Toch even met de voetjes op de grond bij $XFAB. Alle sympathie voor onze Belgische chipper, maar de hoge capex/onbestaande FCF is altijd een rem geweest op een multiple-expansion van dit aandeel. Sic ? Ja, maar is 4% van de groepsomzet. Photonics ? 8% van prototyping revenues.

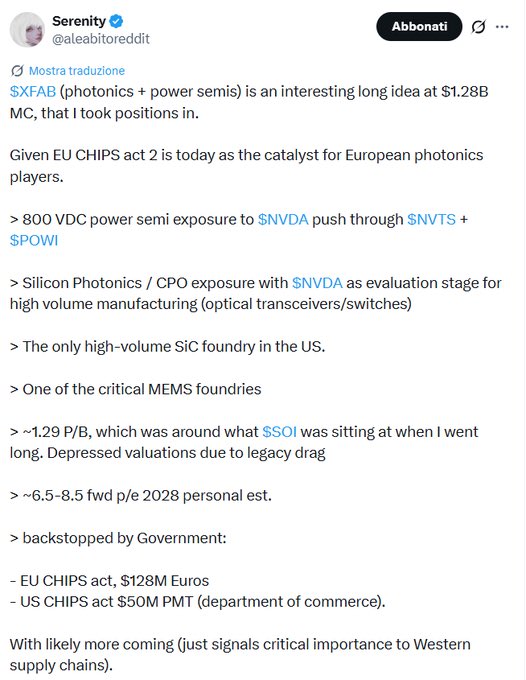

X-FAB has been written about all year. There is nothing new to learn about X-FAB that is not already reflected in the price.

Yet the stock moves up as much as 70% today because of this post. So either the market has been completely wrong until now, or the claims being made are wrong.

Spoiler, it is the claims that are wrong.

X-FAB is being pitched as “photonics + power semis” with four supposed AI hooks. The reality is that these segments together account for only about 23% of revenue, and almost none of that has meaningful AI exposure. Microsystems and photonics are mainly tied to automotive sensors, medical microfluidics, and industrial sensing, while integrated photonics contributes only about $5–6M in NRE and remains in the R&D phase. Wide-bandgap exposure is still overwhelmingly automotive and renewables, with datacenter only described on the Q1 call as a recent add-on market. Real AI datacenter revenue is likely well below 2%. The remaining 77% is classic analog and mixed-signal CMOS, heavily concentrated in automotive at around 62%, and that core business is currently shrinking with automotive down 10% YoY.

X-FAB is today a European specialty foundry for third-party designs running at roughly 60% utilization, FY2025 revenue around $770M, with only marginally positive EBIT, $291M net debt, and negative owner FCF. This is a high fixed-cost contract manufacturer sitting at the bottom of a cyclical downturn.

The claimed 800V power semi exposure through Navitas and Power Integrations is simply wrong. There is no pathway from NVIDIA’s 800V push into X-FAB. Navitas runs through Powerchip and, from late 2025 onward, GlobalFoundries for U.S. capacity. TSMC exits GaN entirely by mid-2027. Power Integrations manufactures PowiGaN internally. Infineon, Innoscience, MPS, ROHM, STM, and TI are vertically integrated. X-FAB’s GaN remains developmental with no commercial revenue, and its production-capable dMode platform is not aligned with the eMode datacenter mainstream. There is no NVIDIA, Navitas, or Power Integrations design win.

The silicon photonics argument is half true but massively overstretched. NVIDIA is indeed part of X-FAB’s photonixFAB consortium, but only as an application development partner evaluating technology. That does not imply high-volume manufacturing. NVIDIA’s actual CPO supply chain runs through TSMC and Tower. X-FAB’s photonics business is still pre-revenue, with product commercialization likely not before 2027–2028, and LIGENTEC controls the direct customer relationship. Consortium membership is not a production contract.

The MEMS claim is technically correct but irrelevant for AI. X-FAB is a meaningful pure-play MEMS foundry for automotive sensing, medical microfluidics, and industrial applications. But the MEMS segments that matter for AI datacenters, optical circuit switch micro-mirrors and MEMS timing oscillators, are controlled elsewhere. The total addressable pure-play MEMS foundry market is only around $1B globally. X-FAB is a top-five player in a niche that is simply too small to move the valuation narrative.

The “only high-volume SiC foundry in the U.S.” statement is also true but misleading. The global SiC market is dominated by integrated manufacturers like Infineon, STM, Wolfspeed, onsemi, and ROHM, which control over 90% of industry revenue. X-FAB’s share is around 1% globally and still operates on 150mm wafers while the industry transitions to 200mm. The headline 152% YoY growth is coming off a tiny base and is constrained by consignment substrate supply, limiting margin expansion.

Government support is real, but it is not an earnings backstop. The funding is tied to growth capex for future capacity, with commercial ramp from Fab4Micro only expected around 2029. The U.S. support remains politically uncertain. These subsidies imply years of additional capital outflow before any return, not reduced near-term risk.

second post ➡️

@Goemaere_Bart Ik hoop het van harte dat ik verkeerd ben, hoewel XFAB geen Nvidia is natuurlijk. In elk geval zal Xfab een beter track record in de toekomst moeten voorleggen om tot een duurzame hogere waardering over te gaan.

Toch even met de voetjes op de grond bij $XFAB. Alle sympathie voor onze Belgische chipper, maar de hoge capex/onbestaande FCF is altijd een rem geweest op een multiple-expansion van dit aandeel. Sic ? Ja, maar is 4% van de groepsomzet. Photonics ? 8% van prototyping revenues.

Maison Pommery (Vranken) vraagt de retail-obligatiehouders een jaar uitstel voor de terugbetaling, in ruil voor een belachelijke 0.15% extra coupon (tot 3.9%), volledig buiten benchmark. Een deftige fles champagne is misschien een beter voorstel om ze te overhalen.

Het voorgestelde uitkoopbod op #Paytonplanar, aan amper 8 maal de nettowinst excl. cash, lijkt op een diefstal op klaarlichte dag bij de minderheidsaandeelhouder.

Dat mevrouw Kadri, ex-CEO van #Syensqo, een buitensporige jaarvergoeding van 40 miljoen opstreek voor een ondermaatse prestatie, is vanuit corporate governance perspectief moeilijk te verteren. En momenteel is ze nog steeds "senior advisor to Syensqo" voor wat extra zakgeld.

#Solvay noteerde aan 101 euro bij het aantreden van CEO Kadri op 1 maart 2019. 6 jaar later staan we, gecombineerd #Solvay en #Syensqo zelfs lager. Hoge bonussen mogen, maar niet wanneer aandeelhouders met lege handen achterblijven.

Het contrast tussen #Melexis en de Duitse sectorgenoot #Elmos kan niet groter zijn. Elmos verwacht 11% omzetgroei dit jaar, Melexis wellicht paar procentjes groei. Koers Elmos afgelopen 5 jaar verviervoudigd, Melexis -37%. Waarderingsgap tussen de 2 is vandaag terecht beëeindigd.

Het is vandaag exact 1 maand geleden sinds de laatste koersvorming bij #ABO. 1 maand ! Zonder nieuws, zonder update, zonder iets. Dat kan je toch niet serieus menen @FSMA@euronext ?

De joint-venture van #KBCSecurities en #VanLanschotKempen voor equities is wellicht noodzakelijk om het economisch leefbaar te houden, maar het betekent op termijn alweer een verschraling van het analistenlandschap voor Belgische aandelen. Bijzonder jammer nieuws !

Deze ochtend, wandelend naar het werk (ja, op een stakingsdag) kwam ik een aantal beleggers tegen...

Na de beurstaks, de meerwaardebelasting, de roerende voorheffing (van 15 naar 21, 25, 27, 30%), nu dus ook verdubbeling effectentaks

"Als je een miljoen op een effectenrekening hebt staan, is 0,15% verdubbelen naar 0,30% dan een citroen uitpersen? Als Geert Noels boos is, is dat omdat hij de belangen van zijn klanten dient. Maar de citroen uitpersen? Alsjeblieft."

Frank Vandenbroucke in #terzaketv

Beleggers struikelden over elkaar om een kwartje van de gevraagde Kinepolis-obligaties aan 5% couponrente te krijgen. De obligaties zijn duidelijk populairder dan het aandeel.

#Melexis analistenconsensus die een dividendverlaging voor zowel 2025 (3.30 euro per aandeel) als 2026 (3.07 euro) verwacht, terwijl je uit een ontmoeting met het management mag afleiden dat een stabiel dividend (3,70 euro) het meest waarschijnlijke scenario wordt.

@ambriage@elvermo Ambriage, i volgt overduidelijk dit bedrijf niet... Misschien toch even naar hun track record kijken op lange termijn kijken. Grafiekje van de kwartaal-omzetcijfers