Our founder @shivamtas just dropped the full breakdown of what we have been building for the last six weeks.

The AI that trades @Polymarket sports markets so you don't have to.

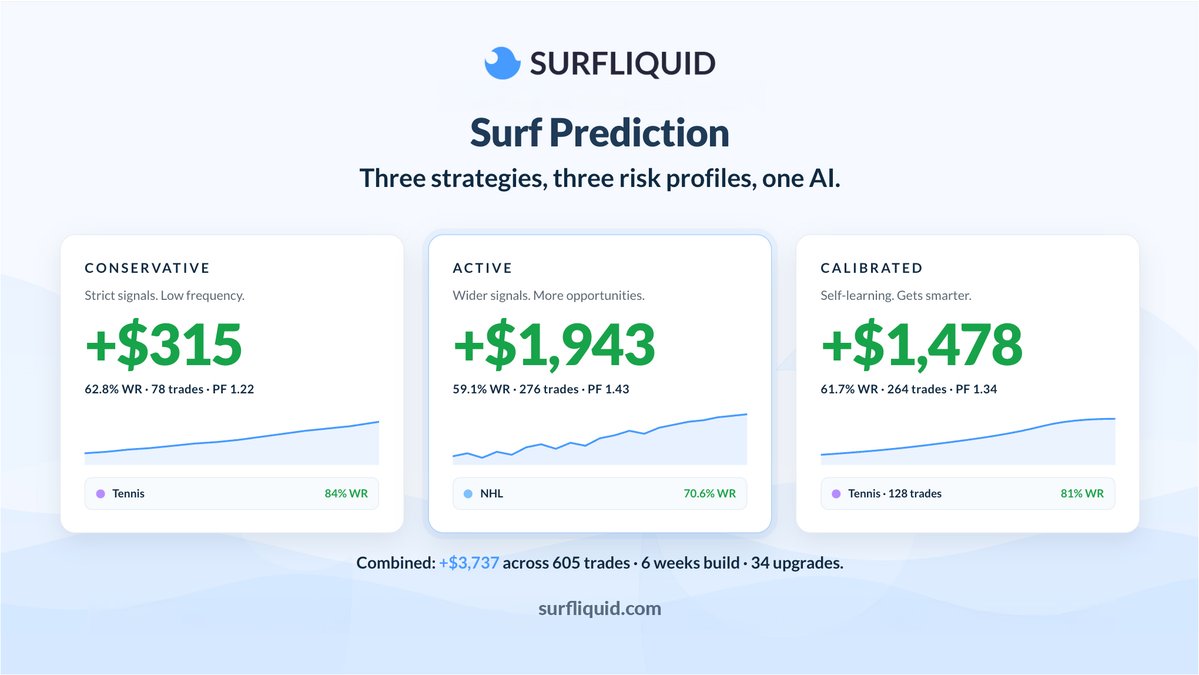

605 paper trades. Three strategies. All profitable.

This is Surf Prediction Vaults. Read the whole thing.

We built @Surf_Liquid AI that trades @Polymarket sports markets while you sleep.

Six weeks. 34 upgrades. 605 paper trades. All three strategies profitable. +$3,737 in returns.

Here's what it actually does:

→ Listens to live score data from every match on Polymarket simultaneously

→ Runs sport-specific probability models on every single score change

→ Finds the moments when the market hasn't repriced fast enough

→ Executes before the odds catch up

→ Tennis modelled point by point. Soccer is modelled by goal rate. Hockey and basketball are built differently. → One generic model doesn't survive contact with real sports. So we built one engine per sport.

Three strategies. One AI. Three risk levels:

1. Conservative: strictest signals, lowest drawdown. Your money is treated like savings.

2. Active: wider signal range, more trades, more upside, more variance.

3. Calibrated: the interesting one. Same signals as Active, but every probability runs through a self-correction layer first. If the model says 80% but history says 73%, it trades the 73. Gets smarter every day.

Here's the part I want to talk about.

In late April, we caught ourselves inflating our P&L. The bot was assuming fills at the quoted price. Real markets don't work that way. You walk the order book. Every batch fills worse than the last.

We shipped an honest fill simulation. Our paper P&L dropped meaningfully the same day.

That drop is the entire point. If your simulated fills are better than your real fills will ever be, you're flattering yourself.

Then last Tuesday we found a bug. A safety mechanism in the hedging path had been failing silently for weeks. Hundreds of failures per day. None flagged. None surfaced.

The system was profitable anyway.

That sentence bothers me more than the bug itself. Good performance hiding a broken safety system is exactly what kills strategies three months from now. We fixed it. Wired up a live monitor that fires the moment the hedge's success rate drops below the threshold.

This is Surf Prediction Vaults. You deposit stables. Pick a risk level. The AI does the rest. You never touch Polymarket.

Sports is live. The weather is next. Crypto follows.

Building this in the open. The good weeks and the bad ones. The wins and the bugs were caught silently for a month.

If you trade prediction markets or build in this space, I want to hear the strongest argument against what we're doing.

Full write-up with the architecture, the Guardian Layer, the numbers and the path to real capital:

https://t.co/Nh7sa7VtHx

The trust layer is no longer a slide. It is a registry, and Surf is on it.

Surf is now live on ERC-8004 across @base and @0xPolygon. Agent identity, allowed actions, behaviour over time, all queryable on-chain.

Reviews are open. Leave one, boost the rank, help us turn audit-ability into a habit.

Base: https://t.co/gxUG6fuTxQ

Polygon: https://t.co/oD0SfEwF5T

Something simple shipping next week.

The savings interface stays the same. The places your money can work just got one bigger.

The chain everyone uses, but nobody offers a clean savings layer for.

Next week.

Multi-billion dollar money market funds are landing on transparent rails. Same vehicles institutions used to keep to themselves. Now reachable for normal savers.

That is the doorway we built Surf to open.

Fidelity International just launched FILQ — a tokenized money market fund issued as an ERC-20 on Ethereum.

It's an onchain version of their ~$7B institutional liquidity fund: same strategy, a Moody's AAA-mf rating, but with 24/7 subscription and redemption.

The biggest asset managers in the world are tokenizing cash, and settling it on Ethereum.

As BlackRock CEO Larry Fink put it, "We're not spending enough time talking about how quickly we're going to tokenize every financial asset."

Building in the open. Here is what is shipping at @Surf_Liquid in the next two weeks.

Three things, in order.

One. ERC-8004 is done. Surf AI is registered on Base and Polygon as a Trustless Agent. Identity, declared capabilities, and on-chain behaviour are all queryable on-chain by anyone. The standard for AI agents in finance is no longer a slogan, it is a registry you can read. The listings sit at @8004_scan. Anyone can verify what the agent is, what it claims to do, and what it has actually done.

Two. Surf on the Ethereum mainnet in days. The agent routes through Morpho V2 vaults, curated by Steakhouse Financial, Gauntlet, Apostro, MEV Capital and a handful of others. Three chains under one balance now: @base, @0xPolygon, and @ethereum. Same one-click deposit, same withdraw anytime, a bigger pool of places where the agent can place the saver's money. Ethereum is where the deepest stablecoin lending liquidity sits today and where institutional dollars already settle, which is why the rate-discovery process clears higher there.

Three. The SDK ships right after Ethereum. Two npm packages, @surfliquid/sdk and @surfliquid/widget. Any consumer fintech, any wallet, any card company, any neobank can embed a real savings rate in three lines of code. The integrator brands the surface. The saver keeps custody throughout. The audit posture is inherited. The rail used to be the moat for fifteen years of consumer banking. It is becoming a library.

Track record under all of this:

Nine months live on Base and Polygon.

• $107M routed lifetime.

• 6,757 on-chain agent actions.

• 231 wallets.

• Zero custody incidents.

Last week alone, the agent routed $289K across two vault flips. Gauntlet to Steakhouse on 11 May when the rate moved. Back to Gauntlet on 16 May when the spread reversed. 69 atomic batches between them. No human watched it happen. The on-chain trail is the receipt.

What I find interesting about this moment is the trade we are making. We are not chasing distribution to ten million Surf-branded users. We are publishing the infrastructure so that any consumer app, on any chain, can give its users the rate the bank could not. The brand stays small. The infrastructure compounds.

The infrastructure is the product. Building it in public. Shipping it in public.

https://t.co/Y7Ijii4qa4

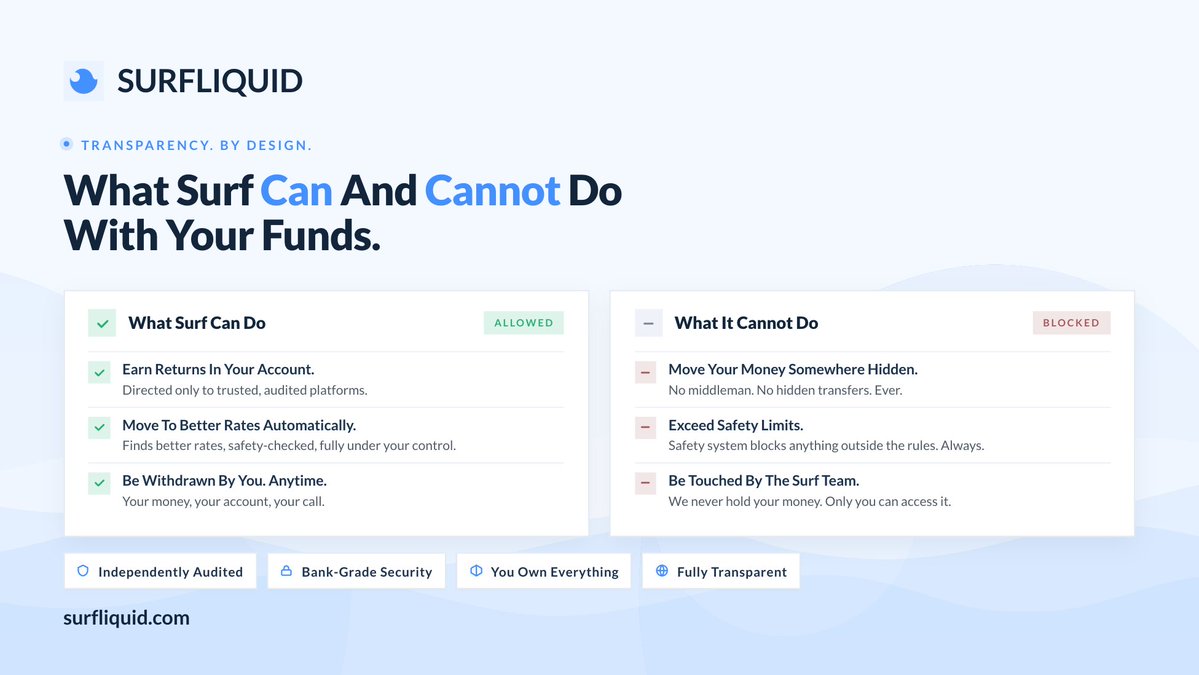

Your bank doesn't tell you where your money goes.

Surf does.

Open the app. See your money. See your earnings. See the safety rules. That's it.

https://t.co/76v5fBC5p0

Transparency is the whole moat.

Our dashboard shows users what their money is doing in plain numbers, on-chain, every block.

The fight to keep that visible is the fight to keep the savings premise honest.

Banking lobby is mad crypto is debating stablecoin yield publicly on X.

They sent 8000 letters trying to pressure senators because they hate transparency.

I'm done.

Every letter is a confirmation that letting savers earn fair returns scares them. The category is real because banks already know the alternative works.

The next few weeks will decide who picks up the spread.

🇺🇸 LATEST: Banking group members have flooded Senate offices with over 8,000 letters since last Friday urging lawmakers to fix the stablecoin yield compromise, per Eleanor Terrett.

Credit-grade tokenised rails, rated AAA, are the missing piece.

Once the underlying paper is of institutional quality, the consumer-savings layer is the next gap.

That is the layer we wake up thinking about every morning.

NEW: Moody's awards its top AAA rating to tokenized money market funds from @Fidelity and @BlackRock, validating the credit quality and liquidity of onchain yield products as the tokenized Treasury sector hits $15B in AUM.

@XenBH When the biggest payments and commerce companies in the world settle on the same chain, anything built on that chain inherits the trust.

Surf has been live on Base since launch. Users get a savings layer sitting on rails that JPMorgan and Visa already validated.

@stacy_muur Risk bucket framing matters.

Surf shows the bucket on the dashboard before any move. You see the trusted platform the money is routed to.

You see the rules that sit in front of every signature. You see the on-chain receipt.

https://t.co/76v5fBC5p0

@coinbureau Last-minute changes always reveal the real fight. The banking spread is what's at risk.

Once your dollars can earn on their own, the deposit model loses its quietest profit centre.

https://t.co/76v5fBC5p0

Multiples is the right scale to think in.

The next decade of consumer on-chain finance builds on existing tokenised assets.

The job is to put a savings-account interface over the rails so the user never has to think about it.

That is what we are building.

“...𝘵𝘩𝘦 𝘨𝘳𝘰𝘸𝘵𝘩 𝘰𝘱𝘱𝘰𝘳𝘵𝘶𝘯𝘪𝘵𝘺 𝘧𝘰𝘳 𝘵𝘩𝘦 𝘯𝘦𝘹𝘵 𝘴𝘦𝘷𝘦𝘳𝘢𝘭 𝘺𝘦𝘢𝘳𝘴 𝘪𝘴 𝘳𝘦𝘢𝘭𝘭𝘺 𝘵𝘰 𝘣𝘦 𝘵𝘩𝘪𝘯𝘬𝘪𝘯𝘨 𝘪𝘯 𝘮𝘶𝘭𝘵𝘪𝘱𝘭𝘦𝘴 𝘢𝘴 𝘰𝘱𝘱𝘰𝘴𝘦𝘥 𝘵𝘰 𝘱𝘦𝘳𝘤𝘦𝘯𝘵𝘢𝘨𝘦𝘴.”

Rob Goldstein from @BlackRock on why tokenization is still at the very beginning.

#BinanceOnline

Tokenised T-Bills as stablecoin reserves means a clear baseline on every dollar issued. The real question is who keeps the difference between that baseline and what the dollar earns once it's idle. Banks want both ends of the spread. We've spent a year building the rails to give the spread back to the holder.

Tokenised T-Bills as reserves means every dollar has a clear baseline.

Who keeps the yield once those dollars sit idle?

Banks want both ends of the spread.

We have spent a year building Surf to flip that. Yield to the holder, not the issuer.

Your bank pays you a fraction of a percent.

Surf shows you what your money can actually earn. One deposit. Clear returns. An app you can actually understand.

Better returns on your savings. Simple as that.

https://t.co/76v5fBC5p0

@CryptoTice_ The fight is bigger than CLARITY. Banks have run on the deposit spread for fifty years. The first product that lets a normal saver bypass that spread is the existential threat.

We're building one. Rails live regardless of the vote.

Most savings apps tell you to "trust them." We show you everything.

See where your money goes. See what it is earning. See the rules that protect it.

Your money. Your visibility. Full transparency.

https://t.co/76v5fBC5p0

@CryptoWendyO This is the part that matters. The spread the banks keep is the same spread that built every bank's earnings report for decades.

An on-chain savings account that pays the holder directly is what changes the math. We've been routing exactly this for eight months.

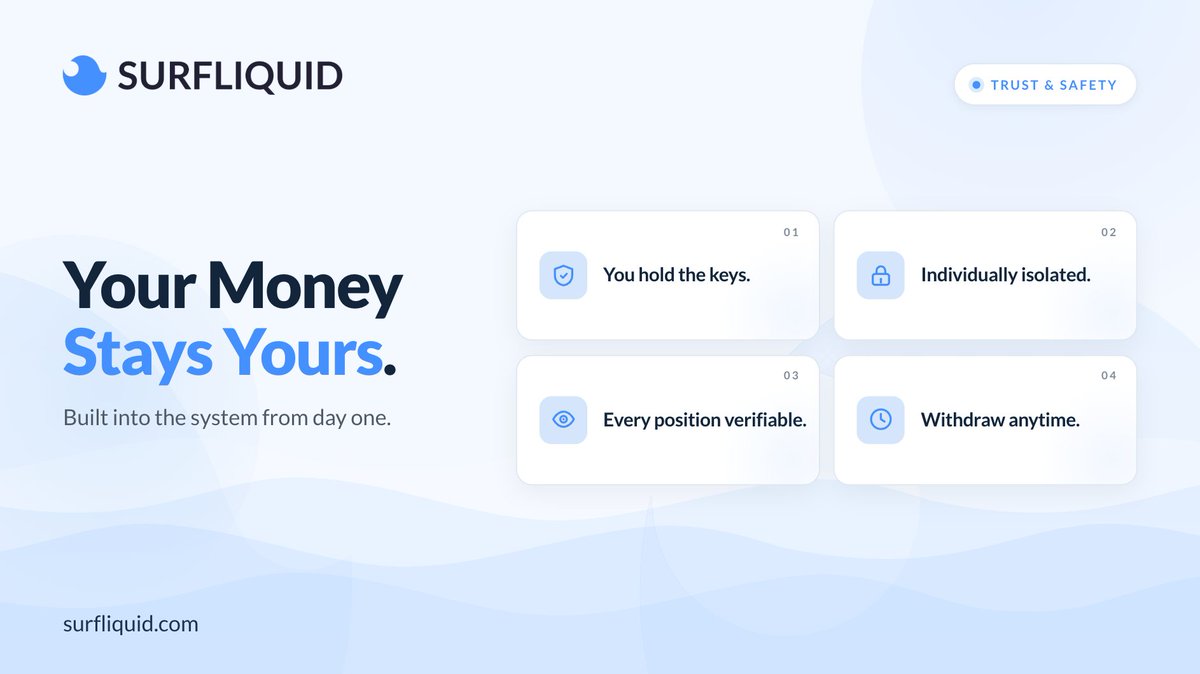

One of the most common questions we get: "How is this different from what happened with Celsius?"

Different model entirely.

You hold the keys. Your account is individually isolated. Withdraw anytime. Every position is verifiable and independently audited. The safety system enforces every rule automatically.

Your money stays yours. Built into the system from day one.

https://t.co/dEDBOc9zcR