Carvana $CVNA Bear Case: May be the worst stock I've ever analyzed.

Bullet Points:

1. Carvana’s profit margins are too good to be true. The best companies in the industry don’t come close to their 19% gross profit margins.

2. The CEO of Carvana (Ernest Garcia III) Also owns a privately owned auto business named Drivetime. Drivetime is a dumpster fire.

3. Ernest Garcia III has been funneling his unwanted Carvana inventory to Drivetime to prop up Carvana’s earnings. Drivetime overpays Carvana for this inventory and then takes the loss on their own balance sheets.

4. Over the last few months Ernest Garcia III has been selling tens of millions of dollars of stock to keep Drivetime afloat

5. Carvana has issued roughly 15.3 million shares over the last year. At average $330 price this comes to roughly 5 Billion USD. None of this reflects on the company’s financial report.

Thesis:

Based on CVNA October 2025 earnings report the company’s equity attributed to shareholders increased by 1B usd.

In the same period the company issued ~15.3 million shares worth over 5B usd. None of this issuance reflects on the company’s balance sheets. Healthy companies issue dividends and buy back stock. Carvana has no dividend and has issued billions in stock solely to their core insiders.

Drivetime (a company owned by Carvana’s CEO) has the worst inventory I have ever seen. Thousands and thousands of cars that are absolutely overpriced garbage. Some of the cars they have been sitting on for over 6 months.

In October and September of 2025 Ernest Garcia III has sold roughly 82 million dollars of carvana stock.

I am not a private investigator, financial pro, or accountant, but to me the evidence is compelling that carvana’s results are being directly propped by DRIVETIME and once the Garcias have enriched themselves the real results will emerge.

Now to mention the two Pump and Dump lawsuits they're facing from their own VC firms. They already went through a bubble burst before from $330 to $9

$CVNA is up to $450, one of the greatest come back stories ever and Wallstreet analysts keep pricing them higher🤯 . This may be the riskest play I've ever done but I may full port short $CVNA for the long-term after I'm done with my up swings on Figma and Netflix

Started a position in $RBRK at $51.

Cybersecurity isn’t optional anymore.

Every company runs on data now - and ransomware attacks are exploding. When systems go down, businesses can lose millions per day.

Rubrik focuses on cyber resilience: protecting data and helping companies recover fast after attacks.

The growth is real:

• Subscription ARR: $1.35B (+34% YoY)

• Revenue growth: ~48% YoY

• Net retention >120%

Despite that, the stock is still ~40% below its $103 high.

My trade:

Entry: $51

Stop: $46

Target: $75–90

Cyber attacks aren’t slowing down.

The companies that protect the data will win.

Stop believing these fake financial gurus, they're using the withdrawal glitch "$5k to 200k" "5k to 2m"🤡 Look how when I withdraw my 50k a $CVNA short it goes from "30k to 100k 169% gain" to "5k to 50k 1,507% gain"

@Remzztrades@RJCcapital Stop believing these fake financial gurus, they're using the withdrawal glitch "$5k to 200k" "5k to 2m"🤡 Look how when I withdraw my 50k a $CVNA short it goes from "30k to 100k 169% gain" to "5k to 50k 1,507% gain"

On the moneymaking side, I think $NFLX has incredible value right now near it's 52 week low: Bullet points:

Netflix is being priced like a mature media company while throwing off $7–8B in free cash flow and marching toward ~$9B+ in owner earnings as content spend normalizes.

At around the mid‑$90s reference level you’re paying roughly 26.5x “earnings power” for a business growing revenue 6–7% with rising margins and dominant streaming economics.

Its moat is built on scale (302M subs), sticky brand, data‑driven content, and best‑in‑class tech, making it the only profitable pure‑play streamer while rivals like Disney+ and Max still bleed.

Real growth from here is global: another ~150M subs over the next decade, mostly from APAC and LATAM, plus ARPU/pricing and ads layered on top.

WB deal might dip it now or near future (don't know, not predicting), but long-term they gain huge after grabbing the biggest cinema franchises ever like DC, Harry Potter, LOTR.

Thesis: At $90 you're buying a cash machine at 26.5x earnings power growing forever, incredibly undervalued vs media comps. Plus with Netflix paying the WB deal in cash, it's more certainty for WB shareholders and a more likely chance the deal will go through and even if it doesn't, there's a good chance Netflix not spending money would make the stock go up. Smart play could be to wait post-earnings Jan 20 for potential dip and gain more certainty, but at current price I'm starting a position cause I think it's a steal. Not advice - DYOR.

My take? I did it.

I went $35k to $10M in 21 months (286x) going all in 1 stock at a time - no options, no margin, no crypto. And shared every trade live on Reddit as "Sir Jack".

Concentration makes wealth. Period.

Most people want to make life-changing money, not 7%.

They also need simplicity.

People are dumb.

Swing trading 1 stock at a time focuses research, concentrates gains, and avoids getting rugged.

It's the best way to get started actively trading.

I full endorse it.

(also the fund manager stat is stupid af bc it's much different trading your $1000 vs millions in AUM)

I think $NFLX has incredible value right now near it's 52 week low:

Bullet points:

* Netflix is being priced like a mature media company while throwing off $7–8B in free cash flow and marching toward ~$9B+ in owner earnings as content spend normalizes.

* At around the mid‑$90s reference level you’re paying roughly 26.5x “earnings power” for a business growing revenue 6–7% with rising margins and dominant streaming economics.

* Its moat is built on scale (302M subs), sticky brand, data‑driven content, and best‑in‑class tech, making it the only profitable pure‑play streamer while rivals like Disney+ and Max still bleed.

* Real growth from here is global: another ~150M subs over the next decade, mostly from APAC and LATAM, plus ARPU/pricing and ads layered on top.

* WB deal might dip it now or near future (don't know, not predicting), but long-term they gain huge after grabbing the biggest cinema franchises ever like DC, Harry Potter, LOTR.

Thesis: At $90 you're buying a cash machine at 26.5x earnings power growing forever, incredibly undervalued vs media comps. Plus with Netflix paying the WB deal in cash, it's more certainty for WB shareholders and a more likely chance the deal will go through and even if it doesn't, there's a good chance Netflix not spending money would make the stock go up. Smart play could be to wait post-earnings Jan 20 for potential dip and gain more certainty, but at current price I'm starting a position cause I think it's a steal. Not advice - DYOR.

If y'all smart, you should buy $NFLX and hold for 5 years, it's at it's 52 week low and is absolutely one of the best stocks in the future with the WB deal granting them Lord of the rings, DC, Harry Potter, Breaking Bad, and Game of Thrones

Ok so here’s how I’m seeing it. Everyone’s focused on $NVDA, $AMD, $INTC, but they’re just one piece of the whole puzzle. Here’s how I see it: AI needs constant computational and electrical power. Not just for the data centers and the fabs that make the chips, but the chips themselves burn power 24/7. The more models scale, the more energy they eat. That power has to come from somewhere. Big tech ceos are already talking about potential future power shortages if we dont come up with something better than what we have rn So here’s how I’m thinking about it: We started with AI companies throwing money at chip companies → chip companies throwing money at fabs like $TSMC → fabs and AI centers pulling insane amounts of power off the grid → and now we’re about to see power companies (especially nuclear) get flooded with cash → and that means the uranium miners feeding those reactors are next in line. This is how i see the chain: AI companies → $NVDA / $AMD / $INTC → $TSMC / Samsung → SMRs like $Oklo / $SMR / TerraPower → uranium miners like $BWXT/ $UUUU / $LEU / $CCJ. Every stage up the chain got paid. The last ones left to run are nuclear and uranium. I think we’re about to see a repeat of the same pattern within the next few years as we experience energy shortage. Just like how $NVDA and $AMD dominated chips, I think a couple players will dominate nuclear. Right now we’ve got:

$Oklo (backed by Sam Altman and Meta, ~$16.46B)

NuScale / $SMR (~$6.2B)

TerraPower (still private but Gates-backed and getting a ton of attention) That’s probably the big 3. Others will show up, but like everything else, a couple names are going to take 80% of the market and leave everyone else behind. Same goes for uranium. $CCJ is the king, but $BWXT, $LEU, and $UUUU are getting attention. Supply is tight, and if nuclear demand explodes, miners get squeezed upward just like GPU demand squeezed $NVDA. So yeah, are $Oklo / $SMR / TerraPower are the next $NVDA / $AMD / $INTC just further up the chain? The ones getting paid by the ones getting paid. It’s the last piece of the AI/infrastructure puzzle that hasn’t run yet.

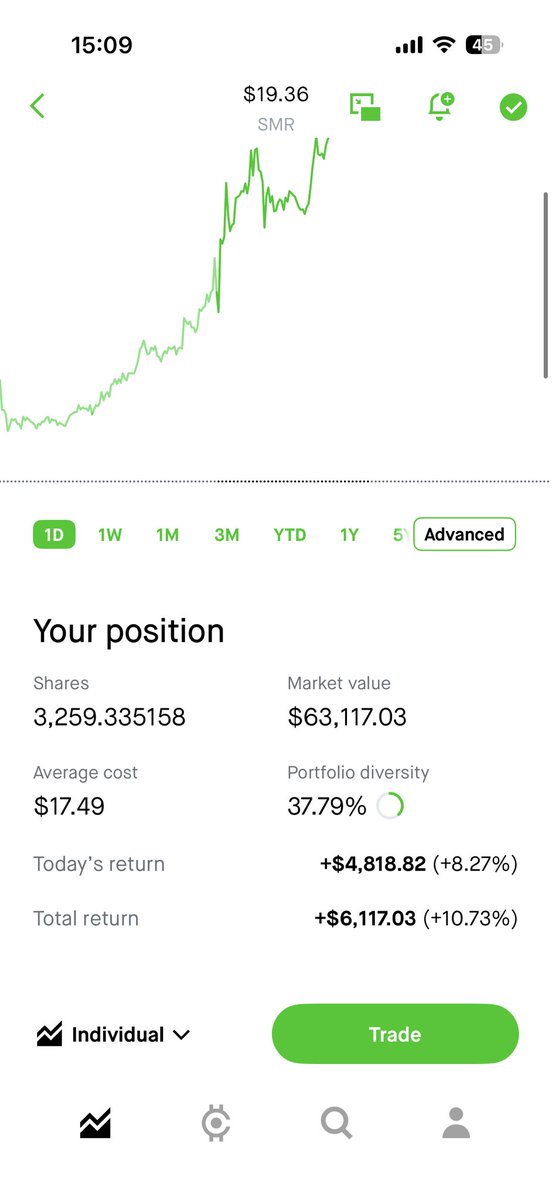

Game plan is to hold $SMR $OKLO into Discord IPO, while shorting Carvana. Also starting a $FIG position too just for fun cause it’s in a prime spot to bounce