Pennar Industries FY26 – Key Highlights

🚀 Record Financial Performance

Delivered its highest-ever consolidated revenue of ₹3,666 Cr, up 16.2% YoY.

PAT grew 16.2% YoY to ₹139 Cr, supported by operating leverage and improving business mix.

ROCE remained healthy at 22.3%, reflecting efficient capital deployment.

📈 Robust Growth Visibility

Order book stands at approximately ₹2,850 Cr, providing strong revenue visibility into FY27.

Management expects continued momentum across Pre-Engineered Buildings (PEB), Engineering Services and the US business.

🌎 US Business Scaling Up

Ascent Structural and the US PEB business continue to gain traction, supported by increasing demand from data centres, industrial facilities and warehouse projects.

The US business is expected to become a larger contributor over the next few years.

🏗️ Capacity Expansion Underway

Management has guided for ~₹150 Cr of capex in FY27 to support future growth.

Investments are focused on expanding manufacturing capacity, technology upgrades and enhancing engineering capabilities.

🤖 Focus on Productivity

AI-led engineering tools and digital initiatives are being deployed to improve design productivity, reduce turnaround time and enhance margins.

💰 Valuation Remains Attractive

The stock currently trades at around 15x FY26 earnings, compared with the engineering sector average of 20–25x.

A re-rating toward sector multiples could imply a fair value in the ₹206–257 range, with a base case around ₹230, assuming continued execution.

⸻

Positives

✅ Record revenue and earnings

✅ Healthy ROCE above 22%

✅ Strong order book providing multi-quarter visibility

✅ Growing US presence with structural demand tailwinds

✅ Diversified business across PEB, Engineering Services, Hydraulics and Boilers

✅ Management focused on margin expansion and productivity improvements

⸻

Key Risks

⚠️ Gross borrowings increased to approximately ₹1,142 Cr, primarily to fund growth and working capital.

⚠️ Inventory (₹1,010 Cr) and receivables (₹731 Cr) remain elevated, requiring close monitoring of cash conversion.

⚠️ Execution delays in large PEB projects could impact margins.

⚠️ Raw material price volatility may affect profitability if cost increases cannot be passed on.

⚠️ US construction demand remains an important variable for the international business.

BJP has been doing a 90/100 things right, infrastructure is moving at an unimaginable pace, people are coming out of poverty at a much faster pace, a new spending middle class is emerging. Yes BJP has issues because it is now government most part of the country. Let’s not start comparing BJP with congress. BJP on the governance front has been spot on.

@sagarikaghose What an ass you are Sagarika. Have you ever wished something meaningful on Hindu festivals?

Women like you as MPs is why this nation fails

Connect the dots……

🚀 TVS Motor just delivered a MONSTER monthly update.

✅ Highest-ever sales: 5.67 lakh units

✅ 31% YoY growth

✅ Highest-ever exports: 1.76 lakh units (+49%)

✅ EV sales up 56% YoY to 43,632 units

✅ Motorcycle sales +30%

✅ Scooter sales +32%

✅ Three-wheeler sales +55%

What stands out to me isn’t just the headline growth.

The real story is:

🔹 Export recovery is accelerating

🔹 EV scale-up is gaining momentum

🔹 Growth is broad-based across segments

🔹 Domestic demand remains healthy

When a company is hitting record volumes, record exports, and record EV sales simultaneously, it’s worth paying attention.

The next question for investors:

Can this 31% volume growth translate into a meaningful earnings upgrade in the coming quarters? 🤔

#TVSMotor #TVS #StockMarketIndia #Investing #Nifty #AutoSector #ElectricVehicles #EV #Exports #LongTermInvesting #IndianStocks #WealthCreation

If #Honasa can execute on both fronts—scale existing winners like Mamaearth & DermaCo while successfully building new categories such as oral care, fragrances and nutraceuticals—the current story could look very different in 5 years.

Management is guiding for:

• Revenue: ₹24B → ₹55B+ by FY31 (18% CAGR)

• EBITDA margin: 10% → 15%+

• EBITDA growth: ~28% CAGR

Execution is everything, but if they deliver, this has the ingredients of a potential multi-bagger.

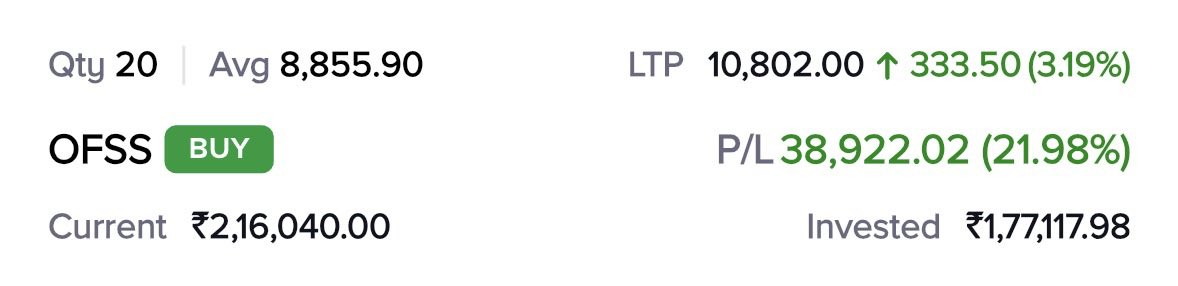

#OFSS one of the two IT stocks I am currently invested in and doing extremely well. However I very much regret not averaging further when the stock price had touched Rs 6800. I somehow didn’t have enough funds and I never borrow money to invest in market. This is an area I need to learn to get better ( Liquidity management). However still reaping rewards through my deep research and conviction

@sagarikaghose@narendramodi No one gives two shit flying fuck of your column and your fake propaganda. How about you care to join Mamta on the street for protest, it might help with your visibility. Is ranting on social media your only job? Sore loser

📌 PARADEEP PHOSPHATES: The Story Most Investors Are Missing

While the market is busy tracking quarterly fertilizer numbers, management is quietly building a fully integrated phosphate platform.

In FY26, Paradeep commissioned:

✅ 0.5 MTPA Sulphuric Acid plant at Paradeep

✅ 0.1 MTPA Sulphuric Acid plant at Mangalore

This increased total Sulphuric Acid capacity by 45%.

To understand why this matters, investors need to understand the phosphate value chain:

🪨 Rock Phosphate (Imported Raw Material)

⬇️

🧪 Sulphuric Acid

⬇️

⚗️ Phosphoric Acid

⬇️

🌱 DAP & NPK Fertilizers

Rock Phosphate is the core mineral used in phosphatic fertilizers. However, it cannot be directly converted into DAP or NPK. It first needs to be processed using Sulphuric Acid to produce Phosphoric Acid, the most critical intermediate product in the chain.

This is exactly where Paradeep is investing.

Historically, fertilizer companies have been vulnerable to volatile prices of Sulphur, Sulphuric Acid, Rock Phosphate and Phosphoric Acid.

Paradeep’s strategy is simple:

➡️ Produce more Sulphuric Acid in-house

➡️ Increase Phosphoric Acid capacity

➡️ Reduce dependence on imports

➡️ Improve margins across the value chain

Management has already outlined plans to DOUBLE Phosphoric Acid capacity from 0.5 MTPA to 1.0 MTPA while targeting near 100% backward integration.

Why this could matter for earnings:

🔹 Lower raw material procurement costs

🔹 Better supply security

🔹 Improved EBITDA per tonne

🔹 Reduced earnings volatility

🔹 Greater operating leverage

🔹 Captive power generation from waste heat recovery

This becomes even more relevant as China continues to influence global fertilizer and chemical supply chains through export restrictions, supply discipline and raw material controls.

What’s equally interesting is promoter behaviour.

Promoter holding has increased from ~56% to ~57.8% over the last year despite FII selling.

When promoters increase ownership while simultaneously commissioning new capacities and expanding integration, it’s worth paying attention.

The market sees a fertilizer company.

Management appears to be building a fully integrated phosphate platform with control over critical parts of the value chain.

Key monitorables:

📍 Phosphoric Acid expansion progress

📍 Sulphuric Acid utilization levels

📍 Rock Phosphate sourcing strategy

📍 EBITDA/tonne improvement

📍 Reduction in promoter pledge

📍 Further promoter accumulation

The biggest earnings upgrades often come not from selling more fertilizer, but from controlling more of the value chain behind it.

#PARADEEP #PARADEEPPHOSPHATES #Fertilizers #NPK #DAP #StocksToWatch #ValueInvesting #IndiaMarkets #ChemicalStocks #stockmarkettrader