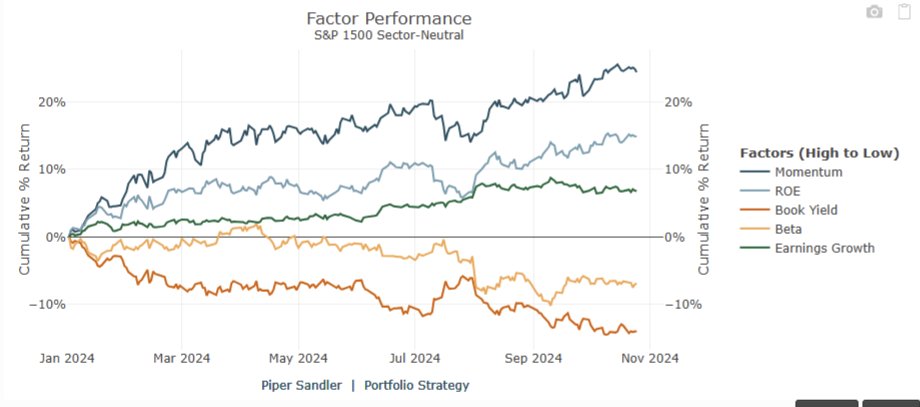

We track over 100 sector-neutral long/short factor portfolios. Momentum is the best-performing factor in '24 by a country mile. Also atop the list is quality (ROE) and growth (our top 2 themes in '24). High beta and deep-value portfolios have underperformed all year. I think this is a reflection of the bifurcated earnings backdrop. Higher rates for longer = momentum & quality outperformance for longer? #macro #HOPE

Might share a clip of this so folks on fintwit can better understand what a Wall St strategist does (it’s minimally about whether the SP500 is going to rise/fall, far more about process and positioning). Would you all be interested to see? Below is an image, not a video link. 😉#macro #hope

Very quickly, higher interest rates have gone from just impacting leadership in recent weeks to now weighing on the broad indices as 10yr yields approach 4.25%. To be sure, the flip-flopping of the rates-equities correlation has been dizzying. $SPY #hope#macro

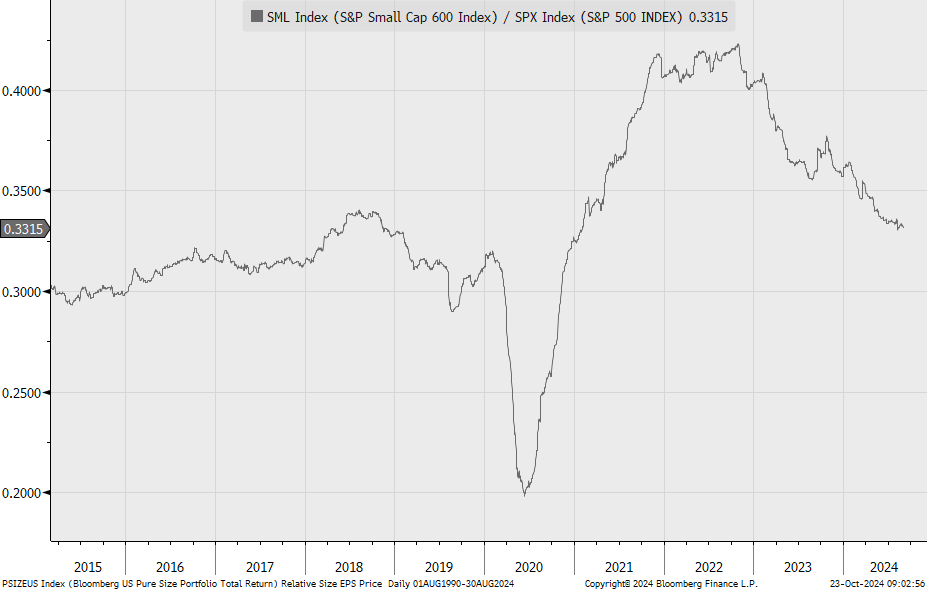

Small-cap earnings continue to lag S&P 500 (chart), explaining sustained larger-cap equity leadership. In my #HOPE framework, a rebound in leading housing data (apps, permits, starts) is the green shoot that has led to smaller-cap earnings (and price) outperformance. Quality leadership likely until we see that inflection. #macro #HoPe

We've recommended a "quality" overweight to our clients for the past two years - i.e., owning stocks with higher profitability, EPS growth, larger cap and stronger revisions. Quality stocks are also the driver of 2024's record performance in momentum strategies. A soft landing has historically been a good period to own high ROE stocks. We think momo continues to outperform until smaller-cap earnings improve. $MTUM $QUAL $SPY #macro #hoPe

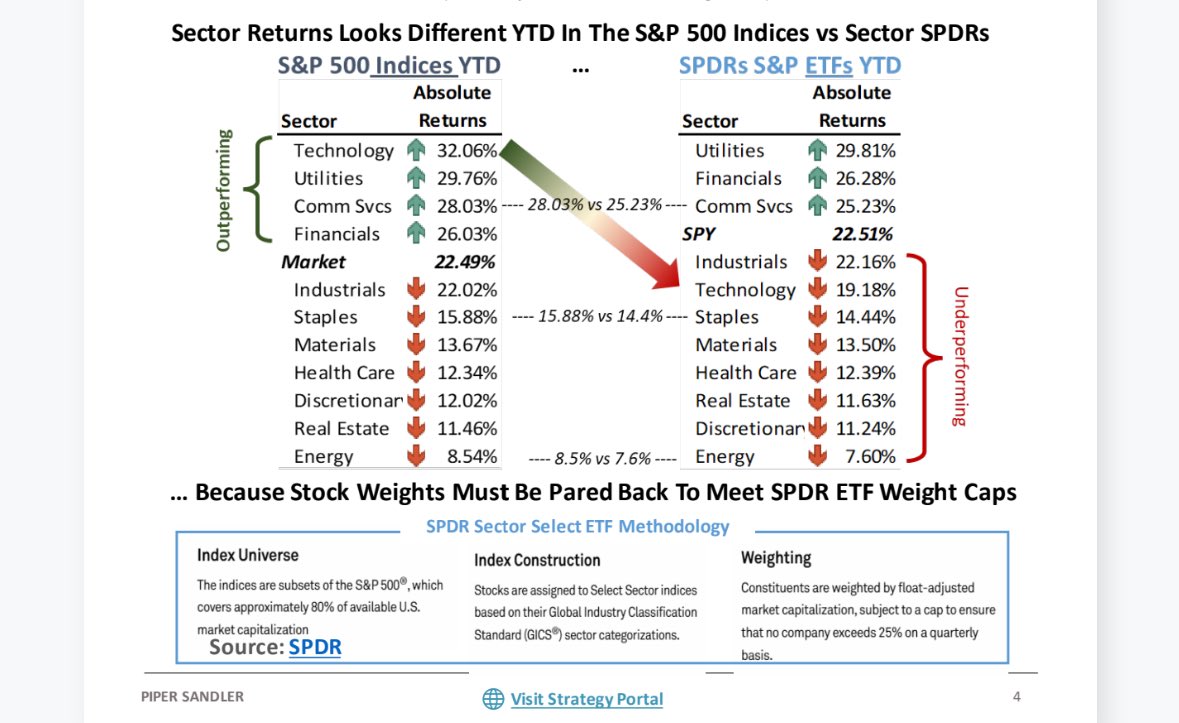

Tech is the best performing S&P 500 sector in 2024, but if you’re an asset allocator or retail investor that bought $XLK you’ve underperformed due to SPDR ETF construction methodology. There are many options when it comes to ETFs, understanding how they’re built is important.

Equity valuations have expanded a lot in the past two years as macro risk has been “priced out”. Nowadays, both credit and equity markets aren’t worried about much. Equity valuations can stay higher for longer as long as credit spreads remain tight. #macro#hope $SPY

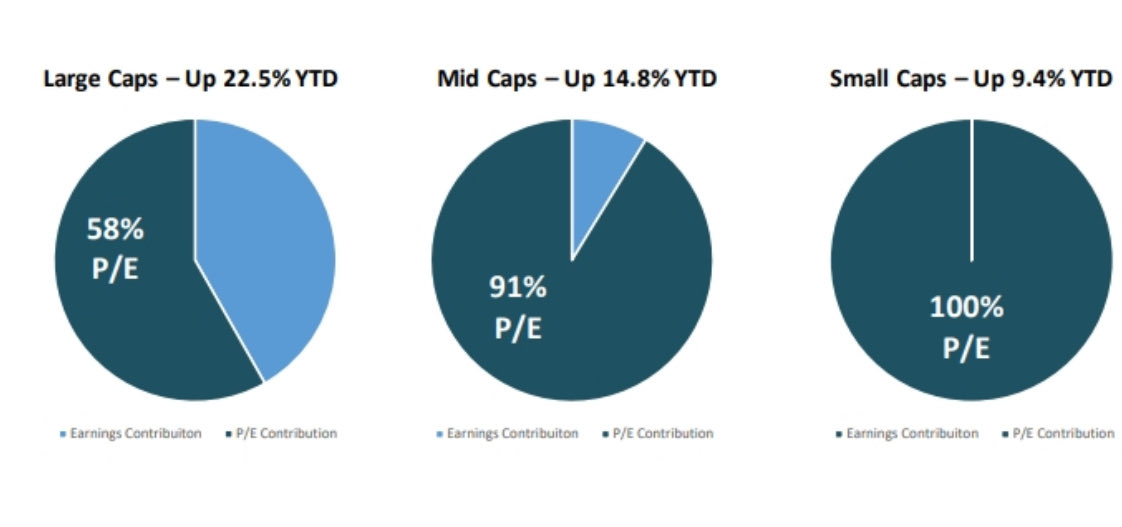

Earnings are the driving force of sustainable and stable returns. There is a big difference across size indices YTD. Gains in small caps have all come from P/E expansion - a reflection of an improving macro backdrop. Earnings will need to show up to sustain returns ahead. #macro

One of the reasons that credit spreads are so tight, and equity market P/Es are so elevated, is because risks of a recession have abated. We’re unlikely to see recession fears return, leading to wider spreads and lower P/Es, unless the unemployment rate rises above 4.5%. This suggests P/Es stay higher for longer. $SPY #macro #hopE

This is the #1 explanation for why the $SPY is trading at 22x. Until a risk arises (rates, oil, unemployment spike), it won’t be priced into equity or credit markets. #macro#hope

The $SPY is either trading at ~24x, ~22x or ~20x next year’s earnings … depending on what you think about consensus estimates for 2025. Fair value is just a concept, not a mathematical certainty. #macro#hope

Nothing better than spending quality time with your kids, especially when they have an imprinted moment in their lives. Front row tickets seeing @gracieabrams at @RadioCity … $$$$. Seeing the smile on your daughter’s face … priceless. #macro