slice of ownership, and watch it grow.

It sounds simple. It should be simple.

However, there is a silent friction in our financial machinery that is grinding retail investment to a halt. It is not market volatility. It is not the exchange rate (though that is a headache for another day). It is the exorbitant, confusing, and frankly, punitive cost of simply buying and selling shares on the Nigerian Exchange (NGX).

If you are an average Nigerian trying to build wealth through stocks, you are starting every race five meters behind the starting line, carrying a backpack full of rocks. It is time we unpack this backpack and ask the hard questions of the folks who put the rocks there.

The Global Context: A Game of Inches vs A Game of Yards

To understand how absurd our current situation is, we need to look outside our borders.

Over the last decade, a revolution in global finance occurred. In the United States, the world's largest capital market, trading costs for average investors effectively went to zero. Giants like Fidelity, Schwab, and the disruptor Robinhood realised that charging people $10 to buy a stock was obsolete. They eliminated commissions.

Today, if a plumber in Ohio wants to buy $1,000 worth of Apple stock, it costs him essentially $1,000. Maybe a few cents in regulatory fees, but it'ss negligible. The friction is gone.

Now, let us look at Nigeria.

If a plumber in Surulere decides to buy ₦100,000 worth of MTN Nigeria stock, and then decides a month later to sell it, that "round trip" transaction is not free. It is not cheap. It will cost him, on average, over 4% of his capital.

Let that sink in. Four percent. Just for the privilege of moving your money in and out of the market.

Before the stock price moves up by one Kobo, you are already down significantly. You need the stock to rally by at least 4.5% to break even. In a world where an 8-10% annual return is considered decent, giving away half of that to pay the "gatekeepers" is a tough pill to swallow.

The African Peers: Even the Neighbours Are Cheaper

"But wait," the apologists might say, "Nigeria is an emerging market. We have infrastructure costs. You cannot compare us to Wall Street."

Fair enough. Let us compare ourselves to our peers.

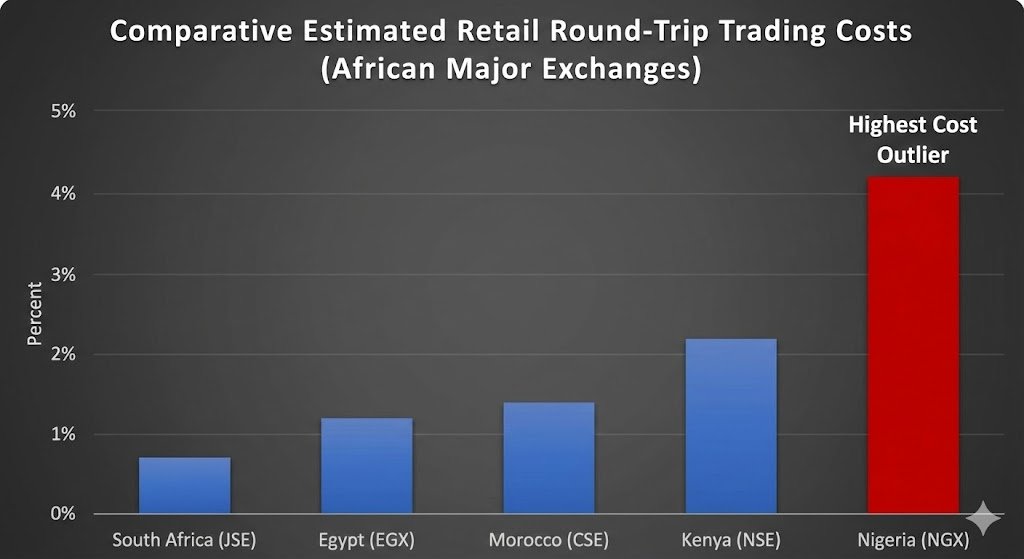

If you trade on the Johannesburg Stock Exchange (JSE) in South Africa—the most sophisticated market on the continent—your total round-trip costs as a retail investor are likely between 0.6% and 1%.

In Egypt or Morocco, you are looking at perhaps 1% to 1.5%.

Even in Kenya, which has its own bureaucratic hurdles, the costs are significantly lower than ours.

Nigeria, the self-proclaimed "Giant of Africa," has achieved the dubious distinction of having some of the highest equity trading costs not just on the continent, but in the investable world. We are trying to attract foreign portfolio investment and encourage domestic retail participation. However, we have erected a tollgate at the market's entrance that charges Rolls-Royce prices for a Camry.

Why is it so expensive here?

The Autopsy: Dissecting the Nigerian "Layer Cake" of Fees

If you ask an average investor what they pay to trade, they might say, "Oh, my broker charges me about 1.3 %."

That is true, but it is a dangerous half-truth. The broker's commission is just the icing on a very dense, very expensive cake.

The problem with the Nigerian cost structure is that it is a multi-layered stack of statutory fees, levies, and taxes, all calculated as a percentage of your transaction value. It is not one big fee; it is death by a thousand cuts.

Let us break down this "layer cake" so everyone—from the seasoned trader to the university student opening their first investment app—can understand where the money vanishes.

When you click "Buy" or "Sell" on the NGX, here are the hands that dip into your pocket:

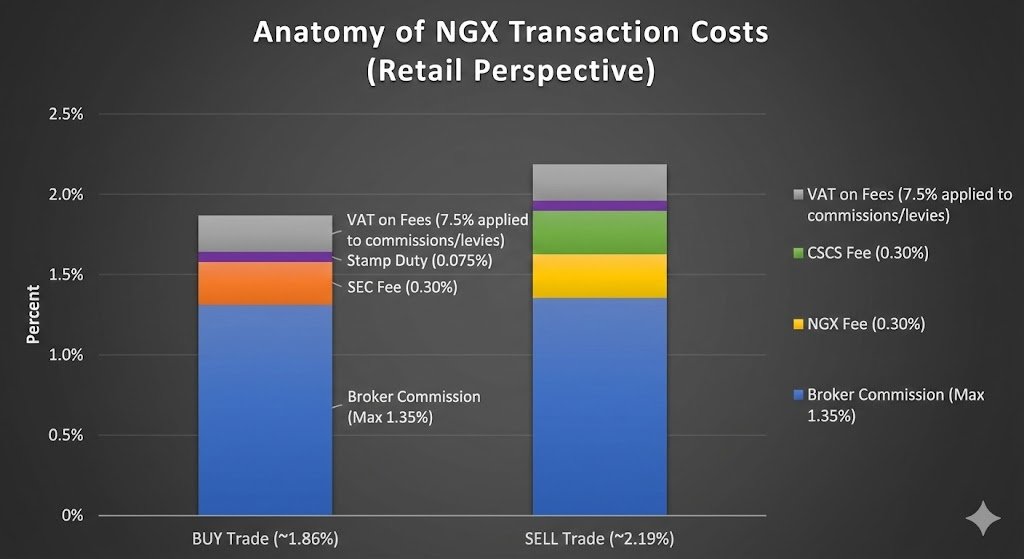

1. The Stockbroker (The Agent)

This is the person or firm executing your trade. The regulators have capped their maximum fee at 1.35% of the trade value. Most brokers charge close to this maximum for retail clients because, frankly, the other costs they face are high too.

2. The SEC (The Referee)

The Securities and Exchange Commission is the apex regulator. They ensure the rules are followed. To fund their operations, they take a slice of your trade. This is currently set at 0.30% (usually on the buy side).

3. The NGX (The Marketplace)

This is the exchange itself, the platform where the buyer meets the seller. Like renting a stall in Balogun market, you have to pay the market owner. The NGX Group charges a 0.30% fee (usually on the sell side).

4. The CSCS (The Vault Keeper)

The Central Securities Clearing System is the engine room. They make sure that when you pay cash, you actually receive the electronic shares in your account, and vice versa. They are the custodians of trust. For this vital service, they charge a fee, also around 0.30% (usually on the sell side), plus smaller transaction alert charges.

5. The NRS (The Taxman) - The Double Whammy

Here is where it gets really painful. The government needs its share, and they take it in two ways:

✅ Stamp Duty: A federal tax on financial instruments. That is another 0.075% (approx.) shaved off your contract note.

✅VAT (The Tax on the Tax): This is the kicker. The standard 7.5% Value Added Tax is applied to all service fees mentioned above: the broker commission, the SEC fee, the NGX fee, and the CSCS fee. You are paying tax on the fees you pay to trade

The "Sticker Shock" Math 🧑🔬

When you add all these percentages up—the broker, the regulator, the exchange, the clearer, the stamp duty, and the VAT on top of everything—the math is brutal.

Buying shares costs you roughly 1.8% to 1.9% in fees. Selling those same shares costs you roughly 2.1% to 2.2% in fees.

Total Round Trip: Over 4%.

Imagine you are buying ₦1,000,000 worth of stock. Before you even own the shares, almost ₦19,000 in fees has evaporated. When you decide to sell that N1,000,000 position, another N22,000 vanishes.

That is ₦41,000 of friction on a ₦1 million investment. That is real money. That is school fees. That is a rent supplement. Furthermore, it has gone regardless of whether you made a profit or a loss on the stock itself.

The Consequences: Why This Hurts Us All

Why should the average Nigerian, or even the regulators, care about this? Isn't this just rich people's problems?

Absolutely not. A vibrant stock market is essential for national wealth creation. The current fee structure is actively damaging that goal in three critical ways.

✅1. It Kills Liquidity and Encourages Hoarding

Liquidity is the lifeblood of a market. It is the ability to easily buy or sell without causing wild price swings. When it costs over 4% to enter and exit a position, investors become paralysed.

If you buy a stock and it goes up 3%, you should be happy. Nevertheless, in Nigeria, you cannot sell it to lock in that profit because the transaction costs would turn your 3% gain into a 1% loss. So, you hold. You wait. The market becomes stagnant. We do not have a "trading" market; we have a "buy and pray it doubles over five years so the fees do not matter" market.

✅2. It Fuels Capital Flight to Crypto and Foreign Apps

Nature abhors a vacuum, and capital abhors friction. Young Nigerians are some of the most astute, tech-savvy financial actors globally. They know how to do the math.

When a 21-year-old sees that they can trade Bitcoin on Binance for a 0.1% fee, or buy Tesla stock on a foreign app for zero commission, why on earth would they bring their liquidity to the NGX to pay 4%?

We are driving the next generation of investors away from our national exchange because our pricing model is stuck in the 1990s. We are forcing them to export their capital to more efficient markets.

✅3. It Depresses Asset Prices

High transaction costs act as a tax on investment. Basic economic theory tells us that if you tax something heavily, you get less of it. Because trading Nigerian stocks is so expensive, investors demand an "illiquidity discount." They are willing to pay less for the shares because they know how much it costs to get out of them. This keeps the valuations of our best companies artificially low.

An Appeal to the Regulators

This address is not meant to disparage the hardworking professionals at the SEC, NGX, or CSCS. We understand that market infrastructure costs money to run. We need a strong regulator, a robust exchange, and a secure clearing house.

However, we must recognise that the current aggregate cost structure is unsustainable and counterproductive. We cannot tax our market into prosperity.

It is a call for a coordinated, high-level review of equity trading costs in Nigeria by all stakeholders—the SEC, NGX Group, CSCS Plc, the Association of Securities Dealing Houses of Nigeria (ASHON), and, obviously, the tax authorities.

We need to ask hard questions:

1⃣Can we cap the statutory fees? Instead of percentages that scale endlessly with trade size, can we introduce flat caps for regulatory charges on larger trades to encourage institutional volume?

2⃣Can we review the VAT application? Applying VAT to regulatory levies feels punitive. Is there room for a waiver or reduction for capital market activity to spur growth?

3⃣Can brokerage commissions become more competitive? While brokers need to survive, the current 1.35% maximum often becomes the default. How can technology be leveraged to reduce execution costs, enabling brokers to pass savings to clients?

If we want the NGX to be the premier investment destination in Africa–if we want to achieve the Federal Government's goal of a $1 trillion economy–we need a capital market that is accessible, liquid, and efficient.

Right now, our market is like a beautiful luxury store with a bouncer at the door charging a ₦5,000 entrance fee. People look through the window, admire the goods, then walk away to shop elsewhere.

Let us lower the tollgate fees. Let the market breathe. Let Nigerians participate in their own economy without paying a penalty just for showing up.

It is time to cut the cake. 🎂

While it is common to find Equity Research Analysts, it is rare to come across analysts whose primary focus is on fixed income research. This is because of the knowledge gap in the space, making analysis on the Nigerian fixed income to not be up to standard as equities research.

Based on the foregoing, Gifted Analysts is proud to announce a collaboration with @ecoscenti to train Analysts on standard fixed income research and practical trading techniques. This training will also be covering macroeconomics (with emphasis on inflation, exchange rate, and fiscal balance modeling) that have to do with fixed income analysis. It is expected to be a two-month program, starting in May 2026.

Kindly be on the lookout for further details.

The Bull Run.

My algorithm has been about the Nigeria Stock Market and numerous takes about the bull run.

Let's just take a few minutes to talk about investing.

I believe this will be helpful. Let's dive in

Investors in the Nigeria market have been smiling steadily due to the up thick prices of shares. However, it is important to note that this thread wouldn't be forever.

Some people have questions like is this or that company still a good buy at the current price?

Key takeaway:

Value investing focuses on a company's intrinsic value and long-term growth, while opportunity investing relies on market trends and short-term gains.

Both approaches have their risks and rewards however, there is a lesser devil. What's your investing style?

OI focuses on;

Mkt momentum: Investors chase stocks with rapid price increases, hoping to ride d wave.

Speculation over fundamentals: Less emphasis on a company's financials & more on mkt sentiment.

Short-term focus: Opportunity investors often look for quick gains, buying.

This is getting too long 😔.

Let's move to the other part, the opportunity investors

Opportunity Investing

Opportunity investing, often driven by FOMO, involves making investment decisions based on market movements and trends rather than fundamental analysis. Fast money 😉

Warren Buffett, a legendary investor, is a prime example of value investor. He looks 4 companies with strong fundamentals, durable competitive advantages, & talented mgt.

I strongly believe dat d best way to nt lose money in d long run in dis mkt is 2 invest in value and wait

They invested based on d value they saw. In investment, time is d greatest teacher bcox either you are right or wrong, time will tell.

NGX market is looking so great now but few years ago it was bloody. Those who kept on investing then saw value & time is proving them right

Value investing is often a long-term strategy, riding out market fluctuations. Few months ago MTN was trading below #200 but now it's currently trading above #700.

Some people invested at that point even when the prices was going down. They did that because they saw value..

If you can't speak or understand how a company generates or tends to generate #1 which we term "Business model", I don't think that company is worth investing in.

Aside from understanding how value is being created, value investors don't just invest for the now...

So how do company create value?

Value creation: Companies create value for investors through:

- Earnings growth

- Dividend payments

- Increasing book value

There are several factors that speak to earning growth and that will be a conversation for another day

With fundamental analysis, we dive deep into the strategy, policies as well as understanding the brain behind the company. In fact, we look into the industry the company is operating to see if there is indeed value to be created in the future.

In value investing, fundamentals are key: Value investors analyze a company's financials, management, industry trends, competitive advantage, and growth prospects.

Fundamental analysis helps one understand how value is created. How the company makes money...

Value Investing

Value investing is an investment approach that focuses on buying stocks of fundamentally strong companies at a price lower than their intrinsic value. It's about understanding the true worth of a company and investing when the market undervalues it.