The $SPCX SpaceX IPO is going to make everyone LOSE MONEY.

You don't make money investing in a company worth 1.4T.

Here are 7 companies I’m watching:

$CRCL (Circle) → $76 Must buy

$TSM (TSMC) → ~$410 Must Buy

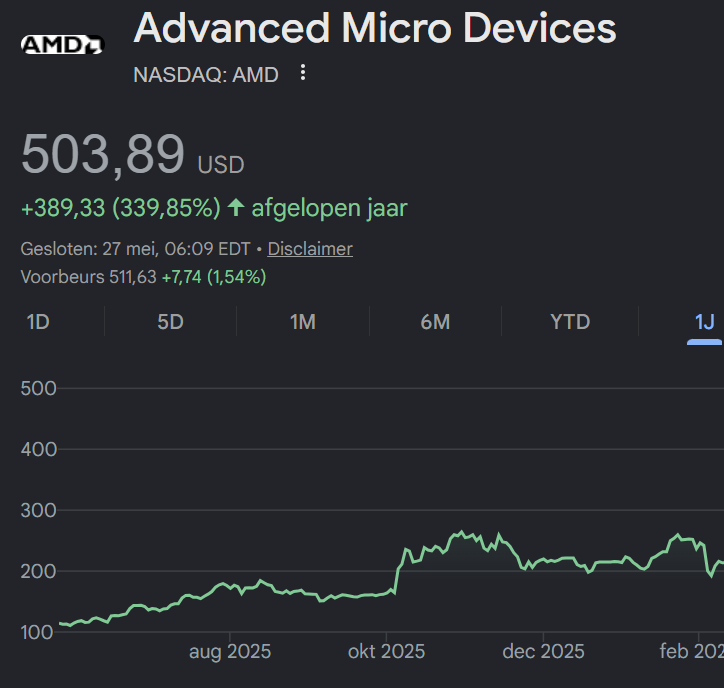

$AMD (A M D) → $470 Must Buy

$MRVL (Marvell) → $270 Must Buy

$NVDA (NVIDIA) → $200 Must Buy

$SMCI (Super Micro) → $ 29 Must Buy

$QCOM (Qualcomm) → $195 Must Buy

People ask, Why don’t you charge? I’ve made enough. Sharing is my passion ,that’s why I post for

NFA

Here are my favorite buys of 2026:

$NOW at $105

$QCOM at $200

$CRWV at $98

$SOFI at $16

$NVDA at $205

$PLTR at $130

$MSFT at $400

$META at $585

$ZETA at $20

$BMNR at $16

$NOK at $13

$OKLO at $55

$ENPH at $50

THE MARKET IS TANKING…

$NVDA will be a $195 stock

$SOFI will be a $15.50 stock

$NOW will be a $105 stock

$ZETA will be a $19.50 stock

$MSFT will be a $415 stock

$META will be a $600 stock

There are still opportunities for us!

🚨 $SOFI at $16 might be a better opportunity than $AMD at $500…🚨

And I say that as a MASSIVE $AMD bull with a 64% position, in since $100.

The risk/reward in $SOFI is incredible with >40% growth and <30FPE and sentiment at all time lows while $SPY inclusion is still coming!

$SOFI It’s hard to ignore a profitable company when the CEO keeps executing, keeps buying shares, and believes this could become a $1T company. How many people are still sleeping on this stock?

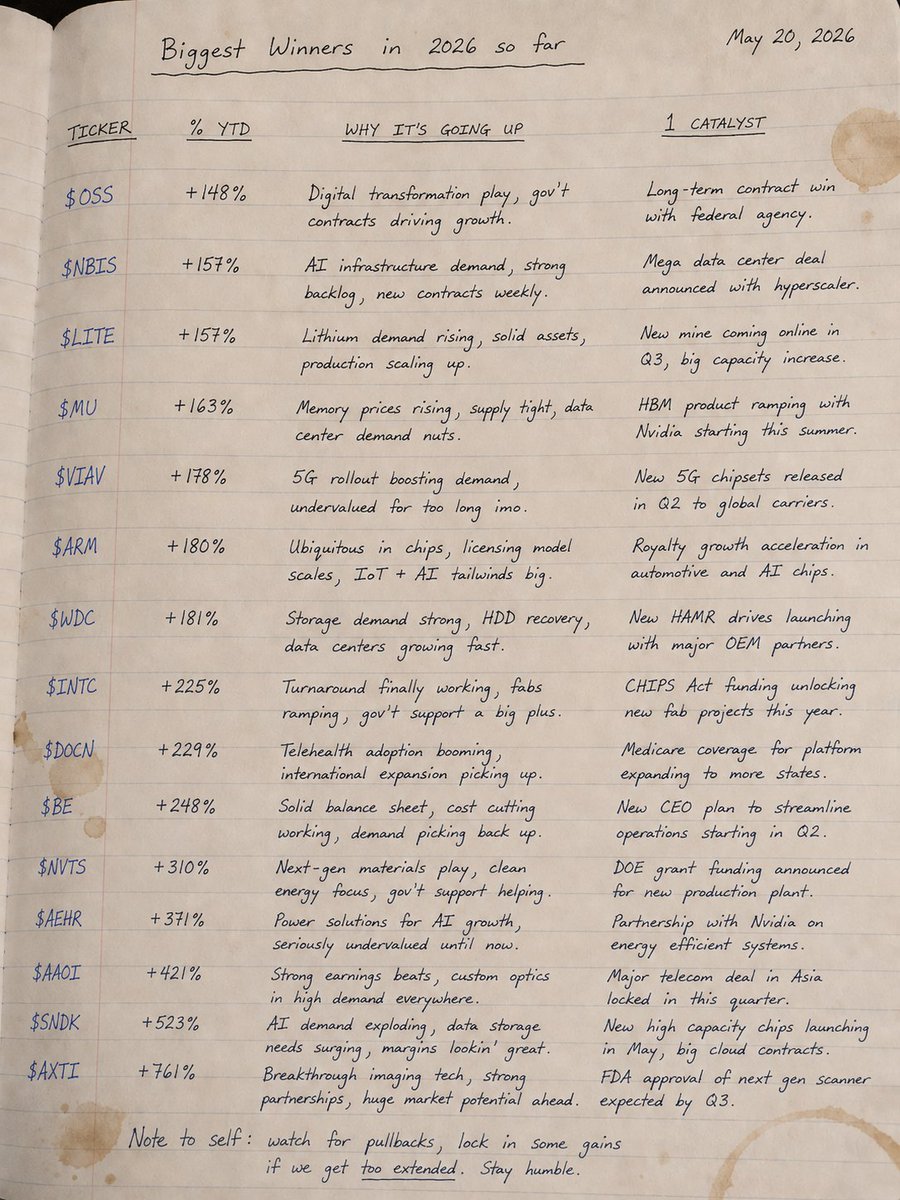

Top 12 winners for 2026 with catalyst

1. $AXTI +761%

Catalyst: $632M equity raise to double indium phosphide capacity. Pure-play AI optical infrastructure InP substrates are the critical supply bottleneck for AI data center connectivity. Record $100M+ backlog.

2.$SNDK +523%

Catalyst: Nasdaq-100 inclusion + blowout Q3 earnings ($5.95B revenue, 3.5× YoY). AI data center storage supercycle NAND prices rising 234% in 2026 per Gartner. $42B in long-term supply deals signed.

3. $AAOI +421%

Catalyst: Hyperscaler demand surge for fiber-optic transceivers driving AI data center buildouts. Applied Optoelectronics became the top-performing large-cap stock as the optical networking supercycle took hold.

4. $AEHR +371%

Catalyst: New silicon photonics customer win (March 31) ordering multiple FOX-XP burn-in systems for high-volume production. Record $50.9M backlog. Direct beneficiary of the optical transceiver boom.

5. $NVTS +310%

Catalyst: GaN/SiC power platform showcase for AI data centers at PCIM 2026. Revenue inflection as design-wins with hyperscalers and Nvidia Blackwell rack systems begin to ramp. Q1 beat on revenue + EPS.

6. $BE +248%

Catalyst: $2.6B partnership with European AI infrastructure company (May 2026). AI data center power demand making Bloom Energy's fuel cells a critical off-grid energy solution for hyperscalers.

7. $DOCN +229%

Catalyst: AI-driven cloud demand surge among SMB and startup developers. DigitalOcean's simplified GPU cloud offering became the go-to for AI builders who can't navigate hyperscaler complexity. Strong revenue reacceleration.

8. $INTC +225%

Catalyst: CEO Lip-Bu Tan's foundry turnaround 18A node in HVM, Xeon 6 selected for Nvidia DGX Rubin systems, Apple + Terafab foundry deals. 6th consecutive earnings beat. Stock hit 26-year all-time high.

9. $WDC +181%

Catalyst: Post-$SNDK spin-off refocus on enterprise HDD/flash. AI data center storage demand driving record HDD shipments. Rode the same memory supercycle as $SNDK rising NAND prices lifted all boats.

10. $ARM +180%

Catalyst: AI chip designers shifting to ARM architecture for power efficiency. Royalty revenue acceleration as Arm-based AI accelerators and server chips proliferate. Near-total dominance of mobile + growing data center share.

11. $VIAV +178%

Catalyst: Network test and optical component demand surging alongside AI data center fiber buildouts. Viavi's network visibility tools became essential as hyperscalers upgraded to 800G+ optical interconnects.

12. $MU +163%

Catalyst: HBM (High Bandwidth Memory) for Nvidia GPUs Micron became the critical memory supplier for AI training chips. Analyst note: "HBM can be priced ridiculously high." Memory supercycle with AI-driven pricing power.

13. $LITE +157%

Catalyst: Optical transceiver demand for 800G/1.6T AI data center interconnects. Lumentum is the key bottleneck supplier for coherent optics hyperscalers have no alternative. Highest quant rating among top performers (4.99/5).

14. $NBIS +157%

Catalyst: Q1 2026 revenue of $399M up 684% YoY. Raised 2026 guidance to 4GW+ contracted power. Nebius is Europe's leading AI cloud infrastructure play, backed by Nvidia and benefiting from US-centric hyperscaler capacity constraints.

15. $OSS +148%

Catalyst: Q1 2026 revenue +55% YoY with record 51.6% gross margin. One Stop Systems provides rugged AI compute for defense and edge AI defense contract wins accelerating. Lake Street, Roth Capital, and Alliance all raised targets to $18.

Every winner on this list is an AI infrastructure play.

♻️ RESHARE this post and make 1 comment for my list of stocks under $20. There's only 5 left for 1000% winners.

🚨Why $SOFI is a $30 stock RIGHT NOW 🚨

🟩2026 EPS guidance: $0.60

📈Growth: revenue and EPS >40% which is 5x(!!) the market, deserving of a MINIMUM 50FPE when the average stock has around a 21 FPE.

🟰Quick math: $0.6 x 50 = $30.

A double from here, TODAY. STEAL OF THE MOMENT.

WHY $SOFI IS A TOP 3 POSITION FOR ME

The market is overpricing the credit fear and underpricing the platform optionality when it comes to SoFi which is why I think it's one of the weirdest setups in the market right now.

The business is still executing very well but the stock is stuck in one of the worst sentiment buckets since the market clearly doesn't want exposure to credit-sensitive stocks in a higher-for-longer rate environment and SoFi still gets treated like a bank-like lender even though the business is becoming much broader than that.

The Loan Platform Business (LPB) is more important than people realize since SoFi originated $3B of personal loans on behalf of third parties through LPB in the quarter and added another $3.6B of capital commitments from three new partners. That matters because it gives SoFi flexibility so they can choose which loans to keep on the balance sheet and which loans to push through partners for fee revenue without taking the same balance sheet risk (very different model than being a traditional lender that is stuck holding everything).

This is also why the private credit fear looked less scary if you listened to the actual earnings call. One of the biggest bear arguments was that funding partners would pull back if credit conditions weakened but Noto said they're not seeing issues in performance or partner demand and LPB demand was actually above what they chose to fulfill.

The member flywheel is still the main reason this is a top 3 position for me because this is a real moat the market is overlooking. SoFi added over 1M members in the quarter, ~45% of new products came from existing members and 50% of SoFi Plus sign-ups took another product. The more members they add, the more products they cross-sell, the more deposits they gather, the more revenue they generate per member and the more efficient the platform becomes (how SoFi becomes more valuable over time). SoFi Plus becoming a paid subscription is also great to see because recurring fee revenue on top of a growing user base can improve unit economics over time.

The biggest thing I want to see next is the Tech Platform turning around which is obviously the weakest link. Technology Platform revenue fell 27% YoY to $75M, contribution profit fell 61% and total accounts declined because of the large client that transitioned off the platform. Management is rebranding it as SoFi Tech Solutions and breaking it into processing, banking core ledgers, payment hub, and risk and fraud. If that platform starts growing again then great but I view this more as a free call option on owning SoFi.

I truly believe SoFi is a good business trapped in a bad sentiment bucket. The market is focused on rates, credit risk and the weak Technology Platform while I'm focused on members, deposits, cross-buy, loan platform flexibility, operating leverage and the long-term path toward becoming a top financial institution.

It can absolutely trade lower if the market sells off or if credit fears come back but I think the business is much stronger than the stock action suggests and I have no problem keeping this a top 3 position for me.