There is an extremely high probability that the Nasdaq has culminated.

It is exceptionally rare for a pattern with such steep valuations appearing within an inherently bearish chart structure to continue higher.

Consequences are imminent, and intensifying bond market erosion will likely drive interest rates up as the primary catalyst.

Yours truly,

The Great Martis✨

The way X bitches are crying, panicking and running to cash tells me everything I need to know.

That’s usually when the bottom is here… or very close.

Markets always work the same way:

They panic.

We buy from these bitches.

Months later when the same bitches are screaming “BULL MARKET 🚀” and chasing green candles…

We sell it right back to them.

Different cycle.

Same bitches.

Let’s fucking go. 📈🔥

The King of Copper, Robert Friedland, full presentation at the Future Minerals Forum titled 'The dawn of the copper age'

"It's very clear that the copper

price must double to meet future mining

needs."

If the Copper Price doubles, Copper stocks will 10X.

Stanley Druckenmiller: “Copper is the tightest position I have ever studied.”

Ignore the hard-landing narrative.

Copper demand is surging while production is peaking.

That’s all you need to know.

Rick Rule: Copper is the next bull market

- Copper offers the best risk/reward setup

- 7% of global copper supply has vanished

- In a market already in structural deficit

“The copper price has a coiled spring aspect to it”

At the same time, it is getting increasingly harder to find new copper deposits.

- Grades are lower

- Mines are deeper

- Risks are rising

As a result, exploration and mine development costs are surging.

Copper has a bright future

Copper deficits are piling up

- From 2027 onward, deficits widen through 2040

- From 2037, annual deficits exceed 10 mt

- That’s ~50% of today’s mine supply

Cumulative deficits reach ~80 mt, or more than 3 years of global mine supply.

Copper’s supply-demand model is broken.

The copper supply picture remains in a persistent deficit.

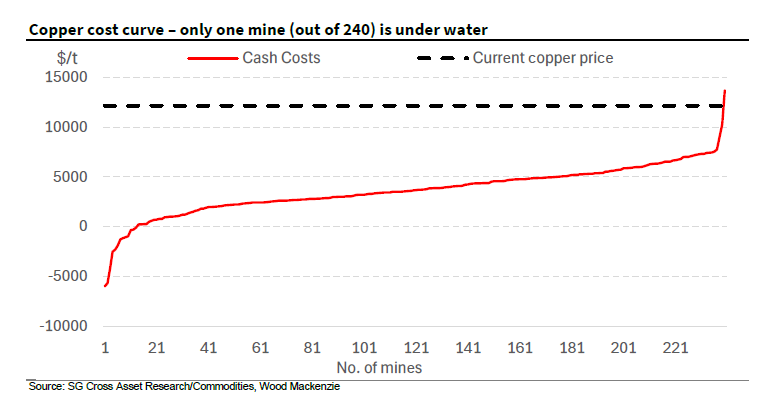

- Only 1 out of 250 copper mines is losing money at today’s prices

- Many mines are operating at or below their original design capacity

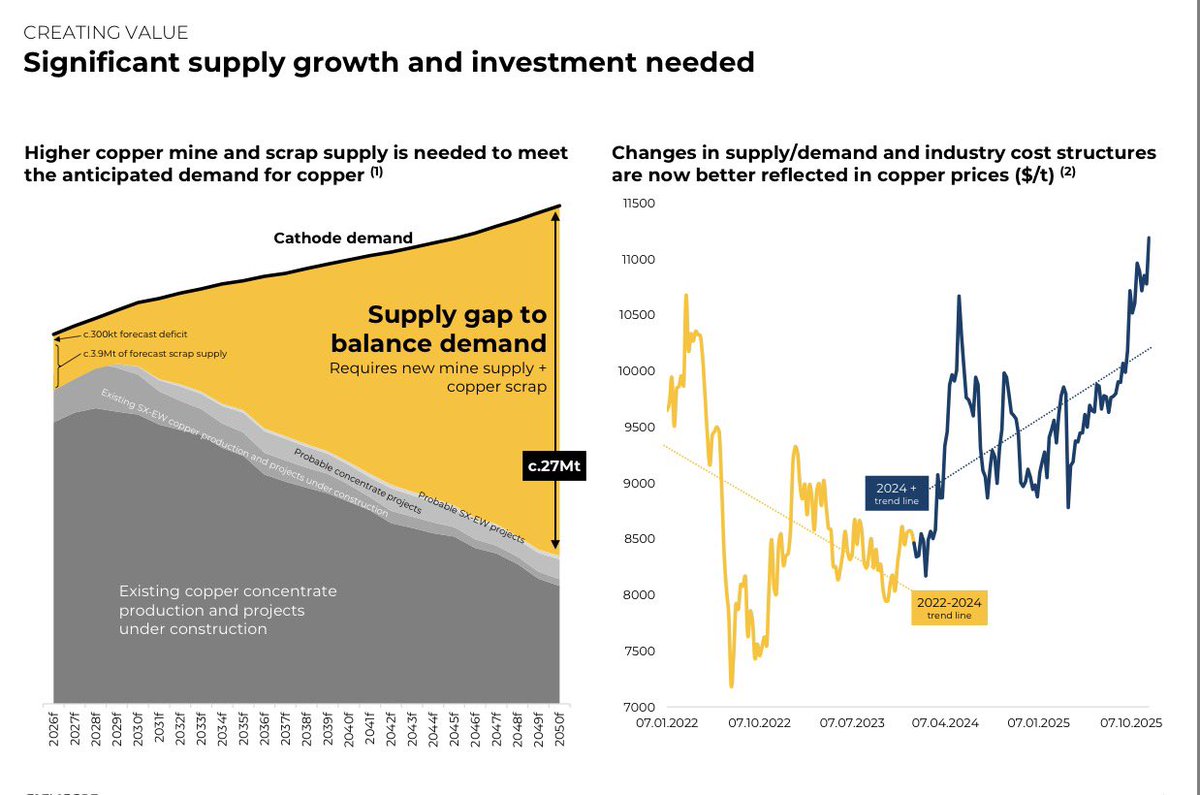

- The incentive price needed to add meaningful new supply is $5.50-$6.50

But reaching that price does not mean the market will be flooded with copper.

- It takes an average of ~18 years from exploration to first production

- Only ~50% of discoveries ultimately become producing mines

In other words, copper found today may not be produced until 2044.

Projected copper deficits for the year total 308 kt... equivalent to the 9# largest copper mine globally.

Supply simply cannot keep up with demand.

The #Copper supercycle is about to begin…

The shortage has officially started, & will progressively worsen to a deficit of 10 million tonnes by 2040.

This is equal to 33% of current global demand.

This is your last few chances to enter copper below $10.

Save this for later…

Commodity supply is structurally broken

New mine development has collapsed:

- Copper: 2015 peak -> down 90%

- Iron ore: 2000 peak -> down 90%

- Nickel: 2010 peak -> down 80%

- Gold: 2012 peak -> down 60%

Yet production kept rising.

Expanding existing, already-permitted mines was easier, cheaper, and faster than building new ones. Companies squeezed every last ton out of their assets.

That phase is now over.

Expansion alone can no longer meet demand. The world needs new mines... badly.

There is no quick fix. It takes ~20 years from discovery to production. Even an immediate reversal would only deliver new supply around 2046.

Between now and then, shortages are inevitable.

This is why commodities are entering a golden era.

Copper’s supply problem isn’t just about new discoveries....It’s embedded in existing production.

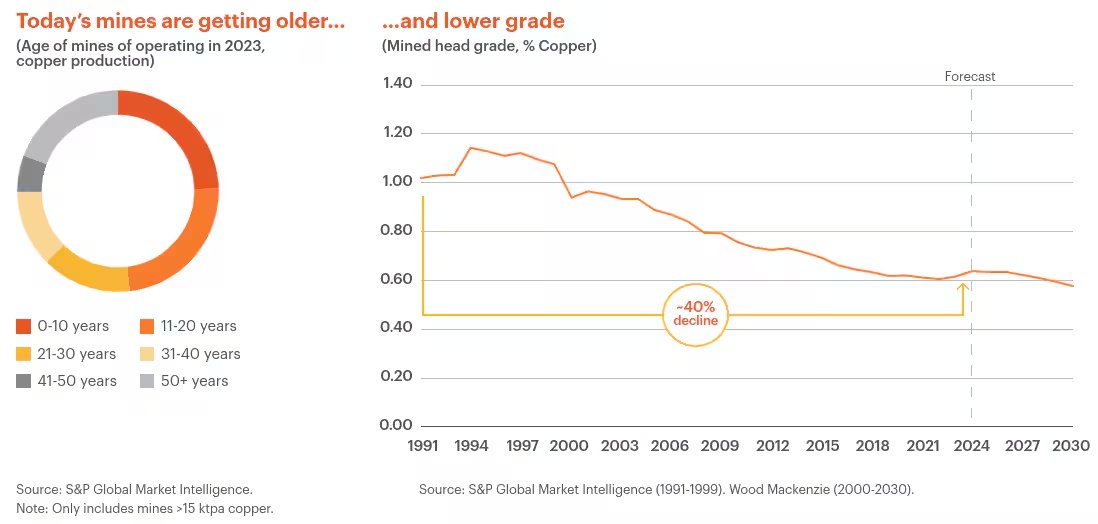

- ~50% of producing copper mines are 20+ years old

- Average ore grades have fallen ~40% since 1991

- Half of global production will face additional grade decline over the next decade

That means:

- More rock moved

- Higher energy input

- Rising costs per ton

Future supply will be structurally more expensive.

The marginal ton now costs more.... permanently.

You can’t electrify the world without copper and the world is running out of it.

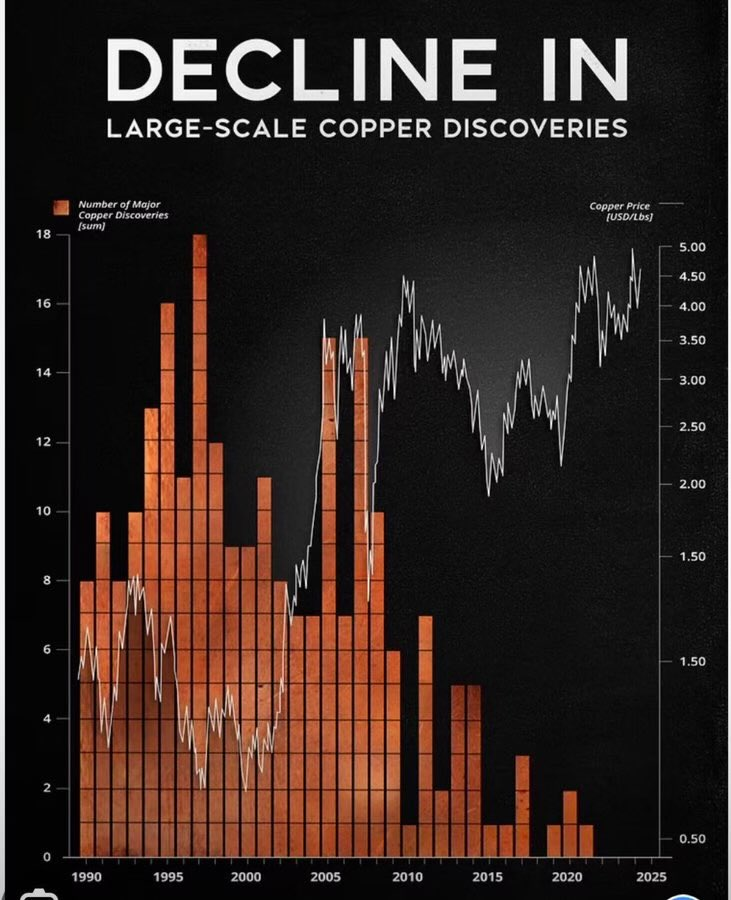

- Large-scale copper discoveries are down 90% over the last two decades

- Copper deficits are projected to widen through 2030

- Copper demand is surging: driven by electrification, data centers, and AI

- It takes 20+ years from discovery to first production

This copper bull market will surprise everyone, both in magnitude and in duration.

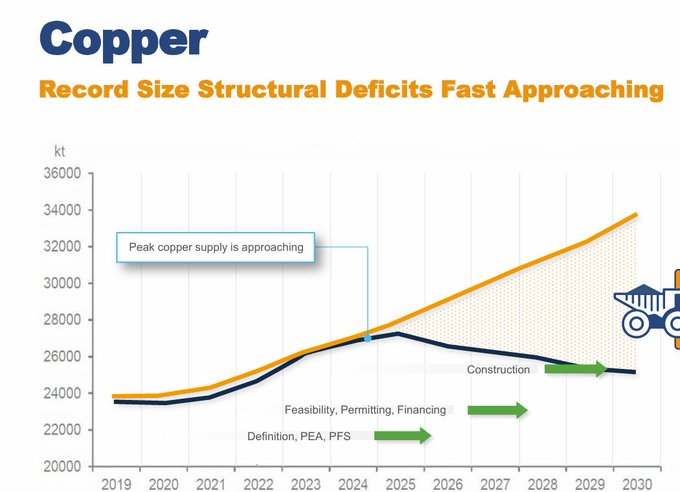

We have reached peak copper supply.

- Copper production is projected to steadily decline

- Meanwhile, demand is surging

Copper prices must rise to incentivize new production.

The problem:

It takes ~18 years from exploration to first copper.

Copper deficits are structural.

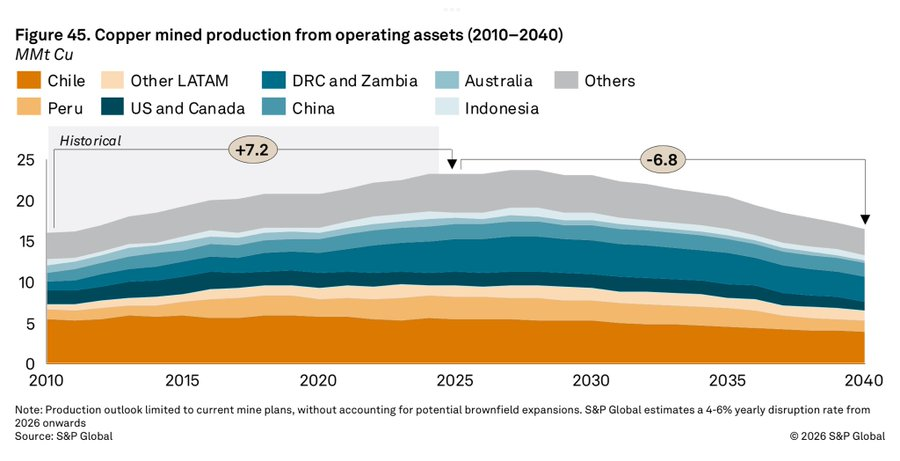

We have reached peak copper production

- In the past 15 years, copper production rose ~7%

- In the next 15 years, copper production is expected to fall by ~7%

Meanwhile:

- Data center copper demand is rising

- Electrification is surging

The copper supply-demand model is broken.

This is why copper shortages are inevitable.

- Copper supply can’t keep up with demand.

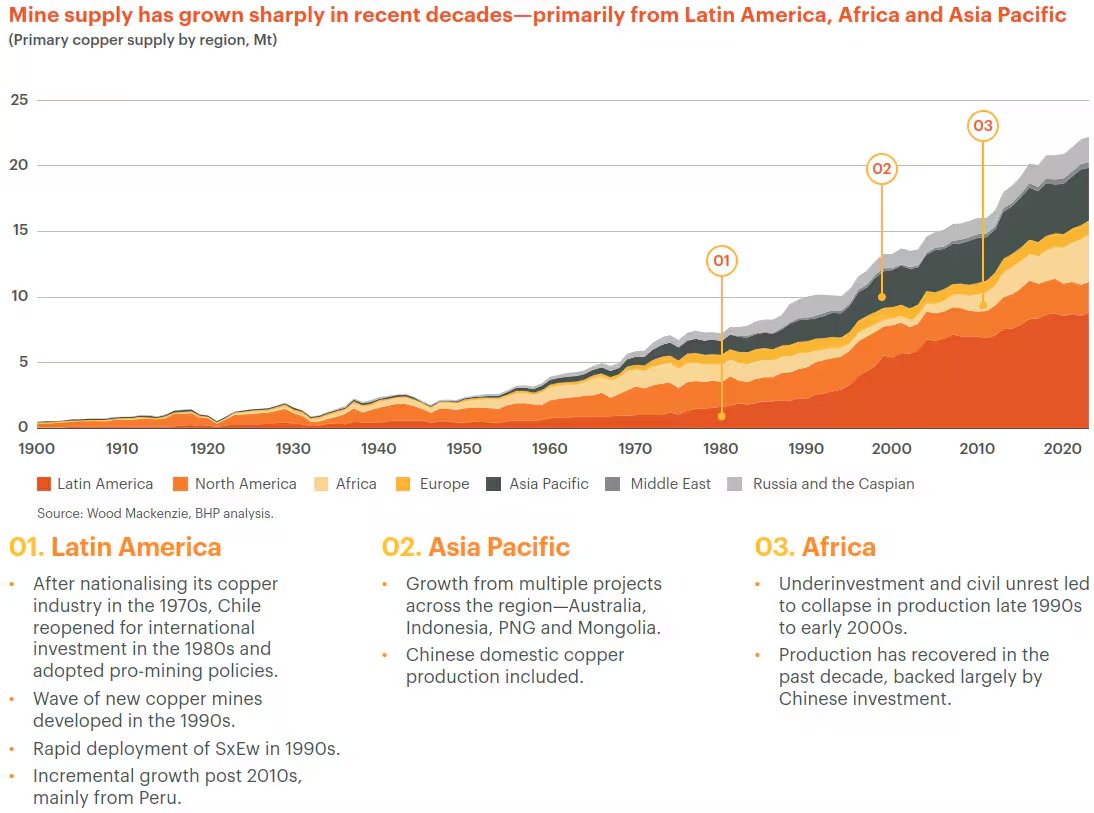

- Over the past 30 years, copper supply increased by ~12 Mtpa

We now need to add the same amount in just one decade... 1/3 of the time

In the meantime:

- 1990-2010: ~200 large copper discoveries, ~1,250 Mt of copper

- 2010-2025: ~20 large discoveries, ~165 Mt of copper

- Ore grades: ~2% in 1990 vs. ~0.6% today... and still falling

So the industry faces a double constraint:

- Fewer discoveries

- Lower-quality deposits

We’re exploring less.

And each discovery delivers less metal.

The copper supply picture is broken.

Billionaire Robert Friedland drops the reality check:

We need to mine 10,000 years of copper in the next 18 years.

The world has absolutely no clue about the supply squeeze we are facing.

Save this video to stay ahead of the curve.