Markets enter the week with the $VIX at 15.3, near the lower end of its 52-week range.

At the same time:

• U.S.–Iran headline risk remains elevated

• Breadth remains narrow

• AI leadership remains crowded

• Volatility is pricing a relatively calm week ahead

The trend remains constructive. Although some of the strong leaders like $AXTI and $LITE have seen consolidation this week.

The question is whether stability is being priced too confidently.

Asymmetric Opportunities - Week Ahead is now live.

We break down: → expected moves across $SPY, bitcoin:native , $GLD , and $USO (Oil) → volatility structure $VIX→ positioning & flows → narrative vs pricing disconnects → the key catalysts that could force repricing

Link below.

Opened a position before the close in $BE: Short BE Aug $180 puts (79 DTE).

- Spot: $287

- Strike: $180

- Premium received: $16

- Breakeven: $164

BE currently carries 122% ATM IV and an options-implied move of roughly ±$131 over the next 79 days.

1SD downside band sits at $163. The breakeven on this trade is almost identical.

The market is effectively paying me to underwrite a scenario where BE declines more than 43% from current levels over the next 79 days.

A 0.137 delta strike, strong premium, and a breakeven near the modeled 1SD downside range made the setup attractive enough to take.

The chart looks quite good as well, high momentum name. Consolidating around the 10 and 20 daily MAs. Rising 50D EMA.

Could definitely break down and drop fast, but we have the cushion and the time to manage if necesary.

Position size remains small, but willing to add if the stock breaks out above the ATH again.

Always do your own DD.

$CRWD earnings after the close.

Current setup:

• Expected move: ±10.3%

• Skew spread: -6.3 vol points

• Upside calls trading at a premium

Clear story:

Investors appear more worried about missing an upside surprise than protecting against a downside miss.

Downside 1SD move $91.72 / -11.79%

Upside 1SD move $103.97 / +13.36%

Let's see if the earnings will justify this pricing.

$AVGO earnings after the close.

The options market is pricing a move of ±$44.10 (±9.1%) over the next 2 days.

Current setup:

• Spot: $485.05

• ATM IV: 140.2%

• 25Δ Call IV: 163.8%

• 25Δ Put IV: 142.0%

• Upside skew: +21.8 vol points

What's interesting isn't the size of the move.

It's the skew.

Even into earnings, traders are paying a substantial premium for upside exposure.

The options surface remains tilted toward a positive surprise despite the stock already being one of the biggest AI winners of this cycle.

Model range:

📈 1SD upside: $549.58 (+13.3%)

📉 1SD downside: $428.10 (-11.7%)

The market is still willing to pay more for upside convexity than downside protection.

Tomorrow we'll find out whether that optimism is justified.

$AVGO earnings after the close.

The options market is pricing a move of ±$44.10 (±9.1%) over the next 2 days.

Current setup:

• Spot: $485.05

• ATM IV: 140.2%

• 25Δ Call IV: 163.8%

• 25Δ Put IV: 142.0%

• Upside skew: +21.8 vol points

What's interesting isn't the size of the move.

It's the skew.

Even into earnings, traders are paying a substantial premium for upside exposure.

The options surface remains tilted toward a positive surprise despite the stock already being one of the biggest AI winners of this cycle.

Model range:

📈 1SD upside: $549.58 (+13.3%)

📉 1SD downside: $428.10 (-11.7%)

The market is still willing to pay more for upside convexity than downside protection.

Tomorrow we'll find out whether that optimism is justified.

$PANW earnings after the close.

The options market is pricing a ±12.6% move.

Historical average move over the last 7 quarters:

~4.2%

More notable: 0 of the last 7 quarters exceeded the currently implied move.

Current setup:

• IV premium: +8.4 percentage points

• Estimated IV crush: ~68%

• Implied move is roughly 3x historical realized

The market is paying a substantial premium for uncertainty. Historically, that premium has not been justified by realized post-earnings volatility.

Opened a short straddle as part of my IV earnings crush as $PANW fullfills the criteria. Always super small sizing on these. 0.5% of the account as these can move violently.

$SPCE There was a lot of focus on the stock losing 40% in a single session. Currently, there is massive speculation going on on the stock.

I think the more interesting story is what's happening in the options market.

Current setup:

- Stock price: ~$4.46

- DTE: 15 days

- ATM straddle: ~$1.80

- Implied move: ±40% (in 15 days!)

At first glance, that's already a huge amount of uncertainty. But what makes it even more interesting is the skew.

- 25 Delta Call IV: 382.7% - 11C

- 25 Delta Put IV: 218.7% - 4P

In other words, traders are willing to pay dramatically more for upside exposure than downside protection.

Normally, after a move like this, you'd expect investors to scramble for downside protection. Instead, the market is still aggressively bidding for upside calls.

What the distributions show:

This first chart uses a standard lognormal framework. Keep in mind, this is a simplified model, we are not taking every single strike and its respective IV into account.

However, wou can still clearly see the market is pricing an extremely wide range of outcomes over the next 15 days.

The second chart incorporates the actual options skew (only the 25 delta IVs, so again a simplified model).

This is where things get interesting. Because call IV is significantly higher than put IV, the distribution shifts noticeably to the upside.

This clearly isn't a balanced set of outcomes. The market remains obsessed with upside convexity.

Why?

We all know this one already. SpaceX.

There has been increasing speculation around a future SpaceX IPO, and many retail traders appear to be treating SPCE as a proxy vehicle for anything related to commercial space and apparantly a core part of the thesis is that $SPCE will be the most common error for people actually looking to buy $SPCX

Whether that logic is correct is a completely different discussion. The options market doesn't care if the narrative is rational, it only cares that people are willing to pay for it.

$SPCE is an interesting case study. I will probably stay on the side for this one, but curious to hear if anyone is trading this currently.

$META | January 2027

- Spot: $616

- Expected move: ±$150

- 1SD range: $453 - $839

- 2SD range: $333 - $1,141

Despite a $1.5T + market cap, the options market still assigns a meaningful probability to $META appreciating another ~36% from here over the next 226 days.

This would put the stock comfortably above ATH again.

Upside calls continue to trade at a slight premium to downside puts.

Positioning matters and the options market continues to lean optimistic.

$CRWD earnings after the close.

Current setup:

• Expected move: ±10.3%

• Skew spread: -6.3 vol points

• Upside calls trading at a premium

Clear story:

Investors appear more worried about missing an upside surprise than protecting against a downside miss.

Downside 1SD move $91.72 / -11.79%

Upside 1SD move $103.97 / +13.36%

Let's see if the earnings will justify this pricing.

The market spends a lot of time debating AI demand.

Far less time is spent analyzing the physical constraints required to satisfy that demand.

Power, Networking, Optics, Photonics.

The biggest winners of the AI buildout may ultimately be the companies solving bottlenecks rather than the companies selling compute. Exactly what some of your theses implied.

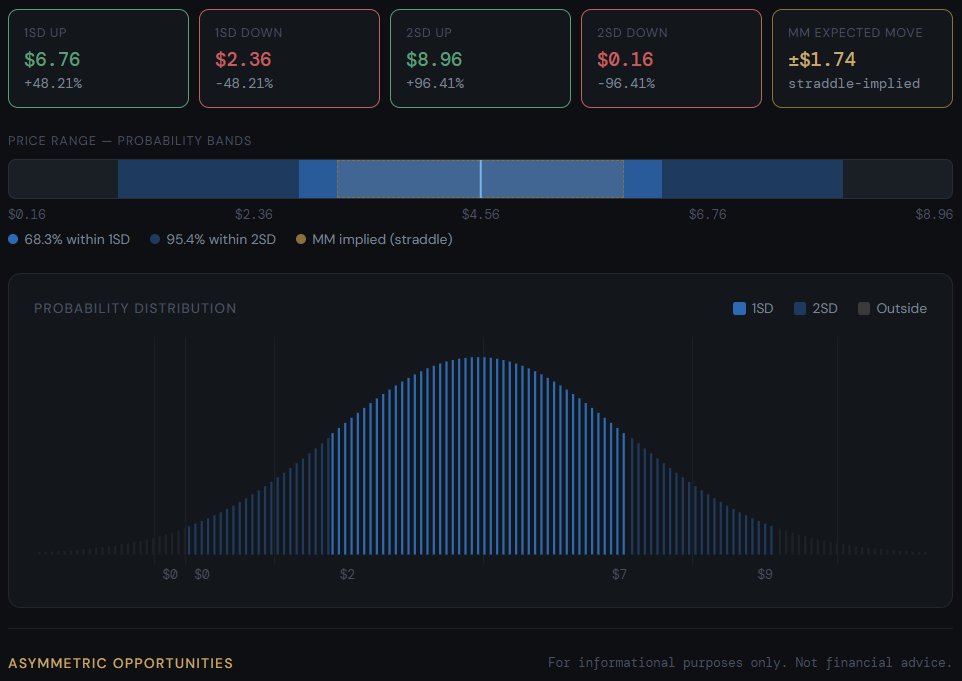

$SPCE just fell nearly 40% in a single session.

It is not $SPCX after all.

Yet what's fascinating is what the options market is pricing after the collapse.

Spot: ~$4.56

- 15D ATM straddle: ~$1.74

- 1SD range: $2.36 – $6.76

- 2SD range: ~$0.16 – $8.96

Of course, reality doesn't follow a normal distribution. Meme flows, dilution risk, and news events can completely reshape the path.

But as a thought experiment, it's interesting:

Even after a 40% crash and a collapse in IV from 300%+, the market is still pricing a distribution where the stock could plausibly double within weeks or go to zero.

The distribution is wide and this stock will remain highly unstable.

A harsh reality

Are you out to turn a little into a lot in a hurry?

Look folks, there has been tons of research done on the success rate of retail traders. By exchanges, regulatory agencies, brokerage houses, trading platforms, academic researchers and the like.

The numbers are in and you are a fool to begin with if you think your are an outlier -- although all retail traders think they are outliers (and they usually are on the left side of the bell curve distribution).

Expectations and eagerness to trade for the sake of money are inversely correlated with success. Sorry, but true (of course except for in your dream world).

You want to turn $50k into $5 million in five years? Well, go for it if you that is your dream. But know that professional career traders in zero-sum markets (like futures, day trading anything and crypto) plead with you to trade their asset class. Please, I beg you to trade futures (my asset class).

Fresh meat is always welcomed.

Maybe you are among the 2 in 1,000 that can with a few years of experience achieve back-to-back-to back-100% years. I do not want to do anything to prevent your effort. I wish you well. In 50 years I've witnessed many try.

Or, do you have realistic profit expectations and want to become excellent in some niche of market speculation?

Then you have a chance.

But your chance depends on your ability to protect your capital and avoid big losses.

Here is the reality folks -- the real world where 99% of us live.

Pick your asset class. Now have adequate capital (the amt is disputable but I use the figure of $50k). Next know that no matter what you do it will take three to five years to even pick up the scent of where your excellence might be hiding.

Your challenge will be to develop some scheme or system or approach that is repeatable. Every successful trader has a different method. No exceptions. You cannot copy anyone. There are reasons why I won't go into.

You might have to try a few different approaches to find what methods are suitable to you.

But here is the HUGE challenge you face.

You will have to keep your capital intact (relatively speaking) or have deep pockets to get through the three to five years of the steep learning curve.

You will also need to avoid the fast talkers who want you to believe they have your answers.

Following are appeals I received via email in just the past week from "reputable" trading services (these are verbatim):

-$10,000 into $30,417. 14 out of 20 trades doubled

-that's a 1,004% return in 6 days, turning a $605 bet into $6,684

-1004% on UMAC

- +100% on BBAI in a day

-See how stock flips could have made $92,000 in one year!

-Soured 1,025% in just six months

-convinced this could be this year's next 1,000%

You fall for these lines, you are done for. Another reality is that not everyone is made for crazy success in trading. Most people would be better off living frugally and putting as much money as they can into a 50% SPY, 30% fixed income, 10% energy and 10% precious metals portfolio and let it work over time. Then pursue a day job that excites you.

So, don't be conned by the circus acts that promise you the moon. Trading is hard work. Tedious. Boring often. Stressful.

My standard recommendation to most young people is to get an education in a field that you like and where jobs are available. Like welding. Or supply chain management. Or engineering.

98% of you young folks will thank me for this advice someday.

Currently hovering around a $30-$40 move.

So far so good, for my position. Let’s wait for the call to conclude and see where we stand tmr. This could be a potential blowout. $PANW

$PANW earnings after the close.

The options market is pricing a ±12.6% move.

Historical average move over the last 7 quarters:

~4.2%

More notable: 0 of the last 7 quarters exceeded the currently implied move.

Current setup:

• IV premium: +8.4 percentage points

• Estimated IV crush: ~68%

• Implied move is roughly 3x historical realized

The market is paying a substantial premium for uncertainty. Historically, that premium has not been justified by realized post-earnings volatility.

Opened a short straddle as part of my IV earnings crush as $PANW fullfills the criteria. Always super small sizing on these. 0.5% of the account as these can move violently.

A few observations from last week’s sector map:

• AI infrastructure remained strong

• Cybersecurity continued attracting flows

• Healthcare broadened participation

• Energy weakened materially

• Mega-cap leadership became increasingly fragmented

The market isn’t simply rewarding high beta stocks, it looks like it is rewarding specific narratives like AI Infra.

That’s usually an important distinction late in a trend, especially as breadth isn’t exceptionally high.

$MU once again with exceptional performance over the last week.